Systematic stock trader, researcher and strategy consultant. AmiBroker expert.

Joined February 2014

- Tweets 471

- Following 89

- Followers 4,628

- Likes 1

75 Photos and videos

21 Nov 2022

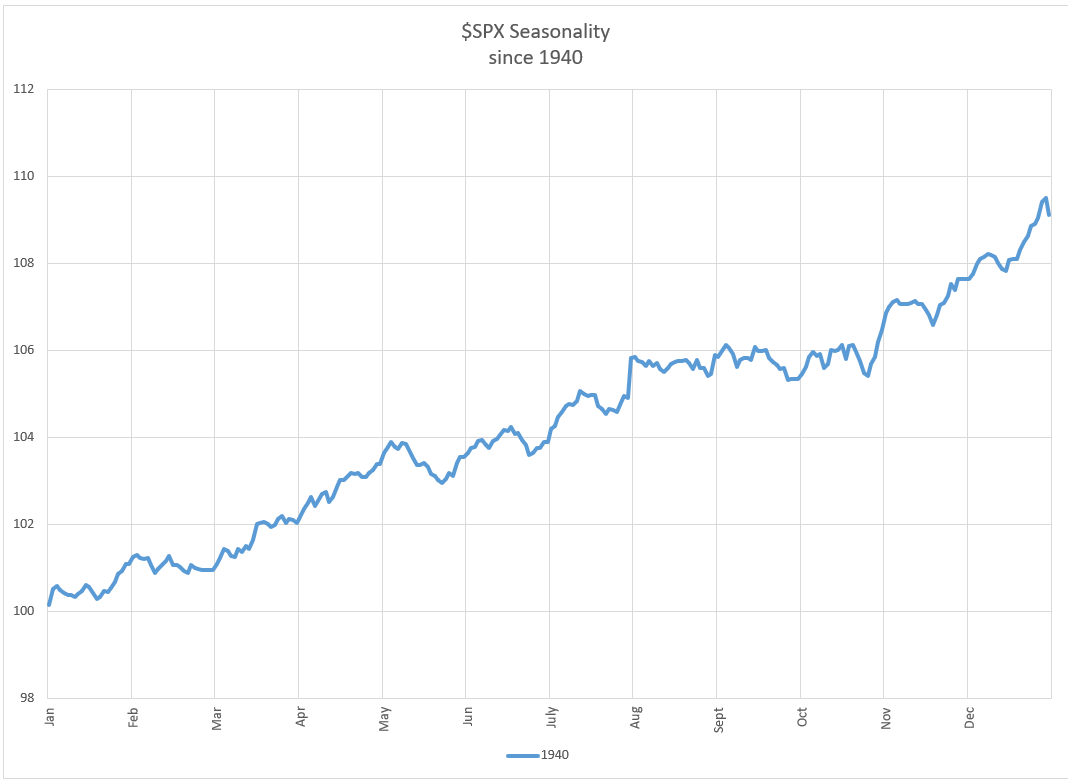

Since 1970, the avg weekly return is .16% with 56% of them up. The avg for Thanksgiving week is .58% with 69% up. When above the MA200 avg p/l is .63% with 76% up. When below the MA200 avg p/l is .47% with 58% up

1

4

17

2 Nov 2022

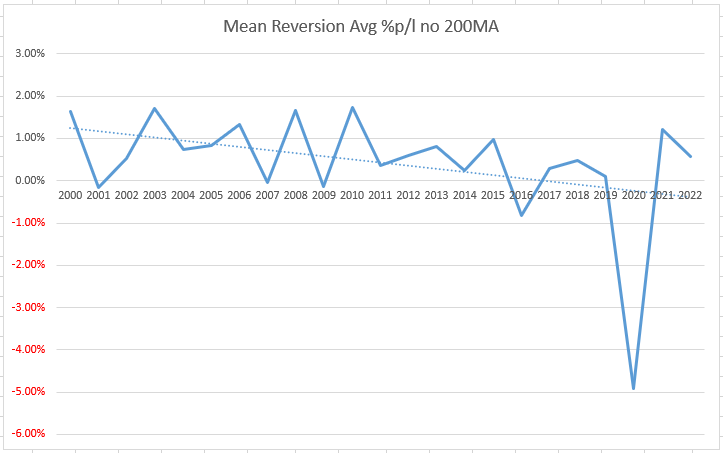

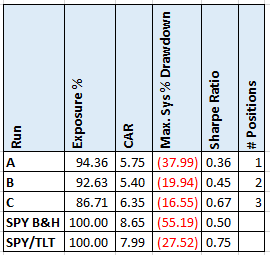

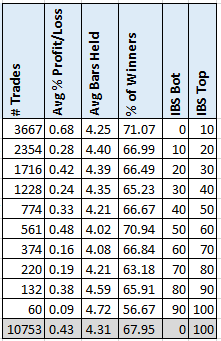

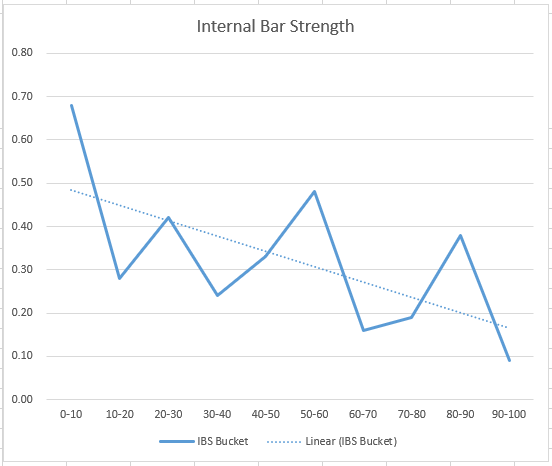

A slow decline in the avg %p/l of mean reversion trades. Read alvarezquanttrading.com/blog…

2

3

12

24 Oct 2022

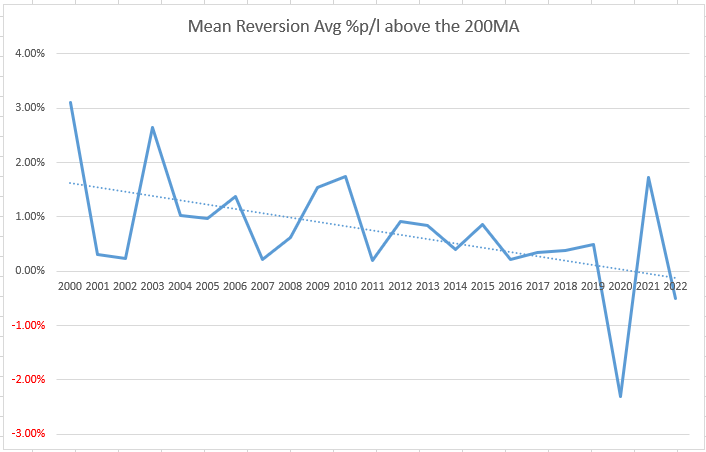

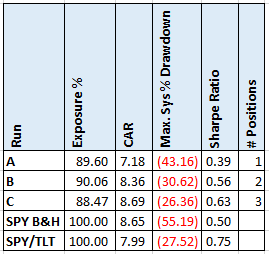

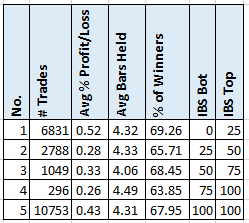

Here are the avg %p/l of mean reversion trades above the 200-day moving average. A slow decline in the edge.Read alvarezquanttrading.com/blog…

1

6

7 Oct 2022

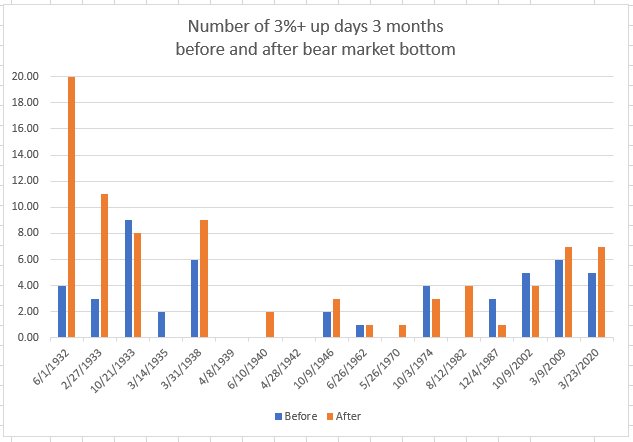

Got to wondering, do 3% up days happen more often before or after bear market bottoms.

2

1

9

30 Sep 2022

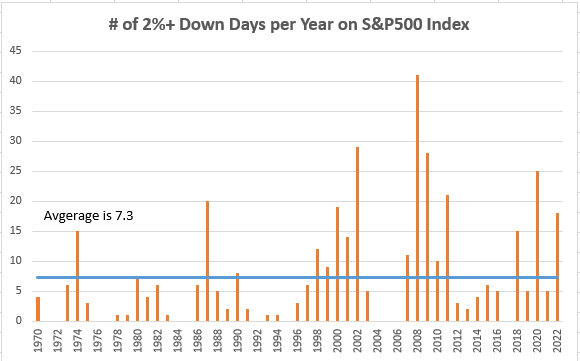

After yesterday's 2.1% decline in the S&P500 index, I wanted to know the typical number of times this happens per year. For this year, the count is 18 so far. If this rate continues for the rest of the year, the count will be 24.

2

3

12

21 Sep 2022

I test an ETF rotation strategy on SPY, EFA, IEF, GLD, ICF using ranking method using 1 month return, 3 month return and 20 day historical volatility. Read alvarezquanttrading.com/blog…

2

5

14 Sep 2022

I test a ranking method -using 1 month return, 3 month return and 20 day historical volatility- for an ETF rotation strategy on XLB, XLE, XLF, XLI, XLK, XLP, XLU, XLV, XLY. Read alvarezquanttrading.com/blog…

1

10

10 Aug 2022

Surprisingly filtering out stocks with historical volatility greater than their median improved drawdowns. alvarezquanttrading.com/blog…

3

4

13

3 Aug 2022

Using historical volatility to filter out trades reduces drawdown by 25%. alvarezquanttrading.com/blog…

1

1

9

23 Jul 2022

From @priceactionlab, "Losing discipline and not following basic rules is more prevalent during a bear market and a slow “pain trade”." So true

4

14

22 Jul 2022

For a mean reversion trade, is better to for further intraday weakness or wait for the resumption of the trend? Wait for further weakness. Returns are 100% better and MDD is the same. Read alvarezquanttrading.com/blog…

1

12

20 Jul 2022

For a mean reversion trade, is better to just get in at the open or wait for the resumption of the trend? Just jump in. Returns are 50% better and MDD is a 10% worse. Read alvarezquanttrading.com/blog…

2

5

15 Jun 2022

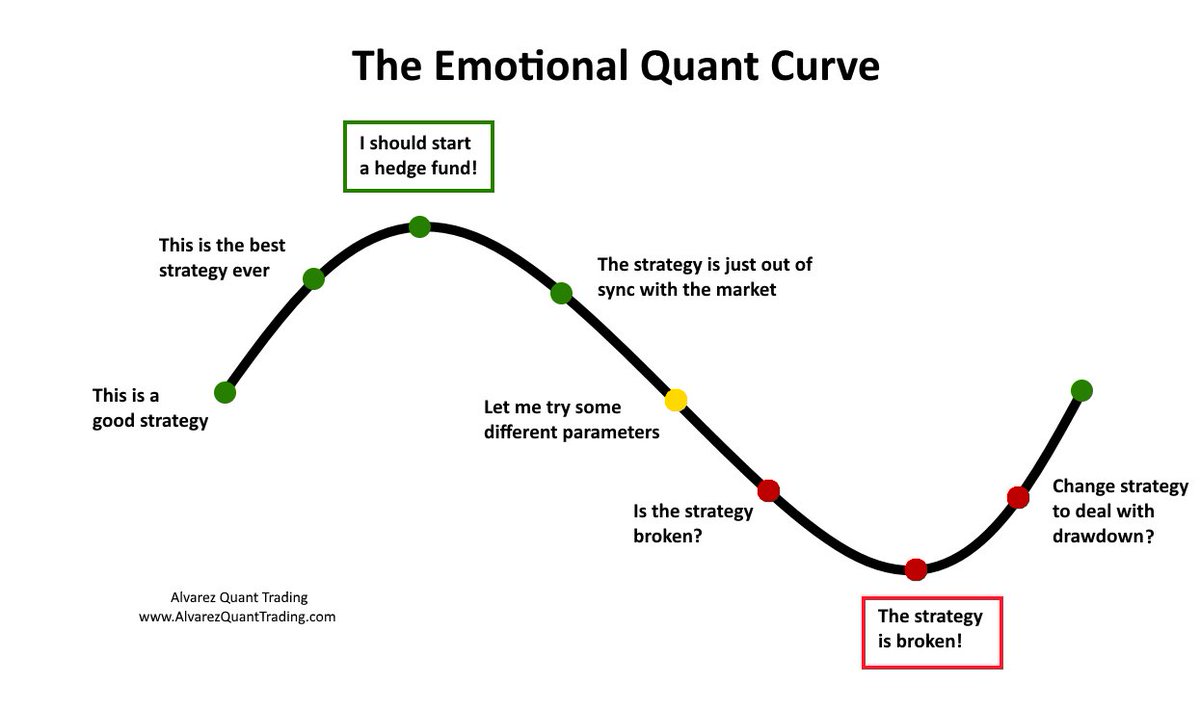

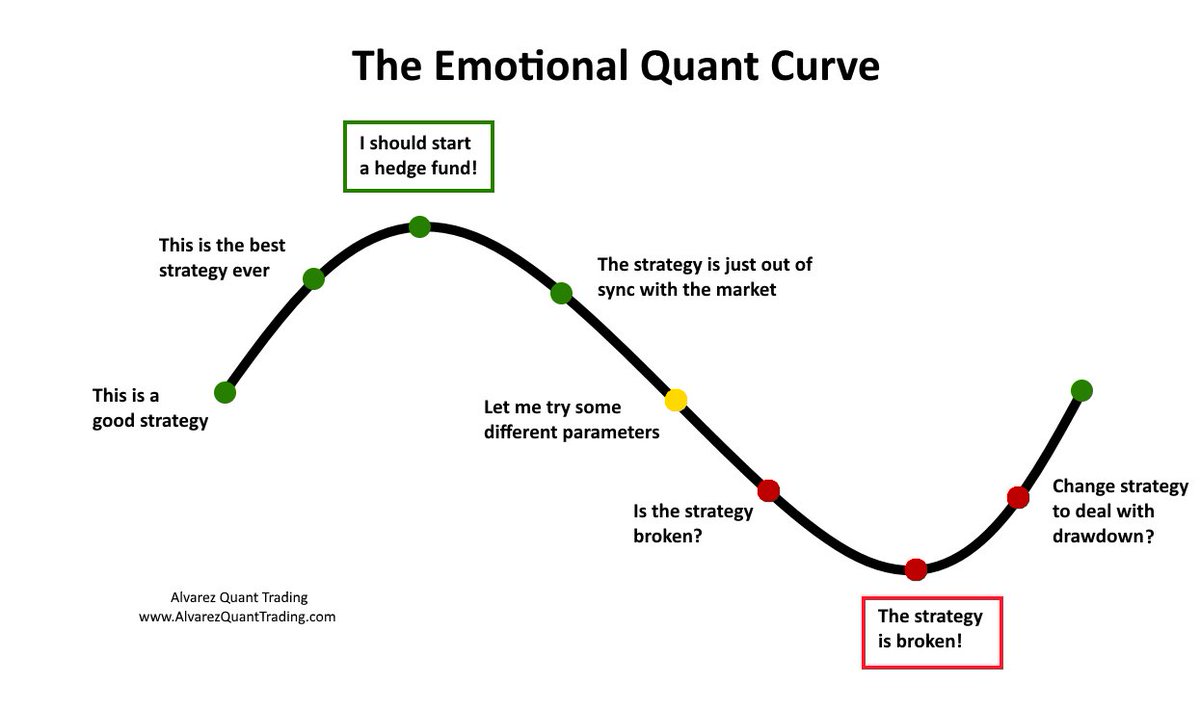

I know I have gone from the top of the curve to the bottom in the last 5 months. How about you? Read more alvarezquanttrading.com/blog…

3

10

61

23 May 2022

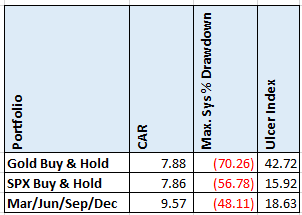

A simple quarterly momentum rotation strategy using Gold and SPX. Read alvarezquanttrading.com/blog…

1

1

7

20 May 2022

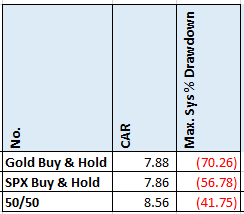

A portfolio of 50% Gold and 50% SPX and rebalancing monthly. Read alvarezquanttrading.com/blog…

1

4

18 May 2022

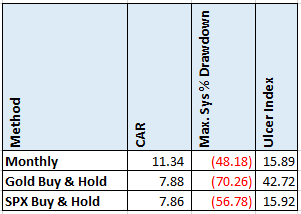

Using Gold and SPX, a monthly momentum strategy. Read alvarezquanttrading.com/blog…

1

1

7

11 Apr 2022

I try using Benford’s Law to help with the selection of a specific variation from an optimization run. It shows promise at first but then with more investigation does not. Read alvarezquanttrading.com/blog…

1

3

8 Apr 2022

Do S&P500 stocks follow Benford’s Law? For the most, the answer is not even close. Read alvarezquanttrading.com/blog…

1

1

7

6 Apr 2022

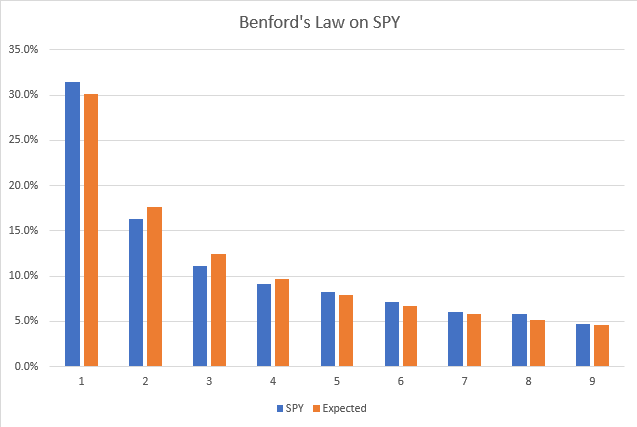

Do the daily returns of the S&P500 Index follow Benford’s Law? They closely do. Read more alvarezquanttrading.com/blog…

1

2

5