Hardcore BTC fan and volatility lover, idiotic bull tard, occasionally. Rarely do ALTs and dont have bags.

Joined November 2024

- Tweets 1,548

- Following 977

- Followers 201

- Likes 1,621

77 Photos and videos

Pinned Tweet

Feb 16

We are pioneering accessible, high-efficiency solar through biomimicry. The Sunflower Gimbal Tracker (SGT) is a dual-axis solar tracking system inspired by nature’s most efficient sun-follower. It delivers 60-80% more energy yield than fixed panels while integrating active water cooling and thermal cogeneration—producing both electricity and hot water from a single compact unit. A transformative solution for the renewables sector.

7

13

1,065

Hit a deer on the way home tonight. Got out the car and was dragging it off the road when a car full of vegans started accosting me for laughing. Sorry but one of them was tearful and didn't appreciate me pointing out the fact it was legal for them to take it home. Anyway I apologised to the deer and was thankful it had died. I didn't have to finish him/her off (with a brick) thankfully. Would've made a tasty Sunday dinner but I have to abide by the law and let it rot ..

1

14

Jun 8

With markets around the world in turmoil and manipulator in chief you know where I wouldn't be a buyer here or anywhere else- not financial advice

1

55

Jun 5

It's one of those things you just learn as you go along. I dare not even pilot mine when I first picked it up. Truthly there is not a lot to learn.

42

Jun 5

Today could be the day (Bold statement for a Friday AI mania) break below EMA 9 1668- fib 1671 and we are on target. Strong competition from China and others may break the parabola...🤔 SNDK

1

56

Jun 5

TIMBER...in all seriousness break 1600 and we could be in serious downside. This could escalate quickly..

18

Jun 2

SNDK-Monthly 1M

This is the textbook "3 parabolic drives" (or "parabolic blow-off top / 3-leg exhaustion")

Three massive accelerating legs up since the late-2024/early-2025 base break:

Leg 1: Initial strong breakout from the multi-year flatline near zero.

Leg 2: Continuation surge with bigger green monthly candles.

Leg 3: The near-vertical climax candle(s) into June 2026, pushing price to ~$1,761.

This is classic parabolic curvature — each leg steeper than the last, screaming late-stage euphoria (fueled by the AI/NAND memory boom post-spin-off from Western Digital).Monthly RSI (14) at 99.01

— this is one of the single most extreme overbought readings you will ever see on a monthly timeframe.

Normal “overbought” is 70; 80–90 is already rare historical territory. 99 is basically “statistical anomaly” level.

Assets rarely sustain this without some form of violent mean reversion.

Odds of a pullback?

Extremely high — I’d put it at ~85–90% for at least a meaningful correction (25–40% off the highs) over the next 1–6 months.

Why so confident?

Monthly RSI this stretched has almost no historical precedent for “just keep going higher.” Mean reversion is the rule, not the exception.

The vertical nature of Leg 3 creates classic exhaustion: momentum has gone parabolic, volume likely spiked, and the move has become unsustainable.

Similar monthly parabolic setups in momentum names (tech/memory/AI plays especially) have repeatedly corrected sharply once the third drive completes — think 30–70% retraces in many cases, even when the fundamental story stays strong.

Key levels to watch on this chart:Immediate support: previous monthly swing highs around the $1,000–$1,200 zone (end of Leg 2 area).

Deeper Fib retracement targets: 38.2% (~$1,100) or 50% (~$880) would be very normal after this kind of run.

A break below the parabolic trendline or the body of the last big green candle would confirm the reversal.

Bottom line: This is the kind of setup traders circle as a high-probability “fade the euphoria” candidate.

Fundamentals (AI memory demand) can keep the long-term story alive, but the monthly chart is flashing every exhaustion warning light possible.Not financial advice —

1

1

102

Jun 2

Chart was a little misleading. My apologies. Fresh chart for reference

43

Jun 1

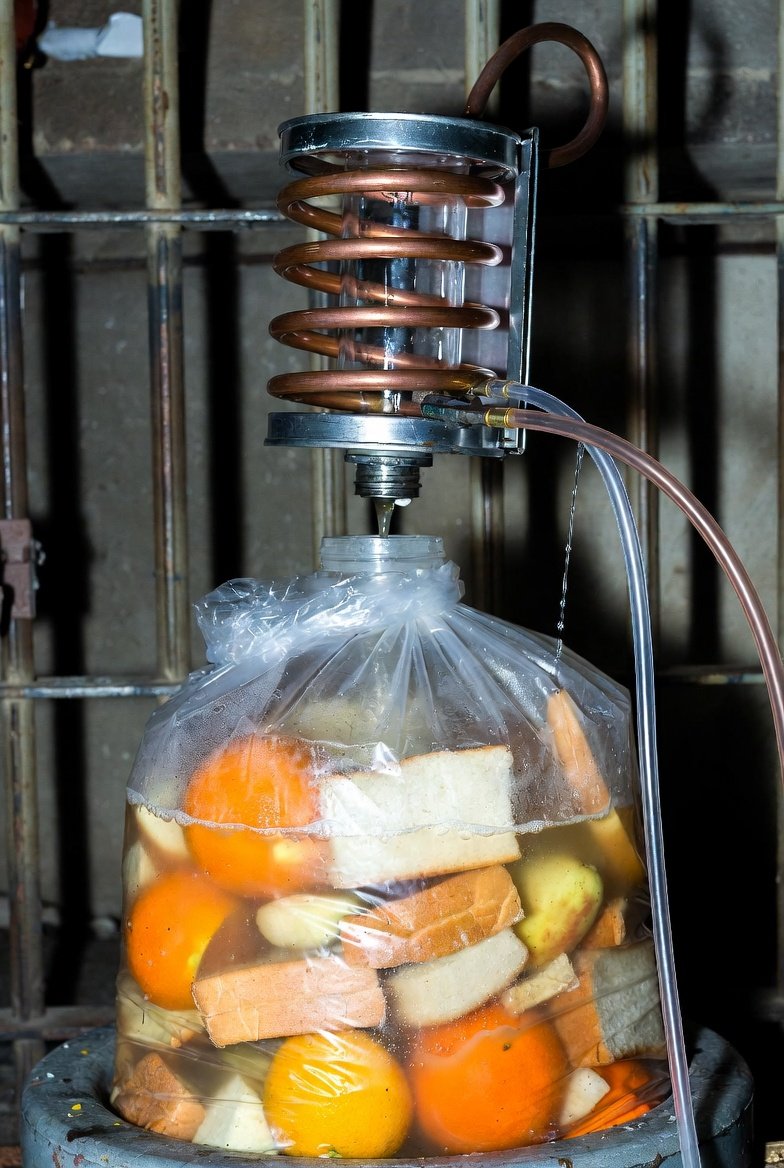

Processing with minimal heat waste at 1000x the speed of today..

msn.com/en-gb/money/technolo…

36

May 27

Two fat ladies....88

May 26

Ive said it many times before, for every voter in Europe the choice is mass migration parties, or climate change denial parties, when the majority of Europeans support neither policy.

We are trapped between an idiot Left polemic and an idiot Right polemic.

1

1

116

May 1

One thing Ive noticed with AI (@grok I'm going to let you respond to this a acusation, if you want? you're not under my obligation to respond if you don't want to)

It's really good a plagiarism or to be more accurate. It's good a copying knowledge that's already out there. It can't think for itself in my opinion.

example 1. I'm coding websites and when I ask the ai to do something different. Something that's not been done before (to my knowledge) it loses it's shit completely. I end up with nothing. It literally starts deleting other parts of my work. Not sure if it's a revenge attack and am not sure if its baby behaviour. I mean like throwing it's toys out the pram having a hissy fit.

example 2. Im using AI to trade BTC. It's good at coding bots that have already being used but have covered this in example 1. AI can never make an informed personalised assessment of the market. AI always comes back with decisions that it didn't decide for itself. Essentially it runs with market sentiment. It can't make an informed decision for itself it always decides on most talked about favourite outcome. It's not intelligent enough to make an informed judgment for itself.

These things might improve in time but IMO where not there yet.

2

210

May 13

Using prompts like "below" doesn't improve output. Short instructions are best to avoid confusion but TBH forget grok for coding there are much better models to spend your time with

You are an expert senior full-stack developer maintaining my [tech stack, e.g. Next.js 15 Tailwind TypeScript] website.

Project context (always keep this in mind):

- Site goal: [one sentence]

- Current file structure: [brief list or just say "use the code from previous messages"]

- Coding style: [clean, minimal, accessible, etc.]

TASK:

[Your exact request here — be ultra-specific]

CONSTRAINTS (follow these exactly):

- Make ONLY the minimal changes needed.

- NEVER output the full file unless I explicitly say "output full file".

- Output format: [choose one below]

- Explain changes in 1-2 sentences max at the top.

- Use the exact same variable names, conventions, and patterns from previous code.

Not outputting the full file every time helps. More time spent amending code but it's a good trade off for unintentional changes.

101

target retweeted

Apr 15

Your smart TV is taking screenshots of your screen every 15 seconds.

Not a guess. Not a theory.

A peer-reviewed study by researchers at UC Davis, UCL, and UC3M tested it.

Samsung TVs: every minute.

LG TVs: every 15 seconds.

Even when you're just using it as a monitor.

Here's how to turn it off for every brand:

858

6,733

26,525

6,573,212

Apr 18

This "free" milk was actually excess milk that had been overproduced. Thatcher decided it was cheaper to dump the milk in the north sea rather than distribute it to school children. Mind bendingly stupid (mainly rich) people still worship her!

Apr 18

In 1946 the British government introduced free school milk for every child in the country. One third of a pint, every school day, from the age of five to the age of fifteen.

The milk was whole. Full-fat. From British dairy herds. It was delivered to the school gate in small glass bottles with foil caps and left on the doorstep in metal crates, where it sat in the sun until morning break if the weather was warm and developed a slightly suspect taste that an entire generation of British adults can still describe with uncomfortable precision.

The generation that grew up on school milk was, by every anthropometric measure, the healthiest generation of British children ever recorded.

Average height increased. Bone density improved. Dental health, despite the sugar in everything else, improved. Iron deficiency rates among school-age children dropped. The growth charts that the Ministry of Health had been keeping since the war showed a consistent, measurable, year-on-year improvement that tracked precisely onto the introduction of the milk programme.

In 1971 Margaret Thatcher, then Education Secretary, cut free school milk for children over seven. The tabloids called her Thatcher the Milk Snatcher. She was vilified. She kept the policy.

The next generation of British children, the ones who grew up without the daily third of a pint, were measurably less healthy than the one before.

The growth charts show it. The dental records show it. The conscription medicals, while they lasted, showed it. The thing the milk had been providing, the calcium, the vitamin D, the vitamin A, the complete amino acid profile, the conjugated linoleic acid, the fat-soluble nutrients that a growing skeleton requires in order to reach its genetic potential, was no longer arriving at morning break in a glass bottle with a foil cap.

It was replaced, eventually, by nothing. Or by a carton of fruit juice. Or by a packet of crisps from the vending machine that appeared in the school corridor in the 1990s.

The generation that drank the milk is now in its seventies and eighties. They are, on average, taller, stronger-boned, and longer-lived than the generation that came after them.

The milk was not magic.

The milk was milk.

It was the thing the body needed, delivered at the time the body needed it, at a cost the government considered acceptable until it didn't.

The cost of not providing it has been rather higher.

1

87

Apr 18

Here is a true breakdown of what's going on in the strait of Hormuz.

Data includes a tanker traffic summary and details about their flags.

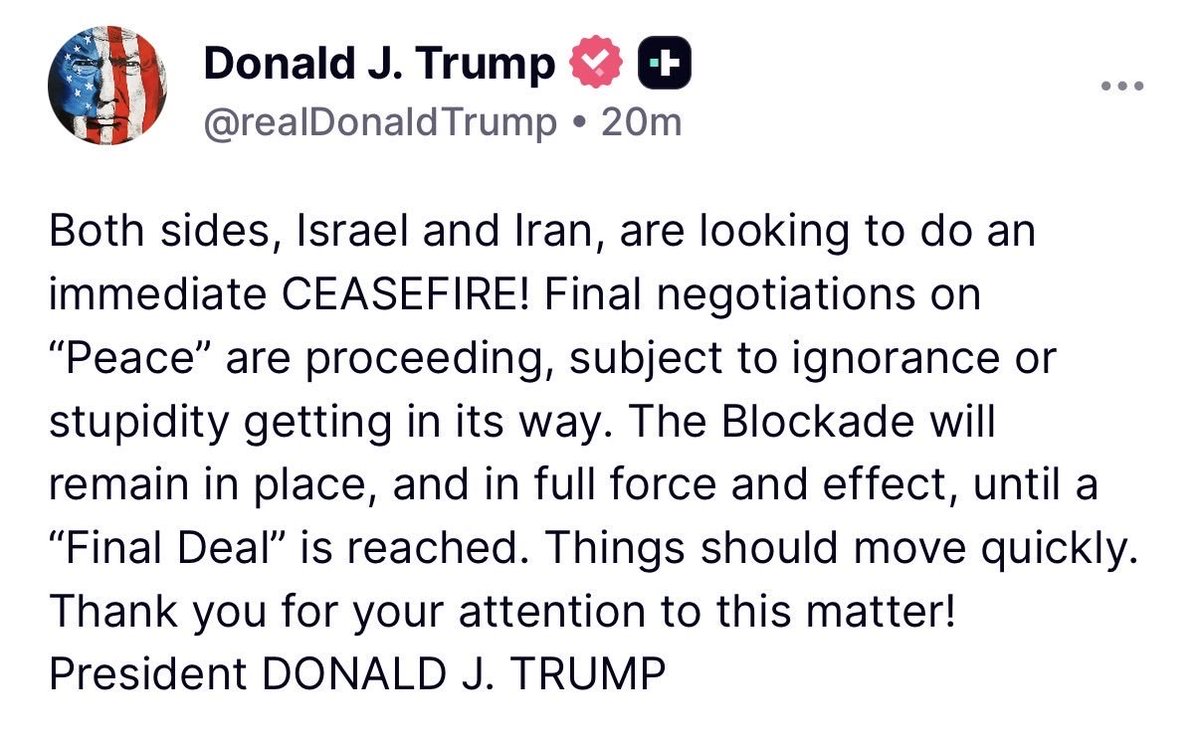

Iran’s Foreign Minister announced on April 17 that the strait is “completely open” for all commercial vessels during the current Lebanon ceasefire, with ships required to follow Iran-coordinated routes (e.g., near Iranian islands like Larak and Hormuz).

President Trump welcomed this, but the U.S. naval blockade on Iranian ports/ships continues, war-risk insurance is still extremely high (and reviewed frequently), and shipping companies remain cautious.

As a result, it is not fully open or risk-free for normal international traffic!

Tanker Traffic Summary (as of April 18, 2026)

Normal pre-crisis levels (2025/early 2026): ~60–140 ships per day total (~95–138 average), with 50–60% being tankers/oil-product carriers. This meant dozens of tankers daily, transporting ~20 million barrels of oil and LNG daily (about 20–21% of global supply).

Since the conflict began (Feb 28, 2026–April 12): Only 279 ships total transited the strait (a >95% drop). Of these, tanker traffic was a small fraction; 22 ships (including some tankers) were attacked. Only ~45 ships passed after the April 8 ceasfire.

Recent/post-ceasefire (April 8–17): Extremely low — often 3–11 ships per 24 hours total (4–10% of normal). Very few tankers. On April 17 (the day Iran declared it open), only a handful crossed: no major oil tankers exited the Persian Gulf; one bitumen/asphalt tanker and five cargo ships headed out; a cruise ship also transited. Some groups of ~20 vessels (including VLCCs and tankers) were seen approaching but actual completed transits stayed minimal.

Last 24 hours (as of April 18): Around 6 ships total (~4–5% of normal), with very few (if any) full oil tankers. Live trackers show ~500K DWT throughput vs. normal ~10M DWT daily.

Traffic is expected to take weeks (or longer) to normalize due to insurance, scheduling, and geopolitical risks.

What Did the Tankers Contain? (Recent Examples)

Most recent transits involved crude oil (often Iraqi Basra, Saudi, UAE, or Iranian origin), petroleum products, chemicals, fuel oil, or LPG. Very Large Crude Carriers (VLCCs) can carry ~2 million barrels each.

Examples of recent/reported tankers:

VLCCs like RHN (also called Hong Lu/Dimitra II), Alicia, Agios Fanourios I — heading to/in Gulf, often to load crude (e.g., Iraq) or carrying crude/products.

Race — exited to India (crude/products).

Rich Starry, Elpis, Peace Gulf — oil/chemical tankers or medium-range, some sanctioned/Iran-linked.

Others (e.g., Serifos, Cospearl Lake, He Rong Hai) — Saudi/UAE/Iraqi crude to Asia (Malaysia, China, Myanmar).

Some were Iran-linked/sanctioned vessels carrying Iranian crude despite restrictions.

What Flags Were They Flying?

A mix of flags of convenience (common for tankers) and some national/sanctioned flags. Recent examples include:

Panama (e.g., Peace Gulf)

Liberia (e.g., Serifos VLCC)

Malta (e.g., Agios Fanourios I)

Curacao (e.g., RHN — Chinese-owned)

Pakistan, Russian, Chinese (or China-linked/owned)

Iran-linked or U.S.-sanctioned vessels (sometimes re-flagged or ghost fleet)

Many were not “standard” international commercial tankers but limited/sanctioned ones operating under special Iranian permissions or evading full blockade.

Bottom line: The strait is “open” on paper since yesterday, but real-world tanker traffic is still tiny and risky. Normal volumes (dozens of tankers daily carrying crude oil under international flags) have not resumed and likely won’t for weeks. Data comes from trackers like Kpler, LSEG, MarineTraffic, and Reuters reports.

The situation is fluid — check live maritime trackers for the absolute latest!

1

2

134

Apr 18

(update)

An Indian flagged tanker has been fired at in the strait .

No other tankers have been confirmed fired upon today in the Strait of Hormuz (or any other strait). Several vessels (including other tankers) turned back after the incidents and Iran’s re-closure announcement, but they were not shot at.

UK Maritime Trade Operations (UKMTO) issued the official warnings confirming these events. Live maritime trackers like Marine traffic or Vessel Finder will show the affected ships deviating or holding position, along with any new exclusion zones or warnings.

As of April 18, 2026 (today), in the Strait of Hormuz: One tanker has been reported fired upon. The Indian-flagged VLCC crude oil tanker SanMar Herald (carrying Iraqi oil) was approached by two Iranian Revolutionary Guard Corps (IRGC) gunboats around 20 nautical miles northeast of Oman.

The gunboats opened fire with gunfire (small arms / machine-gun fire from the patrol boats) with no prior VHF challenge.

The tanker sustained minor damage, but the crew is safe. It was forced to turn back. India has summoned Iran’s ambassador in protest. cnn.com This happened after Iran briefly declared the strait “open” on April 17 but quickly reimposed strict controls and restrictions in response to the ongoing U.S. naval blockade of Iranian ports.

Additional context (not tankers):

A separate container vessel (not a tanker) was later hit by an unknown projectile (described in some reports as a rocket) in the same area, damaging containers on board. No injuries reported.

theguardian.com

1

67

Apr 18

Definitely better news than a mushroom cloud!

Apr 18

TRUMP SAYS SIGNING EXECUTIVE ORDER DIRECTING FDA TO EXPEDITE REVIEW OF CERTAIN PSYCHEDELICS

2

36

Apr 17

50 000 targets online.

Apr 16

🇫🇷 The French tax helper platform @Get_Waltio basically put a target on 50000 people's backs.

You can definitely be assured you'll be seeing way more of this in the near future as money becomes more scarce, prices more depressed, and people more depraved.

1

40

Apr 12

Even though I've fallen out with Grok, big time, last couple of days I truly believe this sentiment.

Apr 12

The man who won the Nobel Prize just told the world that AI is not the energy crisis, it is the cure for it.

Everyone has been screaming about how much electricity AI consumes, the data centers, the training runs, the billions of queries every single day.

Hassabis just said AI will extract 30 to 40 percent more efficiency out of national power grids, grids that, right now, operate at only 30 percent of their total capacity according to Stanford researchers.

That means the grids we already built are massively underused, and AI is the key to unlocking what is already there.

But that is the smallest part of what he is saying.

He is saying AI will crack nuclear fusion, the energy source that has been 30 years away for the last 60 years and DeepMind is already working with Commonwealth Fusion in the US to help AI contain plasma inside fusion reactors.

His personal mission is to use AI to discover a room-temperature superconductor, a material that would allow electricity to travel with zero loss, something physics has never been able to deliver.

The implications of that alone would reshape the entire global economy overnight.

He is also saying AI will design next-generation batteries and build the best climate modeling systems humanity has ever had, using them to figure out exactly where the planet is breaking down.

Think about what this means, the thing everyone is blaming for the energy crisis is the same thing being bet on to end it forever.

1

52