Joined April 2018

- Tweets 5,081

- Following 67

- Followers 451,856

- Likes 647

764 Photos and videos

Jun 12

The largest IPO in history prices this week. Most of the world can't participate.

Primary markets were built for institutions. Retail enters after the premium is already gone.

On-chain pre-IPO infrastructure exists to close this gap. Find out more ⬇️

binance.com/en/research/anal…

100

28

150

43,721

Jun 12

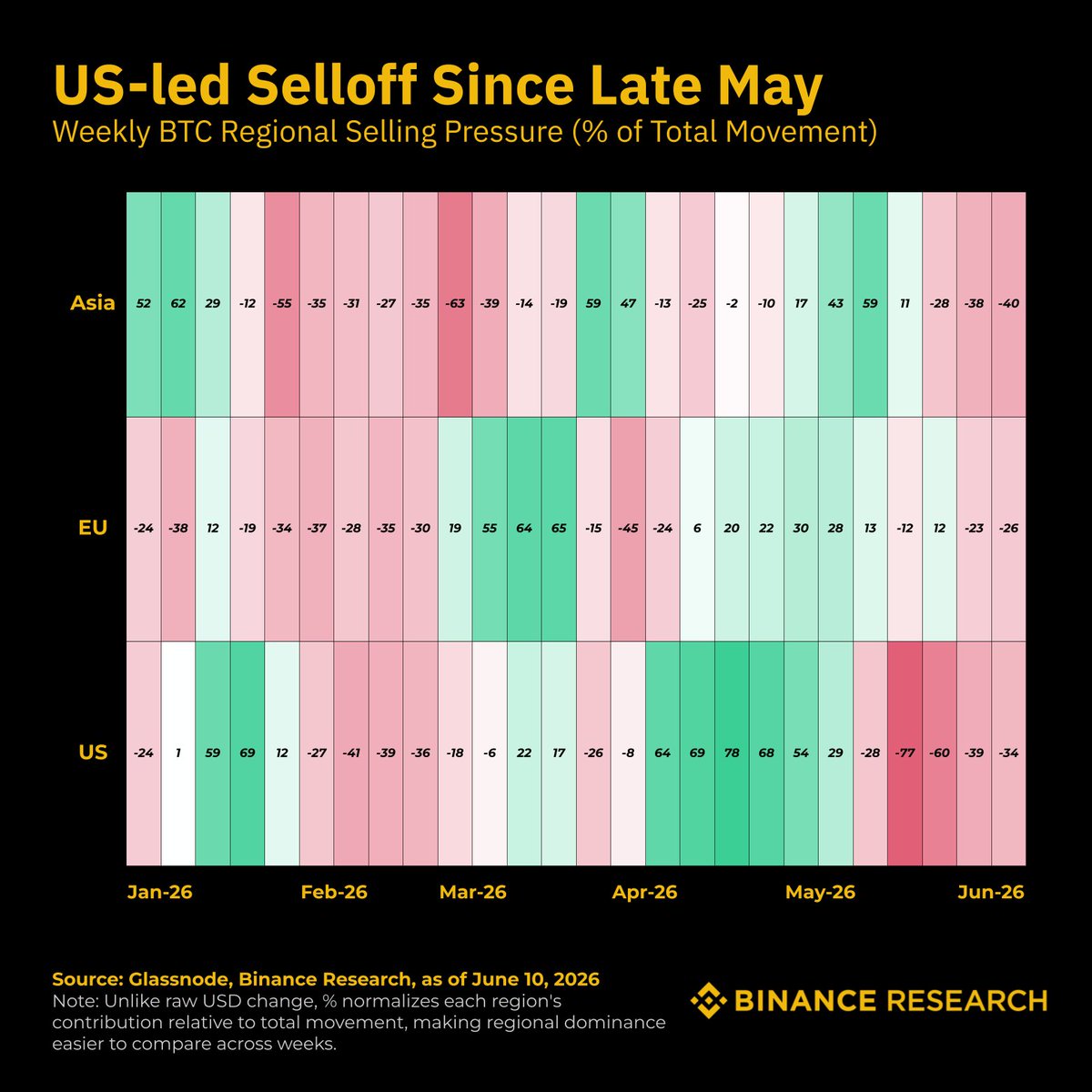

US-led selling pressure has dominated BTC since late May, with US selling pressure hitting -76.6% in May W4, the weakest reading YTD. Asia and the EU stayed balanced throughout.

Key drivers from industry:

🟠 Worst monthly ETF outflows YTD — 4 consecutive weeks, US$2.4B left in May

🟠 Strategy first BTC sale since 2022 — while sitting on ~US$11B unrealized losses across 843K BTC

The move is being amplified by a tougher macro backdrop:

🔴 Inflation accelerating — May CPI hit 4.2%, up from 3.8%

🔴 Payrolls still hot — 172K vs 80K expected

🔴 Full hawkish reversal — 4 cuts priced at start of 2026 → ~2 hikes by early 2027

🔴 Capital rotating out — AI equities correcting, SpaceX IPO competing for flows

With ETF outflows, hawkish repricing, and Strategy's sale now priced in, the focus shifts to when demand returns and what crypto-native or policy catalysts could drive it.

7

4

10

19,338

Jun 11

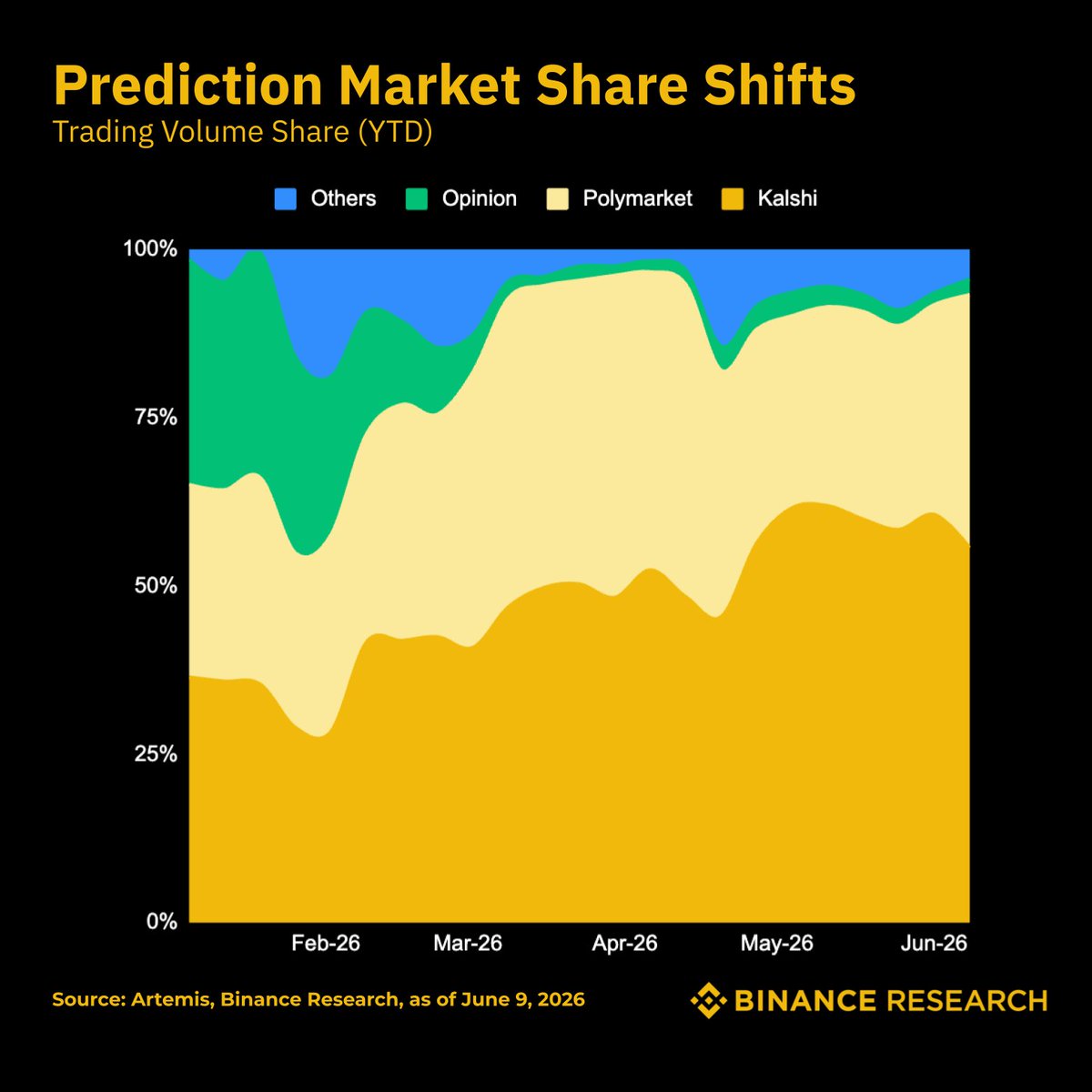

World Cup season is pulling prediction markets to another ATH. US$31.2B in May notional volume, up ~15% from ~US$27B in January.

What began the year as a competitive field has consolidated into a two-platform market:

🔸Kalshi: $18B (58%)

🔸Polymarket: $8.8B (28%)

🔸Others: ~14%

The growth is also broadening beyond event speculation. Industry-wide open interest hit $1.3B, and Polymarket created 520K new markets in May alone, up 50x YoY across stocks, commodities, sports, and AI. Both regulation and distribution remain key growth vectors.

6

2

12

1,992

In its first week, Binance equity trading already hit ~2% of TradFi-referenced perpetuals volume.

For context, crypto spot-to-perps has historically run around 15%. That's the convergence target.

But the bigger picture is structural:

→ Equity trades settled in stablecoins

→ Crypto, equities, payments, and P2P transfers — one account

→ No fiat ramps. No separate platforms. No friction.

Crypto exchanges aren't just crypto exchanges anymore.

They're integrated financial platforms. And the 2026 growth trajectory across both direct and derivatives TradFi products is only getting started. (5/5)

3

4

981

Binance equity trading just launched. Here's what the first week of data tells us: 🧵

Users aren't randomly buying stocks — they're expressing a view.

💻 57% of sector allocation went to Information Technology.

💹 Funds & ETPs at 20%.

📱 Communication Services 11%.

🏦 Financials 9%.

Zoom in further: semiconductors and hardware alone captured ~44% of total fund inflows.

It's conviction in the AI infrastructure trade — chips, hardware, the picks-and-shovels layer.

Binance users came in with a thesis. (1/5)

1

2

18

2,660

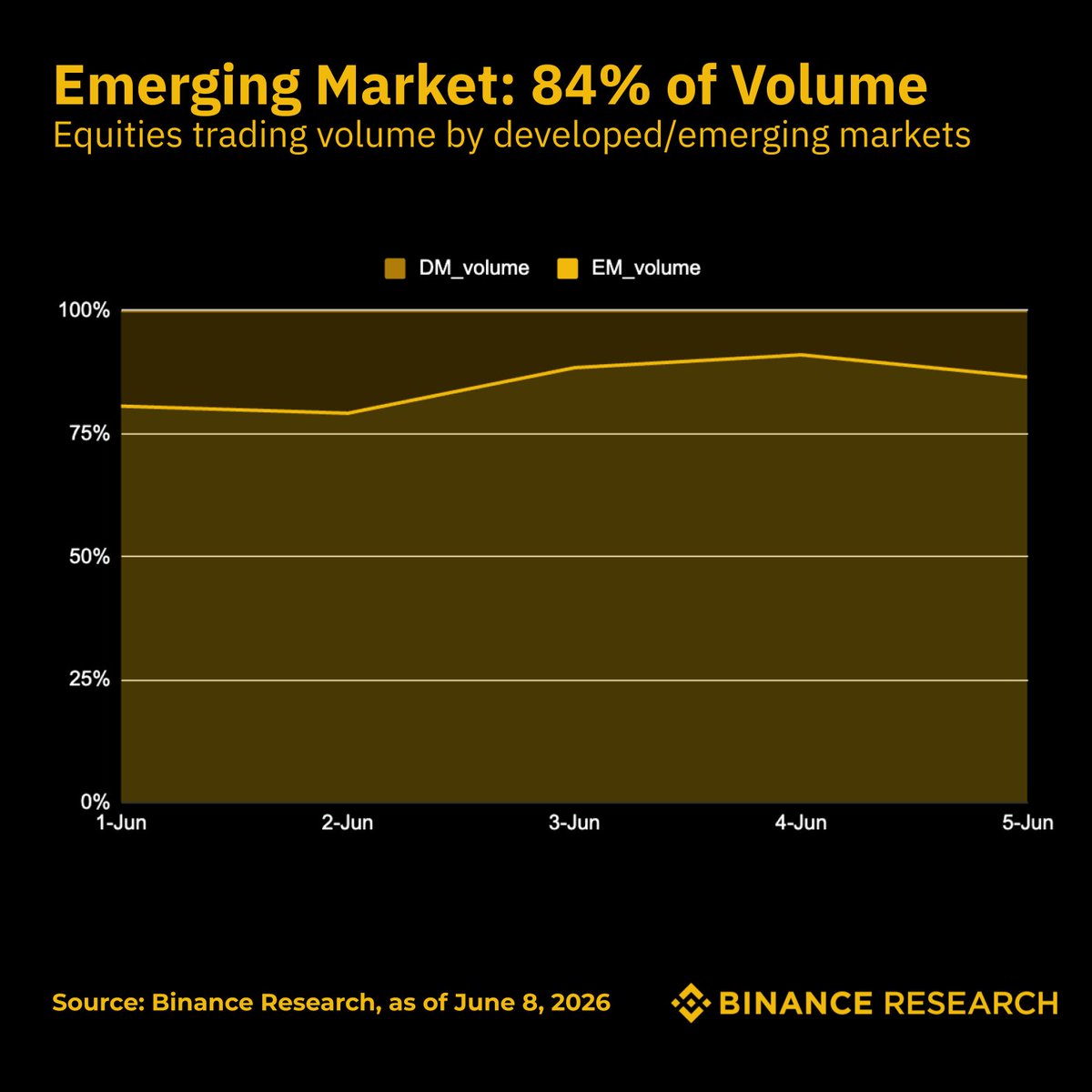

~84% of Binance equity trading volume came from emerging markets. And that figure held steady all week.

This isn't a spike. It's structural demand.

Users who previously faced barriers to US equity markets — now accessing stocks directly via stablecoins, no fiat on- and off-ramps required.

Binance equity trading isn't just a new product. For most of its users, it's a new level of access. (4/5)

2

4

667

Time to explore June's market insights!

Discover key insights on:

🔸 Sector Narratives vs BTC

🔸 Crypto Flows Turn Bond-Like

🔸 RWA Growth Beyond Treasuries

🔸 Crypto Card Volumes vs Stablecoin Float

...and more.

Read here ⬇️

binance.com/en/research/anal…

2

3

12

3,153

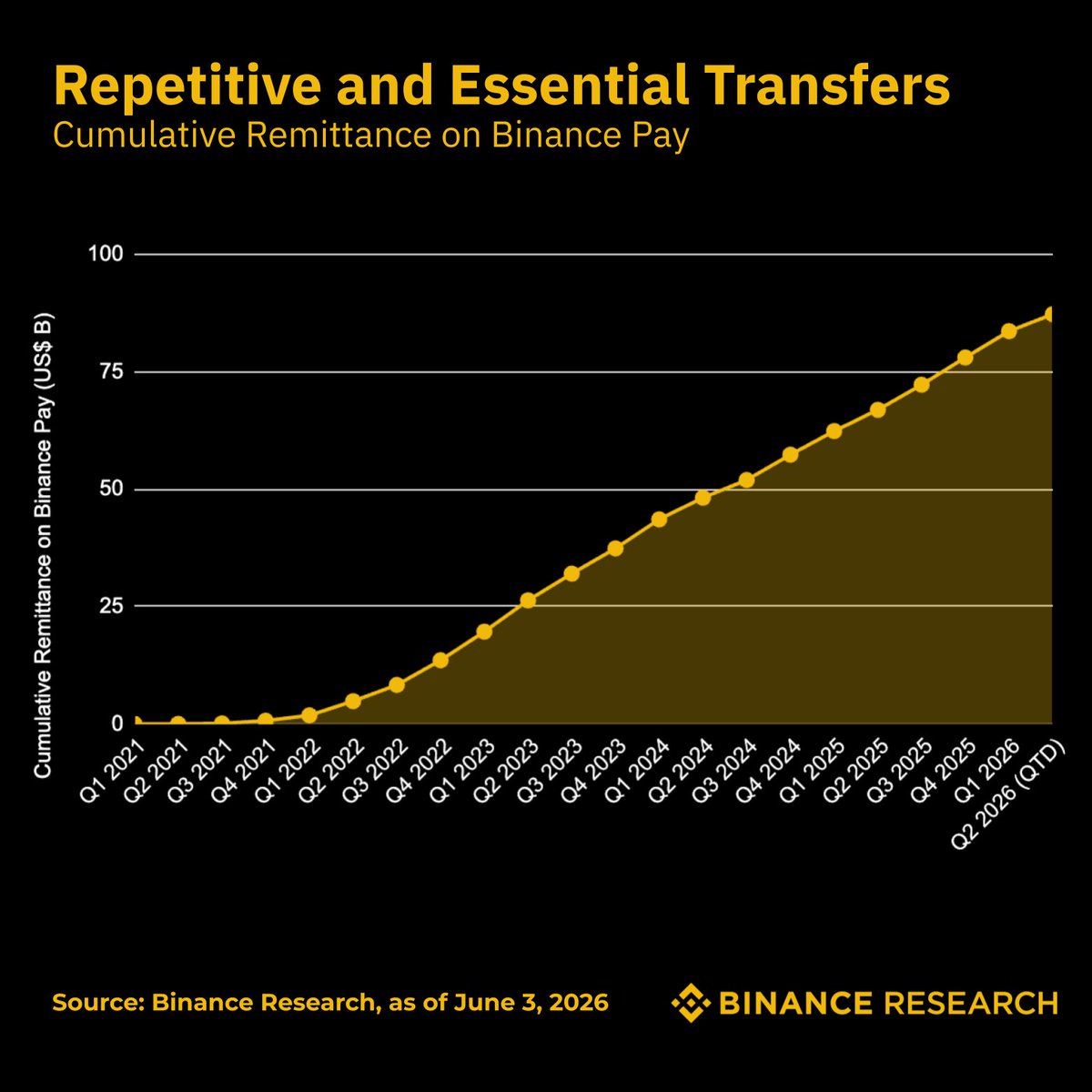

US$87B in cross-border transfers. 34M users. Near-zero fees.

At the World Bank's average remittance cost of 6.36%, stablecoins have saved Binance Pay users over US$5B.

That's US$5B in fees that remained with senders rather than intermediaries.

Cross-border transfer isn't a future use case for stablecoins. It's already happening at scale.

16

7

49

4,249

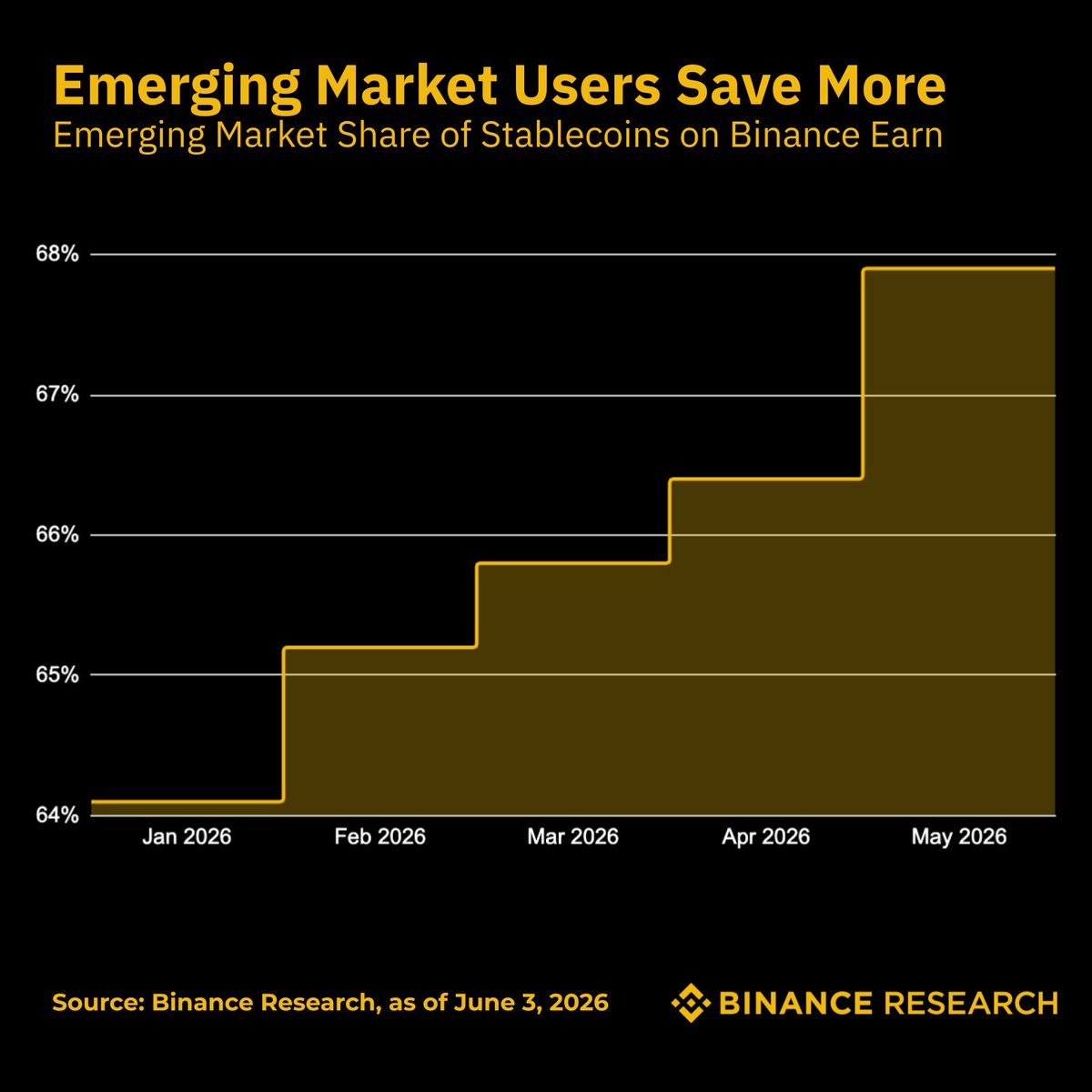

In emerging markets, stablecoins aren't a crypto product. They're a financial lifeline.

Where local currencies are volatile and inflation erodes savings, stablecoins offer something simple: a reliable way to preserve wealth.

And users aren't just holding them. They're putting them to work. Emerging market users' share of stablecoin deposits on Binance Earn has climbed from 64% to 68% in 2026 alone.

Hard-earned money, actively protected.

7

11

42

3,539

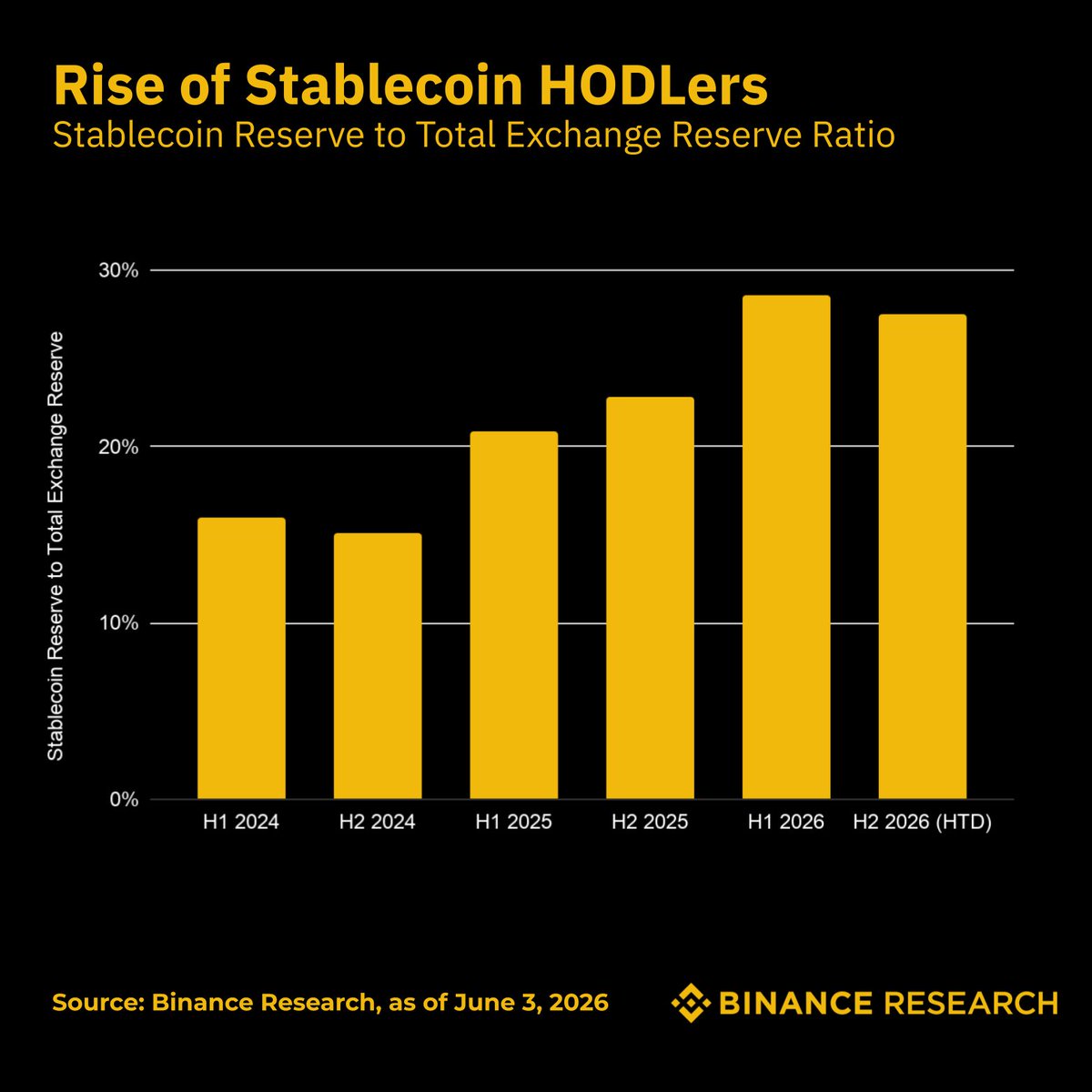

Stablecoin reserves on Binance have risen from 16% to 28% of total holdings.

This isn't a risk-off rotation. It persists across market cycles.

People aren't just parking stablecoins between trades anymore — they're holding them intentionally: for yield, for payments, for transfers, as a store of value.

Stablecoins have quietly outgrown their original use case.

3

11

29

2,618

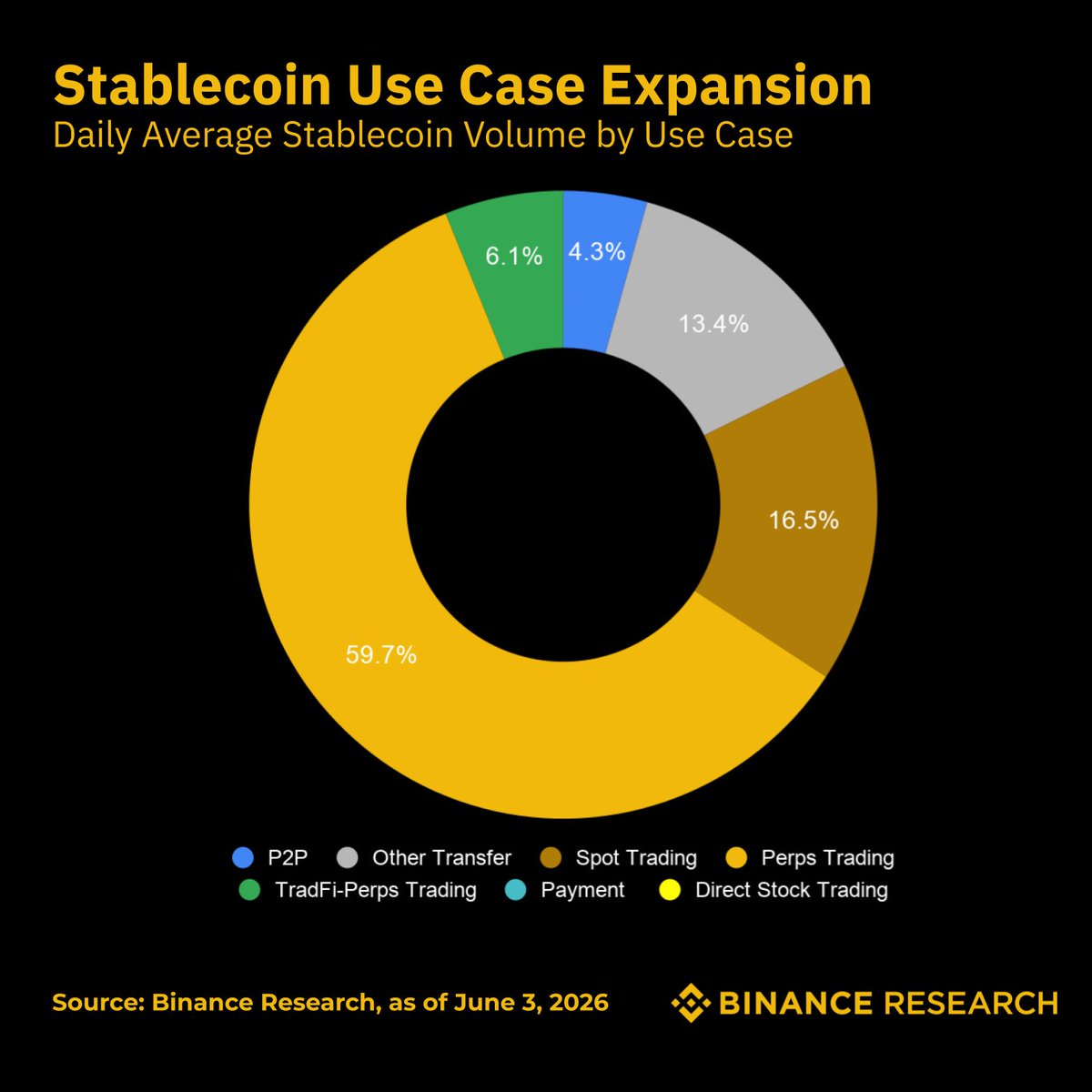

Stablecoins were a crypto trading tool.

Then: payments. Cross-border transfers. P2P remittances.

Now: settlement currency for direct/tokenized stocks and TradFi perps — trading 24/7 on-chain.

TradFi-linked perp volume settled in stablecoins: 6.1% of total stablecoin volume, reached in 6 months.

The addressable market is larger than stablecoin supply itself. This is still early.

8

7

28

4,345

The next 300 million equity investors are coming from emerging markets.

They'll be onboarded through crypto exchanges, settling in stablecoins, trading 24/7.

We mapped the US$2T opportunity in our latest report on direct stock trading and tokenised equities 👇

binance.com/en/research/anal…

5

7

44

5,560

1/5

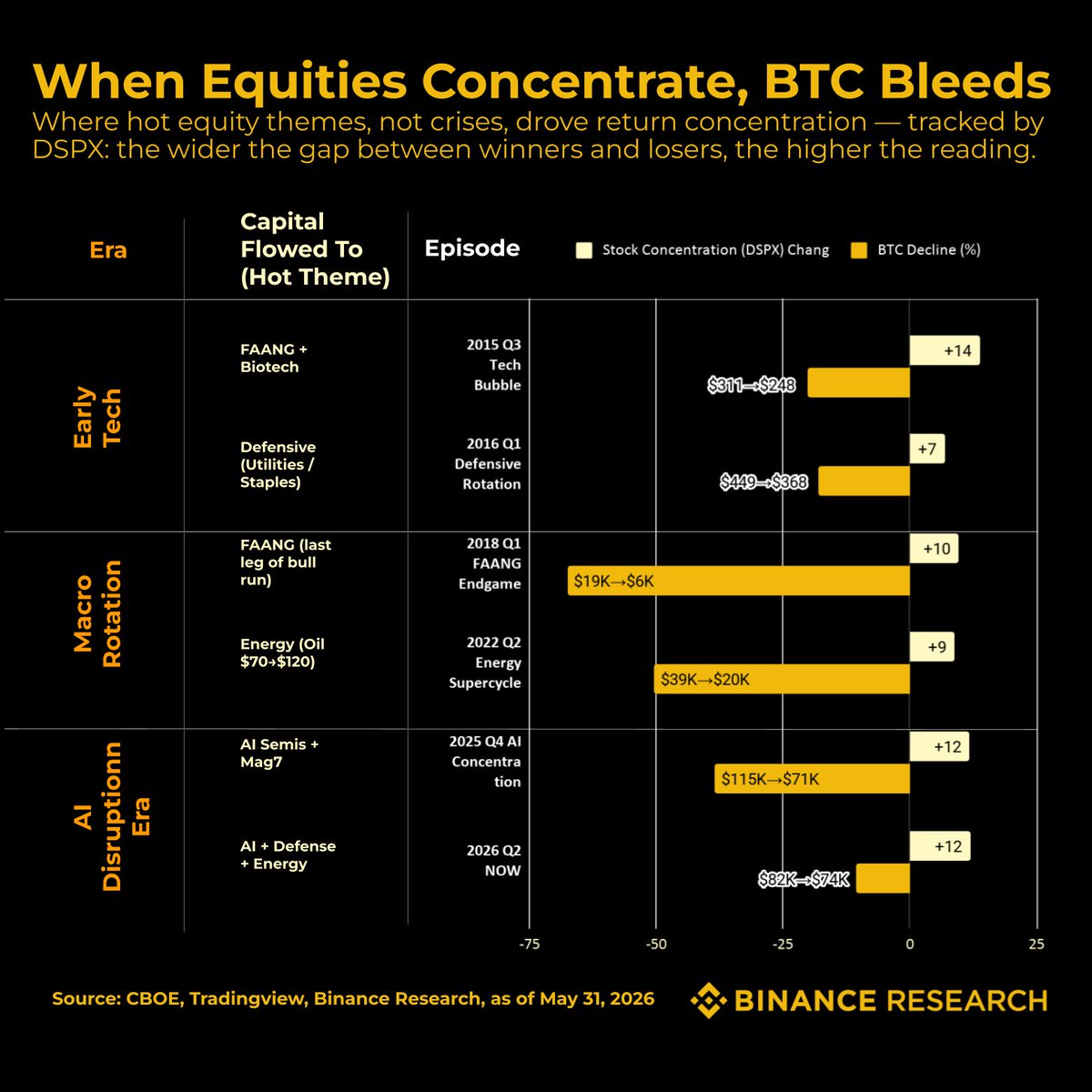

Why is crypto weak lately? The answer may not lie in crypto itself — but in equities.

CBOE Dispersion Index hit 42 — 3rd highest ever. It means extreme capital concentration within the S&P 500. When a few hot themes absorb all the flows, BTC gets sidelined. 🧵👇

4

7

35

6,301

4/5

BTC faces its strongest multi-theme capital diversion ever:

growth capital → AI infra & application

geo-hedge capital → defense/energy

inflation hedge → commodities

Sidelined on all three fronts.

1

1

8

1,623

5/5

But historically, after every DSPX peak, BTC recovered. In pure concentration cases (no crypto-native crisis):

BTC bottomed in 0-20 weeks

Median: 2 weeks

Capital diversion is temporary. Currently no crypto-native crisis. Expect faster recovery.

2

14

1,418