Powering the world’s biggest decisions. 7K enterprises trust our AI and market intelligence platform to deliver timely insights. (Not investment advice)

Joined September 2013

- Tweets 20,626

- Following 509

- Followers 34,409

- Likes 2,143

Photos and videos

Pinned Tweet

Jun 3

What does market conviction look like? A $350M raise at a $7.5B valuation.

Today, we have closed that $350M round and nearly doubled our valuation, all backed by Vitruvian Partners, Accenture Ventures, J.P. Morgan Growth Equity Partners, D. E. Shaw Ventures, Pinegrove Opportunity Partners, and our returning investors @CapitalG, @GoldmanSachs Alternatives, and Viking Global Investors.

Doubling down on their investment, we have also established a new channel partnership with Accenture to further fuel organizations embedding and scaling market intelligence into their core agentic workflows.

The era of fragmented tools in market intelligence has given way to a more integrated approach with the advent of AI and that's why we are also announcing the launch of SuperAnalyst. AI prompts and queries are the workflow most analysts know today but now multi-step research and monitoring tasks can be automated on the user's behalf.

These announcements are more than just momentous milestones: they are an inflection point for the future of market intelligence. We couldn't be more excited to keep building it.

alpha-sense.com/press/alphas…

6

12

31

18,253

Jun 12

📈 Today, $SPCX crossed $2 trillion in market cap on day one of trading.

For investors, the story spans rocket economics, satellite connectivity, and AI infrastructure at an unprecedented scale.

Here is what you need to know, generated from our IPO Primer agent in AlphaSense.

4

12

2,195

Jun 12

Interview with an industry expert on why $META's distribution advantage matters more than its model quality in the AI race ( $AMZN, $GOOGL ):

- The expert sees $META's models as still being behind the top frontier providers, such as OpenAI and Anthropic. Where $META holds a genuine advantage is distribution, with billions of monthly active users across Facebook, Instagram, and WhatsApp giving it a reach that no other AI company can match. The expert sees $META's strategy as less about winning the model race outright and more about integrating AI deeply into products that already have massive global adoption.

- The expert uses Gemini Flash for user-facing applications where latency and cost matter more than raw intelligence, and Claude Opus for coding tasks, which the expert considers the best model for that use case. The coding agent itself is highlighted as equally important as the underlying model, with $GOOGL's Antigravity agent paired with Claude Opus being the current setup of choice.

- According to the expert, the jump in intelligence between new model releases has become noticeably smaller over time, with the excitement around each new launch fading compared to a few years ago. He believes that tuning and prompting within a specific use case often delivers more value than upgrading to a newer model, and that for latency-sensitive applications with less cognitively demanding tasks, a cheaper and faster model is preferable over a smarter one.

- Cost is also a real factor in model selection, with Claude models being credit-based and more expensive, meaning the expert will switch to Gemini 3.1 Pro when credits run out, accepting slightly lower performance in exchange for the cost savings.

- The expert does not see $META playing a major role in the on-device or local deployment space with its newest Muse Spark model, since it is closed source and only accessible via API, making it incompatible with use cases like running models on a Mac mini. $META still has Llama for open source use, but the expert sees the company pivoting away from that and toward its closed source model.

- The expert sees two underrated elements of $META's AI strategy. The first is hardware, with the Ray-Ban smart glasses seen as underrated product that is gaining real traction and represents a unique channel for AI that none of the major foundation model players such as OpenAI or Anthropic are positioned to compete in. The second is distribution, with $META's billions of existing users across its consumer apps giving it an immediate reach advantage.

4

9

132

17,105

Jun 12

If you are interested in more interviews like this one, make sure to follow us!

Stop second-guessing. Whether you're tracking market shifts, exploring new opportunities, or need clarity on complex decisions, our extensive transcript library and custom expert calls give you the competitive edge you need.

⬇️

alpha-sense.com/trial-reques…

1,555

Jun 12

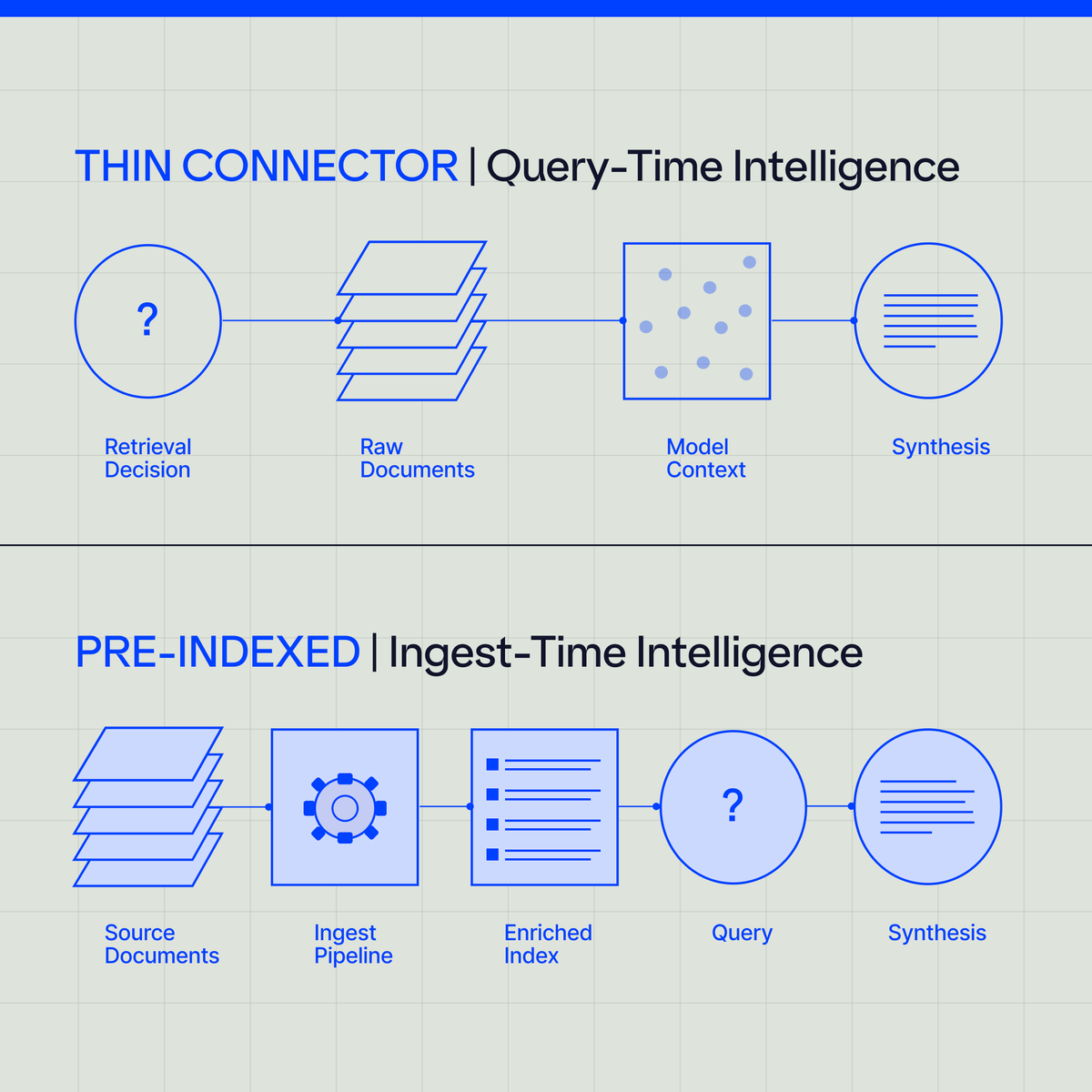

MCP is a transport protocol, not a retrieval architecture, and confusing the two will lead to enterprise AI that quietly underperforms.

Thin connectors work well for live structured data, but they hit structural limits on high-stakes research, where document depth, recall, and grounding decide whether the answer is signal or noise.

@cackerso, SVP of Product at AlphaSense, breaks down where MCP shines, where it falls short, and what to actually evaluate in your AI stack. Read the full article here: alpha-sense.com/resources/pr…

10

1,917

Jun 12

AlphaSense experts say SpaceX's primary competitive advantage stems from its mastery of reusability, which has fundamentally shifted the economics of the entire space industry.

SpaceX begins trading today under the ticker $SPCX

5

8

2,198

Jun 11

$RH CEO Gary Friedman says furniture is the least digitized business with 80% done in stores and at the luxury level it is 95% in stores. He thinks paying influencers to talk about their goods is massively inauthentic and they know nothing about the product. On a three year basis RH has outperformed everybody. He says wait till the other side of this cycle and they are going to have a cash generation machine that this industry has never seen.

"I don't know. They've been doing that for the last three years and we've outperformed all of them. So, I think when you say, we're mailing a book and expecting people to come, we built the best, the greatest physical platform on the planet earth for our kind of products. So don't overlook the physical platform.

And Michael, if you look at that video I did last quarter, I outlined that, furniture is the least digitized business. 80% done in stores, it's 20% done online. At the luxury level, it's 95%/5%. So, this is a business you need to see touch fit in, comfort scale, all those kind of things. So the book is just, it's a small way we use it to integrate the whole thing. People look forward to getting our books. It's a physical thing. It's still. We have a digital book too, but we just don't, I'm just not a believer in following the trends of a lot of people that are following other people.

We just think it's massively inauthentic to pay some stranger to, some influencer to go talk about our goods. And they don't know nothing about us. They know nothing about the product. They're not an expert in the field. And I think that's a lot of noise. Maybe it's good for, building beauty brands to teenagers or, other stuff like that. It doesn't affect what I buy, and I have a lot of homes. And so I don't think it affects our customer or we wouldn't be the biggest brand of our kind.

We wouldn't have outperformed everybody, even if you look at this last quarter we had and if you look at us at over a two year basis or three year basis, over a two year basis, only West Elm has performed as well as us on a three year basis. We're better than everybody. And West Elm just had a great quarter and I think they're doing a great job.

But if you look at anybody buying furniture, I tell people, when you go out there, bang pots and pans and try to get attention, doing inauthentic things, you're just creating noise. You're creating your own noise, and you wind up, chasing things and thinking that they're relevant when they're not, and, we've tried and tested different things and we have a lot of data behind what we've done and why we're doing what we do.

And nobody thought we were smart to build the stores. We did and the galleries we did and those turned out pretty well. And everybody stopped mailing books and we're still mailing books. The only difference right now, in a point in time, you can put our model against anybody. Put it against today's very best customer. Back out our investments in international expansion, back out our investment in building Estates, which is not like some little introduction of a 80 page book that five or seven years later you wind up with one store. We're making serious investments to build a platform unlike anybody else. And

so on a down market like this, Is our model not going to look as good? Yeah, Okay. But you're looking at people that aren't even investing. They're not building anything. They're trying to be great cost controllers, So yeah, just wait till the other side of this cycle for us and and I think we're going to have a cash generation machine that this industry has never seen."

10

2,458

Jun 11

$ADBE CEO Shantanu Narayen says no other company is as well positioned across models, products, and interfaces to take advantage of the AI creativity opportunity. He compares it to what happened with code across AI, which completely turned upside down, and the same opportunity exists in every category from gaming to entertainment to creativity. The creative business is extremely stable and the line optimization deferral is not going away. Half of the ARR impact is from deferring the creative Pro line optimizations and the other half is from going full steam on delivering the freemium experience.

"I think if we really look at it, we just look at what's happening with the AI opportunity for creativity as this incredible opportunity that is upon us right now. And no other company is as well positioned, given what we have across our models, across our products and across our interfaces, to take advantage of it. So this is really about saying what we have done as it relates to capturing MAU with Acrobat and Express what we've done with respect to Firefly the entire creative market. Sometimes I like to also characterize this much like what's happened with the code opportunity.

If you think about what's happened with the code opportunity across AI, it's just completely been turned upside down and every company is thinking about how they can add to all of the billions that are already spent in code. The same opportunity exists, I think, in every single category, whether that's gaming, entertainment and creativity. And this is an opportunity for us not just to focus on creative pros and communicators who've traditionally been the strength of this company, but to actually become that AI platform for all creativity across every single surface. The success that we've seen associated with what we have done on these new products, we talked about the MAU, we've talked about the ARR that's coming. We want to just have a singular focus right now to make sure that we go capture that immense opportunity with a singular focus and a clear marketing message.

It also is based on a complete confidence that we have that the creative business is extremely stable. The amount of innovation that we have delivered in that space continues to make us a category of one as it relates to our focus on that particular market. And so that one we can defer. It's not going away but, anything that comes in the way of the company aligning and the market understanding that we're going to go after that entire creative opportunity right now, I think will detract from what is the real prize for this company. So hopefully that gives you some color. And I think in terms of the impact on ARR, you can think of it as maybe half of the impact of ARR is as a result of what we are doing around deferring that creative Pro line optimizations, and the other half is about going full steam on what it takes to deliver the freemium experience."

5

14

123

15,145

Jun 11

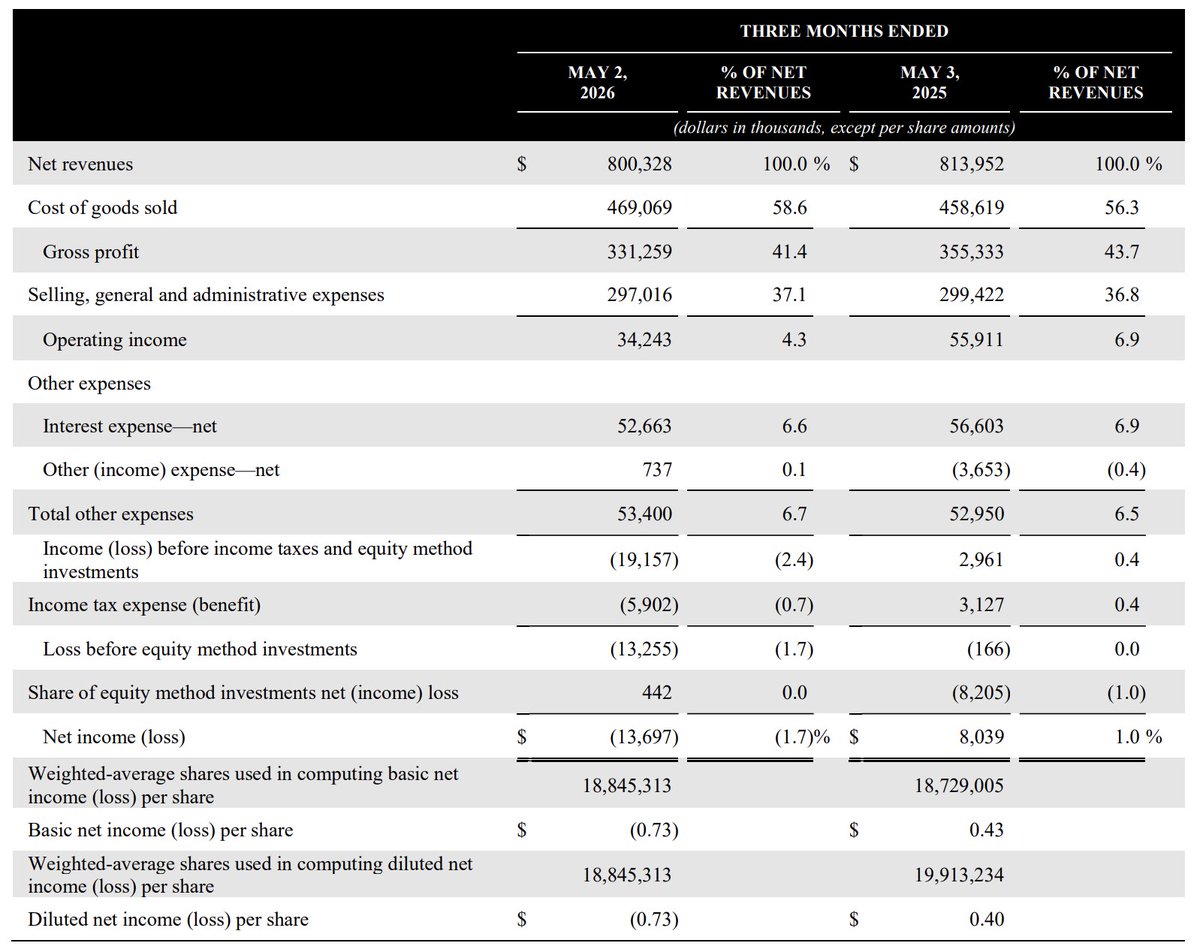

$RH Earnings:

- GAAP Net Revenues Decreased 1.7% to $800.3M

- GAAP Net Loss of $13.7M

- EBITDA of $71.8M and EBITDA Margin of 9.0%

- Adjusted EBITDA of $56.9M and Adjusted EBITDA Margin of 7.1%

- Free Cash Flow of $13.3M

"The Company’s First Quarter net revenues were negatively impacted by approximately $45 million due to higher backorder and special order balances that were approximately $75 million higher than the same period a year ago, primarily as a result of tariff related resourcing. The Company expects a similar elevated balance in Q2, with balances returning to normalized levels by the end of 2026, resulting in a revenue pick up of approximately $75 million in the second half of this year."

5

1,987

Jun 11

$ADBE Earnings:

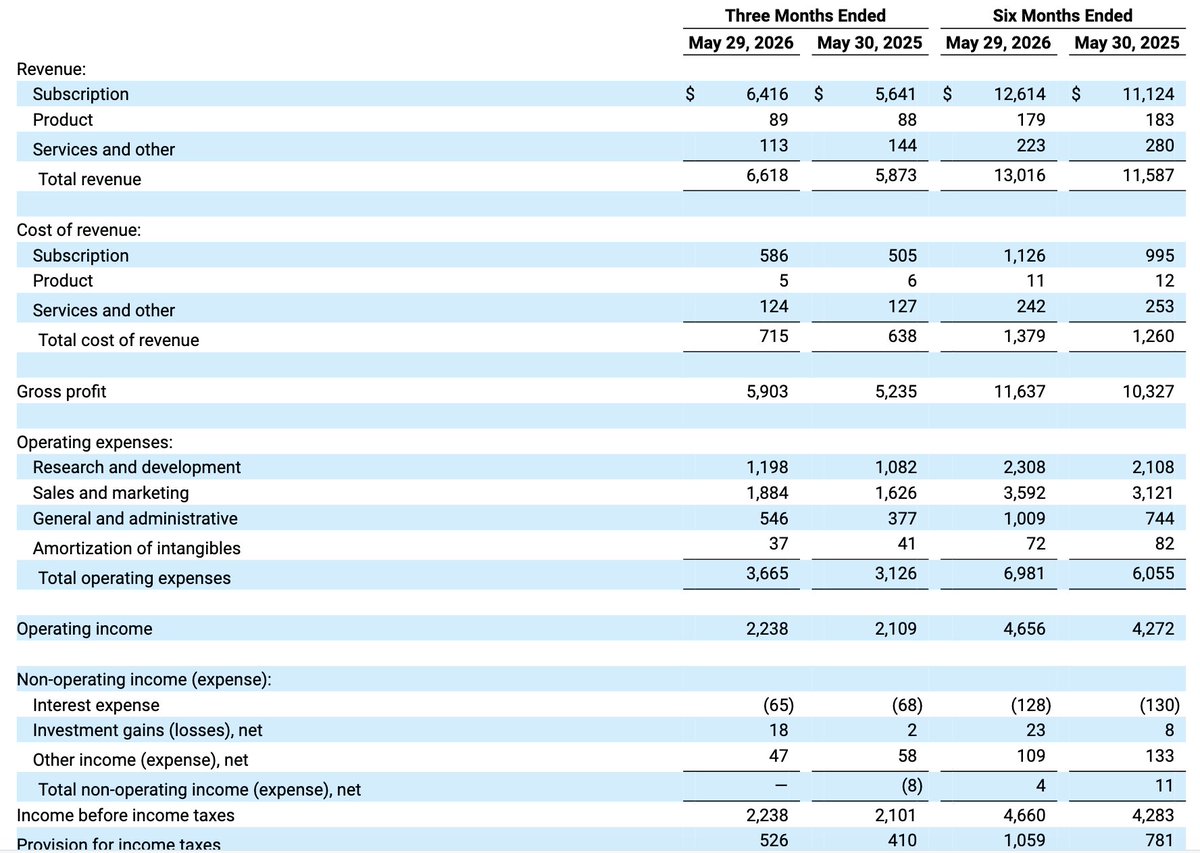

- Adobe achieved record revenue of $6.62 billion in its second quarter of FY2026, which represents 13% year-over-year growth, or 11% in constant currency.

- Diluted earnings per share was $4.25 on a GAAP basis and $5.96 on a non-GAAP basis. GAAP results reflect a $0.17 per share non-cash goodwill impairment charge related to the Publishing & Advertising reporting unit.

- Total Adobe Annualized Recurring Revenue (“ARR”) exiting the quarter was $27.10 billion, including approximately $480 million from Semrush.

- GAAP operating income in the second quarter was $2.24 billion and non-GAAP operating income was $2.95 billion. GAAP net income was $1.71 billion and non-GAAP net income was $2.40 billion.

“Adobe delivered record revenue of $6.62 billion in Q2 reflecting strong AI-driven demand across our customer groups and we are raising our full-year fiscal 2026 revenue and non-GAAP EPS targets on the strength of that performance,” said Shantanu Narayen, chair and CEO, Adobe. “We are inspired to bring the magic of our new AI products to consumers, business professionals, creators, and marketers to deliver on our mission to Empower Everyone to Create.”

Dan Durn, executive vice president and CFO of Adobe, is departing the company on June 15, 2026 to pursue a new professional opportunity. Steve Day, SVP of Corporate Finance and CFO of Adobe’s Customer Experience Orchestration Business Unit, will serve as interim Chief Financial Officer, effective June 15, 2026. Mr. Day brings 20 years of financial leadership experience at Adobe to the Interim Chief Financial Officer role. Day will report directly to CEO and Chair Shantanu Narayen.

“I want to thank Dan for leading the finance organization that will support Adobe's next chapter of growth in the AI era, and wish him all the best,” said Narayen. “Steve has been a key member of our finance organization for two decades, and his deep understanding of Adobe’s business will be critical as we execute our strategy to deliver AI innovations to a broader set of customers across creativity, productivity and customer experience orchestration.”

research.alpha-sense.com?doc…

6

33

6,970

Jun 11

SpaceX IPO is set for tomorrow. Here is a quick IPO Primer:

100% primary offering, no selling shareholders, Elon Musk on a 366-day lock-up period with no early release.

- Starlink revenue at $11.4B in 2025, up 50% YoY, with $4.4B in operating income

- AI segment recorded a $6.4B operating loss in 2025 from data center buildouts and GPU procurement

- Google contract committing $920M monthly for 110,000 NVIDIA GPUs validates near-term AI revenue

- Total capex surged 86% to $20.7B in 2025, with AI infrastructure alone consuming $12.7B

The control structure: Class B shares give Musk 84.4% of voting power post-IPO. SpaceX is classified as a controlled company, exempt from standard governance requirements.

The valuation: $135/share puts SpaceX at 31x 2027E revenue and 77x EV/EBITDA. Legacy telecom trades at 2x revenue. Terrestrial AI infrastructure trades at 14x.

The execution risk: Starship is the unlock for next-gen Starlink satellites and orbital AI compute. The program still faces developmental setbacks, FAA regulatory constraints, and unproven reusability economics.

3

8

32

3,472

Jun 11

Deal teams spend more time managing documents than analyzing them. That has to change.

Now, through the only VDRPro connector that brings confidential data room materials alongside premium market intelligence in one governed, AI-powered environment, you can get to conviction faster.

AlphaSense and SS&C @Intralinks built this native integration together for deal teams who can't afford to work from incomplete context. See how it works: alpha-sense.com/resources/pr…

1

8

1,881

Jun 10

$ORCL CEO Clay Magouyrk says there is still massively higher demand than supply several years in, and there are going to be more and more people trying to figure out how to meet that demand. When things come back for renewal they are instantly snapped up, which is an indicator of great customer relationships. Over time as Oracle deploys more research and development dollars into making things more efficient, he sees ways Oracle gets higher and higher margins while offering lower and lower prices to customers.

"I think that it's very important that we stay focused on customers. So the nice thing is that I think whether you see it from existing RPO or increased contracts that we're getting, yes, there's a lot of things happening in the market, but we have a large, diverse set of customers, both very large and also smaller customers.

And what I spend all of my time doing is I wake up every day and I go, how do I make sure those customers are as happy as possible with us? And that's, when I shared the numbers, for example, in the prepared remarks about the extremely high utilization rate, even when things come back for renewal, they're instantly snapped up. Those are all indicators that we have great customer relationships. They're happy with the products and they're very satisfied with the prices that we're charging for them.

But I think there's going to be a lot of people who enter the space I think there's clearly, several years in, there's still a massively higher demand than there is supply. And so I think There are going to be more and more people trying to figure out how to meet that demand. But I don't worry about that. I really focus on how do we make sure that we can meet as much of that demand at a reasonable margin profile. And that's what I think.

You've seen us invent new business models to go out and try to serve. In terms of how does that affect our future renewals? I find that largely what affects future renewals is the several years relationship that we're going to have between now and then. And

we're fundamentally in the service business. It's one thing if you think that you're just buying something and then you're done with it, it's not the way it works. These people are relying on what we do at Oracle to run and maintain these massive clusters every day. And our ability to do that extremely well creates an extremely positive relationship that then ensures that renewals go well.

And then in terms of the margin profile. Look, I've been at Oracle now for 12 years. The whole time I've been working on OCI. What I can tell you, it's not easy to build an extremely efficient, highly secure, robust cloud. So I think that our customers see and appreciate the value of what we provide, the flexibility that we give them, the comprehensive set of services that we provide.

So I think that over time, as the market continues to mature and we deploy more and more of our research and development dollars into making things more efficient. I think there's ways that Oracle gets higher and higher margins, but we actually can offer lower and lower prices to our customers. That's ultimately the job that is on our shoulders and what we've been doing over the past decade and it's why the biggest and most robust customers come our way."

1

7

67

7,874

Jun 10

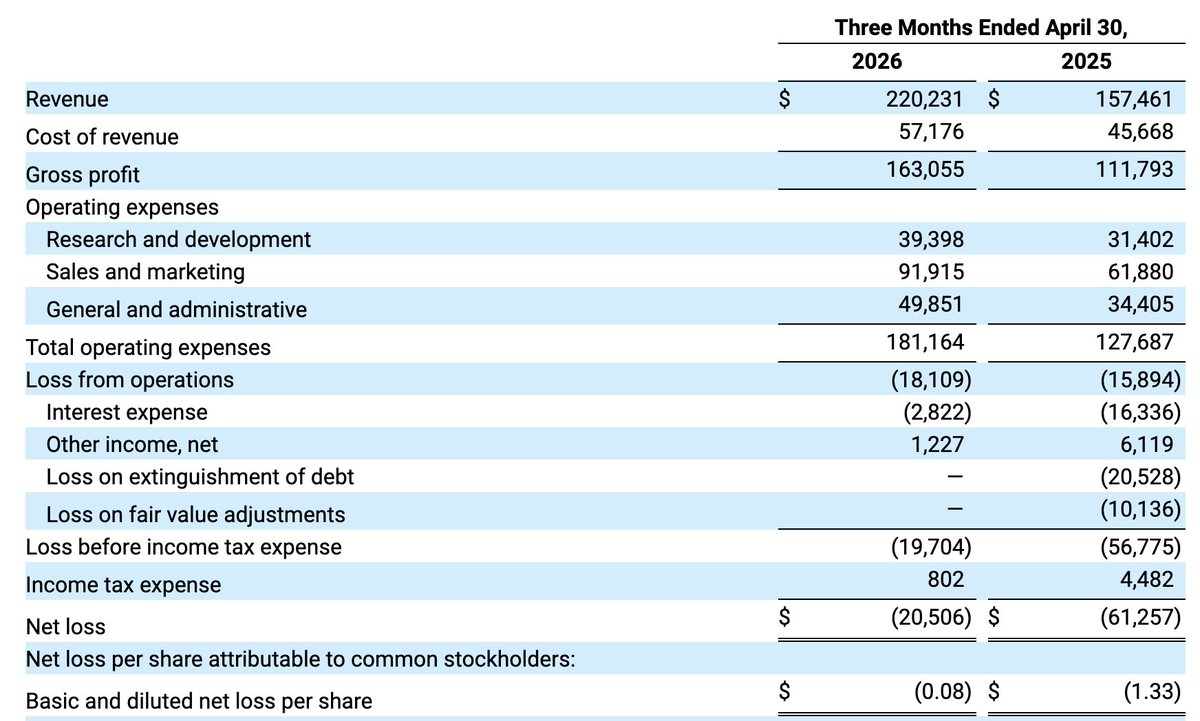

$NAVN Earnings:

- Total Revenue was $220 million, an increase of 40% year-over-year

- GAAP gross profit reached $163 million, representing 74% gross margin, compared to $112 million, or 71% gross margin in the first quarter of fiscal year 2026

- Non-GAAP income from operations was $24 million, compared to non-GAAP income from operations of $3 million in the first quarter of fiscal year 2026; non-GAAP operating margin was 11%, compared to 2% in the first quarter of fiscal year 2026

- Non-GAAP net income was $22 million, compared to a non-GAAP net loss of $7 million in the first quarter of fiscal year 2026

“Navan kicked off fiscal 2027 with an outstanding first quarter, driven by accelerating growth across the business and a 50% year-over-year increase in Gross Booking Volume," said Ariel Cohen, Navan co-founder and CEO. "Our strong performance and continued enterprise momentum give us the confidence to raise our guidance for the fiscal year. We are executing exceptionally well and leveraging our proprietary, AI-led platform to deliver an unmatched customer experience at scale, seamlessly orchestrating human and AI agents. We are not just building the best travel agency on the planet; we are working to define the future of travel.”

“Navan delivered an exceptional first quarter, highlighted by revenue growth of 40% year-over-year, and GBV growth of 50% year-over-year, surpassing the $3 billion milestone,” said Aurélien Nolf, Navan CFO. “The strength was driven by very resilient on-platform booking activity, strong new-customer ramps, and rapidly expanding payments volume. This growth enabled us to deliver meaningful gross and operating margin expansion, underscoring the leverage potential in our business as we scale. With a strong balance sheet and accelerating momentum across the business, we are raising both our FY’27 revenue and non-GAAP operating profit outlook.”

research.alpha-sense.com?doc…

1

4

1,893

Jun 10

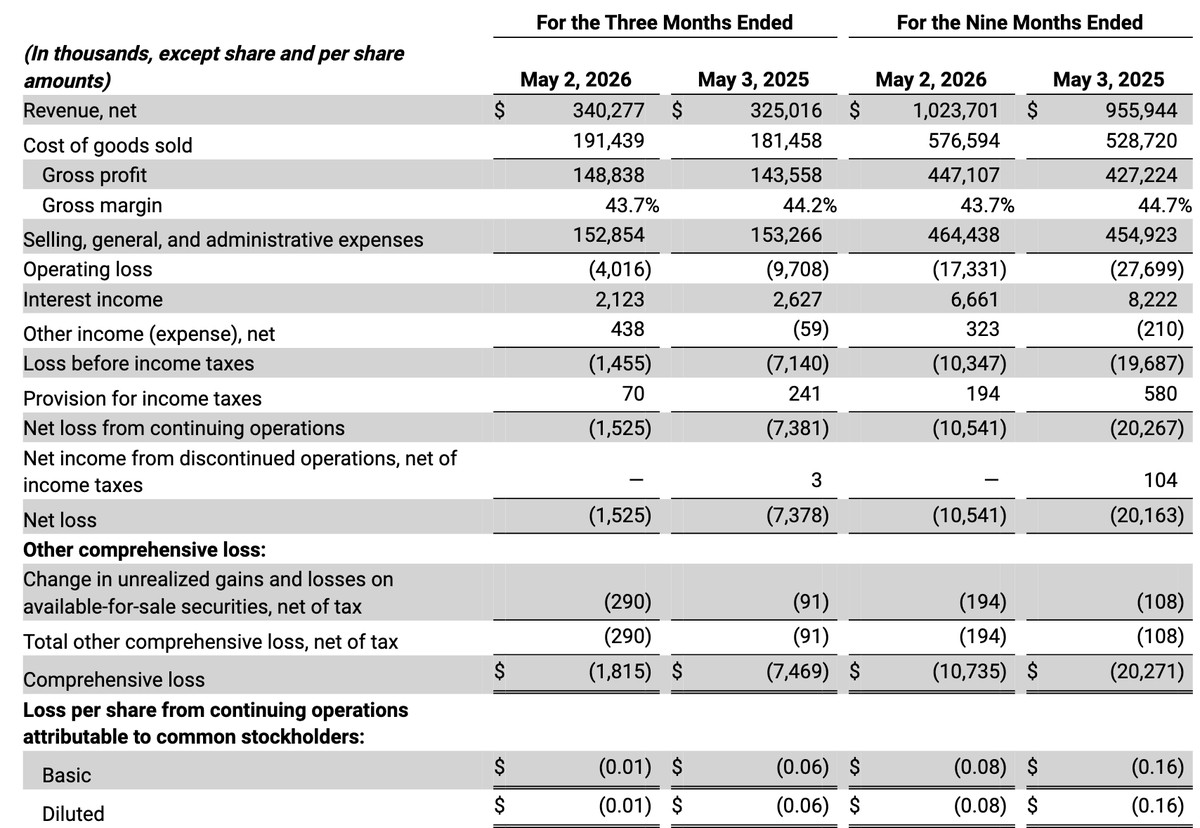

$SFIX Earnings:

- Net revenue of $340.3 million, an increase of 4.7% year-over-year.

- Active clients of 2.309 million, an increase of 0.9% quarter-over-quarter and a decrease of 1.9% year-over-year.

- Net revenue per active client of $578, an increase of 6.6% year-over-year.

- Gross margin of 43.7%, a decrease of 50 basis points year-over-year.

- Net loss of $1.5 million and net loss margin of 0.4%; diluted loss per share of $0.01.

- Adjusted EBITDA of $13.2 million and Adjusted EBITDA margin of 3.9%.

“In Q3, we delivered another strong quarter, reporting our fifth consecutive quarter of year-over-year revenue growth on an adjusted basis, with both revenue and adjusted EBITDA exceeding our expectations,” said Matt Baer, CEO, Stitch Fix. “We also hit a significant milestone with sequential growth in active clients. These results reflect our team’s consistent execution of our strategy and underscore that the improvements we’ve made to our client experience and assortment are resonating. We remain confident that our disciplined approach will enable us to continue to strengthen our position as our clients’ retailer of choice for apparel, footwear and accessories, as well as navigate today’s dynamic consumer environment.”

research.alpha-sense.com?doc…

4

1,697

Jun 10

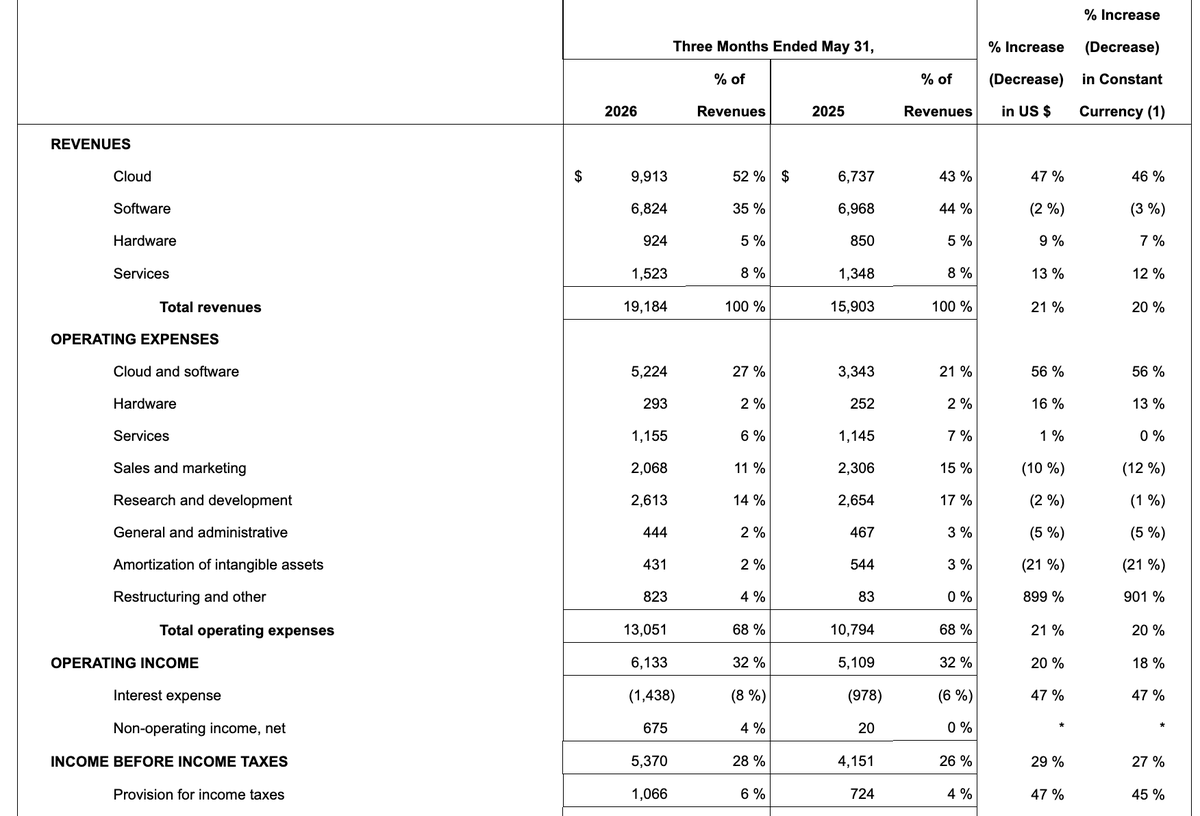

$ORCL Earnings:

- Record Q4 Total Revenues $19.2 billion, up 21% USD, and up 20% constant currency

- Record Q4 Earnings per Share GAAP up 21% USD to $1.45, non-GAAP up 24% USD to $2.111

- Record Remaining Performance Obligations grew $85 billion in Q4 from $553 billion to $638 billion

- Record Q4 Total Cloud Revenues $9.9 billion, up 47% USD, and up 46% constant currency

- Q4 Cloud Infra (IaaS) Revenue $5.8 billion, up 93% USD, and up 92% constant currency

- Q4 Cloud Apps (SaaS) Revenue $4.1 billion, up 10% USD, and up 9% constant currency

"The large increases in Oracle's RPO and revenue are driven by the growing demand for cloud infrastructure for AI training and inferencing. Oracle is building datacenters that are intended to use clean energy from natural gas fuel cells to generate electricity with minimal emissions. Other innovations in the areas of high-performance networking, advanced security and autonomous software have made Oracle the world's fastest growing provider of cloud datacenters.

Our database and applications businesses are both benefiting from Oracle's early adoption of AI. The Oracle Multicloud AI Database grew 404% in Q4—making it our fastest growing business ever. The Oracle Health application suite will soon include a completely new AI version of the Cerner hospital and clinic patient care management system. We expect this new AI patient care management system to push the growth rate of the overall Oracle Health business to double-digits in fiscal year 2027. And this is just the beginning of the expansion of the Oracle Health business.

We believe AI is about to completely revolutionize healthcare. Improvements in patient care are expected to yield much better patient outcomes, while dramatically lowering the cost of healthcare throughout the world. Oracle Health AI systems will allow doctors to spend less time with computers and more time with patients. AI molecular design models are expected to enable researchers to accelerate the development of life-saving drugs. Oracle's new AI clinical trial system is designed to enable regulators to rapidly review and approve clinical trial test results enabling patients to get access to new drugs sooner. AI will make healthcare better, more accessible, and less expensive."

research.alpha-sense.com?doc…

1

8

26

4,069

Jun 10

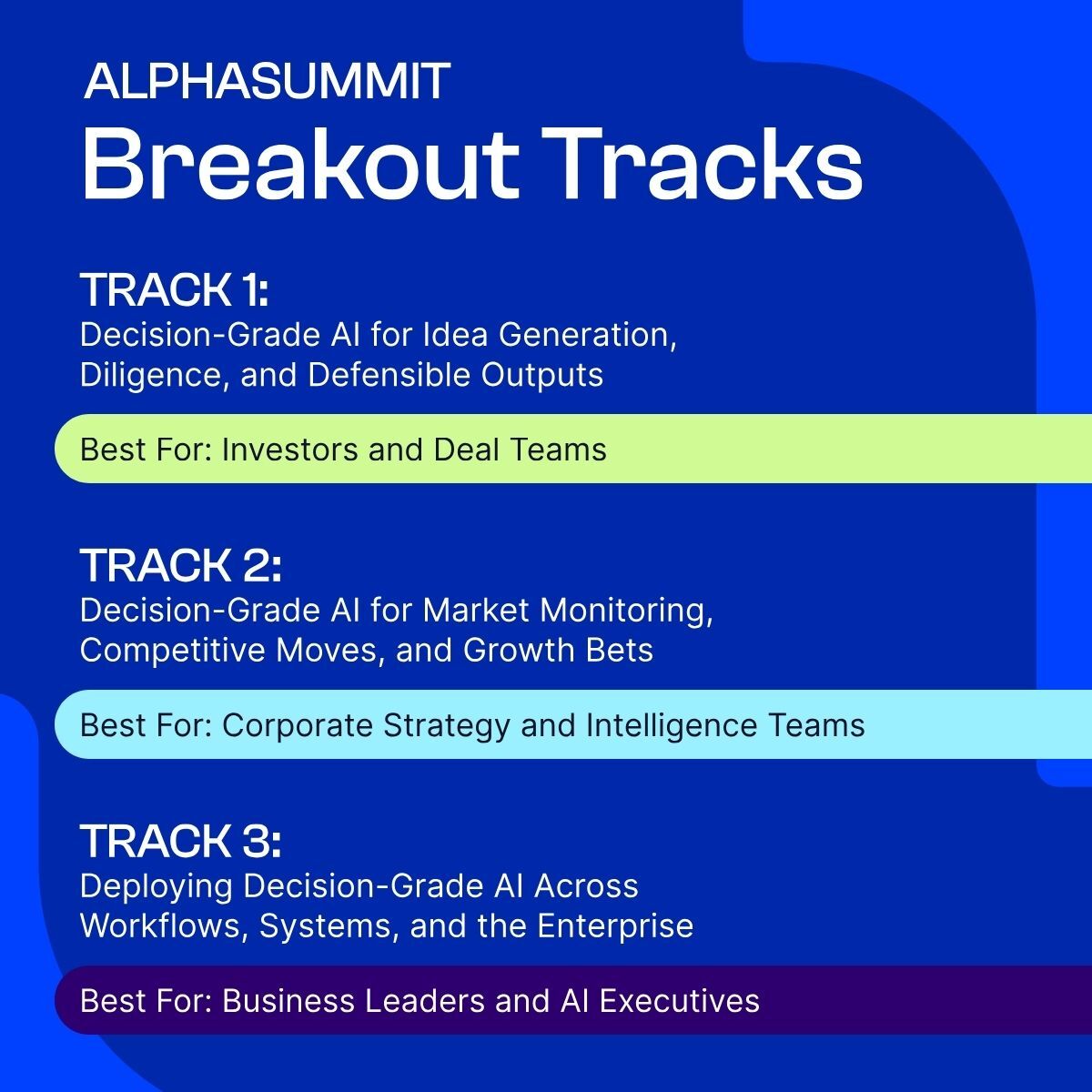

Are you ready to put decision-grade AI to work? The #AlphaSummit2026 agenda is now live and ready to explore!

The best investors, deal teams, and strategy leaders aren't just working with more data. They're pulling ahead with actionable intelligence, and the difference? Their work holds up under scrutiny.

Seeking AI outputs you can actually defend? Find the sessions you and your team can't afford to miss at The Glasshouse in NYC Oct 5-7: events.alpha-sense.com/alpha…

1

3

1,223

Jun 10

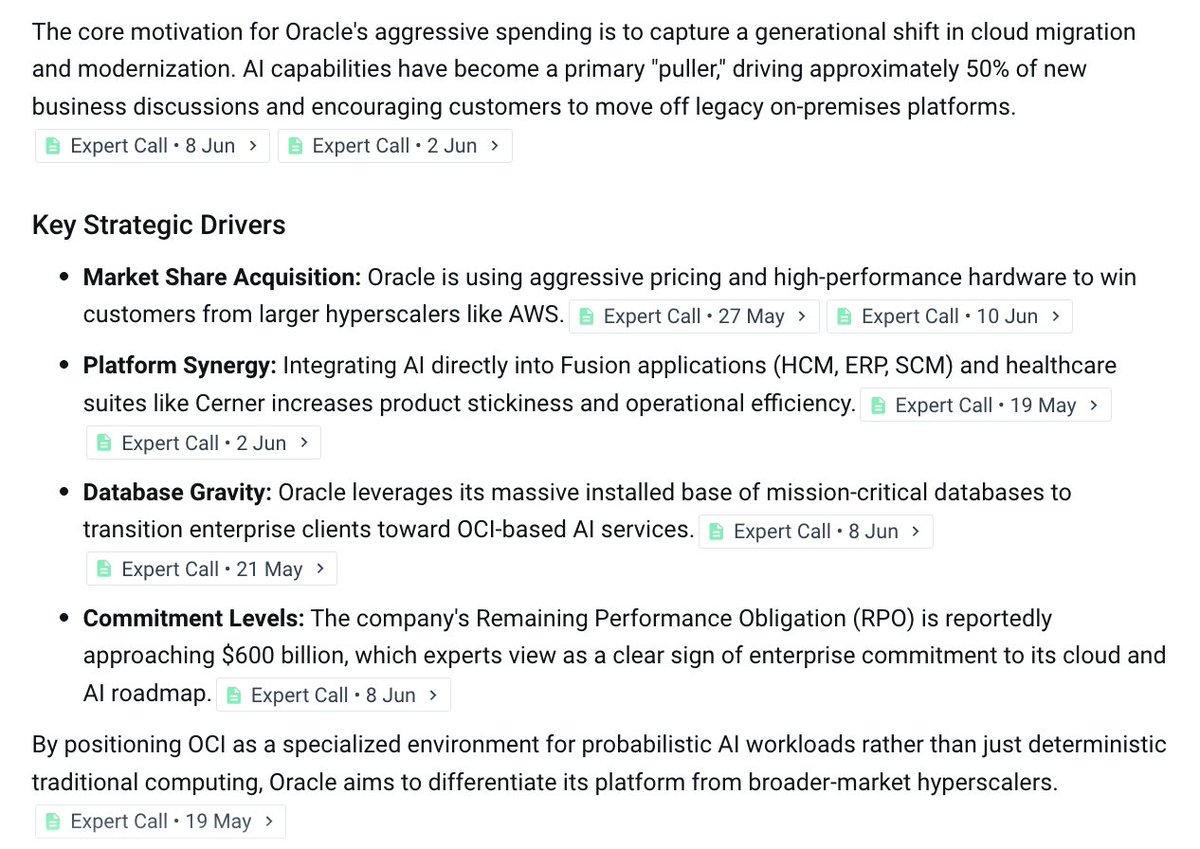

AlphaSense experts describe $ORCL as undergoing a massive transformation from a traditional product provider into a specialized AI infrastructure and cloud platform company.

The motivation behind the aggressive spending is capturing a generational shift in cloud migration and modernization. AI capabilities have become a primary "puller," driving approximately 50% of new business discussions and encouraging customers to move off legacy on-premises platforms.

The differentiation play: positioning OCI as a specialized environment for probabilistic AI workloads rather than just deterministic traditional computing, setting Oracle apart from broader-market hyperscalers.

4

26

3,738

Jun 10

"Confidently wrong" is the most dangerous output. You can't spot it. You can't defend it. And it's already in your AI workflow.

The next era of enterprise AI won't be won by the most connected systems. It'll be won by the ones professionals actually trust with consequential decisions. The conversation has been dominated by connectivity. What can enterprise AI access? What can it generate? But as organizations move from experimentation into operational workflows, the standard has to change.

Kiva Kolstein, President and CRO of AlphaSense, lays out what decision-grade AI actually requires: the right evidence, preserved context, and accountability that holds up under scrutiny: alpha-sense.com/blog/trends/…

1

2

4

1,457

Jun 10

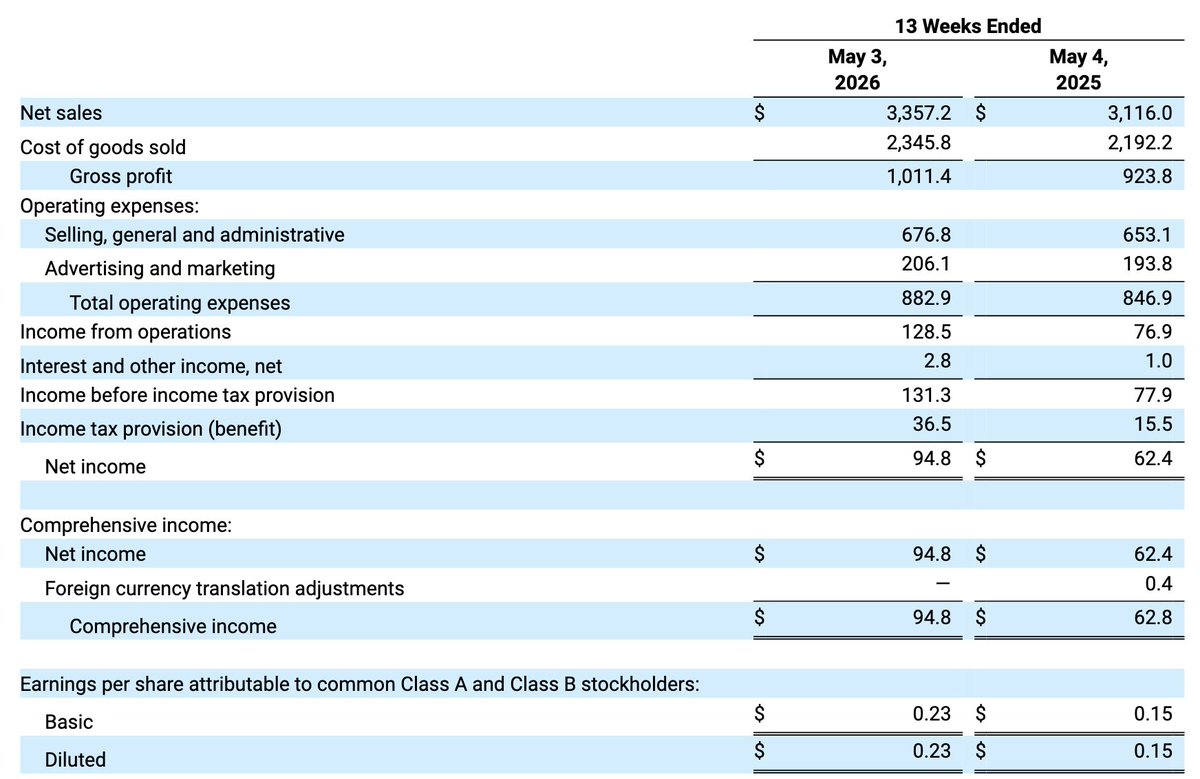

$CHWY Earnings:

- Net sales of $3.36 billion increased 7.7 percent year over year

- Diluted earnings per share of $0.23, an increase of $0.08 year over year

- Gross margin of 30.1 percent increased 50 basis points year over year

- Adjusted diluted earnings per share of $0.43, an increase of $0.08 year over year

- Net income of $94.8 million, including share-based compensation expense and related taxes of $73.4 million

“Chewy continues to outperform the pet category while expanding profitability and free cash flow,” said Sumit Singh, Chief Executive Officer of Chewy. “Our first quarter results demonstrate the resilience of our business model and the strength of our execution, as we delivered 7.7% net sales growth, nearly 200,000 net customer additions, and record profitability in the quarter, despite a more dynamic consumer backdrop. We remain confident in our ability to gain market share, deliver profitable growth, and create long-term shareholder value.”

research.alpha-sense.com?doc…

1

1,576

Jun 9

$CASY Earnings:

- Diluted EPS of $4.37, up 66.2% from the same period a year ago. Net income was $162.7 million, up 65.5%, and EBITDA was $350.3 million, up 33.2%, from the same period a year ago.

- Inside same-store sales were up 5.5% compared to the prior year, and 7.4% on a two-year stack basis, with an inside margin of 42.4%. Total inside gross profit increased 10.5% to $643.4 million compared to the prior year.

“Casey's delivered another record fiscal year as our team closed out the three-year strategic plan on an extremely high note, reaching $714 million of net income and nearly $1.5 billion in EBITDA," said Darren Rebelez, President and CEO. “Inside same-store sales for the year were extremely strong, up 4.2%, or 7.0% on a two-year stack basis, led by strong performance in prepared foods and non-alcoholic beverages. Our fuel team did a great job balancing gallons sold with fuel margin, as fiscal 2026 fuel gross profit increased 21% from the prior year. The operations team performed exceptionally well over the course of the year as we reported substantial EBITDA growth while same-store labor hours were slightly favorable for the year.”

research.alpha-sense.com?doc…

2

1

3

2,010