Asymmetric Stock Ideas, MEME powered. Not Advice.

Joined December 2020

- Tweets 11,159

- Following 1,386

- Followers 4,615

- Likes 19,195

4,105 Photos and videos

Sat thinking about why the $snap board agreed to create a 13th board seat for Luke Wood, with no committee obligations. The only board appointment without one.

Guess his input is required for a very specific strategic purpose, and typically conflicts like active negotiations restrict him from serving on Audit.

Cannot sit on Compensation because acquisition or merger premium affects how executives get paid out.

Cannot sit on Nominating because the board composition changes in an acquisition.

Interestingly, The SEC 8-K Language Is more precise than others.

“Mr. Wood has not been appointed to serve on any committees of the board of directors. Mr. Wood will serve until the earlier of (a) the next annual meeting of our stockholders, (b) the effectiveness of the next action by written consent of stockholders in lieu of an annual meeting, and (c) his death, resignation, or removal.”

This clause exists for one specific scenario - a merger or acquisition that requires shareholder approval via written consent rather than an annual meeting vote.

His directorship ends when:

•Annual meeting happens (routine)

•Or a shareholder vote on a transaction occurs

•Or he leaves

The transaction clause being listed alongside the annual meeting clause suggests the drafters of this 8-K expected a transaction to be the more likely termination event.

Would make a nice theory that Luke Wood is on Snap’s board to facilitate a specific transaction with Apple, my guess is a strategic stake. Given his expertise with beats, and the lack of committee assignment is the legal mechanism that prevents him from being conflicted during that process.

Let’s see what tomorrow brings 👀 #AWE #SPECS

1

9

2,074

$SNAP tomorrow is a massive day for Snap. arguably the most important day in the history of the co since the IPO. investors have abandoned the company for a litany of issues. Extremely weak governance, excessive SBC giveaways, slowing user growth, lack of profitability. @evanspiegel has preached his vision for the next gen computer @Spectacles and tomorrow is the big unveiling. the evidence of momentum with developers and advanced technology is there out in the open, but nobody seems to care. Can @evanspiegel have his steve jobs moment and unveil something people dont even realize they want yet? I am long snap into the event, i think we are starting to see movement on initiatives that are shareholder friendly. the subscriptions, the increased focus on profitability, and the investor sentiment remains a frozen hell scape. This product release could be like the ipod, the first major step in restoring investor interest and business momentum to his current 1B MAU social network. looking forward to tomorrow. @JonahLupton @IrenicCap @RandianCapital

3

2

42

1,373

$SPCX already down on my first purchase 166.75. i think in 30-60 days u will be able to buy all u want at much lower prices. i absolute love Elon, and want to be a shareholder. but i am not paying up right now. one of the crazy things about this deal and the set up, is the sell side, in order to justify the deal and get a piece, are publishing pie in the sky models, DCFs etc, the odds of a miss in the short term against those models is extremely high the first few qtrs out of the gate. u do not need to chase this one. aaaaaannnnnddddd its gone. elon is a savage.

1

837

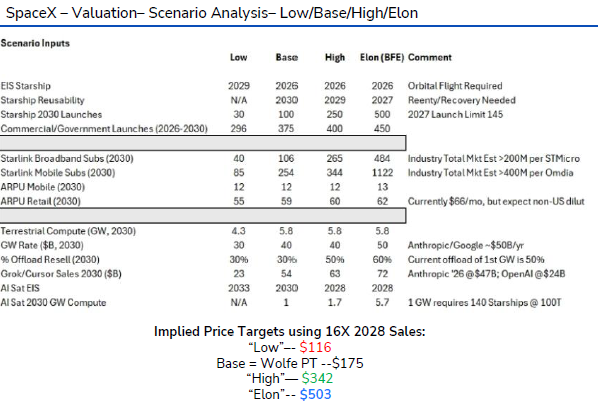

$SPCX wolfe research launches with a buy.

If you’re looking for analysis and modelling on SpaceX post-IPO look no further because Wolfe’s rocket scientist (literally) A&D analyst, Myles Walton. We’re out with a meaty 80 page initiation and a model to make sense of the complicated web of segments. Myles rates SPCX Outperform with a $175 Target and sees Starlink’s current success as sustaining NT financials while Starship will be the key value unlock for the company. Like all Musk enterprises, this will be a story stock with aggressive timelines and big aspirations, so we tried to put some math around the most likely path of travel. He’ll be on our 11am ET Weekly Industrials Webcast to discuss highlights

1

1

2

1,004

$SPCX wolfe initiation more-

Valuation

We’re using 16X our 2028 EBITDA estimate; our SOTP or DCF also yield similar numbers. If Starship doesn’t work, we get to $116, and then the numbers Elon talks about get you to almost astronomical returns

Comps? None that are good, of course, but some of the bad ones trade at massive multiples. RXLB’s multiple would yield more than a triple here (not our base case).

Starship Advantage

For SpaceX longer term, it all comes down to Starship. If they can solve for reusability this drives internal COGS down to levels competitors can’t touch (80% gross margins, before you get to Starship that should add another 10 points. In real numbers then the incremental cost of launch will go from $14M for a 20t payload on Falcon 9, to $~4M for 100t on Starship. Their advantages in verticalization, their drastically lower cost of failure than their competitors should preserve their moat in this business.

Starlink Already Humming

We’ve already seen a demonstration of how their flywheel works successfully to create economic returns with their Starlink Satellite offering where they turned a $10B investment that has already been recouped into a $90B EBITDA/yr business by 2030 that rises from there at a 30% clip.

Risks

If Starship doesn’t work, you basically cut about half of your long-term EBITDA forecasts. Also, because management targets are very aggressive, they’re likely to be missed… hanging your hat on exact dates with a Musk company is a mistake. If the AI bubble busts or someone comes with a better solution that is land based, orbital AI doesn’t work, and the financials don’t include self-funding for Moon and Mars. Admittedly, we don’t have Mars isn’t in our model and it will be it’ll be extra $$$.

838

$BKKT BE READY for the haters to post the generic screen grabs from the iphone in china. The bear thesis will be in broken english, and will be based on dilution is bad. I dont think these calls have teeth unless the stock is over $20. But there is a mafia of haters. They are watching and waiting. Usually on down days they pile on. They have no imagination. They dont believe in Akshay. This one is being built on the fly. More volatility, but given the size of the TAM and the lack of real pure plays. The reward is great. $1-2B EV would not surprise me post Clarity (knock on wood) and continued execution into year end. That would be a huge return. Bakkt fundamentals and duration to build a business get longer and stronger by the day. #1 stock on Stablecoins and death of big lazy banks.

1

5

1,562

$BKKT we stumbled on it in December, original 70k share purchase was called away, we made the mistake of being too cute and writing calls. But current prices offer an even better entry price. And of course, seeing directors invest more long term capital is a strong sign post. Need the clarity act to really get money flows in - but even without it - akshay is a visionary deal maker and is swinging for the fences. For the high beta play. The degradation of USD. There are a lot of reasons Bakkt is becoming more thematic, betting on USD printing is always a good bet over time. I prefer to $MSTR given much earlier in the investment life cycle. Value becomes Garp. Garp becomes growth. Inning 1.

5

698

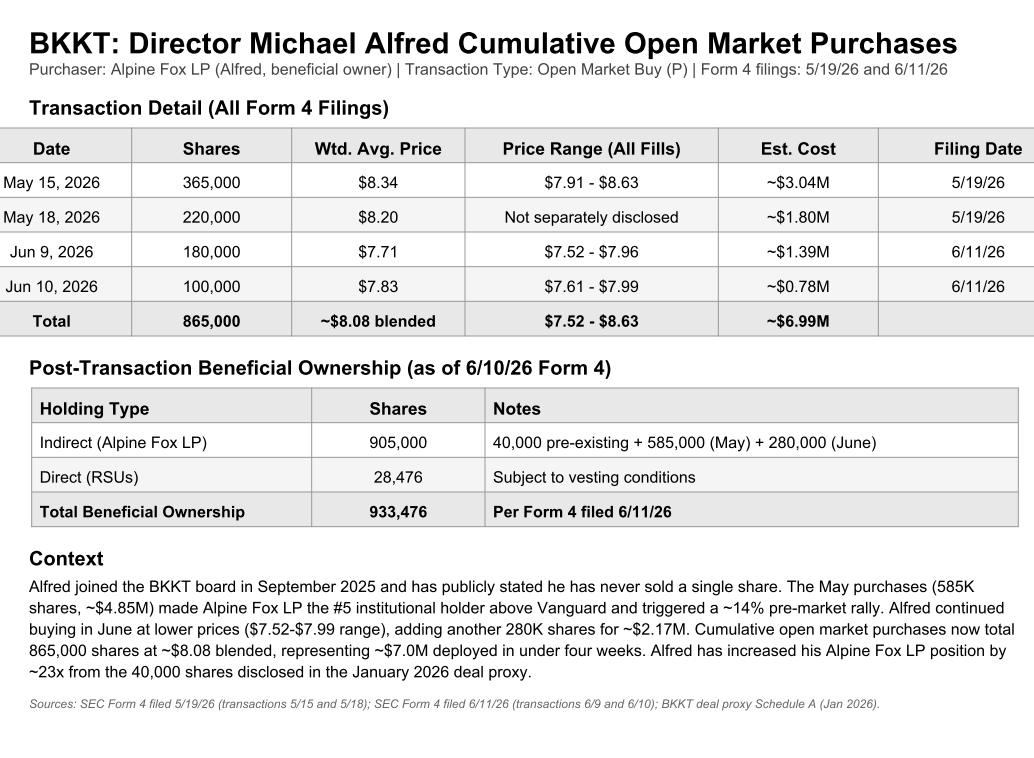

$BKKT HES BACK - ALPINE FOX @mikealfred

$BKKT LIFESTYLES OF THE RICH AND FAMOUS, U CAN NOW OWN BAKKT AT THE SAME PRICE AS THE ALPINE FOX !!!!!! @mikealfred $8.20 - 8.34.... WADING IN, MR MARKET IS GIVING US A CHANCE

1

2

8

3,223

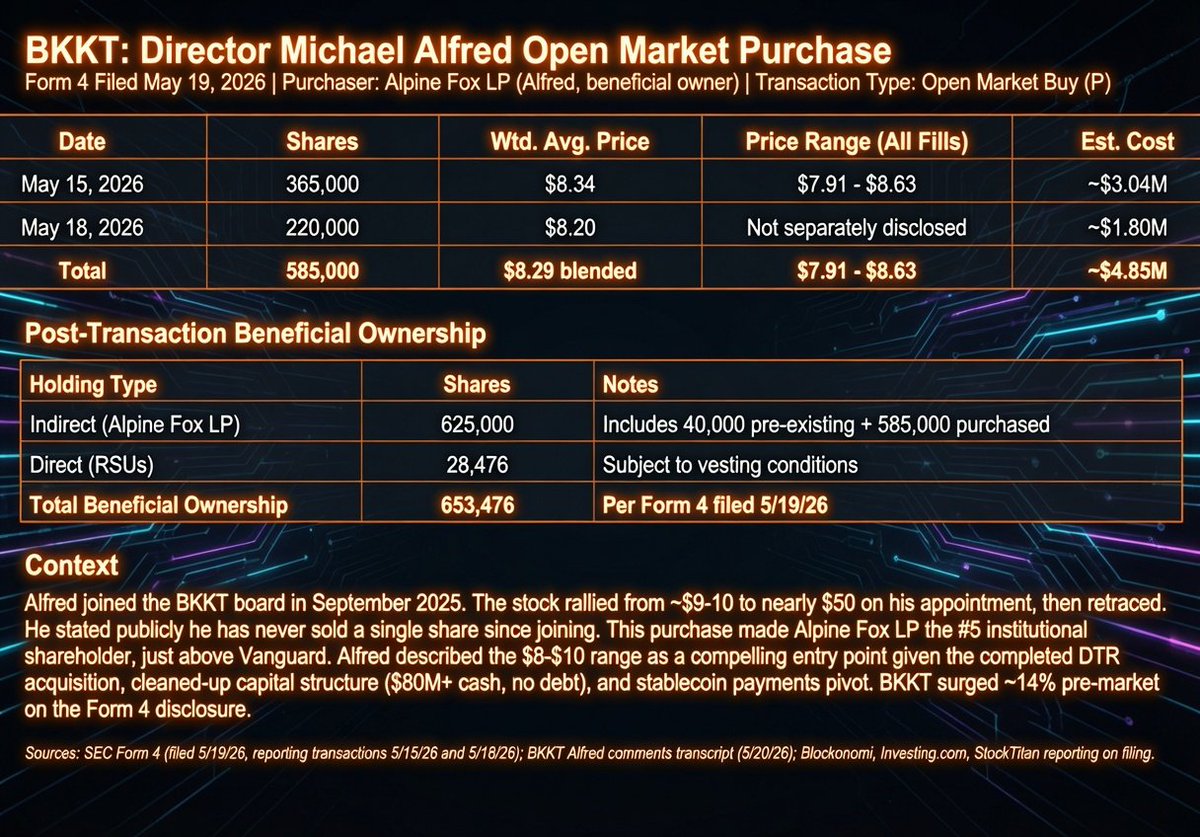

$BKKT a look at the open market purchases of @mikealfred some purchases as low as $7.52 / share. stepping up with open market purchases. why dont more directors do this if they believe in the company?

1

1

9

963

BoxLongs retweeted

Jun 11

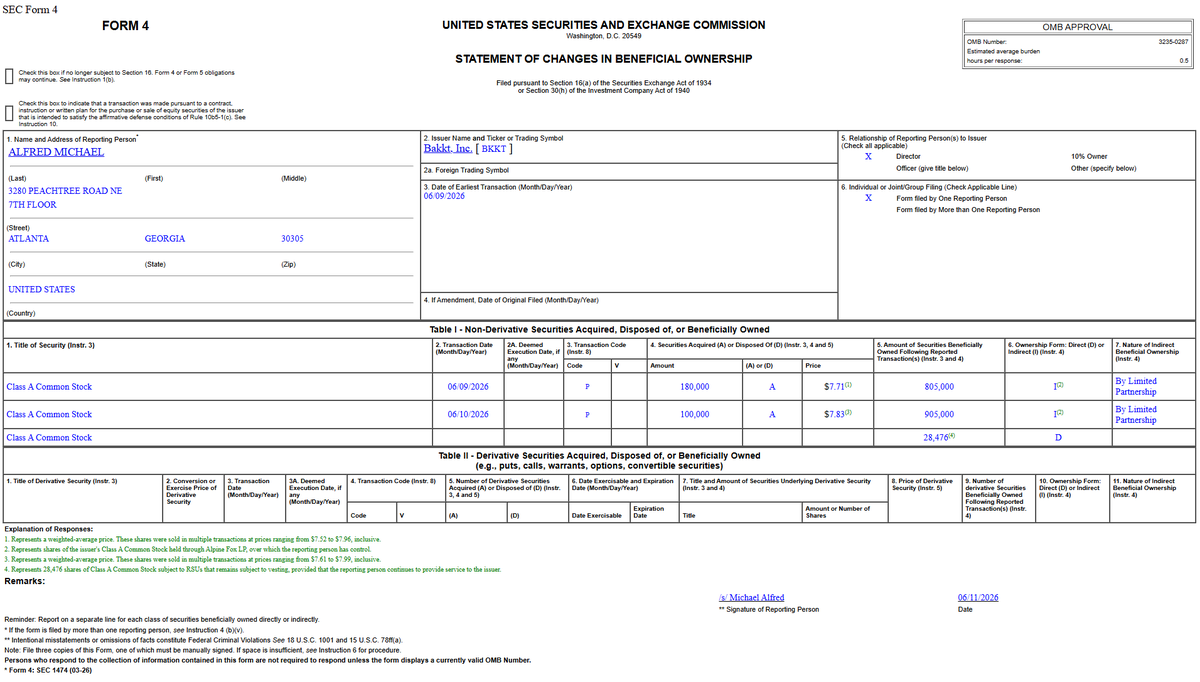

I have purchased an additional 280,000 shares of BKKT via my affiliated entity Alpine Fox LP. Alpine Fox LP now holds 905,000 shares in total and has become the 4th largest institutional shareholder in the company. See SEC Form 4 filing here: sec.gov/Archives/edgar/data/…

71

47

833

93,527