Joined September 2016

- Tweets 38,642

- Following 1,045

- Followers 70,719

- Likes 65,520

4,536 Photos and videos

Pinned Tweet

27 Feb 2023

Indicators are a very important part of Technical Analysis 📚

Today's thread 🧵 is about "Different Type of Indicators used in Stock Markets"

Do read , like and retweet to appreciate the writer and dont forget to follow @ArjunB9591 for more such threads.

Let's Continue

1/n

29

106

316

164,547

Dhan has opened up US Stocks & ETFs via the IFSCA GIFT City route. India INX is the exchange underlying it. Right now, most of your money is betting on just one country. Adding some US stocks means you're not putting all your eggs in one basket.

Jun 15

Introducing US Stocks & ETFs on Dhan 🇺🇸

Interest in global investing is growing in India. Yet, it's felt out of reach for most. Concerns around regulations, hidden charges, and fund transfers kept investors from taking the leap.

Today, that changes for all Dhan investors

1

3

1,211

Jun 12

Remember when Zomato turned its bottom line around and the stock just took off?

Looks like Zepto is running the same playbook, just quite faster.

Two lines in the DRHP move in opposite directions, which is exactly what you want to see:

➡️ Top line is accelerating. NRV grew 57% in two quarters, from ₹5,175 Cr in Q2 FY26 to ₹8,134 Cr in Q4.

➡️ Cash burn is shrinking. Over those same two quarters, FCF loss per order fell from ₹102 to ₹42. A 58% drop.

When revenue is compounding at ~120% and the cash burn per order is getting cut by half at the same time, you're not just buying market share.

The scale itself is doing the work, spreading fixed costs thinner on every order.

Public markets like a clear line to profitability. Zepto's giving them one. Curious to see how it prices.

1

602

Apr 28

Finally seeing some focus on capital strength vs just chasing active users. That’s a more meaningful metric imo. @ashishnanda thanks for this information.

Apr 25

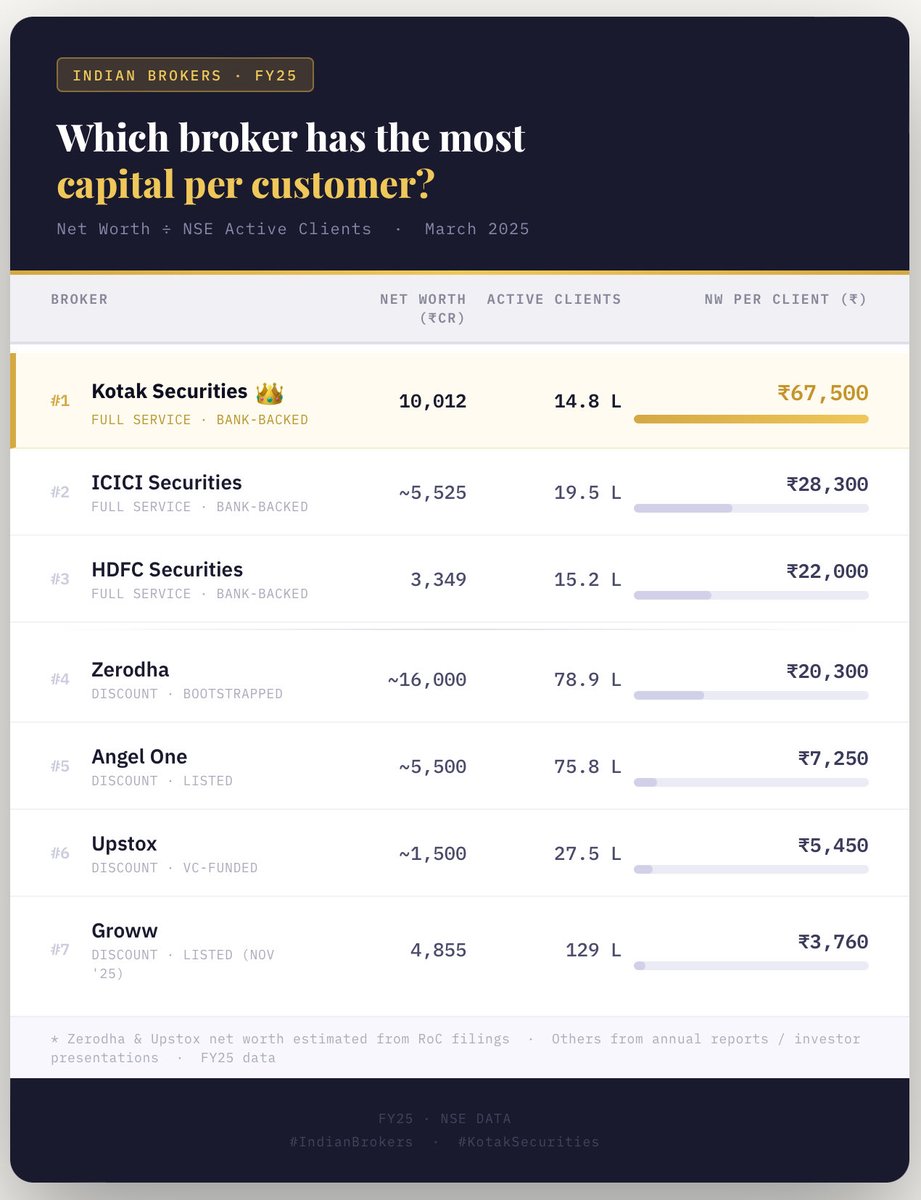

What SEBI is largely implying with the consultation paper is that net worth has to be in line with how many active clients a broker services.

Whatever the safeguards, net worth can never be ignored when it comes to safety of investor capital.

At ₹67,500 net worth per active client, #KotakNeo continues to be on top and by far.

Full-service. Bank-backed. Digital. Built for the long run.

1

2,021

Apr 11

One of the finest and best gin , must try 😉❤️

Plus the reusable copper bottle is icing on the cake 😄

1

1

13

3,348

Apr 8

Again @Milkbasketin

@gharkekalesh

Apr 8

Dear @Milkbasketin

I am writing to express my disappointment regarding the failed pickup of my return item – Good Life Sugar (5kg), scheduled.

As per your instructions, I had kept the product outside my flat for early morning pickup. However, the item was not collected

1

1,129

Apr 6

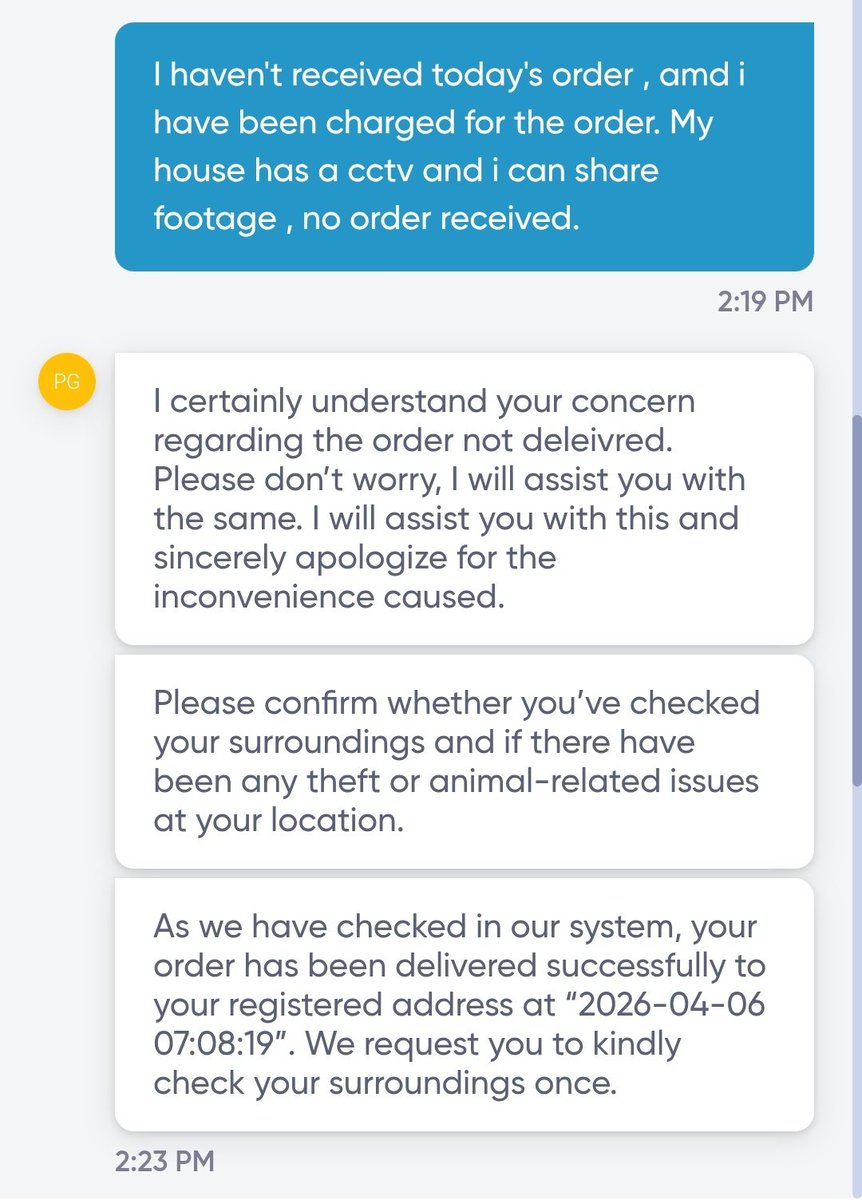

Terrible service @Milkbasketin

Apr 6

X user Arjun Bhatia exposed a major scam by @Milkbasketin: charged for milk but no delivery. Customer care claimed delivery at 7:08 AM with proof of a rider marking it "delivered" via location tag without leaving any order. Refunded after sharing CCTV Vid

3

3

2,731

Arjun Bhatia retweeted

Apr 6

X user Arjun Bhatia exposed a major scam by @Milkbasketin: charged for milk but no delivery. Customer care claimed delivery at 7:08 AM with proof of a rider marking it "delivered" via location tag without leaving any order. Refunded after sharing CCTV Vid

52

409

3,052

213,995

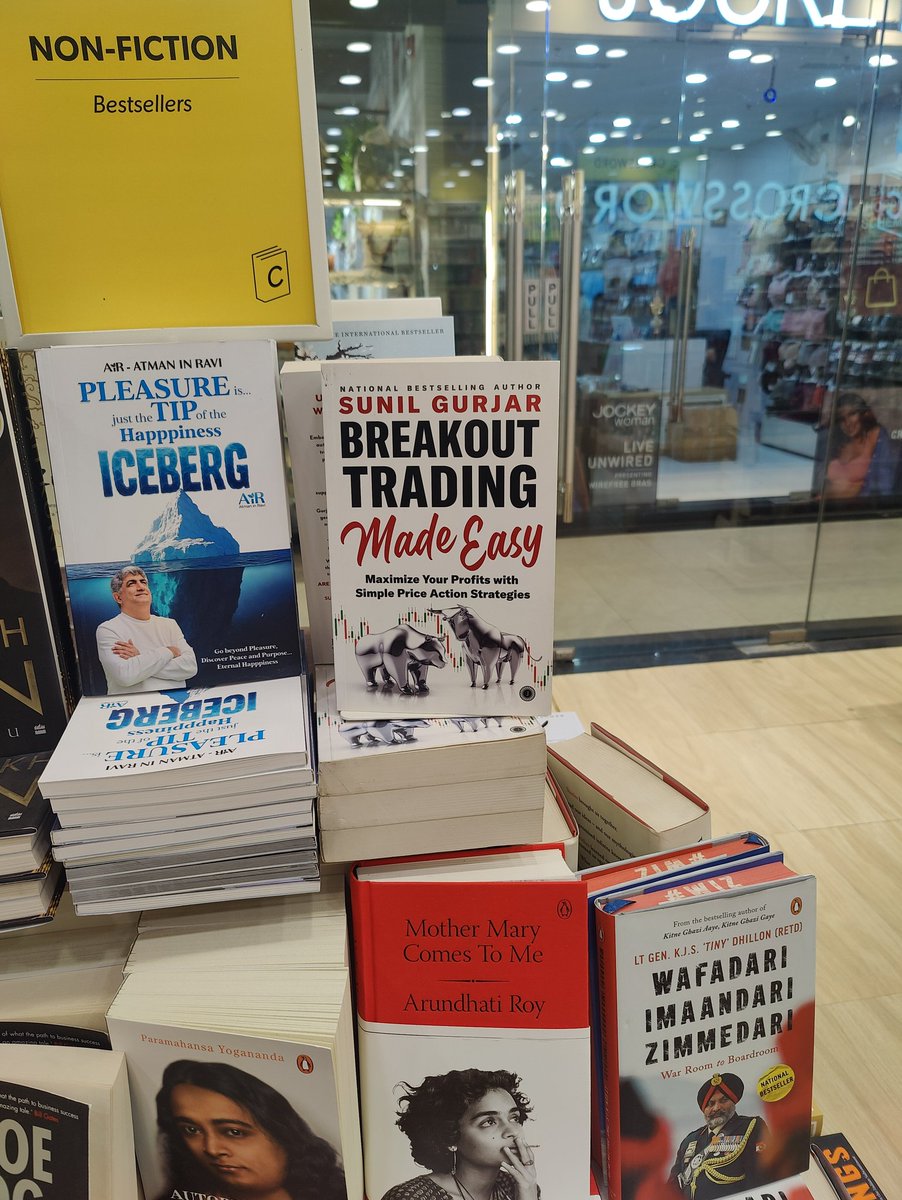

Apr 6

So good to see your books at one of the biggest bookstores in Gurgaon @sunilgurjar01 🧿💯💐

1

1

1,952

Apr 6

A very great scam happening by @Milkbasketin nowadays

This morning i was charged money for my milk order but i didn't receive the order.

On messaging customer care , they said we have delivered at 7.08.19 , here is the cctv footage for the same time , a guy will come from milk basket , stand there , mark the order paid through location tagging but will not keep any order.

They refunded after i shared video

58

191

663

99,009

Apr 2

Hey @instamart_it @ZeptoNow @zeptocares

I live in south of gurgaon with pincode 122103/122102

Surprisingly only @letsblinkit is serving here with monopoly.

Can you guys start delivering in our area ?

1

2

2,028

Apr 1

Simplex Castings - Update

Company is heavy engineering castings business.

It manufactures heavy engineering castings in grey cast iron.

March updates:

• ₹13.02 Cr order – Thyssenkrupp AG

• ₹23.13 Cr order – SMS India Pvt Ltd

Order book stands at ~₹130 Cr.

RDSO approval from Research Designs and Standards Organization could enable railway supply opportunities.

4

22,174

Mar 29

Half Movie twitter pe dekhne ke baad , another half pvr mein dekhne aaya hu 🥲

#Dhurandhar2TheRevenge

9

3,478

Arjun Bhatia retweeted

Mar 19

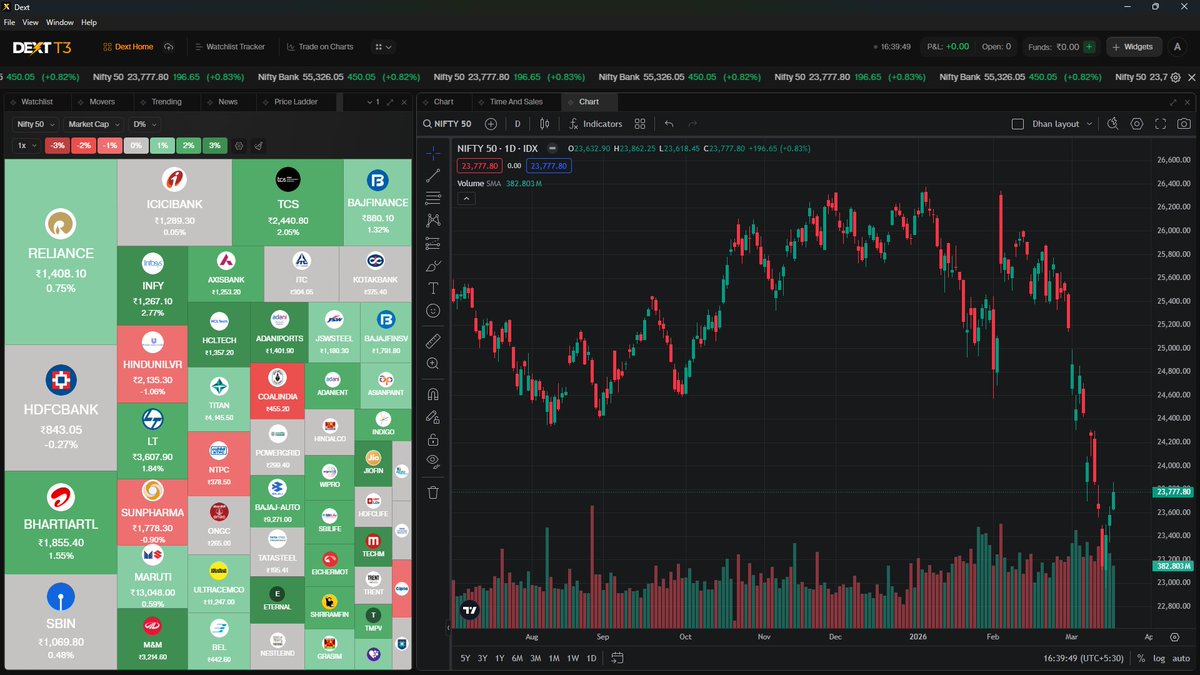

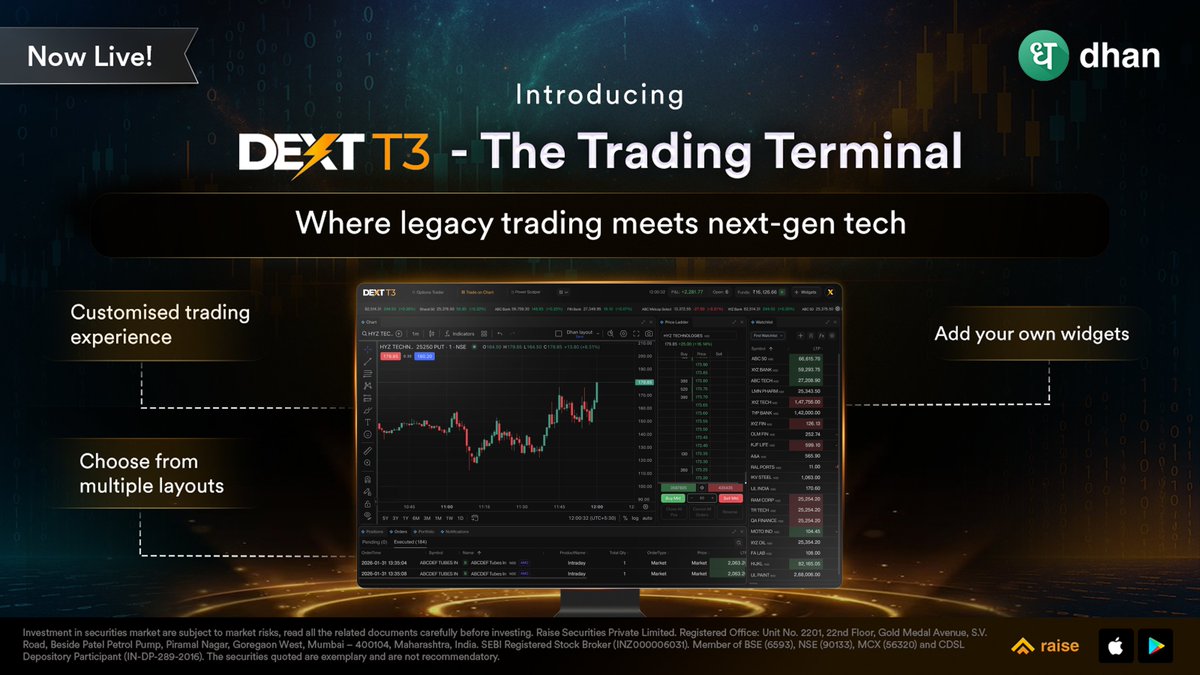

Introducing: DEXT T3 - The All-New Trading Terminal by Dhan

DEXT T3 is a modern trading terminal built on top of our proprietary DEXT Trading Engine, which powers all trades on Dhan.

Here's what you can do on DEXT T3 🧵

43

80

301

397,367

Mar 19

Good to see Dhan pushing the envelope on innovation for retail traders.

Features like Price Ladder and Time & Sales were long due - interesting to see this coming together in DEXT T3.

Mar 19

Introducing: DEXT T3 - The All-New Trading Terminal by Dhan

DEXT T3 is a modern trading terminal built on top of our proprietary DEXT Trading Engine, which powers all trades on Dhan.

Here's what you can do on DEXT T3 🧵

3

9

1,576

Mar 18

Got early access to this trading terminal, and it’s bringing features like Price Ladder, Time & Sales, and Volatility Skew to retail traders - usually institutional territory.

It's called DEXT T3 by Dhan. It's Clean, customisable, fast, and usable on both web & desktop.

I would like to see how traders adapt to terminals and where this goes next .

6

24

5,838

Mar 12

Urgent : Help Required

I am in a medical emergency at Medanta Gurgaon and i may need blood (any blood group) for a family member.

Does anyone stay nearby who can donate blood in need ?

Please amplify and share as much as possible 🙏🏻

6

62

37

10,106

Mar 4

🚨Geopolitical risks are rising.Volatility is expanding. 🚨

While equities fluctuate, not every rupee should stay exposed and not every rupee should stay idle.

In volatile cycles, allocation must be intentional & not emotional. Diversification isn’t about adding more. It’s about adding structure.

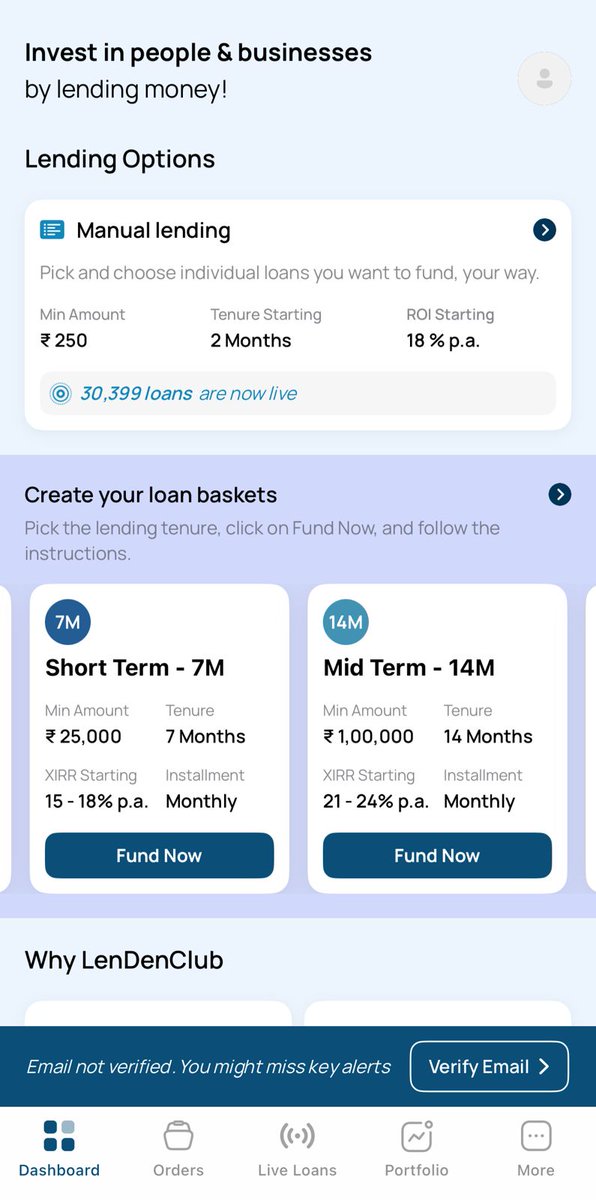

P2P lending by @LenDenClub brings that structure. It is non-market linked and gives regular cash-flow.

Here you invest in people and businesses and you earn as they repay (Principal Interest).

Because smart allocation compounds.Blind exposure doesn’t.

#LenDenClub #P2PLending #WW3 #IranWar #PortfolioStrategy

1

1

2,321

Mar 3

1

5

1,840