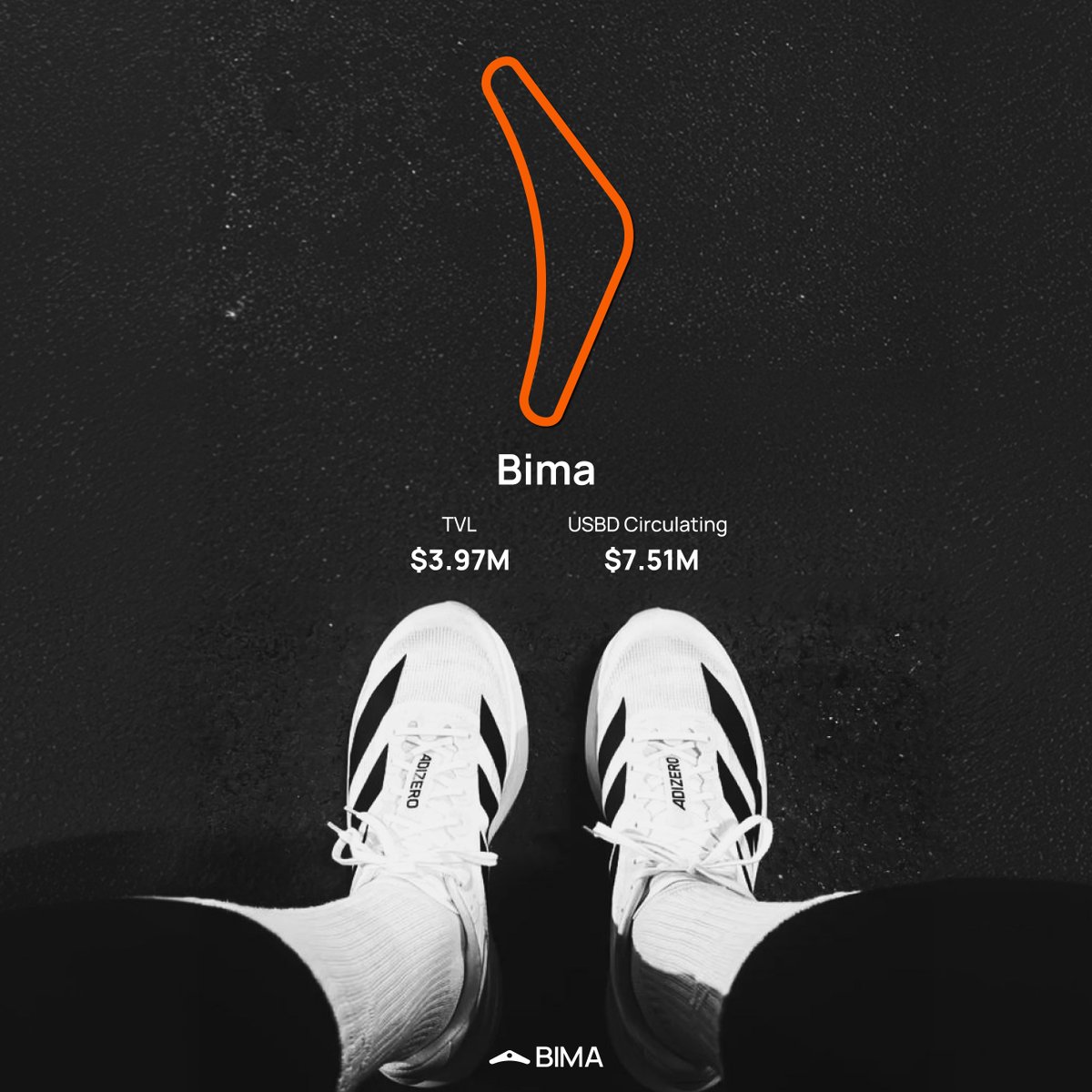

Borrow against your Bitcoin. Earn yield on USBD. Backed by @portalventures and more.

Joined May 2024

- Tweets 8,316

- Following 113

- Followers 139,312

- Likes 3,522

635 Photos and videos

Markets evolve when the rails evolve.

A foundation like this is what institutional flow has needed all along.

Congratulations to the team, full (light)speed ahead!

Apr 22

Lightspeed Is Now Live

The speed of a traditional exchange

The composability of a decentralized exchange

The privacy for real world exchange

3

9

19

937

Pull up at 8PM UTC if you’re watching.

discord.com/invite/WgR5kMz3H…

171

649

BIMA retweeted

Mar 12

DATs are becoming the new grift, and the funniest part is that it actually works.

Here is the playbook. You take a dead or dying DeFi protocol. No users. No traction. No product. It is basically a warm corpse with a token chart attached. Then you pivot into a DAT.

Most people have no idea how NAV-based assets really work. A DAT is essentially a bundle of NAV-denominated instruments wrapped in a marketable equity shell. Preferred equity, bond-like payouts, capped upside, predictable distributions. Nothing wrong with that. It is a legitimate structure. But in crypto, it has become the perfect vehicle for zombified teams to reanimate themselves.

The formula is simple. Acquire a management vehicle with a listing. Fold your failed project into it. Take the management cut. Then port pieces of the equity onto chain as “assets.” Custody it somewhere credible. Create internal loops that inflate the apparent TVL. Then walk into the market raising on the story of “institutional NAV flows.”

And it works. People who could not raise a Series A are suddenly “raising a DAT.” Forks with no users are landing eight-figure exposure commitments. The NAV wrapper becomes a credibility multiplier. The listing becomes the marketing. The chain integration becomes the pitch. The whole thing self-funds.

Is this bad? Maybe. Maybe not. This is how financial engineering has worked for decades. Crypto is just discovering it.

But founders need to understand the truth: you are not going to make real money from DeFi at institutional scale. DeFi is a democratization layer for retail. It is not designed for corporate treasuries, asset managers, or balance sheet allocators. No serious institution wants to touch an AMM, farm a points program, or LP in a pool with reflexive risk.

The real game is NAV. Equity. Credit. Yield. Productive assets. DeFi is the front end. TradFi is the engine. DATs are simply the newest bridge between the two, and like every bridge, it attracts the zombies first.

1

1

184

899

Kickoff's at 20:00 UTC.

Where will you be watching the match from? 🟠⚽

discord.com/invite/WgR5kMz3H…

184

634