Creator of The Convergence Portfolio & Too Big To Fail on @joinautopilot || No opinions. Just convergence.

Joined January 2025

- Tweets 22

- Following 204

- Followers 86

- Likes 1,383

8 Photos and videos

CTK Capital Intel Report

Monday, June 15, 2026

Big green day. The S&P 500 gained 1.49%, the Dow added 1.20%, and the Nasdaq surged 2.38%. The Russell 2000 climbed 0.79%.

The Iran peace deal Trump announced over the weekend that a deal to end US-Iran hostilities is “now complete,” with the Strait of Hormuz reopening as part of the agreement. WTI crude tumbled over 2.5% to settle near $87.71. This is the macro green light we’ve been tracking — oil coming down off its highs directly removes the energy-driven inflation pressure that’s been hitting growth names all month.

One odd wrinkle: market breadth wasn’t as strong as the index gains suggest — barely more stocks advanced than declined, with tech-driven sector themes doing most of the lifting. Fox Corp was the worst S&P 500 performer, down over 17%, in unrelated news. Worth knowing if anyone asks why “everything was green” but their watchlist looked mixed.

Stock of the Day — $ONTO

$338.99 | 4.7% | Fresh all-time high

ONTO just keeps running. B. Riley raised its price target to $355 today (up from $330), and the stock is now up roughly 230% from its 52-week low of $89.40 — all in the last twelve months. The Dragonfly G5 inspection platform, which began shipping this month for AI chip packaging and HBM production, remains the core catalyst, and the stock’s daily technical signal is reading Strong Buy across every timeframe from hourly to monthly.

The honest read: the average analyst price target is now $351.88 — meaning today’s $338.99 close is already within about 4% of where Wall Street thinks fair value sits. This is a name that’s gone from a 33% earnings miss in Q1 to an all-time high in about six weeks, almost entirely on the Dragonfly G5 narrative. It’s the strongest momentum story in the portfolio right now — and also the one closest to “priced for perfection.” Next earnings Aug 6 will be the test of whether the ramp matches the hype.

With the Iran deal removing one of the year’s biggest overhangs, watch whether AI/semis (which led today at 2.38% on the Nasdaq) can sustain the rally without a fresh catalyst, or whether this is a one-day relief pop. Also keep an eye on whether oil’s drop toward $87 continues toward the $90 macro green-light threshold we’ve been tracking for sustained inflation relief.

Both portfolios are live on Autopilot.

Follow the Convergence Portfolio 👇

marketplace.joinautopilot.co…

Follow the Too Big To Fail Portfolio 👇

marketplace.joinautopilot.co…

Educational only. Not financial advice.

1

99

CTK Capital Intel retweeted

Iran says Strait of Hormuz to reopen fully Friday.

114

278

4,466

448,021

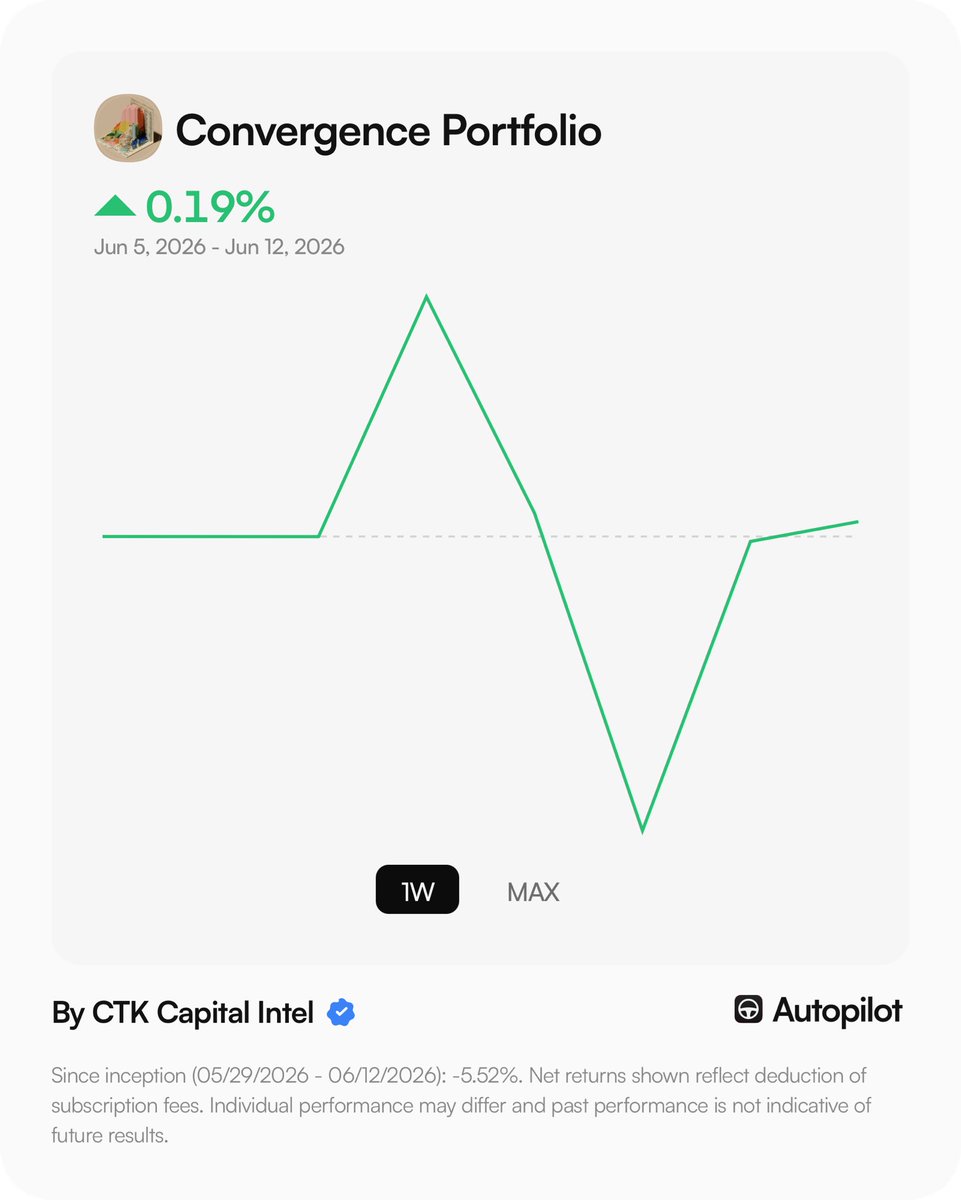

CTK Capital Intel Report

Friday, June 12, 2026

The big story — SpaceX. Shares of Elon Musk’s rocket company gained 19% Friday to close at $160.95 on its first day of trading on the Nasdaq, after pricing the largest IPO in history at $135 and raising $75 billion. At one point shares surged over 30%, briefly valuing SpaceX above $2.25 trillion. It’s now the sixth-largest publicly traded company in the US, and Musk became the world’s first trillionaire on paper.

Goldman Sachs led the IPO. Morgan Stanley led the stabilization process — both directly feeding into TBTF Portfolio earnings through underwriting and advisory fees this quarter. Goldman’s president called the offering a signal that capital markets are ready to fund the AI infrastructure and space buildout — a bullish read-through for the entire financial sector.

This debut landed in a market already at or near records, with AI-linked names broadly higher despite the Iran conflict stretching into a fourth month.

What to watch next week. Watch for follow-through in SPCX trading and whether the “halo effect” extends to other AI-adjacent names into next week. Anthropic and OpenAI’s own IPO paths remain the next catalysts in this mega-IPO cycle — both would be massive incremental fee events for the TBTF banks.

Educational only. Not financial advice.

52

CTK Capital Intel Report

Thursday, June 11, 2026

The Nasdaq jumped 2.54%, the Dow surged nearly 930 points ( 1.86%) back above 50,000 to 50,848.75, and the S&P 500 rose 1.75% to close just shy of 7,400. The Russell 2000 led with 3.02%. The VIX fell nearly 12%.

Trump and Iran signaled a deal is close, with explosions reported near the Strait of Hormuz as part of what’s being read as a de-escalation move. Oil came down off its highs. Tech, industrials, and materials led the rebound; energy, staples, and real estate lagged — a clean mirror image of yesterday’s rotation.

Producer prices came in hot — PPI rose 1.1% monthly (vs 0.7% expected) and 6.5% annually, the fastest pace in nearly four years. Markets shrugged it off today in favor of the Iran headline, but a hot PPI typically feeds into future CPI prints — worth watching.

65

CTK Capital Intel Report

Wednesday, June 10, 2026

Brutal day. The Dow dropped 953 points (-1.87%) to 49,918.78. The S&P 500 fell 1.62% to 7,266.99. The Nasdaq lost 1.98% to 25,169.50. Industrials fell over 3%, Tech and Materials fell over 2%.

Two hits at once. May CPI rose 4.2% year-over-year — the highest since May 2023, driven by energy costs surging over 60% from the Iran conflict. The print was in-line with expectations, but a hot in-line number on top of renewed Iran strikes was enough to push odds of a 2026 Fed hike higher. Then came the second hit — reports the US is striking Iran again, breaking the “ceasefire” that never really held. NVDA fell 3.7%, AVGO fell 5.1%, and SMCI plunged 28% after announcing a $7 billion fundraise. Brent crude rose 1.8% to $93.10.

One bright spot buried in the data — core CPI (excluding food and energy) came in at just 0.2% monthly, below the 0.3% estimate. Food inflation was minimal at 0.1%. The inflation story is almost entirely an energy story right now — which means it is an Iran story, not a broad-based wage-price spiral story. That distinction matters for how long this lasts.

🏦 TBTF Portfolio — Weighted Return Since May 31

TBTF Portfolio (weighted) = 2.38%

S&P 500 (SPY) = -1.65%

Outperformance = 4.03%

The TBTF Portfolio is still up over 2% since inception while the S&P 500 has gone negative. Stocks in defensive sectors rallied following the CPI report — exactly the rotation the TBTF thesis is built to capture. Higher-for-longer rates are a tailwind for bank net interest margins regardless of what they do to growth stock multiples.

What to watch tomorrow. Watch whether the Nasdaq and S&P hold their near-term support zones — today’s late-session weakness suggests sellers retained control into the close. If support breaks this shifts from “correction” to something more serious. SpaceX’s order book closes after today’s close with pricing expected tomorrow — keep an eye on whether IPO demand headlines offset the macro gloom for GS, MS, JPM, and BAC underwriting fee exposure.

Educational only. Not financial advice.

1

77

CTK Capital Intel Report

Tuesday, June 9, 2026

The S&P 500 fell 0.26% to 7,386. Nasdaq dropped 0.97%. The Dow gained 0.17% — rotating into industrials and financials while tech gave back Monday’s partial recovery.

Chips faded after Monday’s bounce. The semiconductor ETF shed 1% Tuesday following a 6% rebound on Monday. The ETF had tumbled 10% on Friday for its worst day in six years. Micron dropped another 1% after Monday’s 10% comeback — the shares tumbled about 20% in two days last week, including a 13% rout on Friday.

What I find more interesting than the bounce itself is what is underneath it. Jensen Huang spent the weekend in Seoul signing a memory partnership with SK Hynix and publicly calling Friday’s selloff a buying opportunity.  When the CEO of NVDA publicly tells investors a dip in semiconductors is a buy — after personally locking in a strategic partnership with the world’s second-largest memory manufacturer the same weekend — that is not routine investor relations.

Trump giveth and Iran taketh away. Investor sentiment was briefly bolstered by comments from President Trump who said a deal to end the conflict could be reached in “two or three days” and that the Strait of Hormuz would reopen “immediately” after such a deal. Then he immediately set those comments ablaze with threats to strike Iran as part of a retaliation for recent retaliatory strikes.  This pattern has repeated more than a dozen times. The market no longer fully prices in Trump’s ceasefire optimism until a deal is actually signed.

The biggest story this week — the IPO hat trick of the century. OpenAI has confidentially filed for an IPO, joining archrival Anthropic and SpaceX in turning to the public markets in what looks set to be the three largest listings on record.

The SpaceX order book closes Wednesday after market close. Pricing is expected June 11 with a trading debut slated for June 12. OpenAI is eyeing a fall 2026 debut.  Goldman Sachs has the lead left position on the SpaceX prospectus, followed by Morgan Stanley, then Bank of America, Citigroup, and JPMorgan Chase.

Anthropic filed last week. SpaceX is set to begin trading Friday at roughly $75 billion raised and a $1.77 trillion valuation. Add OpenAI behind those two, plus Alphabet’s record $85 billion mandatory convertible from last week, and the equity supply heading at this market in a span of weeks is genuinely without precedent.

CPI inflation data drops Wednesday morning — the most important economic number of the week after Friday’s blowout jobs report. A hot print pushes the Fed further from rate cuts and hits every growth name in the Convergence Portfolio. A cool print reverses Friday’s damage and sets up a relief rally. The SpaceX order book also closes Wednesday after the bell.  Watch whether the IPO demand number leaks — $10 billion in orders already confirmed with more coming.

Educational only. Not financial advice.

1

198

CTK Capital Intel Report

Monday, June 8, 2026

The S&P 500 gained 0.8%, the Nasdaq 100 gained 1.5%, while the Dow was 0.4% higher.  A partial recovery after Friday’s brutal session. The chips bounced. Iran complicated everything again.

Iran Conflict Update

Iran launched its first direct missile barrage at Israel since April’s ceasefire, retaliating for an Israeli airstrike in Beirut. Israel responded with airstrikes on Iranian petrochemical facilities.  Brent futures climbed as much as 4% to almost $98 a barrel before cooling off.  Then Iran stated it had ended its military operation in Israel following the strikes, and President Trump signaled optimism about a deal with Iran — easing concerns that escalation would break ongoing negotiations.  Oil pulled back from its highs. Stocks recovered. The pattern has not changed — fear spike, clarification, recovery.

The Biggest Story of the Day

MRVL joins the S&P 500. Marvell and Flex stocks rose after S&P Dow Jones Indices announced the two companies will join the S&P 500, replacing Campbell’s Company and Pool Corp, before the market open on June 22. Marvell shares jumped nearly 9% on the announcement. It’s up 210% since the start of 2026 with a market cap that has risen to $230 billion.  S&P 500 inclusion forces every passive index fund on earth to buy MRVL before June 22. That is mechanical forced buying — not sentiment, not thesis, not fundamentals. Forced buying. Every ETF that tracks the S&P 500 is a buyer.

Apple WWDC — Tim Cook’s last keynote.

Apple hosted its annual Worldwide Developers Conference Monday at its Cupertino headquarters. The event, Tim Cook’s last as CEO, will serve as a kind of reboot of Apple’s AI strategy, which has lagged behind competing firms.  This matters for the Convergence Portfolio because Apple’s AI strategy determines demand for QCOM’s Snapdragon chips in next-generation iPhones and feeds directly into the broader mobile AI thesis. Watch for any specific chip partnership announcements out of WWDC.

What to watch this week

Wednesday brings CPI inflation data — the single most important number for Fed rate expectations after last Friday’s blowout jobs report. A hot CPI print pushes the Fed toward hikes, not cuts, and crushes every high-multiple growth name again. A cool print reverses Friday’s damage. Wednesday night Oracle reports earnings — a key test for AI infrastructure and data center investment.  Oracle’s cloud AI business is a direct read on enterprise AI spending. SpaceX’s historic $75 billion IPO is expected Friday — the largest public offering on record.

Follow the Too Big To Fail Portfolio 👇

marketplace.joinautopilot.co…

Follow the Convergence Portfolio 👇

marketplace.joinautopilot.co…

Educational only. Not financial advice.

4

217

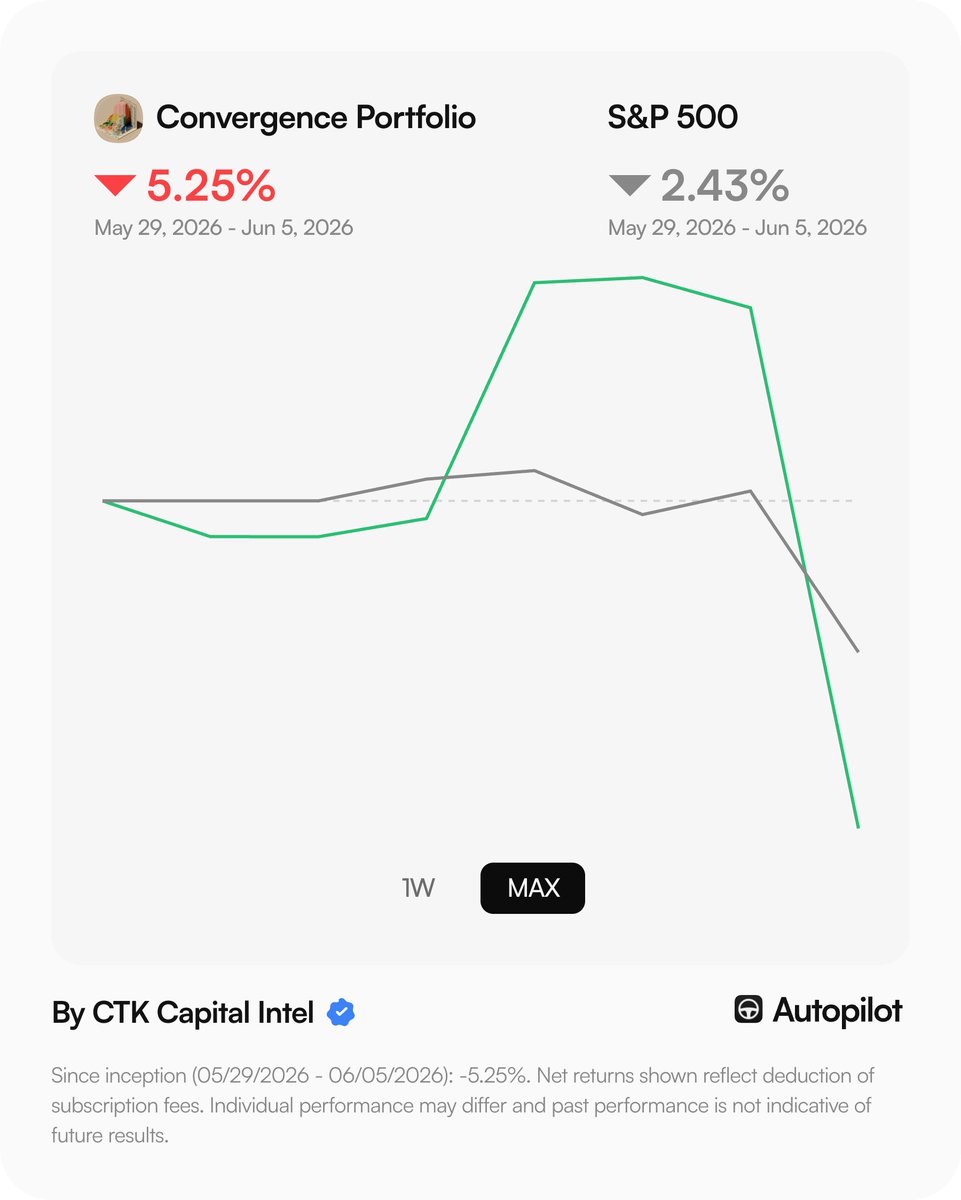

CTK Capital Intel Report

Friday, June 5, 2026

The Nasdaq lost 4.18% — its biggest drop since April 2025. The S&P 500 dropped 2.64% to close at 7,383.74. The Dow lost 695 points.  Ten consecutive positive weeks ended today. This was the worst session in over a year.

Two separate events collided on the same day. The May jobs report came in at 172,000 — roughly doubling the 80,000 consensus estimate. The stronger-than-expected number pushed yields higher and cut rate-cut odds fast.  Then the chip sector, already under pressure from AVGO’s guidance disappointment Thursday, accelerated lower. MRVL, MU, INTC, AMD, and NVDA all fell sharply. Broadcom dropped another 7% following its double-digit decline Thursday.

While that was happening the Too Big To Fail Portfolio finished the week up 3.23% since inception. The market reminded everyone today why diversification across uncorrelated theses is not a nice-to-have. It is the difference between a red week and a green one.

2

3

146

For full transparency, like many others yesterday, The Convergence Portfolio got torched. Updates made today.

Never panic, always diversify.

49

CTK Capital Intel retweeted

Jun 5

🚨 Breaking: May jobs report beats expectations

➡️Nonfarm payrolls: 172K vs 88K expected

➡️Unemployment rate: 4.3% vs 4.3% expected

10

15

106

17,278

CTK Capital Intel Report

Thursday, June 4, 2026

The S&P 500 closed at 7,584.31. Eight of eleven sectors advanced — Financials up 2.67%, Health Care up 3.14%. The Nasdaq was the only real decliner. The rotation continues. Financials strong. Tech under pressure.

Broadcom sank 14% after Q3 AI chip guidance of $16 billion missed the $17.2 billion analyst estimate, pulling AMD and INTC lower. Broadcom delivered record revenue, record free cash flow, and AI chip growth of 143% year-over-year. Q3 guidance of $29.4 billion would have seemed like a typo twelve months ago. The business is exceptional. The stock fell 14% anyway.

When a stock surges 63% in two months investors price in acceleration. Any guidance shortfall triggers sharp repricing regardless of fundamentals.

This is the same pattern you have seen on NVDA, MRVL, and PENG this week. Beat the number. Stock sells off anyway. The businesses are not breaking. The expectations are just impossibly high. The investors who understand the difference between those two things are the ones positioned correctly for when the dust settles.

The House passed a resolution seeking to limit Trump's ability to continue military operations against Iran, reflecting growing concern among some members of his party about the conflict. This is a meaningful political development. Congressional pushback on the Iran operation creates domestic pressure toward resolution that did not exist last week.

Both portfolios are live on Autopilot.

Follow the Too Big To Fail Portfolio 👇 marketplace.joinautopilot.co…

Follow the Convergence Portfolio 👇 marketplace.joinautopilot.co…

Educational only. Not financial advice.

2

101

CTK Capital Intel Report

Wednesday, June 3, 2026

S&P 500 fell 0.14%, the Dow slipped 0.56%, Nasdaq edged up 0.01%. After three straight record closes the market paused. Not a breakdown — a rotation.

Iran launched ballistic missiles toward Kuwait and Bahrain. US forces responded with retaliatory strikes on Qeshm Island. Iran's Foreign Ministry warned it reserves the right to respond against any country allowing use of its airspace for attacks against Iran.

Brent crude climbed toward $97 for a third straight session. Analysts expect oil to trade between $90 and $100 until a lasting peace deal emerges. The macro green light on oil that briefly triggered at $87.93 last Friday is gone. The Strait of Hormuz remains effectively shut because Iranian sea mines laid in late May must be physically cleared before tankers resume — a process that outlasts any ceasefire signing. That detail matters. A diplomatic agreement does not automatically reopen the strait.

ADP private payrolls rose 122,000 in May versus the 117,000 estimate. The labor market is holding. A healthy jobs market with cooling inflation is the ideal backdrop — today's number confirmed that setup is still intact heading into Friday's nonfarm payrolls report.

Anthropic filed confidentially for an IPO on June 1. When the most consequential private AI company in the world files for a public listing it is not timing the top of a bubble — it is confirming that AI infrastructure demand is durable enough to support a publicly traded pure-play AI model company.

Friday's jobs report is the week's defining data point — 93,000 jobs expected with unemployment steady at 4.3%. Watch oil overnight. Any Iran escalation before the open creates immediate pressure at the bell. The five-day rebalance lock lifts Friday — deployment decisions ready to execute.

Both portfolios are live on Autopilot

Follow the Convergence Portfolio 👇

marketplace.joinautopilot.co…

Follow the Too Big To Fail Portfolio 👇

marketplace.joinautopilot.co…

*Educational only. Not financial advice.*

190

CTK Capital Intel Report

Tuesday, June 2, 2026

Markets held near all-time highs for a second straight session.

Penguin Solutions surged 19.23% — closing around $71 after trading near $44 just a few weeks ago.  Two things drove it.

First — the company brought in David Heard, Nokia’s President of Network Infrastructure and former CEO of Infinera, as a new board member. That is not a vanity appointment. It lines up directly with PENG’s AI Factory Platform push into converged memory and AI infrastructure for large-scale AI workloads.  Heard’s background in optical systems and large-scale networking is exactly what you want on the board of a company selling into AI data centers.

Second — the company reaffirmed its full-year fiscal 2026 outlook with both net sales and diluted EPS expected to be at the high end of guidance, citing Agentic AI-driven demand.  Revenue growth guidance raised to 12% year-over-year from 6%, with EPS guidance raised to $1.30 from $0.85.

Rosenblatt raised their price target to $65 from $54 maintaining a Buy rating. Stifel raised theirs to $66 from $24.

The other big story. Alphabet raised $80 billion for AI infrastructure Monday night — including a $10 billion private placement to Berkshire Hathaway. Buffett does not speculate. A $10 billion below-market commitment to GOOGL is a long-term conviction call, full stop.

What to watch tomorrow. Job openings data in the morning — first read on the labor market ahead of Friday’s nonfarm payrolls. Iran developments overnight remain the wildcard. Oil swung 7% yesterday on a single headline. Watch it before the open.

Both portfolios are live on Autopilot.

Follow the Too Big To Fail Portfolio 👇

marketplace.joinautopilot.co…

Follow the Convergence Portfolio 👇

marketplace.joinautopilot.co…

Educational only. Not financial advice.

1

116