Just a guy who built a stock scoring model, trading the best growth setups. Real positions, charts, and the misses. Not advice.

Joined May 2020

- Tweets 69

- Following 122

- Followers 38

- Likes 161

2 Photos and videos

$RDDT deep dive. Credit to @JonahLupton for putting this on my radar. Then it popped up on my scanner at 14.5/15. Why I'm long: in a world that just went majority-bot, Reddit owns the best stash of real human conversation on the internet. Here's the breakdown.

1

3

143

Matt retweeted

May 14

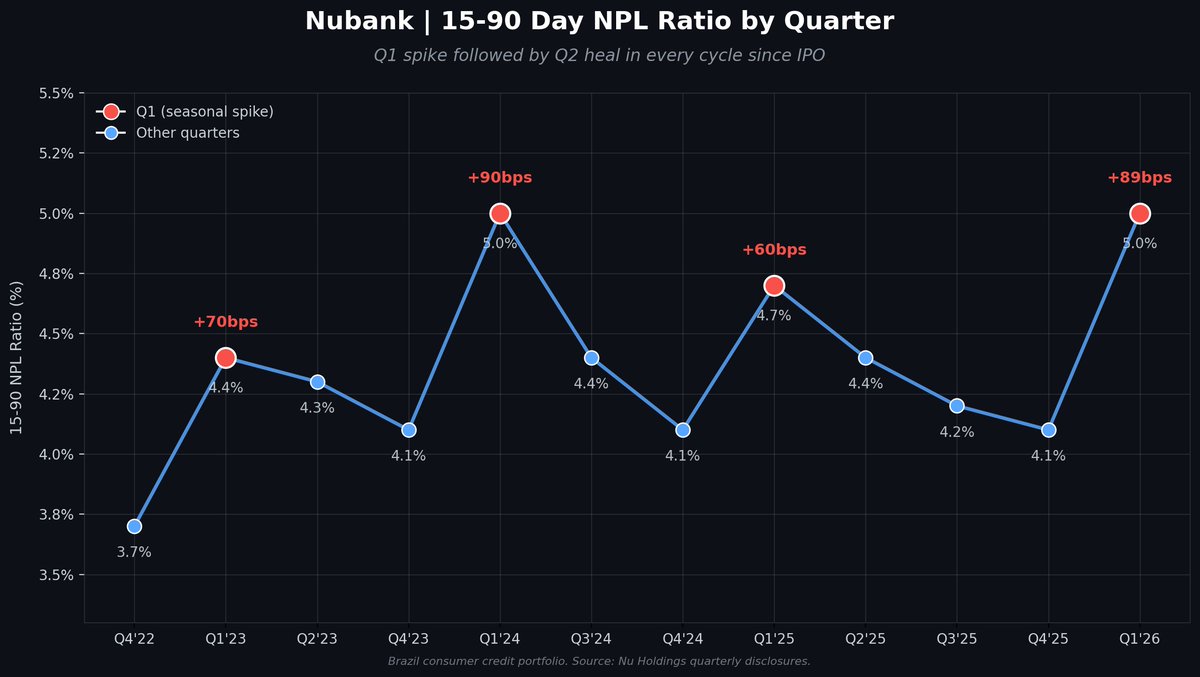

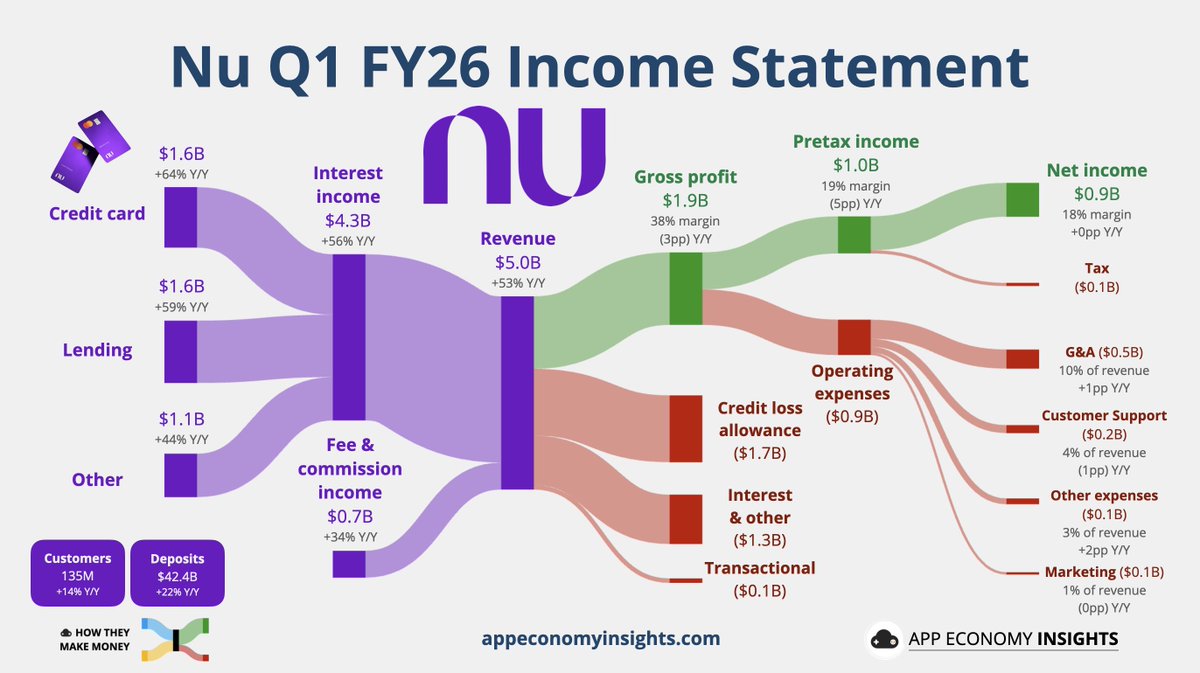

$NU Nubank Q1 FY26:

• Customers 14% Y/Y to 135M

• Deposits 22% Y/Y to $42.4B

• Revenue 53% Y/Y to $5.0B ($0.1B miss)

• Net income 56% Y/Y to $0.9B

• EPS $0.18 ($0.01 miss).

5

59

540

68,121