2,320 Photos and videos

Stocks Weekly Recap

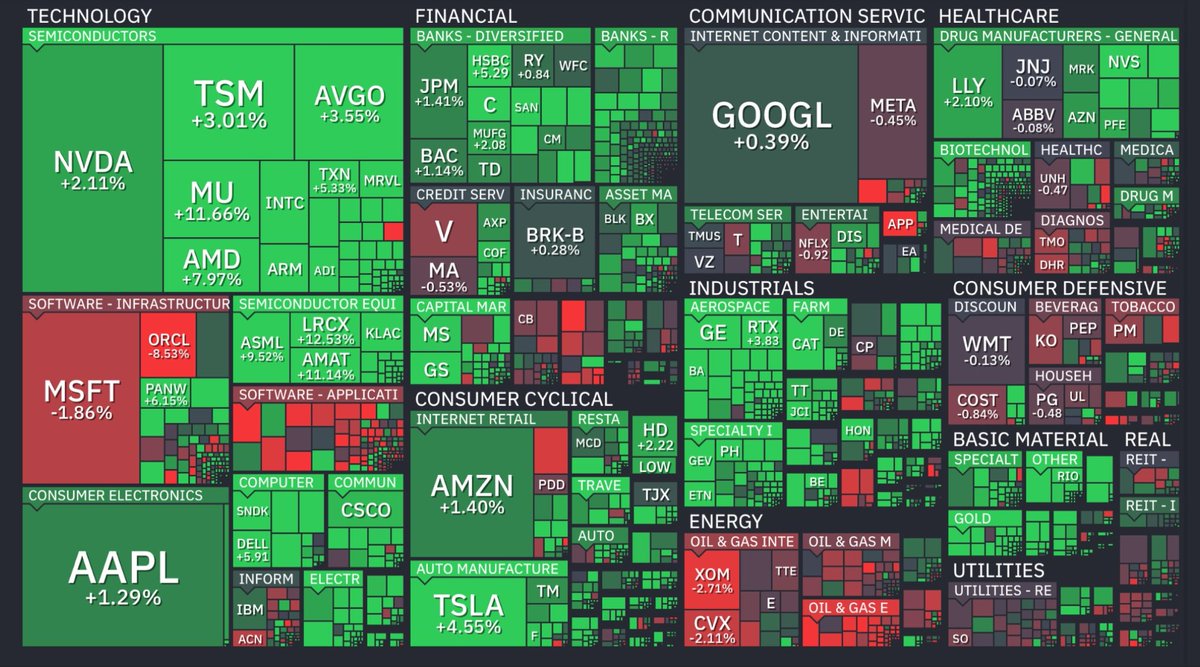

• S&P 500 -2.6%, Nasdaq -5%, Dow -0.5% — AVGO/Anthropic shock Iran risk erased solid PMI/JOLTS/NFP

• STOXX 50 -0.3% — on PMIs vs hot EU PPI, GDP miss & weak Retail

• Nikkei -3.6%, Hang Seng -3% — on tech rotation vs early Tencent/Tokyo Electron pumps

Markets tried to buy growth resilience and AI strength… until the AI shield cracked.

Early in the week, PMI/JOLTS strength, truce headlines and AI momentum kept risk alive.

By weekend the tape flipped from “soft landing” to “AI confidence shock.”

Monday opened green.

US ISM manufacturing beat while Europe/UK/DE/FR PMIs stayed solid, giving markets a global PMI relief rally despite renewed US-Iran strikes and oil ripping again.

Tech was still the shield: ORCL 10%, NVDA and MU both over 6%. S&P 500 0.26%, Nasdaq 0.59%, Dow 0.15%, STOXX 50 0.33%, Nikkei 1.64%, Hang Seng 0.53%.

Tuesday, selective risk-on trade.

US JOLTS beat hard, Europe pushed higher despite hot Core CPI, and Hong Kong ripped on Tencent 10%.

AVGO, MU and AAPL helped tech while Nvidia stayed mostly flat after Monday’s pump.

But commodities were already flashing warning signs as oil stayed bid. Nasdaq 0.93%, Dow 0.76%, STOXX 50 0.84%, Nikkei 0.58%, Hang Seng 2.93%.

Wednesday was the first real crack.

Trump warned the Hormuz blockade could last 3 months, crude jumped again, and markets started pricing prolonged Middle East conflict.

Macro was not terrible: ADP beat, factory orders beat, services data held up, and China RatingDog services beat hard.

But oil shock risk outweighed the macro support. S&P 500 -0.74%, Nasdaq -0.44%, Dow -1.13%, STOXX 50 -0.97%. Nikkei held 1.21% on Tokyo Electron/AI momentum, while Hang Seng dumped -2.41% as Chinese tech rotated lower.

Thursday brought a relief bounce.

Trump said he is “reluctant” to war, so oil dipped hard, helping the Dow and cyclicals recover.

Still, the labor picture softened. Unit Labor Costs came in below estimates, which helped reduce the cleanest stagflation panic, but semis were already messy.

AVGO crashed after earnings, AMD and Micron lagged, while NVDA and GOOGL held the AI narrative together. S&P 500 0.41%, Dow 1.59%, STOXX 50 1.18%, Nikkei 0.42%, Hang Seng -0.74%.

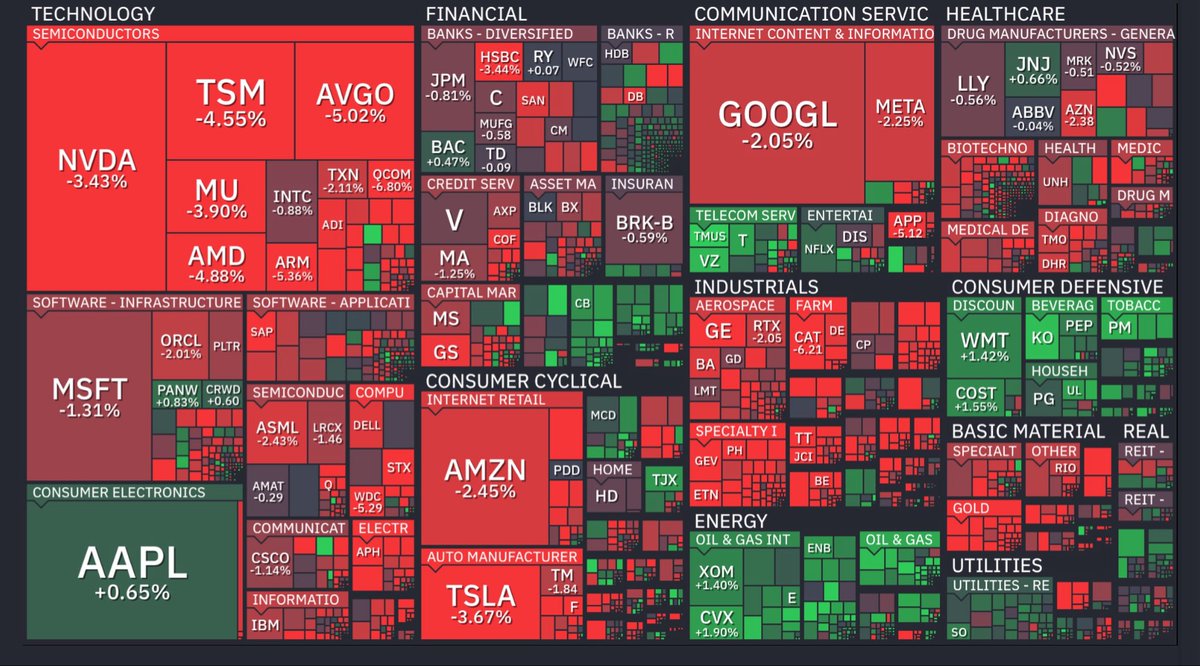

Friday broke the week.

US macro was not bad enough to justify the size of the selloff. NFP beat, private payrolls beat, credit beat, Canada jobs crushed, and US unemployment stayed at 4.3%.

Stocks traded the fear stack instead: Iran/Lebanon escalation and now AI confidence risk.

AI leadership cracked hard. NVDA fell -6.2%, AMD and QCOM dropped around -11%, Intel and Micron joined the selloff, META and TSLA fell roughly -6%, and Broadcom extended its post-earnings crash to over -20% in two days.

Anthropic’s global AI-freeze headline added another layer. S&P 500 -2.64%, Nasdaq -5.07%, Dow -1.74%, STOXX 50 -1.64%, Nikkei -5.9%, Hang Seng -3.18%.

Closing out the week:

S&P 500 finished -2.6%, Nasdaq collapsed -5%, and Dow slipped -0.5%. STOXX 50 held near-flat at -0.3%, but Europe still felt the pressure from hot PPI, weak retail and EU GDP miss. Asia cracked hard: Nikkei -3.6% and Hang Seng -3%, as tech rotation overwhelmed early Tencent/Tokyo Electron strength.

Though, macro did not fully break. Growth data was mixed but alive, and labor still held. The real break came from sentiment.

Once AI/semis stopped acting like the market’s shield, the whole risk-on trade started looking fragile.

Furthermore, stocks erased theirs longest weekly gain streak of this century.

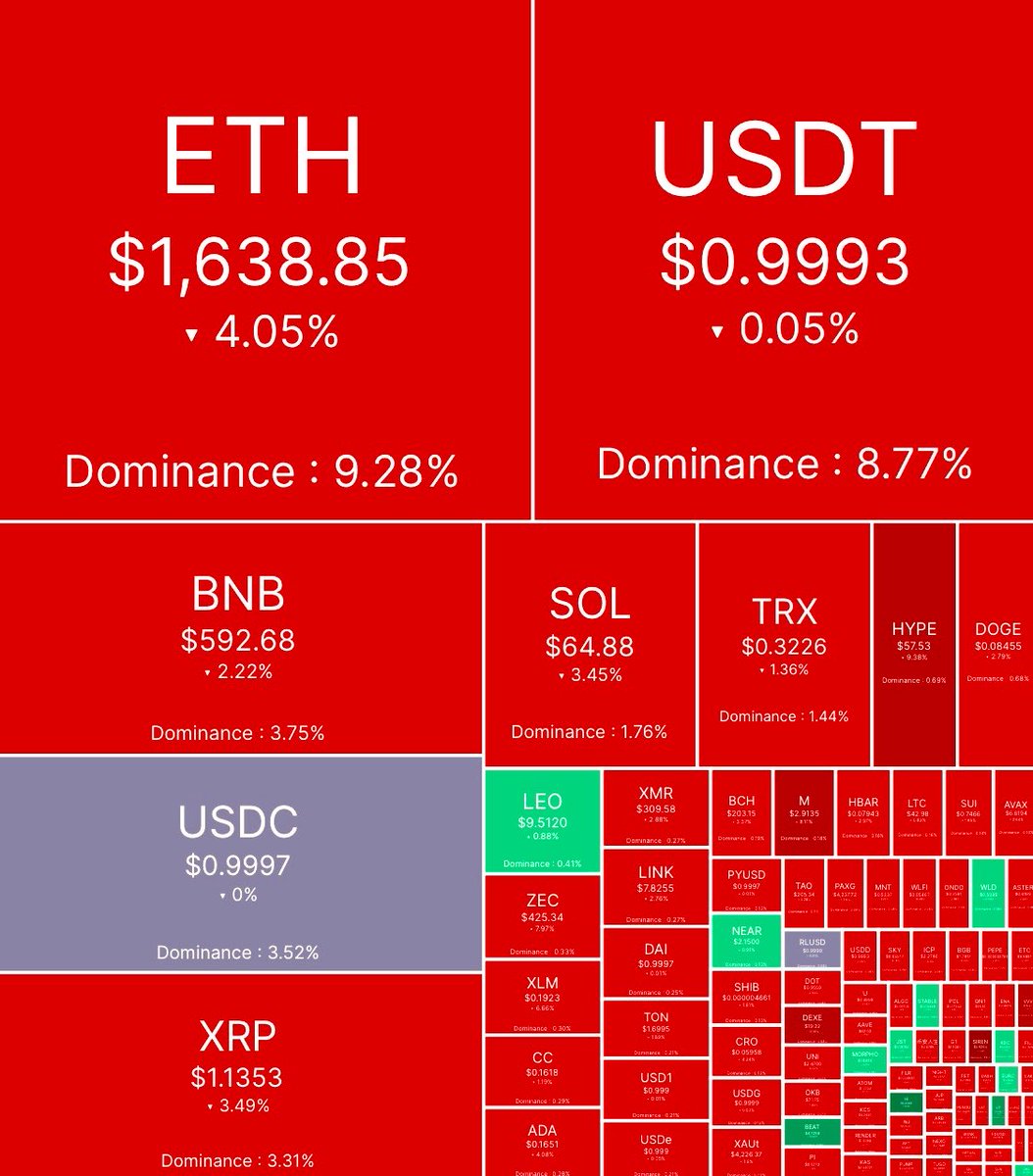

Crypto also confirmed the risk-off tone.

BTC lost $62K, ETH dumped almost -10%, Open Interest fell while liquidations surged.

If AI stabilizes, markets can still frame this as a brutal tech reset.

But if semis keep breaking while geopolitics stays hot (as after recent US-Iran strikes), this starts looking less like rotation and more like a risk-off regime.

Was this indeed the first sign the market’s strongest pillar is finally cracking as stocks extend rotation?

Stocks Weekly Recap

• S&P 500 1.4%, Nasdaq 3%, Dow 0.9% — on 60d plan hopes, oil dip & cooler PCE vs weak GDP/Jobs/Housing

• STOXX 50 0.55% — on cooler DE/FR/ES CPI & EU/IT Conf vs hot FR/IT PPI & FR GDP miss

• Nikkei 4.7%, Hang Seng -1% — JP rallied on IP/Retail/Unemp beats; HK lagged on rare-earth/TW risk & CN FDI

Markets started pricing the 60-day US-Iran framework this week, but not without stress. Oil whipsawed on strikes, Hormuz headlines and unsigned deal terms, while cooler PCE and lower inflation prints helped risk sentiment. Japan stood out on strong domestic data, while Europe and Hong Kong lagged on growth/geopolitical pressure.

Monday closed for (US) Memorial Day.

Tuesday opened volatile as renewed US-Iran strikes and an oil rebound hit sentiment. CB Confidence and M2 beat, but hot BoJ CPI, weak CN FDI and Spanish PPI kept inflation/geopolitical risk alive. S&P 500 0.61%, Nasdaq 0.59%, Dow -0.94%, STOXX 50 -1.03%, Nikkei 0.37%.

Wednesday was more about stabilization than a full breakout. Oil dipped as traders repriced the fragile Qatar/US-Iran framework, but Trump denied sanctions relief and US ADP/MBA missed. Nasdaq 0.2%, Dow 0.37%, Nikkei -0.4%, Hang Seng -1.04%.

Thursday, solid US tech follow-through.

Cooler PCE gave the Fed breathing room, but weak GDP, jobless claims and housing kept growth concerns alive. Europe stayed red on hot FR/IT PPI, while Asia split as Nikkei rose and Hang Seng fell on rare-earth/Taiwan risk despite HK trade beat. S&P 500 0.58%, Nasdaq 0.83%, Nikkei 0.87%, STOXX 50 -0.39%, Hang Seng -0.67%.

Friday closed mixed but steadier. Improved US Trade, cooler DE/FR/ES CPI and stronger JP IP/Retail helped, while France/Canada GDP misses and unresolved Iran terms kept the rebound selective. S&P 500 0.22%, Dow 0.62%, Nikkei 0.79%, STOXX 50 -0.34%.

The Story of the Week:

Hopes around the leaked 60-day US-Iran framework (eg. Hormuz mine-clearing, no transit tolls, temporary oil waivers and frozen-asset negotiations) helped oil ease and supported US equities. Still, the deal remains unsigned, with uranium terms and Trump’s “no-money” clause keeping headline risk alive.

Meanwhile, inflation cooled in Europe and Japan, but growth signals weakened in the US, Canada and France. Markets remained highly volatile on every Hormuz and military headline.

US-Qatar/Iran plan to reopen Hormuz seems to be collapsing once again due to renewed military activity.

This setup might spike the first weekly stocks dump in multiple months.

Do you see markets climbing more despite escalating Middle East conflict?

8

2

46

2,792

POV: You bought $SPCE because you expected it to benefit from SpaceX IPO

Meanwhile, stock crashed -25%

Cause traders thought its $SPCX ticker…

5 hours before the biggest IPO in history.

From 2001-2025, all major US IPOs combined raised around ~$790B.

SpaceX alone is raising ~$75B.

That’s about 10% of 25 years of IPO money in one deal.

But who actually benefits from $SPCX?

Here’s the list:

• $GOOGL gains from direct SpaceX stake exposure.

Alphabet becomes one of the biggest public-market ways to indirectly own SpaceX upside without buying SPCX directly.

• $SATS gains as the clearest public SpaceX proxy.

EchoStar has direct SpaceX equity exposure plus a Starlink direct-to-cell partnership angle.

• $RKLB gains as the “next SpaceX” trade.

Rocket Lab becomes the cleanest public launch comp when investors start looking for smaller high-beta space names.

• $ASTS gains from the satellite-to-phone narrative.

If Starlink pulls attention into direct-to-device connectivity, AST SpaceMobile becomes one of the first hype names traders chase.

• $LUNR gains from lunar economy rotation.

SpaceX IPO shines more light on NASA, Artemis, moon missions, lunar landers and commercial space infrastructure.

• $RDW gains from space infrastructure demand.

More launches means more need for robotics, components, manufacturing and in-orbit systems.

• $FLY gains as another launch/lunar pure-play.

Firefly rides the “alternative launch provider” narrative as investors search beyond SpaceX.

• $PL gains from satellite data growth.

More satellites in orbit means more demand for Earth imaging, geospatial analytics and AI-driven data products.

• $VOYG gains from orbital infrastructure hype.

Commercial space stations and next-gen space platforms become easier for investors to understand after SPCX.

• $BKSY gains from satellite intelligence demand.

Defense, real-time imagery and space-based analytics become more valuable as the whole sector gets repriced.

SpaceX IPO is not just about SpaceX.

It creates a public valuation benchmark for the entire commercial space economy.

Tesla did it for EVs.

Nvidia did it for AI.

Bitcoin did it for crypto.

Now SpaceX could do it for space.

14

4

46

9,374

Stocks reversed SpaceX IPO delay-led dip as MoU has “never been closer” to signature.

• S&P 500 0.5%, Nasdaq 0.43%, Dow 0.6% — on UMich/oil relief

• STOXX 50 0.23% — on inline DE/FR/ES CPI vs weak UK GDP/IP/Trade

• Nikkei 1.1%, Hang Seng 0.7% — on talk & CN Loans

Next:

• US/EU IP, CA HS/Sales, CH PPI/SECO Jun 15

• US Empire/NAHB, EU/SK/IT Trade Jun 15

Tape was messy.

Space-related stocks dipped hard first because SpaceX IPO trading got delayed in Nasdaq auction for 2 hours after the bell.

Virgin Galactic (SPCE) crashed -32%, while other companies which supposed to benefit from IPO followed the selloff: $LUNR -13%, $RKLB & $SATS -11%.

Basically charts looked rugged before trading even existed.

Then SPCX finally went live, ripped above 20%, and the market stopped treating the IPO delay like some disaster.

Though, it didn’t really limit the space-related equities riskoff.

Bigger stock rescue came from macro oil geopolitics.

UMich Sentiment beat.

Consumer expectations beat.

1Y and 5Y inflation expectations cooled.

So after yesterday’s hot PPI weak jobs mix, markets finally got something they could actually buy.

At the same time, oil dumped -2.5% on peace talks.

That’s the real fuel behind the equity bid.

The market is pricing the Islamabad MoU as real de-escalation, especially after Araghchi said the framework has “never been closer” to signature.

So equities are saying:

“Buy the dip.”

$AMD 4.7%, $TSLA 1.8%.

Unfortunately, ain’t a full risk-on yet.

Amazon & Micron still -1.2%.

It’s a selective re-risk after the SpaceX IPO chaos got absorbed and oil kept bleeding.

Funny part?

People who bought SPCE thinking it was the SpaceX trade got nuked, while the actual SPCX IPO ripped.

That’s basically today’s market in one sentence.

Confusion first.

Relief later.

Still, the setup is fragile.

Stocks are green because the market believes the deal story survives the weekend.

Oil is down because the market believes Hormuz risk is fading.

But geopolitics is still hot.

- Hormuz is unstable.

- Hezbollah denies truce.

So yeah, stocks recovered.

But if this “final text” deal breaks again, does this equity bid finally get smoked?

Stocks rip on US strike-cancel/deal-signing bid.

• S&P 500 1.75%, Nasdaq 4.15%, Dow 2.30% — on oil >5% dump vs hotter PPI/Jobs

• STOXX 50 3.13% — on Trump’s “great settlement” vs ECB hold & DE C/A miss

• Nikkei 5.9%, Hang Seng 1.4% — on deal hopes vs JP BSI miss

Next:

• UMich, UK GDP/Trade, CA WS, HK PPI Jun 12

• JP/HK/UK IP, DE/FR/ES CPI, CN Loans Jun 12

This was a headline squeeze.

Macro was too bearish for this kind of move.

US PPI came in hot: 1.1% MoM vs 0.7%, 6.5% YoY vs 6.4%.

Jobs also softened, with claims missing.

Normally that combo is ugly:

- Higher inflation pressure.

- Weaker labor tape.

- Less room for clean Fed relief.

But markets ignored it because geopolitics flipped the trade.

- Trump cancelled Iran strikes.

- Then pushed “deal signing date soon.”

- Then oil dumped hard.

So equities treated it like the worst-case Middle East tail risk got delayed.

Not solved.

Delayed.

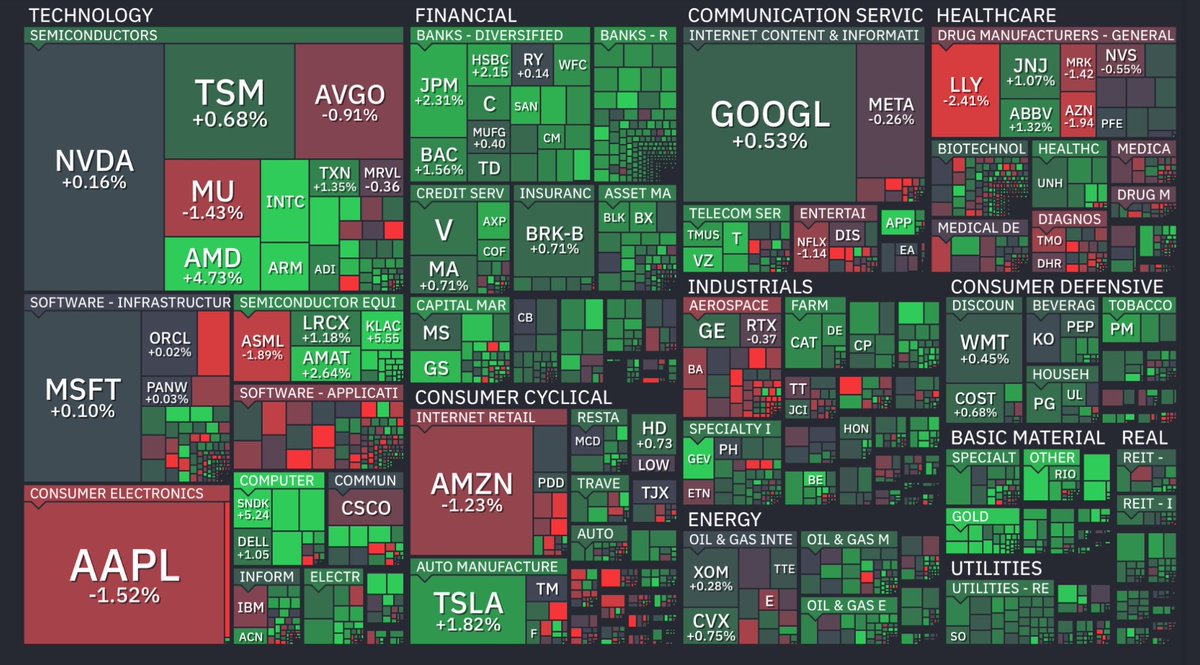

The heat map says everything.

$MU 12%, $AMAT 11%.

Basically a forced re-risking into the same AI/semis basket everyone was dumping earlier.

Though…

Oracle still crashed -8.5%, while Microsoft and Meta remained red.

So this is more like a violent semis relief bid after war/AI-risk got pushed back.

Market choosing to believe deal first and inflation/jobs/Hormuz later is a dangerous setup.

Just a single Iran denial of current terms or delay can change the whole trade in seconds as we approach “July Oil Red Zone.”

Do you trust this rally or is it a trap?

8

2

33

1,060

Geopolitics shifts again as deal-signing talk turns into Islamabad “final text”, while new NATO/Cuba fronts open.

• Trump vs Iran leaks: blasted leaked ceasefire/deal terms from Iranian media as “dishonorable” and “fake”, later reposted Araqchi post giving WH deal legitimacy.

• Islamabad MoU: Iranian FM Abbas Araghchi said the final framework (dubbed the “Islamabad Memorandum of Understanding”) has “never been closer” to signature.

• Hezbollah rejects truce: Hezbollah formally rejected the new US-brokered ceasefire agreement, leaving the Israel-Lebanon front effectively unchanged.

• Official Iran terms: a senior Trump administration official outlined Washington’s written interim demands:

“Iran must dismantle its nuclear program, destroy nuclear material, halt proxy funding and guarantee permanent reopening of Hormuz.”

• Zero-cash caveat: the same official said none of Iran’s money gets released until Tehran performs, clashing with Iran-linked claims around an upfront $24B frozen-asset release.

• Islamabad breakthrough: Pakistan PM Shehbaz Sharif said the US and Iran have formally agreed on the final text of a peace deal.

• Hormuz still under fire: despite the “deal soon” narrative, the US Navy shot down two Iranian one-way attack drones targeting commercial vessels in the Strait.

• India protest: New Delhi summoned the US Charge d’Affaires after three Indian sailors were killed in the Gulf of Oman this week.

• Trump blames Iran: Trump accused Iran of launching the drone strike against Indian commercial vessels, calling it “TOTALLY UNACCEPTABLE.”

• Ukraine Russia Day strike: Kyiv launched a long-range drone wave on June 12 targeting Russian economic infrastructure.

• Tatarstan refineries hit: Ukrainian drones struck the Taneco and TAIF-NK refineries in Nizhnekamsk, setting them ablaze and forcing cancellation of Russia Day events.

• Missile supply chain hit: the same wave struck the Togliattikauchuk plant in Samara, which produces synthetic rubber used for solid fuel in Russian tactical and ballistic missiles.

• Russian retaliation: Moscow responded with a 117-drone barrage on Ukraine; 102 were downed, but a strike in Boryspil triggered a 2,000 sq. meter infrastructure fire.

• Tyre/Nabatieh strikes: heavy Israeli strikes hit Tyre and Nabatieh, damaging Tyre’s ancient Roman-era columns and killing at least six people.

• Japan NATO pivot: Japanese PM Sanae Takaichi plans to attend the NATO summit in Ankara and warned Indo-Pacific and European security are now inseparable.

• Japan-Philippines RAA: Tokyo and Manila are moving to operationalize the Reciprocal Access Agreement, opening the way for direct troop deployments and joint military actions on Philippine soil near the South China Sea.

• US jet cuts to NATO: a leaked US military directive shows Washington may withdraw up to one-third of fighter jets assigned to NATO ops to preserve assets for the Middle East blockade and Pacific operations.

• Cuba flashpoint: Marco Rubio announced new sanctions against Cuba’s state oil and gas company, accusing Havana of hoarding fuel for its military and reselling it on secondary markets.

• Cuba blockade risk: the move triggered fresh humanitarian and fuel-crisis fears as Cuba faces a near-total fuel and naval blockade.

• World Bank warning: the bank warned a prolonged Middle East war could drag global growth down to 2.5% this year, with downside risk to 1.3% if Hormuz disruption remains severe.

Chaos.

The “deal soon” story just got stronger through Islamabad, but the gap is brutal…

Washington wants performance first, while Tehran-linked channels keep pushing money-first expectations.

At the same time, the conflict map is widening.

Iran talks are accelerating.

Lebanon rejected the pause.

India is now pulled deeper in.

Japan is leaning into NATO.

And Cuba just turned into a blockade front.

Escalation is still what’s actually trading.

Is this >25th deal attempt going to be different?

Geopolitics whipsaws as deal-signing talk returns, while Trump cancels Iran strikes & Hormuz shuts.

• Trump: cancelled Thursday strikes after warning US would hit Iran “VERY HARD TONIGHT.”

• US-Iran deal: Trump says "we just made a great settlement" with Iran after noting that the time and place of an Iran deal signing will be “announced shortly.”

• Pakistan channel: Iranian Foreign Minister Araghchi may travel to Pakistan next Saturday as another regional diplomatic track opens.

• Fars optimism: IRGC-linked Fars says chances of Iran approving a US deal are "relatively high" after Washington accepted Tehran's proposed text.

• Qatar mediation: key gaps in Iran-US talks were reportedly resolved during negotiations with Qatari mediators.

• Iran MOU denial: Iran says it has not yet agreed to any MOU document with the US.

• Israeli skepticism: Israeli officials were stunned by Trump cancelling Iran strikes, with one saying they need to hear what Iran actually announces.

• Deal trust gap: Israeli side no longer fully trusts Trump’s version of events, making the “deal soon” narrative shakier.

• Deal claim: Trump said “final points” of a transaction were conceptually approved by all parties.

• Naval blockade holds: Trump says the US naval blockade of Iranian ports in the Gulf of Oman stays in “full force and effect” until a deal is signed.

• Hormuz shutdown: Iran announced total closure of the Strait of Hormuz to commercial ships and oil tankers, warning vessels may be fired on.

• Gulf base attacks: IRGC launched overnight missile/drone barrages targeting US airbases across Kuwait, Jordan and Bahrain.

• Kuwait airspace: Kuwait temporarily shut its airspace after overnight Iranian missile-defense scrambles, then reopened.

• Ukraine deep strike: Kyiv used FP-5 Flamingo cruise missiles to hit the VNIIR-Progress military plant in Cheboksary, over 900km inside Russia.

• Abramovich UA-RU backchannel: Zelensky confirmed Roman Abramovich quietly carried a message from Putin to Kyiv on a possible negotiation framework.

• Rosneft hub hit: Ukrainian drone swarms struck Samara’s Kuibyshev refinery, forcing it offline after fire damage.

• Tyre escalation: IDF expanded operations into Tyre’s historic Christian Quarter.

• Tyre exodus: at least eight more civilians were killed as the city was described as nearly empty, with civilians fleeing inland.

• Japan-China crisis: Beijing issued sharp warnings after Japan said a Taiwan attack could trigger collective self-defense.

• EEZ collision: Japan and the Philippines opened maritime boundary talks east of Taiwan, with China warning against “illegal actions.”

• Taiwan HIMARS trigger: China expanded warship/aircraft presence near Taipei after Taiwan’s US-supplied HIMARS live-fire drills.

• Russia encirclement: Chinese vessels operating around the First Island Chain are reportedly coordinating maneuvers with Russian forces near Japan.

• US weapon delay: European generals warn the US is delaying foreign military sales to Europe while prioritizing its own stockpiles and Middle East ops.

• NATO 2029 clock: Germany’s army chief warned NATO now sees Russia capable of direct invasion by 2029.

• NATO 5% target: Mark Rutte is pushing the 5% GDP defense benchmark, while Meloni says Italy will raise defense spending to 2.8%.

• Huawei ultimatum: US told NATO allies to remove Huawei from critical communications networks to preserve intelligence access.

• Market whiplash: stocks rebounded and oil dropped after Trump cancelled the planned evening missile strikes.

What a rollercoaster.

Trump cancelled strikes and now says the deal signing details are coming “shortly.”

So far signals are positive, but the whole “deal soon” bid can break again fast, if Iran delays, shifts or eventually denies terms.

Diplomacy is alive.

But trust is not.

Does this look like a real deal forming or just another pause amid SpaceX IPO before re-escalation?

7

3

28

2,186

Commodities decouple further on “formally agreed” deal, while metals still hedge the “Hezbollah rejection” trust gap.

• Brent $85.77 -2.69%, WTI $82.64 -2.62%

• Gold $4,219 0.15%, Silver $68 0.97%

• Copper ~$14.38K/t 1.32%

• NatGas $3.07 1.92%, TTF €46.78 -5.87%

Next:

• EIA Jun 17

• IEA OMR Jun 17

Crude keeps sliding.

Islamabad “final text” optimism and Araghchi’s “never been closer” line are still pushing the market to strip more Middle East risk premium out of oil.

But the rest of the board says trust is still not there.

- Crude is pricing “deal soon.”

- Metals are pricing “show me.”

- TTF is pricing less regional panic.

- NatGas bids on weather forecasts.

That fits the latest geopolitics pretty well.

Iran talks are accelerating, but Hormuz is still unstable and Hezbollah rejecting the truce ain’t making it better.

Anyway.

Oil is definitely fading the threat.

Considering global inflation relief, do you see oil going even lower due to “shadow” transit?

Commodities digest Trump’s deal teaser and fresh US-Iran-Pakistan meeting signals.

• Brent $88.14 -5.75%, WTI $84.86 -5.74% — “very hard hits” bid reversed

• Gold $4,212 3.49%, Silver $67.35 6.29%

• Copper ~$14.19K/t 3.11%

• NatGas $3.01 -3.12%, TTF €49.69 -0.6%

Next:

• EIA Jun 17

• IEA OMR Jun 17

Oil got rugged by the peace headline.

Trump cancelled strikes, said deal-signing details are coming shortly.

Market immediately stripped crude’s panic premium (eg. Hormuz declared shut and US blockade active until a deal is actually signed.)

PMs & copper pumping at the same time show that traders are still hedging the trust gap.

Makes sense.

As Iran says no MOU yet Israel don’t believe Trump’s version either.

So crude is pricing “deal soon.”

Metals are pricing “prove it.”

Literally.

Peace trade with zero trust behind it.

EU TTF staying mostly flat says it all.

Do you see crude going lower as US “shadow Hormuz transit” appears to be working?

3

22

602

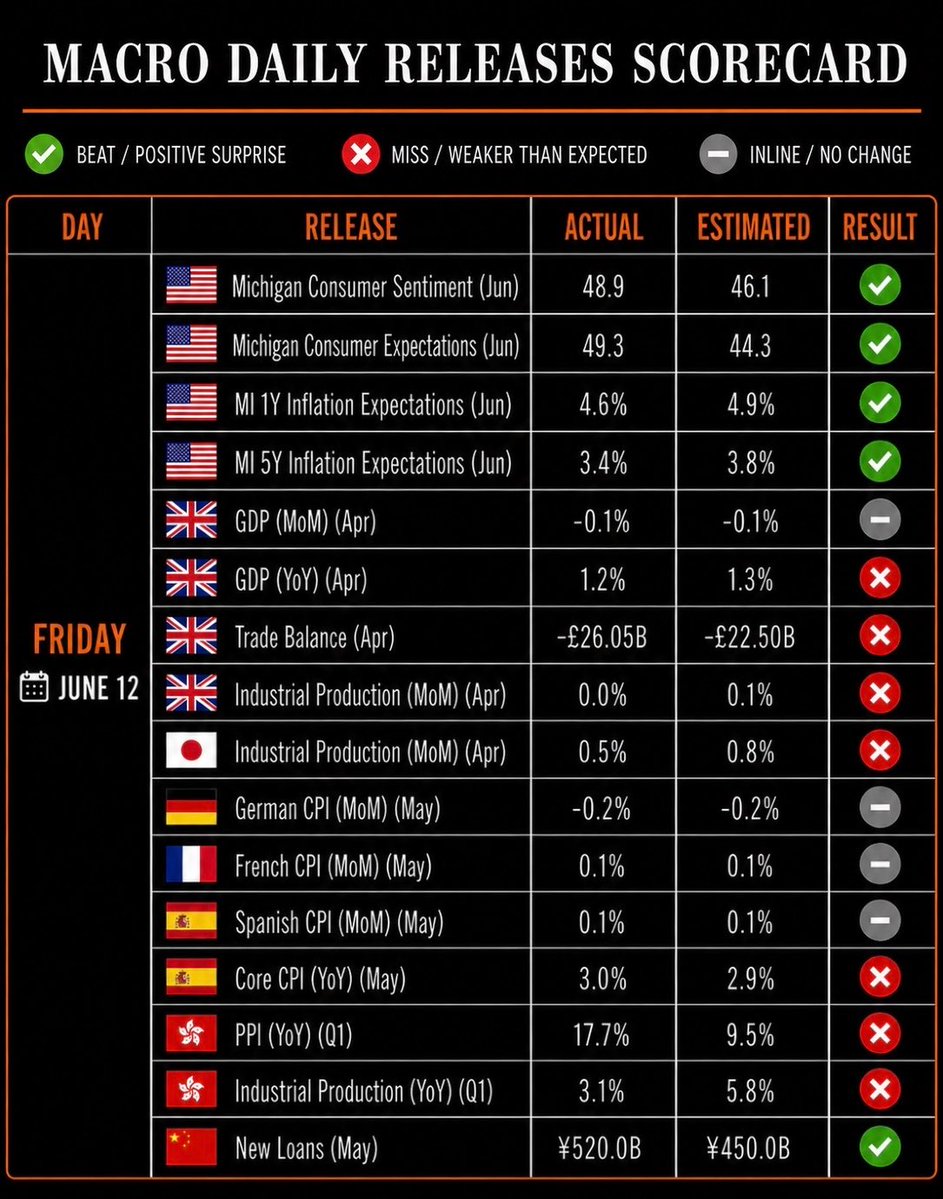

Macro gets UMich-led relief.

• UMich 48.9 vs 46.1, 1Y infl 4.6% vs 4.9%

• UK GDP -0.1% inline; Trade -£26.05B vs -£22.5B

• CPI (YoY): DE 2.6%; FR 2.4%; ES 3.2% (all inline)

• IP: JP 0.5% vs 0.8%; UK IP 0% vs 0.1%

• HK PPI 17.7% vs 9.5%

• CN Loans ¥520B vs ¥450B

Next:

• US/EU IP, CA HS/Sales, CH PPI/SECO Jun 15

• US Empire/NAHB, EU/SK/IT Trade Jun 15

Today’s tape way better than yesterday.

UMich gave markets the exact relief they wanted: sentiment beat, consumer expectations beat, and inflation expectations cooled on both 1Y and 5Y.

That matters after yesterday’s hot PPI weak jobs mix.

But it’s not clean.

UK GDP still contracted MoM, trade missed badly, and industrial production missed.

Europe’s CPI prints mostly landed in line, but Spain core CPI ticked hotter at 3.0%, so inflation is not fully dead either.

China credit was stronger with new loans beating, but loan growth still slipped to 5.5%.

By the end of the day.

- US consumer mood improved.

- Inflation expectations cooled.

- UK growth still looks weak.

- China liquidity surprised higher.

- Europe is stable but not dovish.

- Oil is trading the Iran-deal headline.

That explains why stocks are green while crude is down.

S&P, Nasdaq and Dow are all bid.

Brent and WTI are dumping because the market is pricing Islamabad deal optimism and lower Hormuz risk.

But the whole trade still depends on whether this “final text” story survives the weekend.

Do you expect “final text” deal to survive the weekend?

Macro prints hot PPI & weak jobs.

• US: PPI 1.1% vs 0.7%, 6.5% YoY vs 6.4% (Core 0.4% vs 0.5%, 4.9% YoY vs 5.4%); Jobless 229K vs 220K

• ECB: held 2.25-2.40%; Lending 25bp

• CA BP -7.6% vs -3.7%

• DE C/A €13.8B vs €24.5B

• JP BSI -1.8 vs 4.2; SK Unemp 2.8%

Next:

• UMich, CA WS, UK GDP/Trade, HK PPI Jun 12

• JP/HK/UK IP, DE/FR/ES CPI, CN Loans Jun 12

US PPI came hot on headline MoM/YoY.

6.5% inflation ain’t a “cooling” story.

Core looked better than expected, but still sits at 4.9% YoY, which is not exactly dovish fuel either.

Then jobs added another problem.

Initial claims and continuing claims both missed, meaning the labor side is getting softer while price pressure is still sticky.

Yes… Ugly mix. Tho not full stagflation.

Meanwhile, Europe’s ECB held rates as expected and presser highlighted widening oil crisis.

And what do we have so far?

- Inflation pressure is still alive.

- Growth confidence is leaking.

- Central banks are stuck waiting.

And all of this is happening while the geopolitical tape is pure rollercoaster.

Trump is talking Iran deal-signing again, but Hormuz is declared shut, the blockade remains active, and Israel does not fully trust the White House version.

Anyway.

Iran has not yet agreed to any deal, despite Trump claims.

So we are literally trading macro inside a headline minefield.

Will bearish hot CPI/PPI effect kick in even harder if most recent “settled” deal breaks down once again?

2

1

18

441

Meanwhile $SPCX is still in the Nasdaq auction 2 hours after the bell

This is normal for big IPOs apparently

charts looking like they got rugged before they even existed

POV: You bought $SPCE because you expected it to benefit from SpaceX IPO

Meanwhile, stock crashed -25%

Cause traders thought its $SPCX ticker…

4

1

19

2,081

5 hours before the biggest IPO in history.

From 2001-2025, all major US IPOs combined raised around ~$790B.

SpaceX alone is raising ~$75B.

That’s about 10% of 25 years of IPO money in one deal.

But who actually benefits from $SPCX?

Here’s the list:

• $GOOGL gains from direct SpaceX stake exposure.

Alphabet becomes one of the biggest public-market ways to indirectly own SpaceX upside without buying SPCX directly.

• $SATS gains as the clearest public SpaceX proxy.

EchoStar has direct SpaceX equity exposure plus a Starlink direct-to-cell partnership angle.

• $RKLB gains as the “next SpaceX” trade.

Rocket Lab becomes the cleanest public launch comp when investors start looking for smaller high-beta space names.

• $ASTS gains from the satellite-to-phone narrative.

If Starlink pulls attention into direct-to-device connectivity, AST SpaceMobile becomes one of the first hype names traders chase.

• $LUNR gains from lunar economy rotation.

SpaceX IPO shines more light on NASA, Artemis, moon missions, lunar landers and commercial space infrastructure.

• $RDW gains from space infrastructure demand.

More launches means more need for robotics, components, manufacturing and in-orbit systems.

• $FLY gains as another launch/lunar pure-play.

Firefly rides the “alternative launch provider” narrative as investors search beyond SpaceX.

• $PL gains from satellite data growth.

More satellites in orbit means more demand for Earth imaging, geospatial analytics and AI-driven data products.

• $VOYG gains from orbital infrastructure hype.

Commercial space stations and next-gen space platforms become easier for investors to understand after SPCX.

• $BKSY gains from satellite intelligence demand.

Defense, real-time imagery and space-based analytics become more valuable as the whole sector gets repriced.

SpaceX IPO is not just about SpaceX.

It creates a public valuation benchmark for the entire commercial space economy.

Tesla did it for EVs.

Nvidia did it for AI.

Bitcoin did it for crypto.

Now SpaceX could do it for space.

17

3

44

9,582

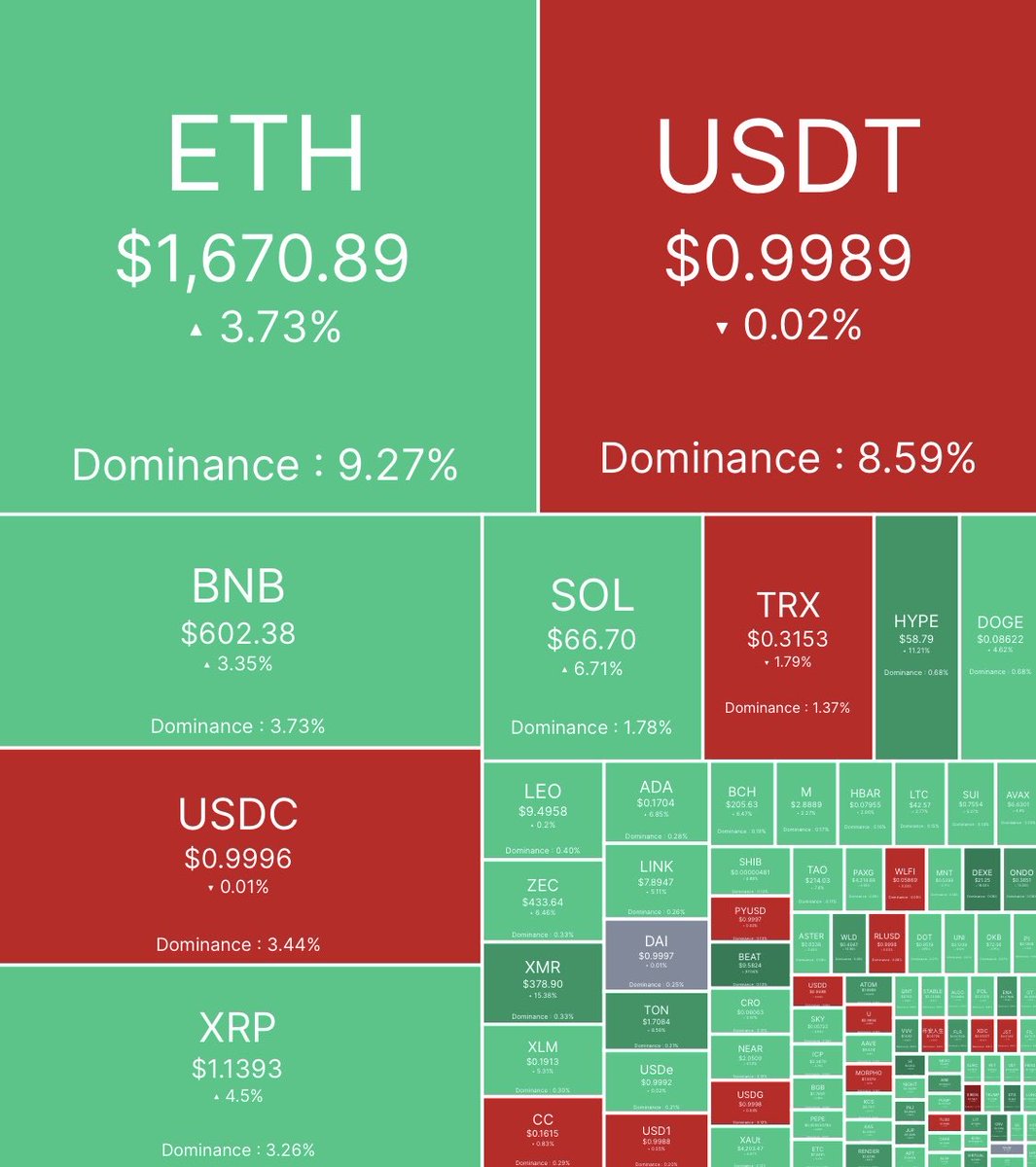

Crypto stages comeback as Trump deal-signing talk revives risk, despite ugly macro.

• $BTC $63.32K 3.49%, $ETH $1.67K 3.73%

• Total MCap $2.151T 2.77%

• Futures OI $104.36B 3.65%

• 24h Liqs $272M -35%

• Bitcoin Dominance 58.36%

• Fear & Greed ~12, AltSeason ~47

Next:

• UMich, CA WS, UK GDP/Trade, HK PPI Jun 12

• JP/HK/UK IP, DE/FR/ES CPI, CN Loans Jun 12

Crypto finally got a relief bid.

Not because macro turned clean.

It didn’t.

US PPI came hot, jobless claims missed and ECB moved into hold/hike.

So this bounce is mostly geopolitics.

Trump cancelled Iran strikes and brought back the “deal signing soon” narrative.

But look at the details.

OI climbed back above ~$104B.

Leverage returns before trust is fixed.

Meanwhile, Iran still denied any MOU.

Hormuz was declared shut again.

So crypto is trading the headline that peace might be close. And that’s the scary part.

This bounce has all the potential to become another trap, it just needs Iran to say anything contradicting.

And it’s over… Again.

How long do you expect the peace tape to survive?

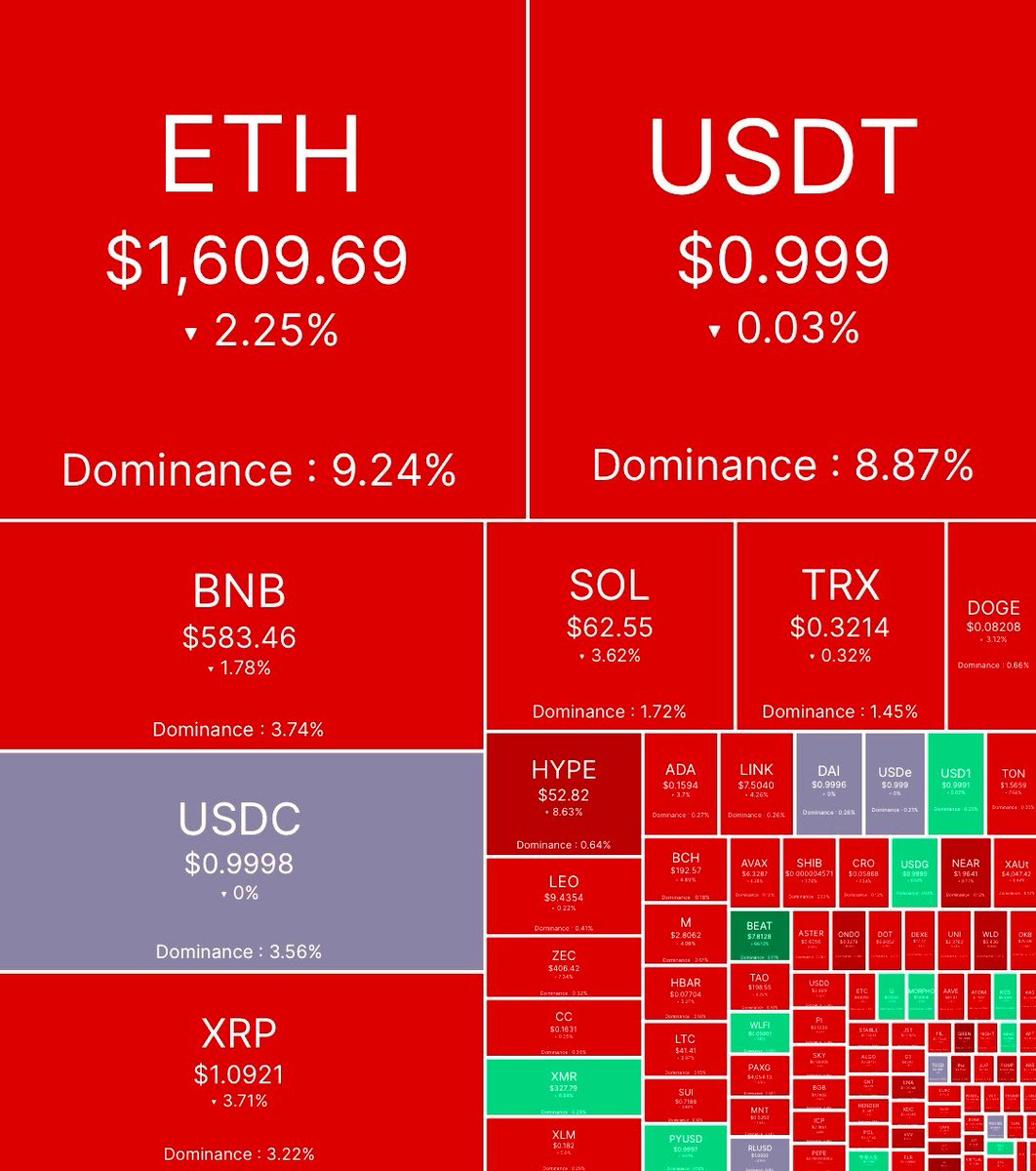

Crypto sinks on Trump’s “Iran will pay the price” & CPI-led rate hikes odds spike.

• $BTC $61.23K -0.75%, $ETH $1.61K -2.25%

• Total MCap $2.086T -1.14%

• Futures OI $100.74B -1.94%

• 24h Liqs $394M -14%

• Bitcoin Dominance 58.35%

• Fear & Greed ~9, AltSeason ~47

Next:

• US PPI/Jobs, CA BP, ECB Rate Jun 11

• JP BSI Mfg, DE C/A, SK Unemp Jun 11

Market tried to breathe.

Then macro and geopolitics stepped on its neck again (eg. US-Iran attacks & Japan/US hot inflation prints).

The weird part: liquidations cooled to ~$394M from yesterday’s ~$460M.

So this is not just one massive wipeout candle anymore.

OI dropped again too, meaning leverage is leaving while price still cannot recover.

That is traders getting tired.

Exactly the type of setup where crypto stops trading like “future money” and starts trading like high-beta liquidity trash.

Especially after CISA warned that new cyber front just opened.

Are you ready for another shakeout?

2

1

26

843

Commodities digest Trump’s deal teaser and fresh US-Iran-Pakistan meeting signals.

• Brent $88.14 -5.75%, WTI $84.86 -5.74% — “very hard hits” bid reversed

• Gold $4,212 3.49%, Silver $67.35 6.29%

• Copper ~$14.19K/t 3.11%

• NatGas $3.01 -3.12%, TTF €49.69 -0.6%

Next:

• EIA Jun 17

• IEA OMR Jun 17

Oil got rugged by the peace headline.

Trump cancelled strikes, said deal-signing details are coming shortly.

Market immediately stripped crude’s panic premium (eg. Hormuz declared shut and US blockade active until a deal is actually signed.)

PMs & copper pumping at the same time show that traders are still hedging the trust gap.

Makes sense.

As Iran says no MOU yet Israel don’t believe Trump’s version either.

So crude is pricing “deal soon.”

Metals are pricing “prove it.”

Literally.

Peace trade with zero trust behind it.

EU TTF staying mostly flat says it all.

Do you see crude going lower as US “shadow Hormuz transit” appears to be working?

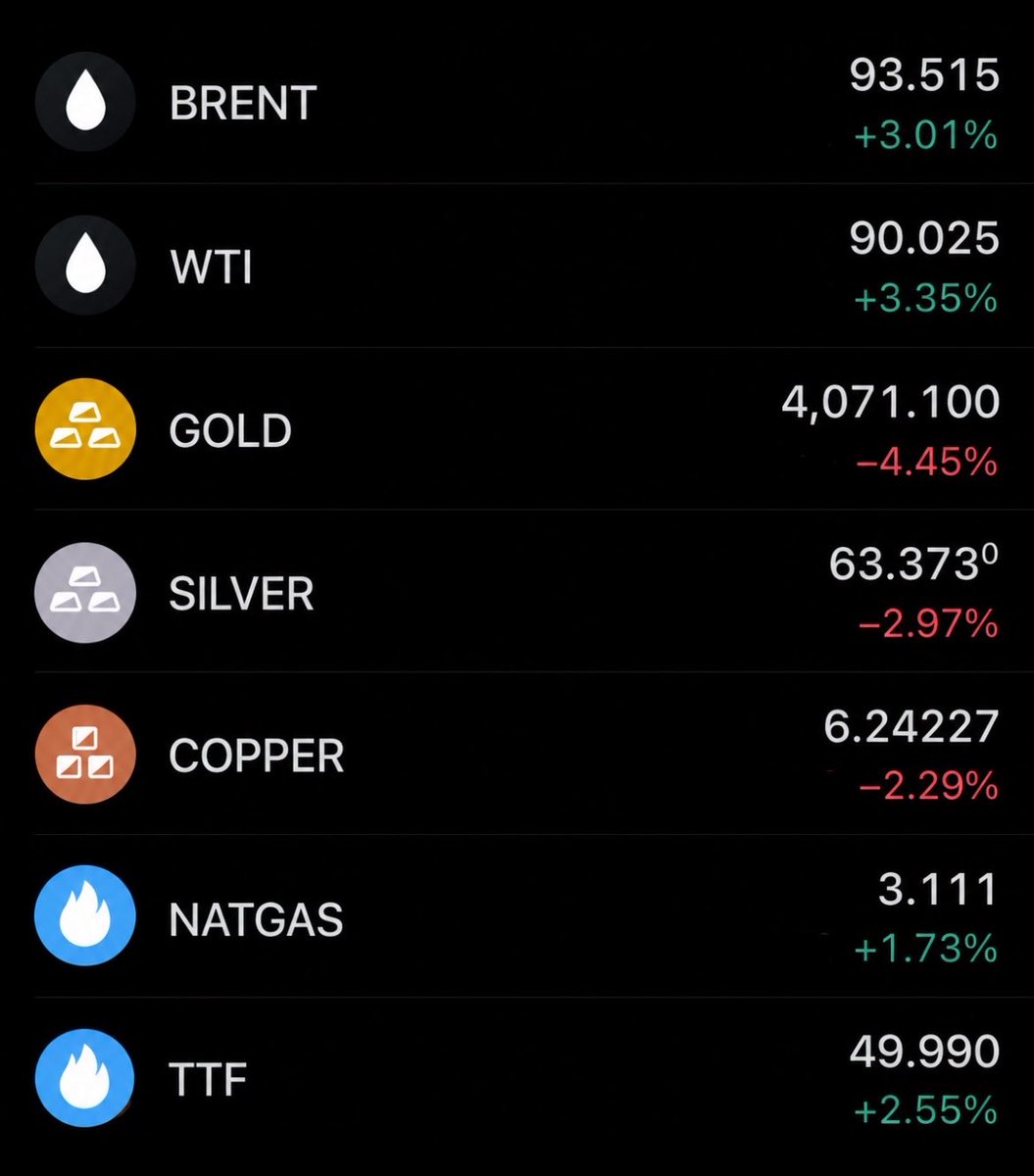

Commodities fragment on hot inflation & Situation Room “retaliation” meeting.

• Brent $93.52 3.01%, WTI $90.03 3.35%

• Gold $4,071 -4.45%, Silver $63.37 -2.97%

• Copper ~$13.76K/t -2.29%

• NatGas $3.11 1.73%, TTF €50 2.55%

• EIA: Oil -7.2M, Gas 0.2M, Dist -0.2M

Next:

• EIA Jun 17

• IEA OMR Jun 17

Energy took back control.

Crude ripped because the market got a bullish inventory draw while the geopolitical tape moved from “deal soon” to active strike cycle.

EIA crude draw was still heavy at -7.2M, even if slightly smaller than last week’s -8M.

But gasoline is the important shift.

Last week had a huge 3.4M build.

Now only 0.2M.

Distillates flipped from 1.5M build to -0.2M draw.

So the product side stopped looking loose right when Gulf/Red Sea risk returned.

That matters because global inflation already bites.

Metals dumping on CPI release show its real impact, as 3y high inflation boosted 2026 rate hike odds.

The odds of entering bearish cycle are skyrocketing as PMs hit below 200MAs in addition to recently triggered Hindenburg Omen (stock market crash) indicator.

Avoid leverage at any cost right now.

Does this look like energy is about to restart the inflation rally?

4

1

20

1,384

Macro prints hot PPI & weak jobs.

• US: PPI 1.1% vs 0.7%, 6.5% YoY vs 6.4% (Core 0.4% vs 0.5%, 4.9% YoY vs 5.4%); Jobless 229K vs 220K

• ECB: held 2.25-2.40%; Lending 25bp

• CA BP -7.6% vs -3.7%

• DE C/A €13.8B vs €24.5B

• JP BSI -1.8 vs 4.2; SK Unemp 2.8%

Next:

• UMich, CA WS, UK GDP/Trade, HK PPI Jun 12

• JP/HK/UK IP, DE/FR/ES CPI, CN Loans Jun 12

US PPI came hot on headline MoM/YoY.

6.5% inflation ain’t a “cooling” story.

Core looked better than expected, but still sits at 4.9% YoY, which is not exactly dovish fuel either.

Then jobs added another problem.

Initial claims and continuing claims both missed, meaning the labor side is getting softer while price pressure is still sticky.

Yes… Ugly mix. Tho not full stagflation.

Meanwhile, Europe’s ECB held rates as expected and presser highlighted widening oil crisis.

And what do we have so far?

- Inflation pressure is still alive.

- Growth confidence is leaking.

- Central banks are stuck waiting.

And all of this is happening while the geopolitical tape is pure rollercoaster.

Trump is talking Iran deal-signing again, but Hormuz is declared shut, the blockade remains active, and Israel does not fully trust the White House version.

Anyway.

Iran has not yet agreed to any deal, despite Trump claims.

So we are literally trading macro inside a headline minefield.

Will bearish hot CPI/PPI effect kick in even harder if most recent “settled” deal breaks down once again?

Macro inflation refuses clean relief.

• US CPI: 0.5%, 4.2% YoY inline (Core 0.2% vs 0.3%, 2.9% YoY inline); Budget -$293B vs -$282.9B

• BoC held 2.25%

• 10Y: US 4.54% vs 4.47%; DE 3.06% vs 3.16%

• PPI (YoY): JP 6.3% vs 5.6%, CN 3.9% inline; CN CPI 1.2% vs 1.3%

Next:

• US PPI/Jobs, CA BP, ECB Rate Jun 11

• JP BSI Mfg, DE C/A, SK Unemp Jun 11

Inflation gave markets a red light.

US headline CPI came in exactly as expected, but core MoM cooled more than expected.

Though keep in mind current CPI 4.2% is a multi-year high.

On top of that…

Japan PPI came in hot on both MoM/YoY.

China was mixed: monthly CPI beat, yearly CPI missed slightly, while PPI stayed inline, yet still highly elevated.

BoC staying at 2.25% keeps the “wait-and-see” central bank theme alive.

US budget miss and higher US 10Y auction yield mean that markets are already trying to digest an escalation as US strikes hit Iran and Iran hit back toward Bahrain Houthis joined.

While hot Inflation forces broader panic.

Considering rumors about renewed full-scale combat operations in Middle East, do you see CPI cross 5% YoY soon?

2

19

833

Stocks rip on US strike-cancel/deal-signing bid.

• S&P 500 1.75%, Nasdaq 4.15%, Dow 2.30% — on oil >5% dump vs hotter PPI/Jobs

• STOXX 50 3.13% — on Trump’s “great settlement” vs ECB hold & DE C/A miss

• Nikkei 5.9%, Hang Seng 1.4% — on deal hopes vs JP BSI miss

Next:

• UMich, UK GDP/Trade, CA WS, HK PPI Jun 12

• JP/HK/UK IP, DE/FR/ES CPI, CN Loans Jun 12

This was a headline squeeze.

Macro was too bearish for this kind of move.

US PPI came in hot: 1.1% MoM vs 0.7%, 6.5% YoY vs 6.4%.

Jobs also softened, with claims missing.

Normally that combo is ugly:

- Higher inflation pressure.

- Weaker labor tape.

- Less room for clean Fed relief.

But markets ignored it because geopolitics flipped the trade.

- Trump cancelled Iran strikes.

- Then pushed “deal signing date soon.”

- Then oil dumped hard.

So equities treated it like the worst-case Middle East tail risk got delayed.

Not solved.

Delayed.

The heat map says everything.

$MU 12%, $AMAT 11%.

Basically a forced re-risking into the same AI/semis basket everyone was dumping earlier.

Though…

Oracle still crashed -8.5%, while Microsoft and Meta remained red.

So this is more like a violent semis relief bid after war/AI-risk got pushed back.

Market choosing to believe deal first and inflation/jobs/Hormuz later is a dangerous setup.

Just a single Iran denial of current terms or delay can change the whole trade in seconds as we approach “July Oil Red Zone.”

Do you trust this rally or is it a trap?

Stocks tank on 3y high US CPI and intensified US-Iran strikes.

• S&P 500 -1.62%, Nasdaq -1.83%, Dow -1.59% — on Budget miss, higher 10Y & hot inflation

• STOXX 50 -1.66% — on EU-CN sanctions

• Nikkei -1.36%, Hang Seng -0.69% — on hot JP PPI, Asia tensions & CN CPI miss

Next:

• US PPI/Jobs, CA BP, ECB Rate Jun 11

• JP BSI Mfg, DE C/A, SK Unemp Jun 11

CPI didn’t calm anything.

Yes, headline CPI came inline.

Yet inline at 4.2% YoY is still a multi-year high. That’s way above last month’s 3.8%.

Basically sticky inflation getting correctly estimated.

Core MoM cooling to 0.2% helped a little, but the heat map shows investors did not buy the relief as “deal in 3d” plan completely shattered.

The most vulnerable is again tech.

Absolute RED wall.

$NVDA & $ORCL roughly -3%

$AMD -5%, while $QCOM -7%

Mega-caps did not save the tape either.

Only Apple held green.

Meanwhile, energy defended hard.

The macro side is already uncomfortable: hotter Japan PPI, higher US 10Y auction yield & hot CPI bigger budget deficit.

Then geopolitics made it worse.

Seems like retaliation “defense” strikes slowly turn into total war restart.

Trump just recently said “it is enough” and new missiles got launched.

Sticky inflation war premium tech weakness all at once.

Deadly mixture…

Will PPI tomorrow confirm the inflation scare?

7

34

2,615

Geopolitics whipsaws as deal-signing talk returns, while Trump cancels Iran strikes & Hormuz shuts.

• Trump: cancelled Thursday strikes after warning US would hit Iran “VERY HARD TONIGHT.”

• US-Iran deal: Trump says "we just made a great settlement" with Iran after noting that the time and place of an Iran deal signing will be “announced shortly.”

• Pakistan channel: Iranian Foreign Minister Araghchi may travel to Pakistan next Saturday as another regional diplomatic track opens.

• Fars optimism: IRGC-linked Fars says chances of Iran approving a US deal are "relatively high" after Washington accepted Tehran's proposed text.

• Qatar mediation: key gaps in Iran-US talks were reportedly resolved during negotiations with Qatari mediators.

• Iran MOU denial: Iran says it has not yet agreed to any MOU document with the US.

• Israeli skepticism: Israeli officials were stunned by Trump cancelling Iran strikes, with one saying they need to hear what Iran actually announces.

• Deal trust gap: Israeli side no longer fully trusts Trump’s version of events, making the “deal soon” narrative shakier.

• Deal claim: Trump said “final points” of a transaction were conceptually approved by all parties.

• Naval blockade holds: Trump says the US naval blockade of Iranian ports in the Gulf of Oman stays in “full force and effect” until a deal is signed.

• Hormuz shutdown: Iran announced total closure of the Strait of Hormuz to commercial ships and oil tankers, warning vessels may be fired on.

• Gulf base attacks: IRGC launched overnight missile/drone barrages targeting US airbases across Kuwait, Jordan and Bahrain.

• Kuwait airspace: Kuwait temporarily shut its airspace after overnight Iranian missile-defense scrambles, then reopened.

• Ukraine deep strike: Kyiv used FP-5 Flamingo cruise missiles to hit the VNIIR-Progress military plant in Cheboksary, over 900km inside Russia.

• Abramovich UA-RU backchannel: Zelensky confirmed Roman Abramovich quietly carried a message from Putin to Kyiv on a possible negotiation framework.

• Rosneft hub hit: Ukrainian drone swarms struck Samara’s Kuibyshev refinery, forcing it offline after fire damage.

• Tyre escalation: IDF expanded operations into Tyre’s historic Christian Quarter.

• Tyre exodus: at least eight more civilians were killed as the city was described as nearly empty, with civilians fleeing inland.

• Japan-China crisis: Beijing issued sharp warnings after Japan said a Taiwan attack could trigger collective self-defense.

• EEZ collision: Japan and the Philippines opened maritime boundary talks east of Taiwan, with China warning against “illegal actions.”

• Taiwan HIMARS trigger: China expanded warship/aircraft presence near Taipei after Taiwan’s US-supplied HIMARS live-fire drills.

• Russia encirclement: Chinese vessels operating around the First Island Chain are reportedly coordinating maneuvers with Russian forces near Japan.

• US weapon delay: European generals warn the US is delaying foreign military sales to Europe while prioritizing its own stockpiles and Middle East ops.

• NATO 2029 clock: Germany’s army chief warned NATO now sees Russia capable of direct invasion by 2029.

• NATO 5% target: Mark Rutte is pushing the 5% GDP defense benchmark, while Meloni says Italy will raise defense spending to 2.8%.

• Huawei ultimatum: US told NATO allies to remove Huawei from critical communications networks to preserve intelligence access.

• Market whiplash: stocks rebounded and oil dropped after Trump cancelled the planned evening missile strikes.

What a rollercoaster.

Trump cancelled strikes and now says the deal signing details are coming “shortly.”

So far signals are positive, but the whole “deal soon” bid can break again fast, if Iran delays, shifts or eventually denies terms.

Diplomacy is alive.

But trust is not.

Does this look like a real deal forming or just another pause amid SpaceX IPO before re-escalation?

Geopolitics breaks from “deal soon” into strike cycle as US-Iran escalation hits Bahrain and Tyre burns.

• Trump reversal: Trump said Iran has “taken too long” to negotiate and will now “pay the price.”

• US strikes Iran: US retaliation strikes hit Iranian launch/radar facilities after the Apache incident near Hormuz.

• Strike map: US “self-defense” strikes hit Qeshm Island, Sirik, Jask and Bandar Abbas between 22:00 GMT Tue and 01:00 GMT Wed.

• Apache update: US intel now points to an Iranian drone bringing down the AH-64 Apache, while Tehran denies responsibility.

• Sea-drone rescue: the two US pilots were pulled from the sea near Oman by a US military sea drone.

• Iran retaliation: Iranian forces launched missiles after the US strikes, with a major explosion reported in Manama, Bahrain, near US base targets.

• Qatar backchannel: a Qatari delegation is in Tehran trying emergency talks despite Trump’s renewed strike language.

• Cyber front: CISA and Five Eyes allies warned state-backed hackers breached critical infrastructure networks across Western countries during the Middle East escalation.

• Red Sea front: Houthis launched drone and ballistic missile attacks on Bab al-Mandab shipping lanes, reopening the southern maritime chokepoint.

• Tyre bombardment: Israel launched a major wave of airstrikes on Tyre after evacuation orders, with residents fleeing the historic coastal city.

• Christian Quarter plea: Tyre’s ancient Christian Quarter leaders appealed for international intervention after the evacuation order reached previously spared areas.

• Israel deep-strike threat: Israeli military leadership said Israel is preparing an independent deep strike inside Iran if the chaos spirals.

• Ukraine hits back: Kyiv launched long-range strikes deep inside Russia after the Kharkiv/Chuhuiv attacks, targeting military and energy infrastructure.

• Air defense influx: Ukraine says it secured new air-defense systems and ammunition commitments from European allies.

• Zelensky envoys: Zelensky’s praised US talks were with Steve Witkoff and Jared Kushner, not generic envoys.

• Putin snub: Putin rejected Zelensky’s open proposal for a direct meeting, saying he sees “no point” in meeting him.

• Kremlin silence: Peskov says US envoys have not yet informed Moscow what frameworks or concessions were discussed with Kyiv.

• China shield: Beijing deployed HQ-16F missile defenses opposite Taiwan Strait, signaling mainland blowback fears from any Taiwan clash.

• Taiwan drones: AIDC announced a GPS-independent drone navigation system built to survive electronic warfare and signal jamming.

• Japan-Philippines front: Tokyo and Manila launched EEZ talks, while Japan moves retired Abukuma-class destroyers and radar systems toward Manila.

• Island chain pincer: Chinese carrier operations expanded east past the First Island Chain, tightening pressure around Taiwan and Okinawa.

• NATO burden shift: Washington told Europe and Canada to boost independent NATO air/naval forces as the US prepares to shift resources elsewhere.

• EU defense clause: EU leaders finalized a framework to operationalize Article 42.7 for collective response if a member state is attacked.

• EU-China sanctions: Brussels’ 20th Russia sanctions round targets mainland Chinese firms accused of enabling Moscow.

• Transshipment dragnet: Western sanctions target RU-linked microelectronics/propulsion flows through Turkey, Kazakhstan and UAE.

• Market fallout: S&P 500 and Nasdaq sold off intraday as the Trump-Iran deal narrative collapsed and Bahrain strike headlines hit.

• Risk rotation: capital rotated from tech/equities toward safe havens like gold and crude as wider Middle East war risk returned.

East Asia is hardening around Taiwan.

Europe is preparing for less US cover.

The sanctions dragnet is now hitting China-linked Russia supply routes.

And cyber risk is now sitting on top of physical war risk.

Does this still look like diplomacy?

5

2

30

3,669

Crypto sinks on Trump’s “Iran will pay the price” & CPI-led rate hikes odds spike.

• $BTC $61.23K -0.75%, $ETH $1.61K -2.25%

• Total MCap $2.086T -1.14%

• Futures OI $100.74B -1.94%

• 24h Liqs $394M -14%

• Bitcoin Dominance 58.35%

• Fear & Greed ~9, AltSeason ~47

Next:

• US PPI/Jobs, CA BP, ECB Rate Jun 11

• JP BSI Mfg, DE C/A, SK Unemp Jun 11

Market tried to breathe.

Then macro and geopolitics stepped on its neck again (eg. US-Iran attacks & Japan/US hot inflation prints).

The weird part: liquidations cooled to ~$394M from yesterday’s ~$460M.

So this is not just one massive wipeout candle anymore.

OI dropped again too, meaning leverage is leaving while price still cannot recover.

That is traders getting tired.

Exactly the type of setup where crypto stops trading like “future money” and starts trading like high-beta liquidity trash.

Especially after CISA warned that new cyber front just opened.

Are you ready for another shakeout?

Crypto loses Monday bounce as “deal soon” hint fails to hold renewed strikes risk.

• $BTC $61.72K -2.72%, $ETH $1.64K -4.05%

• Total MCap $2.11T -1.97%

• Futures OI $102.42B -1.84%

• 24h Liqs $460M 78.5%

• Bitcoin Dominance 57.94%

• Fear & Greed ~10, AltSeason ~49

Next:

• US CPI/Budget, US/DE 10Y, BoC Jun 10

• JP PPI/Orders, CN CPI/PPI, IT IP Jun 10

It’s been less than a day since “pause” got announced and Monday bounce is already gone.

Market got trade support today, but crypto ignored the “macro cushion.”

Because the risk stack is not clean.

Trump is signaling Iran to accept 15-year uranium enrichment pause by weekend, but the same tape has an Apache incident near Hormuz and US retaliation strikes.

Basically a headline roulette.

So leverage is getting chopped again.

And the positioning is awkward too: Binance long/short ratios are still elevated while funding is positive.

That means traders are still trying to long the dip while price is bleeding.

Dangerous combo.

Looks like a survival mode.

Hot CPI tomorrow and (becoming a regular thing) collapsing Trump deal might push BTC to test $60K again.

The question is:

Will that level survive another shakeout?

4

26

1,643