AMC Theatres and Sports - Washington Capitals - Phillies - Yankees - Poker - Appalachian State University - NASCAR - F1

Joined August 2021

- Tweets 27,045

- Following 1,611

- Followers 1,671

- Likes 123,523

2,769 Photos and videos

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

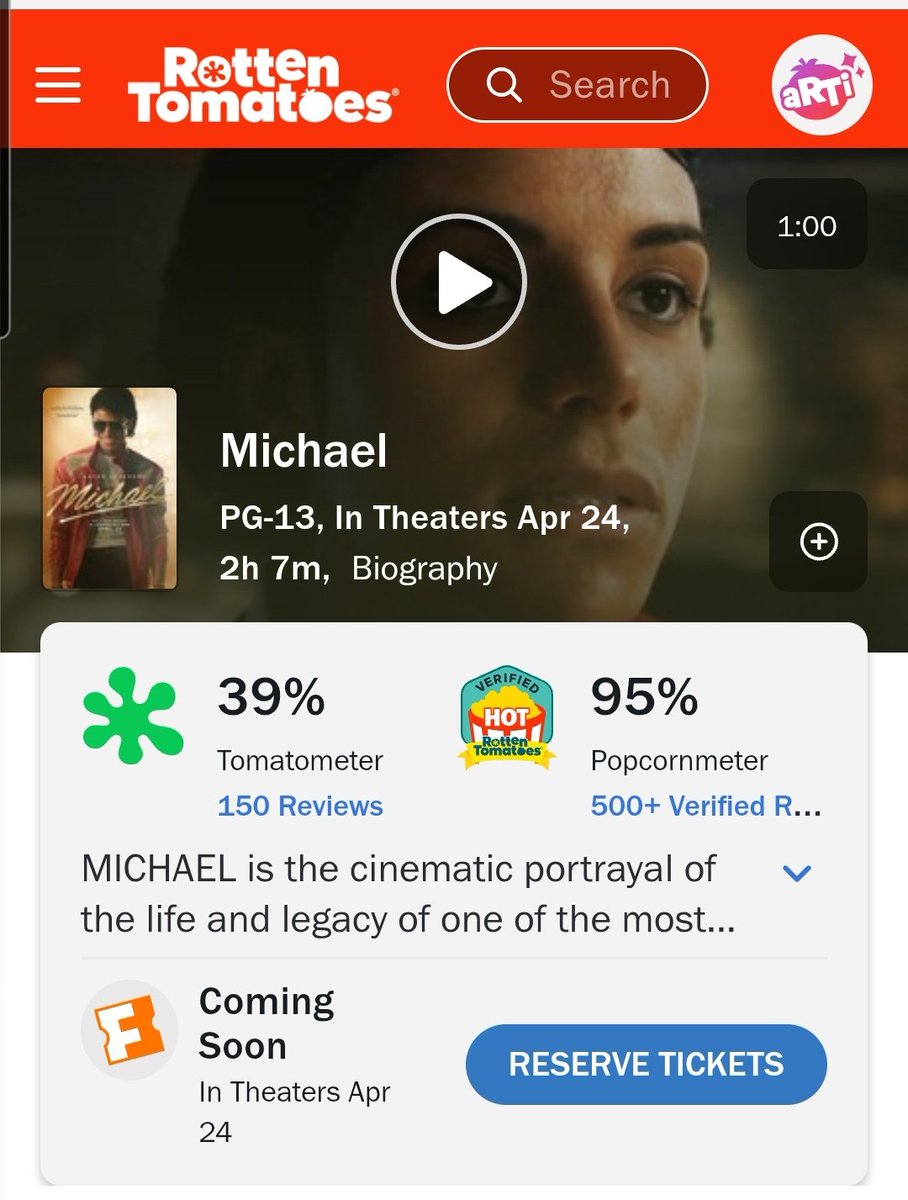

🥳 seen Michael movie 3x's at #AMC Theatres 👏 140 Million away from a Billion 😂

💯 Screw the Critics 💥

Last night I watched Star Wars #TheMandalorianandGrogu at AMC loved loved loved it

🎶🎵

Keep On With The Force Don't Stop 🙌

Don't Stop 'Till You Get Enough

Woo 🚀🚀🚀

4

9

202

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

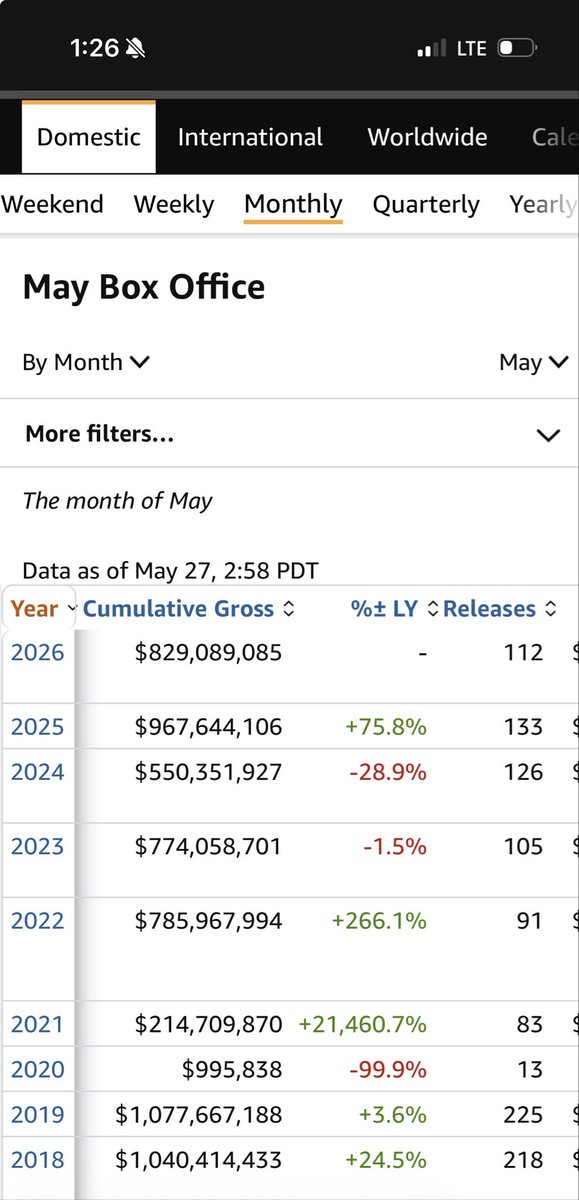

#AMC Once Tuesday updates, we’ll be sitting just shy of $850 Mil for May, with tonight and Thursday night getting us to around $875. Then if this weekend Fri-Sun goes over 125 mil, May will end up over $ 1 Billion 💚 @AMCTheatres

8

38

213

3,548

I have enormous confidence in AMC and the 2026/2027 box office. So today, using my own money, I bought 250,000 more AMC shares personally, at market price.

I now own outright 2,437,020 AMC shares, raising the total where I have an economic interest to 12,322,429 AMC shares*

It actually can be very hard for a CEO of a public company to buy shares. You have to clear having possession of any material non public information, sort out implications of any ongoing debt and equity transactions, and not be in a quiet period before when earnings will be announced. I was finally in a position to buy even more AMC shares today, and I did.

As I said, I have great confidence in AMC’s future. So, again today, I put my money where my mouth is.

This brings my holdings up to 12.3 million shares* of AMC common stock. My understanding is that I have been, and now even more so I remain, AMC’s biggest individual retail investor.

I should probably mention that I have not sold even a single share of AMC stock since January of 2022, more than four years ago.

I RIDE WITH YOU !!!

—-/////—/////—-

(*For precision: this includes AMC shares I already own, and those which previously have been granted to me as part of my annual compensation and which will vest based on length of service and at target levels of performance over the next thirty three months, on a pre-tax basis.)

945

1,236

4,086

224,807

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

Anything virus on my timeline is getting blocked. So sick of the algorithm on @x

1

1

127

Of course @CNN king of the tards with a whole section on this.

cnn.com/2026/05/07/world/han…

29

Stop being retarded. This thing is nothing.

May 7

27

Great White out

2

882

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

10/10 🔥 Michael Movie 🍿

A MUST SEE only at #AMC Theatres #ApeStrong

Favorite Quotes

"Let your light shine for the world"

"You can see it, you can do it"

💥 Critics can Beat It 🥁

2

22

73

982

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

Apr 23

Film critics are useless.

#AMCTheatres 🎬🔥🍿

#Michaelmovie

7

21

133

1,762

🍌🖍️Bubbles Jackson🖍️🍌 retweeted

Apr 23

Lugares donde me emperra no haber estado 🙌🏽🥰

162

2,412

16,714

642,223

I wouldn’t be surprised if @SECPaulSAtkins @HesterPeirce and @lynnmartin had an ownership stake in @JaneStreetGroup

Apr 22

🚨 JANE STREET IS EVERYWHERE.

The same firm accused of rigging markets in India and linked to the daily 10 AM Bitcoin dump pattern may now be behind the $CAR short squeeze as well.

And the data does not lie.

$CAR was a dying rental car company. Avis posted an $889 million net loss in 2025, carried roughly $25 billion in debt, and revenues were falling. Then in just 5 weeks, the stock exploded nearly 700%.

Not because Avis fixed anything.

Because the stock may have been turned into a weapon.

Two hedge funds, SRS Investment Management and Pentwater Capital, quietly accumulated 71% of all Avis shares. When you include swap exposure, their combined economic interest reportedly crossed 108% of total shares outstanding.

At the same time, 54% of the float was already shorted. By April 21, Ortex showed 86.2% of the free float sold short, near all-time record levels.

That creates a basic problem.

There were not enough shares available for shorts to exit.

Short sellers lost $4.09 billion in April alone. $1.01 billion was wiped out in a single Monday when CAR surged 23%. By Tuesday morning, the stock traded at $647.

Now meet Jane Street.

They filed a Schedule 13G disclosing 1,910,016 Avis shares, equal to 5.4% of the company as of December 31, 2025. They also reportedly held 3.7 million CAR call options valued around $476 million .

Call options rise in value when the stock rises.

The higher the squeeze pushed CAR, the more those calls gained. Jane Street’s broader portfolio is heavily options-based. They do not need markets to go up or down. They need violent movement.

But here is where it gets interesting.

A setup like this can pay twice.

First, benefit from the squeeze higher as trapped shorts are forced to buy back stock at rising prices.

Then, once the rally exhausts and liquidity fades, flip positioning and profit from the collapse lower.

The public usually only sees disclosed long equity stakes.

The derivatives book is where the real exposure can sit.

And we have already seen regulators describe similar structures before.

In India, SEBI issued a 105-page order accusing Jane Street of buying large amounts of underlying stocks to push Bank Nifty higher while simultaneously holding much larger bearish options positions. Later in the day, those stock positions were unwound, the index dropped, and the options paid. SEBI impounded roughly $567 million.

On one session, they allegedly lost money on the stock leg while making far more on the options leg. The stock trade was described as the cost of running the operation.

In Bitcoin, traders tracked a repeated daily 10 AM Eastern selloff pattern where BTC would get hit at the U.S. open, followed by sharp recoveries. The theory was simple: create panic on the dump, then profit on the rebound.

In crypto, Terraform Labs’ bankruptcy administrator later filed a federal lawsuit alleging Jane Street used non-public information to reduce Terra exposure before the $40 billion Terra/LUNA collapse. Jane Street denies the claims.

Now look back at $CAR.

Pentwater reportedly sold massive deep in-the-money put options at $110–$150 strikes while the stock was near $96. Buyers of those puts had to hedge by buying the underlying stock.

That created fresh demand in a market with almost no available float.

Price exploded.

Then Avis issued 5 million new shares near record highs.

And Jane Street was sitting there with large call exposure as the squeeze intensified.

Was any of this coordinated?

Nobody knows yet. No formal U.S. regulatory action has been filed.

But the structure keeps repeating:

India: move the underlying, profit in derivatives.

Bitcoin: dump first, profit on rebound.

CAR: ride the squeeze higher, then potentially the unwind lower.

The cash position can be the instrument.

The options book can be the profit center.

And a company losing $889 million a year was suddenly priced like a winner.

If history is repeating, the squeeze was the first payday. The crash could be the second.

1

6

23

1,126

I will agree with this retard on one thing. Ken Griffin sucks and shouldn’t be this rich. He’s a crook.

@Citadel @citsecurities

1

30

Homie like this before red carpets.

LFG. 📸 🦧

🖍️🦍💎🤲🚀🌖

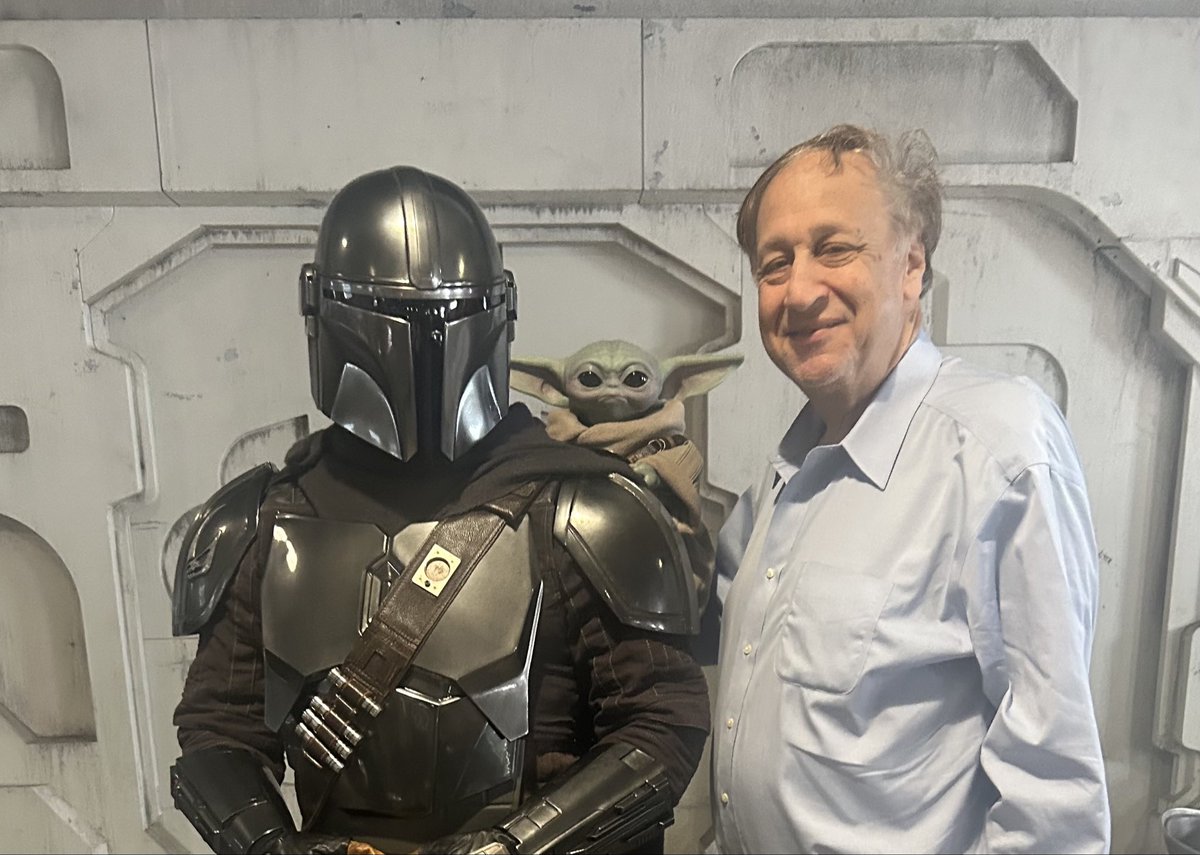

The Mandalorian and Grogu are ONLY IN THEATRES starting May 22.

But today they were in Los Angeles, as was I.

Tickets are on sale now for AMC and the latest Star Wars influenced movie from Disney and Lucas Films. It is spectacular. Really phenomenal!

2

39

I mean. Mad props. I want to reach a point where I can go out with this level of “bed head” 🤣

#AMC #AMCStocks #AMCTheaters

The Mandalorian and Grogu are ONLY IN THEATRES starting May 22.

But today they were in Los Angeles, as was I.

Tickets are on sale now for AMC and the latest Star Wars influenced movie from Disney and Lucas Films. It is spectacular. Really phenomenal!

2

8

333