ScamBinance.Com - All about the crimes and violations of the Binance casino and the crypto cartel. Run, from the Binance Submarine.

Joined January 2021

- Tweets 6,360

- Following 435

- Followers 949

- Likes 56,424

215 Photos and videos

15 Jun 2023

Someday, Tether will lose its $1 peg and... not get it back, but not today- theblock.co/post/234822/teth…

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

1

7

421

15 Jun 2023

#HaruInvest is suspected of transferring client funds to FTX without their knowledge.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

Haru Invest used FTX, as reported by OXT Research.

If this is true, they remained silent about it to customers throughout the year after FTX's collapse. Sigh.

2

462

15 Jun 2023

HSBC and Standard Chartered pressed by Hong Kong regulator to take on #crypto clients - ft.com/content/da31d2d6-e547…

#BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #regulation #GMT #TUSD #GuangyingChen #HeinaChen

1

1

3

346

14 Jun 2023

Talking heads don't understand where the problem comes from. Complete idiots.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

LARRY FINK: AI MAY BE THE TECH THAT BRINGS DOWN INFLATION

5

364

14 Jun 2023

I've been digging through Binance's crap since 2018 and claim they are financial criminals.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

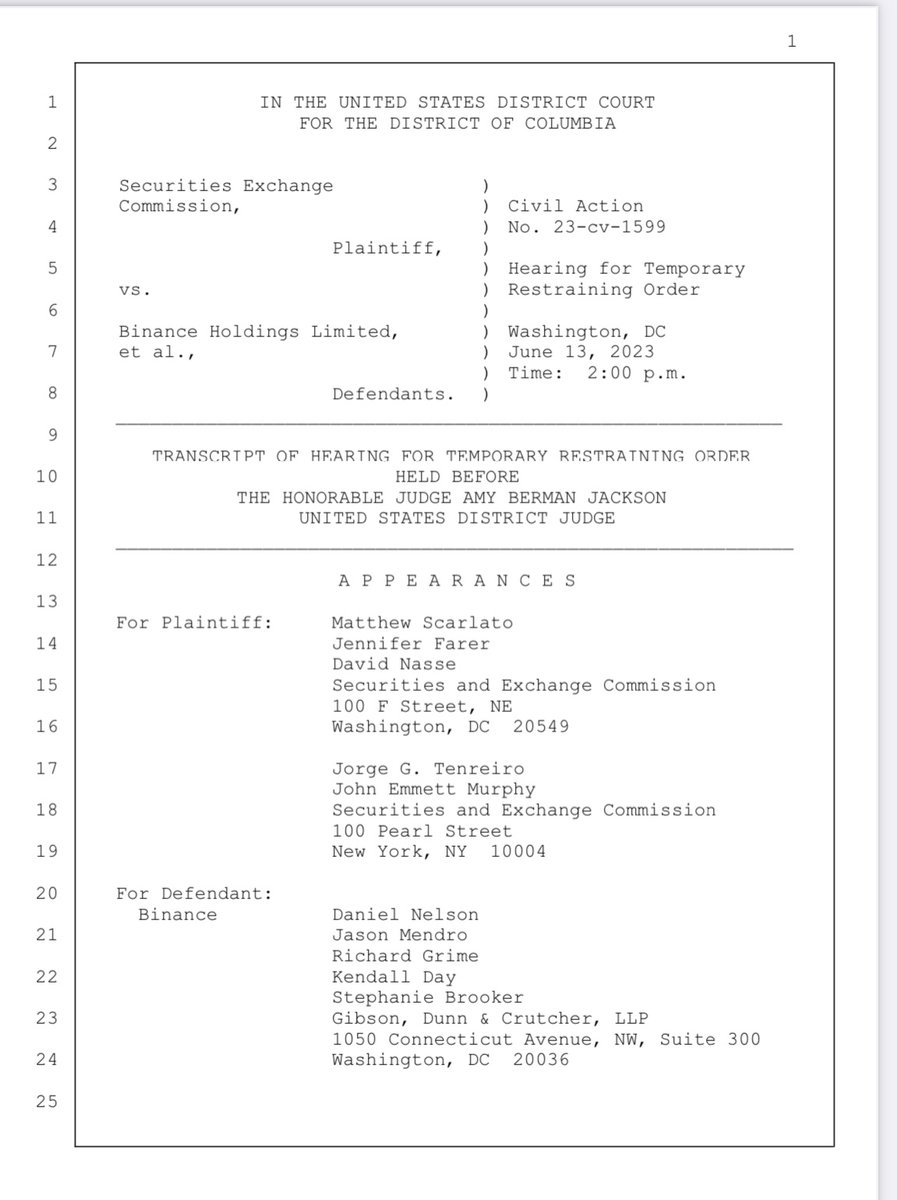

Some are arguing that the judge in the SEC/Binance case expressed skepticism about the S.E.C.’s use of its enforcement powers to regulate the crypto world, calling it “inefficient and cumbersome.”

That might be true, but having now read the transcript of yesterday’s hearing before Judge Amy Berman Jackson, and placed it all in the proper context, not sure I can agree. (Read it for yourself at: johnreedstark.com/wp-content…)

Regularity Clarity (The Lack Thereof) As a Defense

The lack of regulatory clarity in the cryptoverse is the number one talking point of crypto-enthusiasts and has become a fintech lawyer defense rallying cry.

However, as evidenced by these two exchanges with Judge Butler in the SEC/Binance matter, not only is the "regulatory clarity" argument more suitable for Congress, but it is also an argument that is irrelevant:

Judge Jackson: “All right. Now, the defendants say, well, this is a big broad area that is generally unregulated at this point, you should be proceeding by rule making. No one seems to be saying let's see what congress gets around to doing. Why is it prudent, from the Commission's point of view, to assign the determination that would have such far-reaching effects in a billion dollar industry to a lone federal district judge, especially when there's another lone federal district judge in a parallel action who could rule the other way? It seems like an inefficient and cumbersome way to establish a national, consistent, understandable policy for the regulation of trading in crypto assets. Now, I'm not sure on what basis the defense says, well, you should tell them that they should have exercised their discretion to do a rule making, because I don't know that I have the power to do that and I imagine you would tell me that I don't. But, still, the question is, why -- why does it make sense to go this way?”

SEC: “Because this is the law, Your Honor. The Howey test has been around since the 1940s. And, you know, we tried to interact with these entities to, you know, figure out a plan. The technology was new. The rules are longstanding and anything but new, Your Honor, and defendants knew the rules. You know, Your Honor says this wasn't -- many of our claims are not scienter based. But, you know, as we allege, there are many things that the defendants have said that acknowledge they knew these were the rules and they just chose not to follow them. So at a given time the SEC can try to interact with these entities to come to a resolution or try to do rule making. Yes, there's lots of things the SEC could do, but the enforcement arm is here, too, and when we see the law is being violated, we have to act on it.”

--------------------------------------

Judge Jackson: “. . . you [defense counsel] argue and your argument has some force, that these kinds of complex legal and financial issues are better resolved through regulation or rule making than through test case litigation, but I don't run the executive branch. So what would be the authority under which I could say, as you suggested, no, I'm sorry, you've exceeded your that discretion, you must proceed by rule making here. How is that in my lane as a member of the judiciary?”

Defense Counsel: “If we made that statement, that's not what I'm arguing today. I think that it is something -- it may well be in the brief, but I think that that's -- we're not asking you to deny it on that basis.”

Based on yesterday’s SEC/Binance hearing, my take is that the parties will work out an agreement during mediation with the magistrate judge (designated as Magistrate Judge Zia M. Faruqui), though Judge Jackson may have to step in to decide what constitutes "ordinary business expenses” and other micro-issues that remain in dispute.

This agreement will be entered into the court as a "consent order" and alleviate the need for a TRO and preliminary injunction -- and most of all, protect investor assets in the U.S.

A robust and meticulously drafted consent decree gives the SEC pretty much all of the relief the SEC has asked for and will also allow Judge Jackson to preserve the status quo and manage the discovery process, motions, and trial at an expeditious but more traditional pace.

1

2

189

14 Jun 2023

Binance Seeks to Withdraw Cyprus' Unit Crypto Service Registration - coindesk.com/policy/2023/06/…

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

2

1

5

428

14 Jun 2023

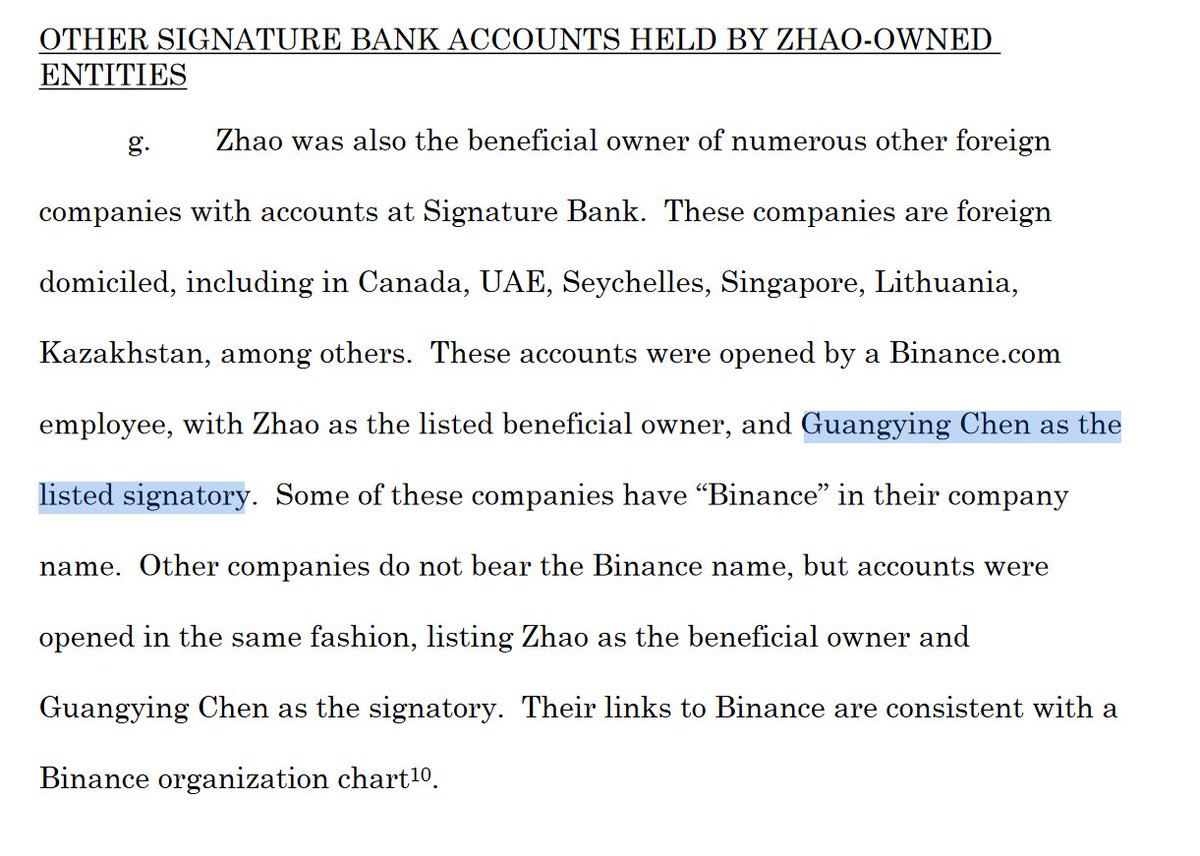

#GuangyingChen hid for a long time. But her ears have been sticking out of #Binance since the beginning. The world needs heroes.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #FTT #NFT #SOL #Bitcoin #CBDC #Meta #PEPE #DeFi #regulation #TUSD #HeinaChen

14 Jun 2023

🚨Read our exclusive @Forbes investigation on Guangying Chen, the Binance executive described by some as the firm's 'real CFO' and by others as CZ's 'personal finance manager.'

From @giacomotognini @DavidJeans2 @SarahNEmerson @SchwabKatharine and myself.

forbes.com/sites/johnhyatt/2…

7

391

14 Jun 2023

BNB crap cost = 0.

#Crypto #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

The native token of Binance, crypto’s largest exchange, has snapped a slide that stoked nervousness among digital-asset investors trib.al/oRs15UF

3

296

14 Jun 2023

#ETH for sale.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

🚨 🚨 🚨 🚨 🚨 🚨 🚨 🚨 🚨 🚨 149,999 #ETH (261,949,642 USD) transferred from unknown wallet to #Coinbase

whale-alert.io/transaction/e…

1

128

14 Jun 2023

SEC & Binance.

Regulator against financial swindlers and swindlers.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

13 Jun 2023

SEC/Binance Newsflash: Dueling Consent Orders (Read Them Now)

The SEC and the Binance defendants have each submitted draft orders of what each party wants the Judge to order in the SEC/Binance Emergency Asset Freeze Enforcement Action.

There is obviously a lot of conflict between what each party argues – but that does not mean the judge cannot order a compromise and find common ground, line by line, of the dueling proposed orders. We may even learn by COB today of a temporary outcome. Or the judge could seek further briefs, order another hearing or take any other action the Judge deems appropriate.

This is all happening in real-time and very difficult to predict.

The Proposed Orders

Here is what the SEC believes is wrong with Binance’s Proposed Order:

SEC Redlined Proposed Stipulation And Consent Order at johnreedstark.com/wp-content…

Here is what the SEC wants the Judge’s Final Order to look like:

SEC Proposed Stipulation and Consent Order at johnreedstark.com/wp-content…

Here is what the Binance defendants wants the Judge’s order to look like and where the Binance defendants believe the SEC is wrong:

Binance Defendants Redlined Proposed Consent Order at johnreedstark.com/wp-content…

3

361

14 Jun 2023

U.S. House panel to vote on cryptocurrency bill in coming weeks: lawmaker - reuters.com/technology/us-ho…

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

1

1

5

316

14 Jun 2023

And criminal prosecution. Then it will be too late.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

14 Jun 2023

When is everyone going to realize that the SEC isn’t what #Binance has to worry about, but rather the DOJ. Take a seat. Few understand this.

1

3

367

13 Jun 2023

Crypto industry and scammers against regulation. they want the Wild West. But it won't, get used to it.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #TUSD #GuangyingChen #HeinaChen

13 Jun 2023

It’s absolutely unconscionable that a regulator – when presented with so much pushback on what he was about to say / how he compiled this fake “test” in the first place – decided to move forward anyway, and throw an entire industry into chaos.

1

4

444

13 Jun 2023

#Binance is using criminal money to save itself and its beneficiaries. They don't want to live like #SBF.

#Crypto #BNB #cz_binance #BTC #CZ #FTX #USDC #ETH #USDT #DOGE #Tether #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #PEPE #DeFi #regulation #GMT #TUSD #GuangyingChen #HeinaChen

12 Jun 2023

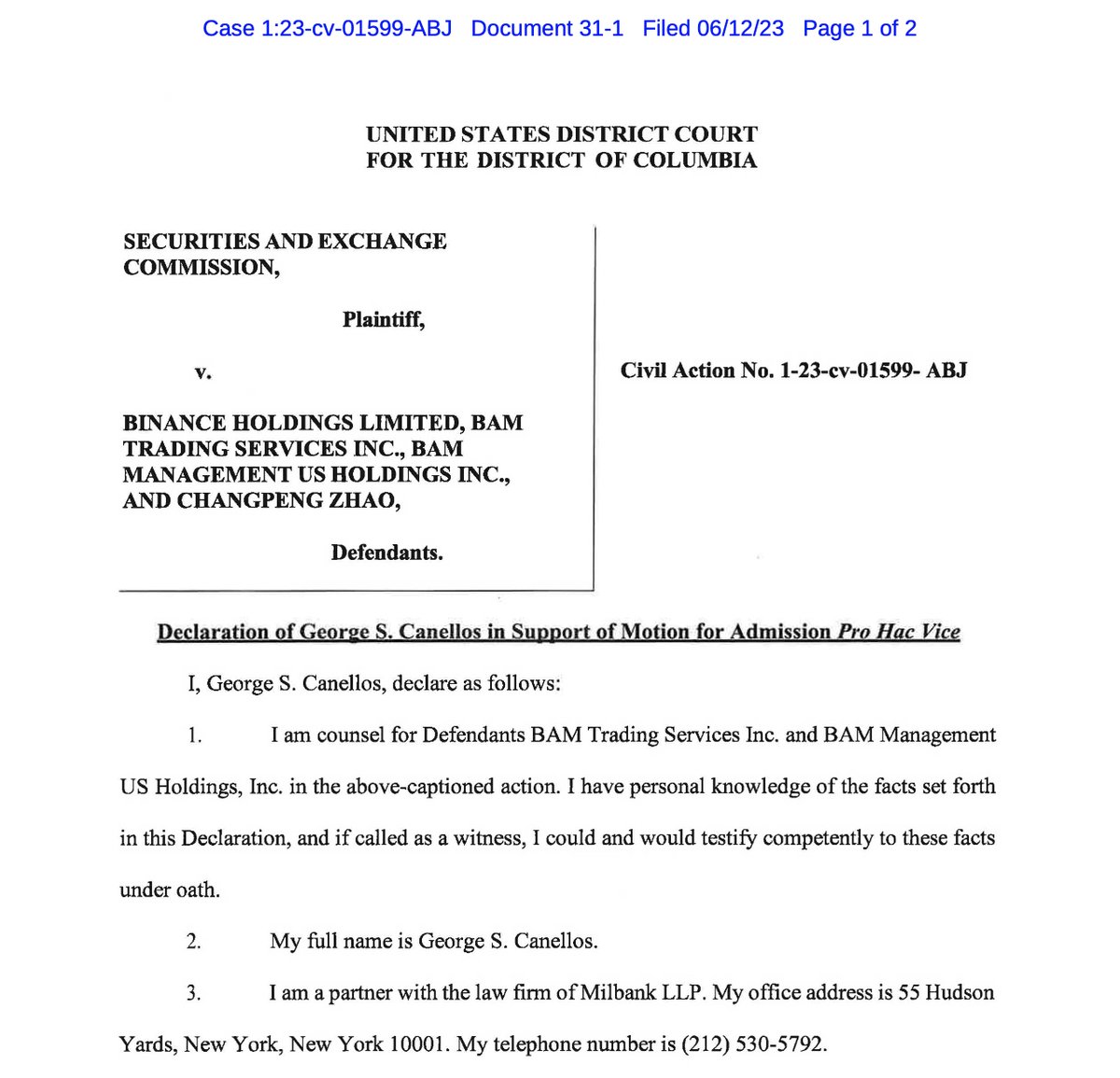

Binance/DOJ Newsflash:

Binance and CZ just added a uniquely qualified criminal defense all-star lawyer to their legal team: George Canellos, former Chief of the Major Crimes Unit in the U.S. Attorney's Office for the Southern District of New York and former head of the SEC's New York Office and former SEC Enforcement Division Co-Director.

Canellos posesses a rare and remarkably special combination of skillsets -- having served as both an SEC prosecutor and a DOJ prosecutor. Think Liam Neeson meets Perry Mason.

Binance is clearly preparing for a criminal prosecution and continuing to hire the best defense attorneys in the world. But I doubt even Ironman, Captain America and the Hulk could get Binance out from their current perilous legal quagmire.

3

383

13 Jun 2023

#BrianBrooks, the second CEO of #BinanceUS - Knew nothing, controlled nothing, #CZ and China (#HeinaChen) ruled everything.

#Crypto #BNB #cz_binance #BTC #FTX #USDC #ETH #USDT #DOGE #Tether #Binance #FTT #NFT #SOL #Bitcoin #CBDC #Meta #AI #regulation #GMT #TUSD #GuangyingChen

13 Jun 2023

5

392