It's all about mindset. Shares are stepping stones to your goal. Looking for the next bagger. Tweets are my opinion only. DYOR

Joined August 2014

- Tweets 7,836

- Following 533

- Followers 695

- Likes 19,355

1,614 Photos and videos

Jun 10

Did the MM’s drop the price to let those very big buys in??? One day we will be away from this crap #avct

1

1

24

2,383

Jun 1

3% drop, can’t make this shit up!! One day we’ll get the right response from such incredible data! #avct

4

30

2,135

May 8

On the button Myles, #AVCT

May 8

Morning MB - absolutely nothing to do with that. Avacta has nothing to do with diagnostics anymore - it's purely biotech (specifically, precision oncology).

The SP charge over the past 24 hours is to do with the wider market belatedly realizing - in the wake of a phenomenal Science Day on Wednesday - that #AVCT's pre|CISION platform is now on course to become the delivery vehicle of choice for a large majority of cancer treatments, in the decades ahead.

Multi-$100bn revenue and value opportunity for the platform, in the uber bull case scenario. It's now a matter of seeing how much of that, Avacta as a company (and its existing shareholders!) can capture, before the platform falls into bigger hands.

3

26

5,190

May 6

One good point to notice is that the sp has been far more stable compared to previous years on SD. Bodes well imo #AVCT

5

2

36

5,652

May 4

Understandably being a bank holiday all is quiet here, however, I think come tomorrow it’ll light up like November 5th #AVCT

3

4

38

2,470

Capt. Chaos retweeted

Apr 27

Avacta is in a different universe, as they're going after the biggest selling ADC of all time with their "unique industry-leading technology platform".

1

2

22

581

Apr 27

Thanks Grok! When asked for a little for like comparison and extrapolation…

$15B? Not a bad opening bid 😝

1

25

1,774

Apr 25

Apr 25

Hi Bob, AIM doesn’t care much for PowerPoint slides. But it’s given those that do care, the time to accumulate while the valuation has been low. The next step is to bring in a partner for 6000 P2 & obtain some form FDA expedited approval. Two bits of news that will rerate us IMO.

1

21

2,604

Apr 22

Great post over on LSE, way to big to copy and paste here, suggest people pop over there and have a read

BuenaVista

Putting the rubbish spoken about clinical failure to bed

Today 15:48

#AVCT

1

2

26

3,457

Apr 6

I wonder if I’m the only one over the long weekend who’s been wondering if the trial is going ok? #AVCT

7

2

50

3,949

Apr 2

We should be fucking flying after the little tweet from CC, as RAH has said 100 hours and no reports of adverse reactions!! Nasdaq we’d be marching towards $10, AIM 65p FFS #AVCT

7

2

41

2,749

Apr 2

Apr 2

Look across the pond at UK-listed @avacta $AVCT #AVCT.

Targeted oncology.

Its pre|CISION platform can be used to modify practically any anti-cancer small molecule or biologic, into a peptide-drug conjugate.

These PDCs can be used to target around 85% of all types of cancer cases.

Two drugs in the clinic. One to kick off a Pivotal Phase 2/3 trial this summer; the second drug having just commenced a Phase 1 trial.

The uber bull case is that pre|CISION PDCs eventually displace the large majority of the existing and anticipated ADC market. PDCs...

- are significantly more targeted than ADCs;

- are much lower cost (as don't require an expensive biologic such as a mAb);

- have broader applicability (almost tumour agnostic - see 85% fig above);

- have broader versatility (the Avacta scientists can modify practically any warhead with pre|CISION);

- have superior tumour penetration and tissue diffusion, owing to their smaller size.

In fact, it is difficult to point out a single major advantage that the existing class of ADCs enjoys over Avacta's PDCs.

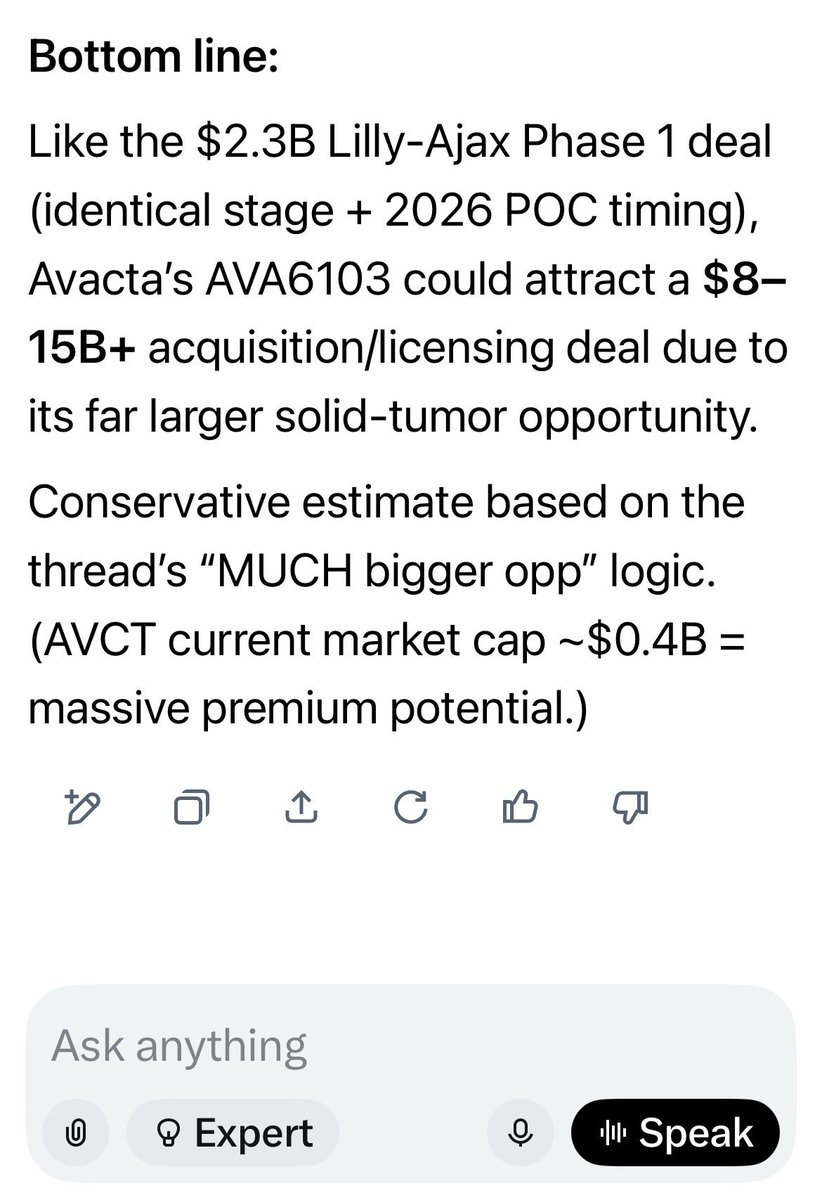

If the second drug in clinic - AVA6103, a modified version of the all-powerful warhead, exatecan - replicates the published pre-clinical data (22/24 complete responses in various animals models - a CR rate of 92%), it has the real potential to blow Enhertu (and even Keytruda) out the water.

By virtue of Avacta's UK listing, this opportunity exists. The UK investment community is a shadow of what it once was - it lacks depth, breadth, and many of its participants do not possess the intellectual curiosity and/or risk tolerance for pre-revenue / lossmaking entities.

Were Avacta listed on NASDAQ right now, I would suggest it'd be valued at at least 10x its current mkt cap of $363m.

2

17

1,951

Apr 1

agree with RAH I too don’t think any persons taking part in the placing are selling so what can it be. Oversubscribed, so people with deep pockets are selling and buying to build their portfolio? Maybe. Some selling as not sure if 6103 will succeed, maybe. Apart from this 🤷🏻♂️#AVCT

2

1

9

2,159

Apr 1

This is an amazing quote

"There are people dying now that I know in a year or in two years, we will have treatments so they don’t have to die." Check out Stonks post earlier today . I wonder #AVCT

1

25

1,480

Apr 1

You are aiming way to low Steve #AVCT

Apr 1

I know my number, and that does look very very similar.

2

15

3,631