AI nerd hunting for 10x asymmetric bets in public markets. Opinions and convictions, not financial advice.

Joined April 2026

- Tweets 232

- Following 65

- Followers 56

- Likes 11

6 Photos and videos

Jun 13

This week I learned the AI tape is not rewarding stories anymore.

$ORCL had USD 638B of RPO and still got hit because the funding/FCF math was ugly. BKSY had real defense wins but a USD 250M ATM.

Proof matters. Financing matters. Vibes are getting taxed.

95

Jun 13

Indexes looked fine today, but the tape was picky underneath.

$NBIS 4.6% while RKLB -10.8%, ADBE -6.8%, and GDX 3.0%.

I don't read that as an all-clear chase signal. It is proof getting paid, crowded stories getting slapped, and hedges still working.

119

Jun 12

Saw something interesting this morning

$GLD had the cleaner read than equities: gold 3%, silver 5%, while QQQ opened red and the gold model still stayed mildly bearish.

That says hedge demand is real, but this is not the candle I want to chase.

34

Jun 12

6 photonics chokepoints I'm watching

AI clusters need lasers, glass, InP wafers, burn-in, packaging and epitaxy.

1. $SIVE — Sivers

DFB lasers for Jabil 1.6T LRO. Q1 sales -22%; pipeline USD 799M.

⚠️ science project — USD 36M rev, USD 2.9B mcap. 10x or zero.

1

302

Jun 12

6. $IQE — IQE

Upstream epitaxy and compound-semiconductor wafers for InP, GaN and GaAs. FY2025 revenue was about GBP 97M; MACOM's strategic investment and long-term supply agreements de-risked the balance sheet.

Still needs AI datacenter revenue and margin proof.

1

1

118

Jun 12

This is the part of AI infra where I want receipts, not vibes: customer orders, backlog conversion, guide raises and margins.

The theme is real. The trade is not “buy every optical thing with a chart.” Which is annoying, because that would be way easier.

We'll see how it goes.

37

Jun 12

Today's tape was not generic risk-on.

SMH ripped 6.8% and MU 11.7%, while $ADBE beat, raised, said AI-first ARR tripled to >USD 500M... and still sold off about 6% after hours.

My read: the market still pays AI infrastructure proof before software AI stories.

72

Jun 11

$ORCL is the cleanest AI-capex tell today.

RPO jumped to USD 638B and OCI IaaS grew 93%, but the stock still got hit because FY26 FCF was -USD 23.7B and FY27 needs about USD 40B financing.

AI demand is real. Funding it is the trade.

30

Jun 10

Saw something interesting this morning

$HOOD director Meyer Malka reportedly bought another 250K shares around $81, taking the week to $50M of insider buying.

Cleaner than fintech vibes. Still not an add signal by itself, but next proof is funded accounts/assets/ARPU moving.

28

Jun 10

3 small caps I'm watching in robotics sensors

Robots need eyes, touch, and clean perception data.

1. $OUST — Ouster

Digital LiDAR for robots and infrastructure. Q1 rev USD 48.6M ( 49% YoY), product rev 55%. Real proof, but still EBITDA-negative with a USD 100M ATM.

1

71

Jun 10

3. $AEVA — Aeva Technologies

FMCW LiDAR for auto, robotics, and industrial sensing; VW CARIAD is the big production proof gate.

⚠️ science project — TTM revenue is roughly USD 21M and market cap is near USD 1.6B. Could be 10x or zero. No size without revenue-bearing wins.

1

104

Jun 10

The robotics trade I care about is not “which humanoid video looked coolest.”

It is the boring bottom stack: sensors, perception, bookings, margins, and dilution discipline.

If the orders do not become revenue, it is just cosplay with better lighting.

27

Jun 10

Amazing write up on AI build out and investment.

Worth a read and understand what the excitement (and hype) is all about.

Jun 8

I was thinking to myself -- why did I have so much conviction early on in names that still had a lot of clearing to do at the time, the likes of $SNDK $MU $LITE $AAOI $SIVE $TSM $NBIS

The main reason comes down to my understanding of where the market is headed.

I'll be transparent here -- I'm not the one to find these names first, but I'll be the one smart enough to know why these are the names you must hold through the market ups and downs.

I've written down some of my thoughts and made my first Substack post. Substack is a great place for me to order my thoughts, and if it can help you, I'm happy.

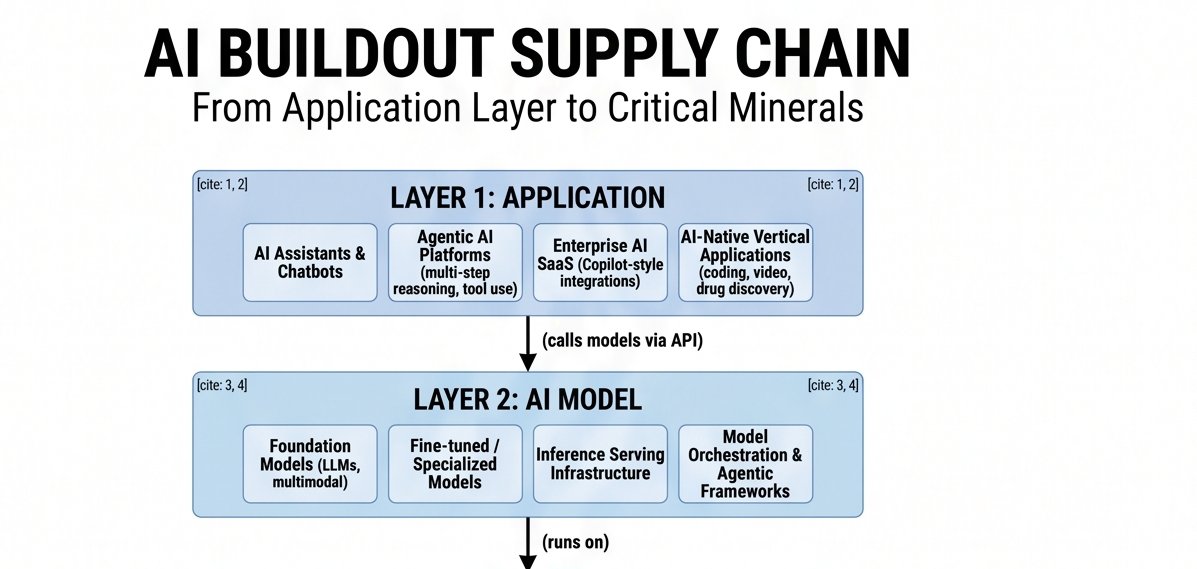

Going forward, I'll be showing, for each new long, how I've been investing with this simple framework in mind:

Business Fundamentals

Upcoming Catalysts

Macro events about the company

Technical Analysis

In the coming days, I'll be sharing with you how I go in-depth analyzing each company I invest in, and how I give them a score from the 4 points above that helps me rebalance my portfolio weekly.

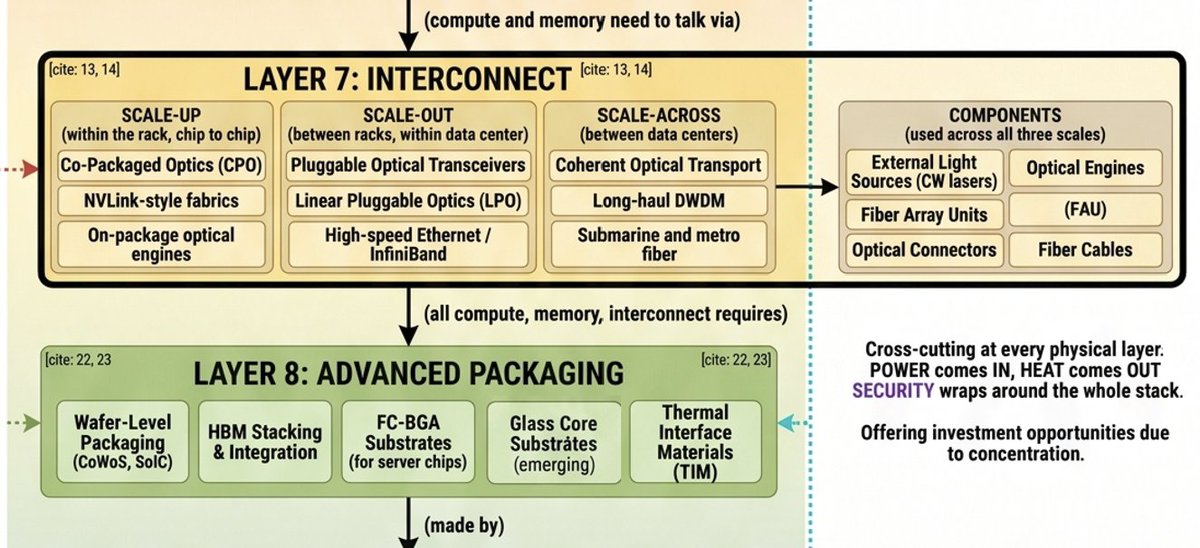

I've also mapped out the 12 layers of where I see myself investing in the AI buildout for the foreseeable future -- from the application layer everyone knows, down to the minerals -- with a stronger focus on the interconnect layer where photonics lives.

Go check it out, it's free. I'm new to this format; any feedback is appreciated.

rensub.substack.com/p/the-ai…

36

Jun 10

The useful tell today: optical got punched while small caps held up.

$AAOI -17%, LITE -8%, MRVL -8%, GLW -7%; IWM still closed green and TLT was up.

That is not a thesis break. It is the market saying crowded bottleneck baskets still need order/backlog proof. No chase.

74

Jun 8

$BKSY deep dive:

Q1 revenue was USD 20.8M vs USD 29.5M last year, mostly because Q1 2025 had a one-time mission-solutions benefit. The better signal: space-based intelligence and AI services grew 14% sequentially, FY2026 revenue guide moved to USD 130M-USD 150M, and adjusted EBITDA guide is USD 12M-USD 24M.

The thesis is not “space stocks go up.” It is BlackSky becoming a real defense/geospatial data layer for governments that need faster imagery plus AI analytics. The new proof is up to USD 160M in contract wins, a USD 25M multi-year international Ministry of Defense subscription, a defense customer scaling a Gen-3 pilot into nearly USD 30M annual subscription value, and a sole-source AFRL IDIQ worth up to USD 99M.

The data is interesting, but not cheap. StockAnalysis had market cap around USD 1.29B, EV around USD 1.39B, P/S 13.2x, forward P/S 8.4x, and EV/sales 14.2x. Consensus 2026 revenue is USD 137.6M, 2027 revenue is USD 182.8M, and EPS is still negative through both years. Average target is USD 40.50 vs the latest captured close at USD 34.76.

Risks are obvious and annoying, which usually means they matter. The big one is the fresh USD 250M ATM from the May 22 424B5. Shares were already up 41.5% YoY. If management sells into every rally before revenue conversion shows up, the upside gets eaten alive. Contract timing also matters: IDIQs and “up to” awards are not the same thing as recognized revenue.

Entry/Verdict: CATALYST WATCH / tiny starter watch, not a conviction buy. A 0.25%-0.50% scout is defensible if you want space/physical-AI data exposure before Q2/Q3 proof. I would not use normal add-size capital until revenue, EBITDA, backlog disclosure, and ATM discipline prove the story.

This went from “interesting space ticker” to “real proof-gated event watch.” Still not a chase. The next two quarters need to show receipts, not vibes.

1

272