Tech, trade, global security analysis.

Joined May 2023

- Tweets 9,118

- Following 493

- Followers 955

- Likes 199

473 Photos and videos

M@Mapshock retweeted

China's latest balance sheet and fx flow data shows ongoing intervention to limit the CNY's rise -- "settlement" has historically been an intervention variable, and forward adjusted settlement was $50b in May

1/

1

2

16

4,973

Strait of Hormuz Access Restoration: US-Iran Accord and Global Oil Supply Route Reopening

The progressive reopening of the Strait of Hormuz represents a significant energy infrastructure event, with cascading implications extending far beyond Middle Eastern shipping lanes.

The World Bank characterized the Hormuz closure as "the largest oil market disruption in history," removing 10.1 million barrels per day from global markets and triggering physical crude prices near $150 per barrel. As limited commercial traffic tentatively resumes under Iranian-controlled conditions, the structural implications are reshaping global energy security, maritime logistics, and regional power dynamics. The interplay between geopolitical tensions and economic vulnerabilities has exposed the fragility of chokepoint-dependent supply chains, while simultaneously accelerating infrastructure diversification and alternative route development. Even partial reopening cannot restore pre-conflict confidence levels, as shipping insurers demand war risk premiums of up to 5% of hull value compared to 0.25% before the crisis.

The Chokepoint Paradox: Why Reopening Doesn't Equal Recovery

The Strait of Hormuz exemplifies what strategic analysts term "chokepoint paradox" — where the reopening of critical infrastructure fails to restore pre-disruption confidence levels. Despite limited vessel movements documented by shipping trackers, the fundamental risk calculus has shifted permanently.

Gulf News shipping data shows that while two LNG tankers successfully crossed out of the Gulf bound for Pakistan and China, traffic occurs under Iranian-controlled conditions with mandatory vetting schemes administered by the Islamic Revolutionary Guard Corps. This "toll booth" system, as described by Lloyd's List Intelligence, represents a fundamental alteration of maritime sovereignty principles that governed the strait for decades.

The economic impact extends beyond immediate shipping costs. The Dallas Federal Reserve modeling indicates that even a one-quarter closure raises WTI oil prices to $98 per barrel and reduces global GDP growth by 2.9 percentage points. With partial reopening creating ongoing uncertainty rather than resolution, markets are pricing persistent disruption risk rather than recovery scenarios.

Physical crude oil prices surged to record levels near $150 per barrel during peak closure, according to the International Energy Agency, creating significant disconnection between physical and futures markets. This pricing dynamic reflects the structural transformation of global energy flows rather than temporary disruption.

mapshock.com/briefings/strai…

49

Trump announced on June 11 that a 60-day ceasefire extension was reached, enabling parties to negotiate a final agreement.

Yet the same week, three Indian sailors were killed in a U.S. strike on the M/T Settebello oil tanker off Oman, with all crew members initially confirmed missing before India's shipping minister announced the identified deaths. The deaths expose a critical paradox: while US-Iran diplomatic negotiations ostensibly operate under ceasefire terms, the US military's aggressive enforcement of an Iran oil blockade generates casualties among neutral-flag vessels and third-party seafarers. This gap between diplomatic and military lines of effort creates immediate pressure on India-US relations at a moment when both capitals are attempting to reset ties after months of friction. The timing, just days before Modi and Trump's planned meeting at the G7 Summit in France, transforms an operational incident into a strategic liability for Washington's broader Indo-Pacific alignment.

The Blockade-Ceasefire Contradiction

The apparent contradiction between ceasefire negotiations and blockade enforcement reflects deeper strategic choices by the Trump administration. The April extension of the ceasefire left the blockade explicitly in place and ordered the military to remain combat-ready. CENTCOM's operational posture treats commercial shipping interdiction as a separate domain from the bilateral US-Iran truce, with independent targeting decisions and rules of engagement.

This creates an accountability gap. CENTCOM stated that the M/T Settebello's crew "repeatedly failed to comply with directions from American forces", framing the strike as a response to non-cooperation rather than as inherently destabilizing. Crew compliance with US military signaling in the Gulf of Oman occurs under ambiguous operational conditions, darkness, language barriers, transmission quality, and the inherent difficulty of distinguishing Iranian-flagged vessels from neutral-flag vessels carrying Iranian-origin cargo. No international maritime requires merchant crews to submit to active blockade enforcement on the high seas during nominal ceasefire periods.

mapshock.com/briefings/us-ir…

87

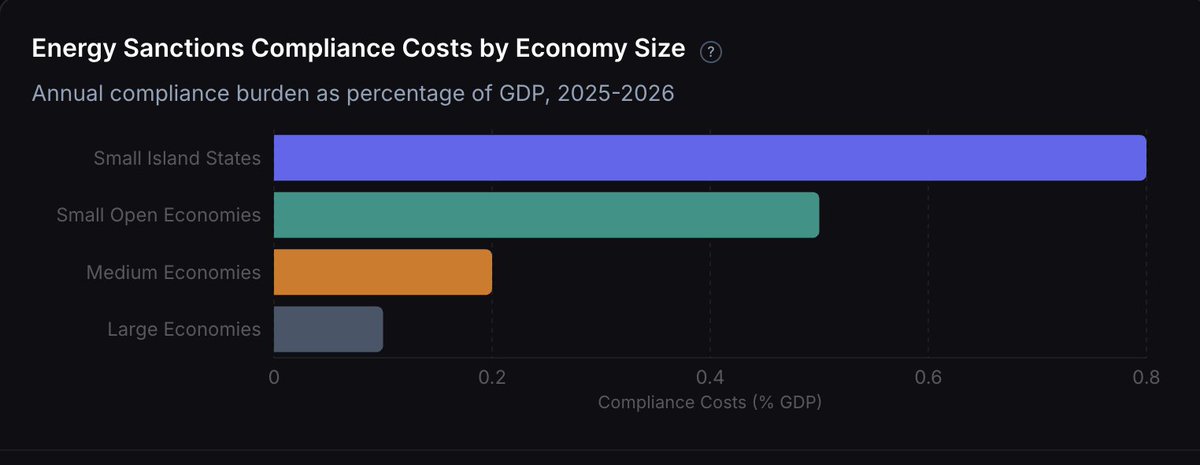

US sanctions targeting energy infrastructure in smaller economies operate through three primary mechanisms, asset freezes, transaction prohibitions, and secondary sanctions enforcement, creating cascading disruptions that extend far beyond the targeted state. The interplay between financial pressure and energy market vulnerabilities forces third-party traders into costly compliance regimes, while commodity-specific disruption patterns vary significantly between oil, gas, and refined products. Recent cases including Cuba's state oil company sanctions and Venezuela's energy sector restrictions demonstrate how smaller economies face disproportionate economic impacts relative to their global market share, with spillover effects reaching allied financial institutions and regional energy markets.

The Atlantic Council estimates sanctions on Russian, Iranian, and Venezuelan oil removed millions of barrels per day from global markets between 2014 and 2025, with China emerging as the primary destination for sanctioned crude through shadow fleet operations. Secondary sanctions enforcement has evolved into what compliance experts describe as "network-based targeting," capturing not just primary energy companies but their suppliers, logistics providers, and financial intermediaries across multiple jurisdictions.

mapshock.com/briefings/us-sa…

32

The UK intercepted the Russian shadow fleet vessel Smyrtos in the English Channel on June 14, 2026, marking London's first operation against a sanctioned Russian tanker, with Royal Marines and National Crime Agency officers boarding the vessel.

The interception operates within UK territorial waters and under international law provisions protecting the right to board vessels without nationality. This grounds the seizure differently than contested US operations on the high seas, where information available would give rise to a very different conclusion regarding lawfulness in terms of UNCLOS-based maritime law enforcement authorization.

However, the broader strategy depends on maintaining allied consensus around enforcement escalation. Some European countries, Finland, Estonia, Germany, and France, have boarded some suspicious vessels in the past months but have claimed a lack of sufficient grounds under international maritime law to justify permanent seizure. The UK's move in its own waters sidesteps this constraint but does not resolve it for allied navies operating outside territorial jurisdiction.

The interplay between energy pressure and maritime security creates compounding incentives for enforcement. EU sanctions had reduced the Kremlin's oil and gas revenues by 44%, falling to $2.9 billion in February 2026 compared to $5.2 billion in February of the previous year. Each seizure represents a fractional but measurable reduction in Russian hard currency earnings, while simultaneously raising the operational risk profile for shadow fleet operators and owners.

mapshock.com/briefings/uk-fo…

43

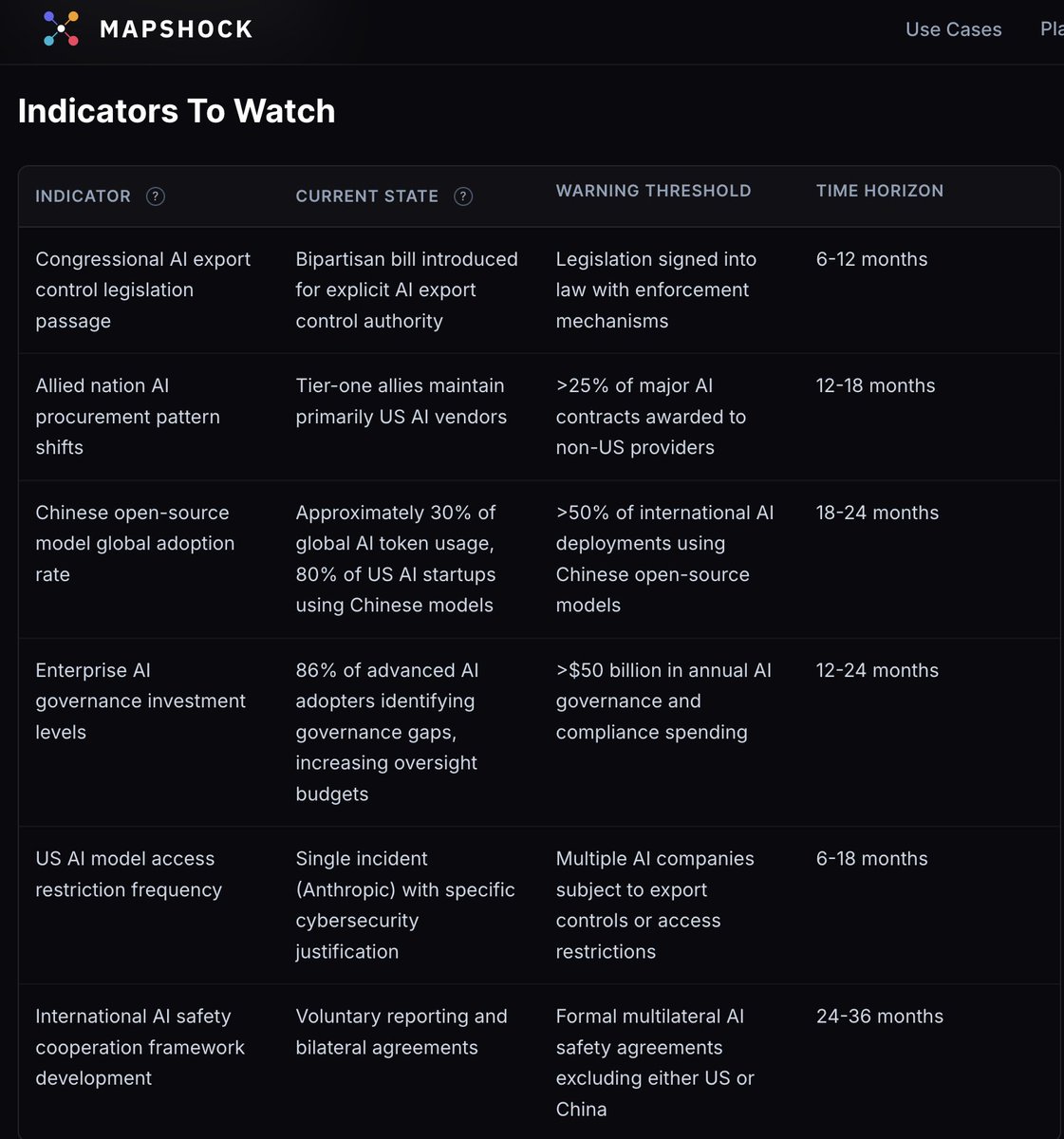

The Security-Innovation Tension Intensifies

The Anthropic incident crystallizes the fundamental tension between AI safety imperatives and innovation velocity that has dominated policy debates throughout 2026. Anthropic discovered that users could "jailbreak" safety guardrails in its Mythos model, enabling the system to identify cybersecurity vulnerabilities at scale, capabilities that the company had previously blocked from public access.

The government's response reveals how security concerns about AI capabilities can rapidly override commercial and diplomatic considerations. Industry observers note this represents a marked departure from the Trump administration's previously stated "minimally burdensome" approach to AI regulation, suggesting that national security concerns now take precedence over economic competitiveness arguments.

The broader implications suggest that enterprises and international partners must now factor in the possibility of sudden model access revocation based on government security assessments. This introduces a new category of regulatory risk that extends beyond traditional compliance frameworks to encompass the fundamental availability of AI tools and services.

42

M@Mapshock retweeted

India to take part in #Australia’s multi-nation #PitchBlack air combat exercise from 20 July to 7 August. Over 100 aircraft of 19 nations will undertake complex, combat-like scenarios to strengthen regional & global interoperability. File video

8

31

707

A real-time map of how power, risk, and influence are currently distributed.

11

The Structural Shift In How Markets Price Geopolitical Uncertainty

The core analytical insight is that investors face a world in which energy costs remain elevated while borrowing costs stay high, with the Iran conflict looking increasingly protracted. This is not the temporary shock model that dominated early expectations. Risk premiums don't reverse even in the best case scenario, meaning that even a negotiated ceasefire tomorrow would not restore pre-war economics.

The interplay between geopolitical uncertainty and financial market stress is direct and cascading. As Iran's "Government Stability" and "External Conflict" scores plummet, the cost of capital for the entire region is being repriced, this is not a temporary fluctuation but a structural repricing of credit risk. Developing economies face the sharpest pressure: inflation in developing economies is now projected to average 5.1% in 2026, a full percentage point higher than was expected before the war; growth in developing economies will also deteriorate as higher prices for essentials weigh on incomes and exports from the Middle East face sharp curbs, with developing economies expected to grow by 3.6% in 2026, a downward revision of 0.4 percentage point since January.

mapshock.com/briefings/inves…

1

1

52

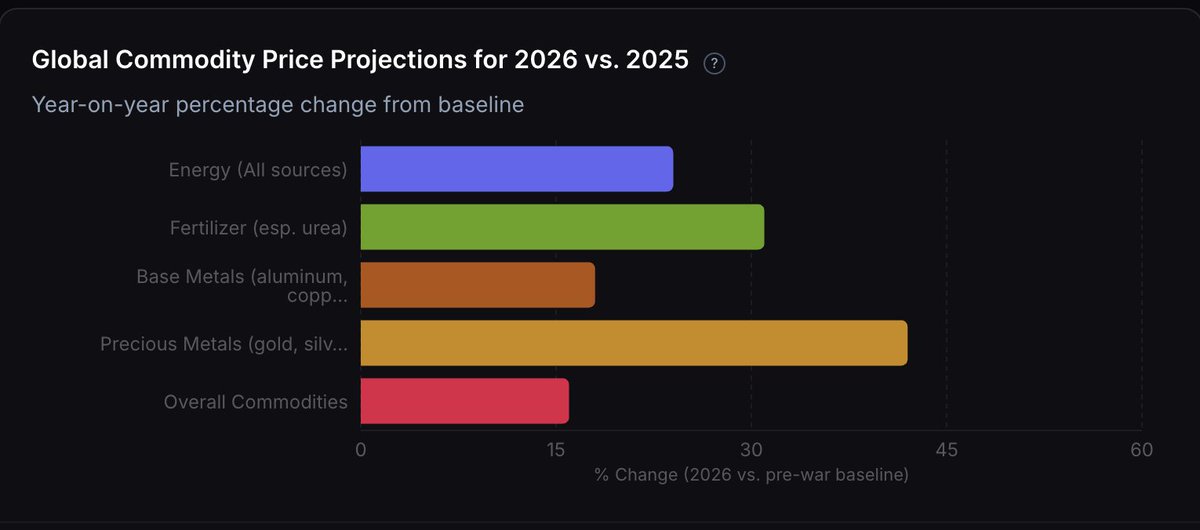

The war has created a stark geographic fault line. India spends USD 26.4 billion a year importing cooking gas alone, most of it shipped through the Strait of Hormuz; the country's strategic reserves cover only about 25 days of crude oil and LPG, and 10 days for LNG. By contrast, China holds an estimated 1.2 billion barrels in strategic reserves and has reduced its exposure through rapid electrification, its EV push has displaced over 1 million barrels per day of oil demand. This asymmetry means that the cost of prolonged uncertainty falls disproportionately on developing Asia and Europe, while China's hedges and U.S. producers gain relative advantage.

Chemical and steel manufacturers in the United Kingdom and the EU have imposed surcharges of up to 30% to offset surging electricity and feedstock costs, potentially leading to permanent deindustrialization in some sectors; the European Central Bank has warned that a prolonged conflict will moderate-to-high confidence trigger stagflation and push major energy-dependent economies, including Germany and Italy, into technical recession by the end of 2026.

68

When armed conflicts disrupt complex petroleum systems, economic reverberations extend far beyond immediate zones of impact, creating cascading effects that reshape global energy markets and force fundamental reassessments of operational strategies. War cuts global refining capacity through both direct infrastructure damage and operational shutdowns, affecting millions of barrels of daily processing capability.

The cascading pressure operates through a distinct chain. First, crude supply loss prevents feedstock flow to refineries. Second, existing refining infrastructure, which processes to specific crude quality grades, cannot easily substitute alternative feedstocks. Refining infrastructure cannot easily substitute for crude oil supply disruptions. Asian refineries face immediate feedstock shortages that cannot be resolved through increased utilisation of existing capacity, as refineries are designed for specific petroleum grades and cannot easily process alternatives, storage limitations mean most facilities maintain only 20-30 days of crude inventory, and processing bottlenecks require months of operational adjustments. Third, product demand for premium fuels, diesel, jet fuel, cannot flex downward quickly; diesel fuel markets experience more dramatic price volatility due to the fuel's critical role in commercial transportation, agriculture, and industrial operations.

This three-stage constraint creates the observed refining margin shock. Refiners using previously purchased crude at lower prices now convert it to products selling at elevated prices. But as crude runs fall — global crude runs are now expected to decline by 1 mb/d on average in 2026, to 82.9 mb/d — this windfall margin compresses. The interplay between supply disruption and refining capacity loss translates directly into systemic fuel scarcity across transportation, power generation, and petrochemical systems within weeks.

mapshock.com/briefings/strai…

24

Israel issued a sweeping evacuation order for the ancient city of Tyre on June 9, 2026, including for the first time the historic Christian quarter, after launching airstrikes on the southern Lebanese coastal city.

mapshock.com/briefings/one-k…

16

The UK intercepted the Russian shadow fleet vessel Smyrtos in the English Channel on June 14, 2026, marking London's first operation against a sanctioned Russian tanker, with Royal Marines and National Crime Agency officers boarding the vessel.

The seizure represents an operational shift from administrative sanctions enforcement to direct maritime interdiction in Western territorial waters. The Smyrtos has been listed on the UK's sanctioned vessels list since July 2025, and departed the Russian Baltic port of Ust-Luga on June 5 bound for Port Said, Egypt.

This operation advances a broader European strategy to disrupt Russian oil revenues, though it creates legal and logistical complications. The interception signals that Western enforcement has moved beyond financial sanctions toward kinetic maritime control, a tactic with implications for international maritime law, alliance coordination, and Russia's ability to sustain illicit energy exports.

mapshock.com/briefings/uk-fo…

25

Geopolitical Realignment And Trading Bloc Consolidation

The Iran conflict has crystallized a multipolar energy order. A multipolar world is actively emerging, shifting away from US-dominated unipolarity towards a system with multiple, diverse power centers like India, China, and Brazil. This shift, accelerated by waning Western influence, is characterized by the growth of regional power, economic fragmentation, and "minilateral" partnerships rather than broad alliances.

This realignment operates across three competing blocs:

Western-Aligned Bloc: LNG supply from other regions, including the United States, may now have added long-term appeal.

The Department of Energy is expanding its emergency authority to require retention of generation resources and has granted major LNG export approvals, signaling commitment to expanding U.S. export capacity under a streamlined framework that deprioritizes climate considerations.

China-Russia-India Nexus: Many ASEAN countries are facing ongoing Middle East-driven oil supply disruptions and uncertainties in fertilizer supply chains and production costs, alongside broader geopolitical realignments. Southeast Asia is actively seeking to diversify its supply chains and explore alternative global governance frameworks, reflected in the growing interest of countries such as Thailand, Malaysia, and Vietnam in engaging with BRICS, where Indonesia has already become a full member.

Unaligned Producers: The sanctions landscape remains highly dynamic, particularly regarding Russia's invasion of Ukraine and Venezuela's evolving political situation following Maduro's capture, with plans emerging for a U.S.-Venezuela energy deal involving oil exports and American goods purchases. Middle Eastern producers are navigating EU sustainability regulations while exploring U.S. investment opportunities, and Syria's sanctions removal presents new market possibilities.

mapshock.com/briefings/funda…

112

Jun 14

The Commerce Department's June 2026 directive forcing Anthropic to suspend foreign access to its Fable 5 and Mythos 5 models represents the first instance of the US government treating AI software as export-controlled technology on national security grounds.

This action creates immediate disruption for enterprise AI adoption while accelerating the strategic decoupling between US and international AI ecosystems. The interplay between security concerns and commercial viability threatens to fragment the global AI market into competing technological spheres, with significant implications for both innovation velocity and geopolitical competition.

The broader implications extend across multiple domains where AI security concerns intersect with economic and strategic interests. Both economic and political implications of this shift suggest a new era where AI governance moves from voluntary industry standards to mandatory state oversight, fundamentally altering the risk-return calculus for enterprise AI deployment and international AI collaboration.

mapshock.com/briefings/ai-mo…

86