26 Photos and videos

mauricio bustos retweeted

12 Dec 2024

Let me get this right.

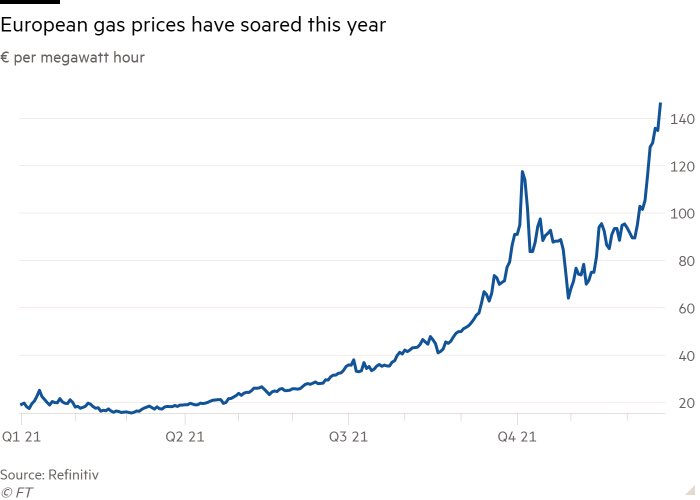

5 out of the 6 convertible bonds for $MSTR are eligible for conversion, carrying an interest expense 0.811% at an annualized rate of $34.6 million.

If these bonds get converted early, and the debt is wiped off the balance sheet (other than the 2029 bonds, which are 0%).

This would put @saylor in an even more favourable position and get even better terms for the next convertible bond offerings. Borrow more, less interest.

The room to run here will be huge.

27

53

759

73,331

18 Jun 2023

La forma antigua de validar es a través de una institución o una autoridad(normalmente personas o grupo de personas), la nueva forma sera a través del código(matemática es la autoridad) . entonces es :

1. mas eficiente

2. mas transparente

3. mas confiable

1

68

18 Jun 2023

Servicios de Comunicación

Consumo Discrecional

Consumo Básico

Energía

Servicios Financieros

Cuidado de la Salud

Industrial

Materiales

Inmobiliario

Tecnología

Servicios Básicos

todos estos sectores ocupan algún tipo de validación .

1

44

18 Jun 2023

por eso opino que el web 3 sera disruptivo a la forma de como validamos.

13

18 Jun 2023

Just got my #GarbageUniversity Student ID. Ready to become a Garbage Collector for @GarbageFriends

19

11 Sep 2022

la forma mas eficiente para transportar gas natural es de esta manera, aparte de una tubería que cruce el atlantico

1

1

11 Sep 2022

que crees que pase?crees que estados unidos ayude a su aliado mas grande de esta manera? o quizá lo ayude con bonds extranjeros? quizá los dos?

1

18 May 2022

Para la comunidad latina que me sigue , les comparto con mucho amor este podcast que se enfoca en educar en tecnologías innovadoras. open.spotify.com/episode/2q5…

1

1

mauricio bustos retweeted

1 May 2022

Really cool bumping into fellow @primobots holders yesterday. @BustosMauri, my degen bro, pulled a gold legendary 🔥🔥🔥 @elyunghefna and his cousin repping too 💪💪💪

4

3

31

22 Apr 2022

#InvsbleFriends very little of my IF family following me , where is my IF family? #IFfollowIF

17

7 Apr 2022

Why not leverage mexico-usa export policies? In the following years i see mexico as the capital of repair for this asic machines as well as a brigde for logistics and tax purposes to move this miners. Probably just assembling un mexico.@RicardoBSalinas

3

1 Apr 2022

Boomers experienced the transition of no internet to everything going through the internet , and they are the most skeptic about web 3 and crypto. Bruuuh🤦♂️

1