Joined September 2024

- Tweets 282

- Following 330

- Followers 188

- Likes 647

21 Photos and videos

Pinned Tweet

Apr 5

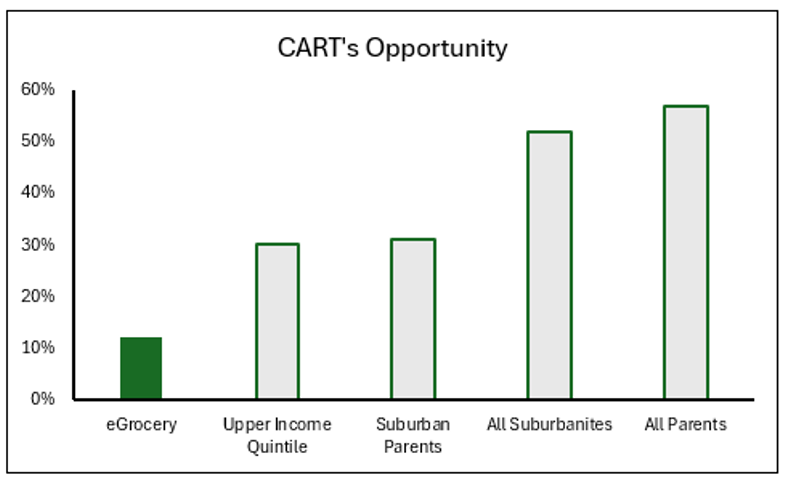

eGrocery is likely winner-takes-most and $CART's large-basket flywheel gives it the right to win. I see a path to ~30% 3yr IRR

New Instacart $CART memo and model up on the Substack: substack.com/home/post/p-193…

1

127

FermatCap retweeted

Jun 14

NEW YORK FOREVER

WE DID THIS TOGETHER

THE CITY'S ALIVE

KNICKS IN FIVE

436

22,615

144,912

1,467,135

Apr 15

1/ This article provides a helpful mental model for thinking about an industry's vulnerability to AI disruption. Key indicators of potential disruption below:

1. Breadth of available data

2. Availability of clearly defined SOPs

3. (Continued below)...

a16z.com/where-enterprises-a…

1

55

Apr 15

2/ ...

3. Discreteness of the outcome set

4. Measurability of ROI

5. Limited regulation (i.e. low cost of failure)

6. Impersonality of the transaction

40

Apr 14

3/

- XB rev 2% QoQ on a seasonally weak 4q (average of -2% in the L3Y)

- Active Customer count continues steady growth ( 4% QoQ, 22% YoY) driven by 26% YoY Biz growth

- Customer Balances maintain HSD QoQ growth, outpacing user growth

1

72

Apr 14

4/

- Excess Interest down, likely due to lower interest rates

- $WISE stopped breaking down rev between Biz & Personal; XB can be backed out, Biz rev was -1% QoQ vs -3% 4q L3Y average); Perhaps mgmt is trying to obfuscate businesses slowdown coming off two LDD QoQ quarters

161

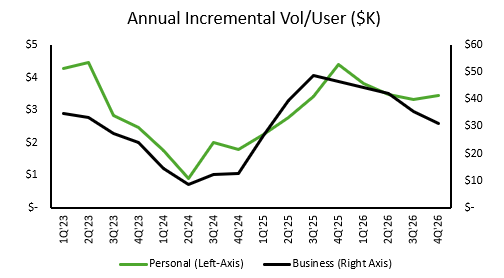

Apr 14

1/ $CART's Instaleap acquisition seems both an int'l CAC lever and a defensive land-grab. There's much tech overlap, but acquiring grocer and user relationships facilitates int'l expansion. eGrocery is a density business, this acquisition provides density while boxing out rivals

1

78

Mar 11

Interesting analysis of how wealth inequality is really power inequality, and is a constant tug of war between politicians and the wealthy

capitalgains.thediff.co/p/me… via @byrnehobart

55

Jan 3

Bezos in '02 (paraphrased): "It's one thing to take data and do backward looking data mining... but this doesn't help with feedback loops. Owning the data allows for experiments with results clear within hours"

Essentially, controlling data expedites learning curve progression

1

45

Jan 3

Bezos labeled this as "a really big point that most people miss." Link below, ~20min mark

youtube.com/watch?v=J2xGBlT0…

60

2 Oct 2025

Improving shortfall rates by shedding problematic clients is a phenomenal example of exploiting survivorship bias; EY should take responsibility for their shortfalls, and seek to improve their practices, rather than ignore complicated situations

wsj.com/articles/inside-eys-…

1

140

28 Sep 2025

1/4: I’ve been studying serial acquirers for a few months and I’m beginning to view hurdle rate discipline as the most crucial (& underappreciated) component of the biz model; acquirers need decentralization and strict subsidiary WACCs incentivize capital to be pushed upwards...

1

1

194

28 Sep 2025

3/4: The most successful serial acquirers don’t seem to be the ones who thrive operationally, but rather those with a genius at the helm, or with programmatic M&A. I suspect this boils down to what is easier to control; ops seem far more difficult to standardize than M&A.

1

115

28 Sep 2025

4/4: Plus, having 100% ownership allows these acquirers to harvest cash, growth be damned. More research & thoughts on acquirers to come in the coming months, I’m beginning to study Transdigm

116

19 Sep 2025

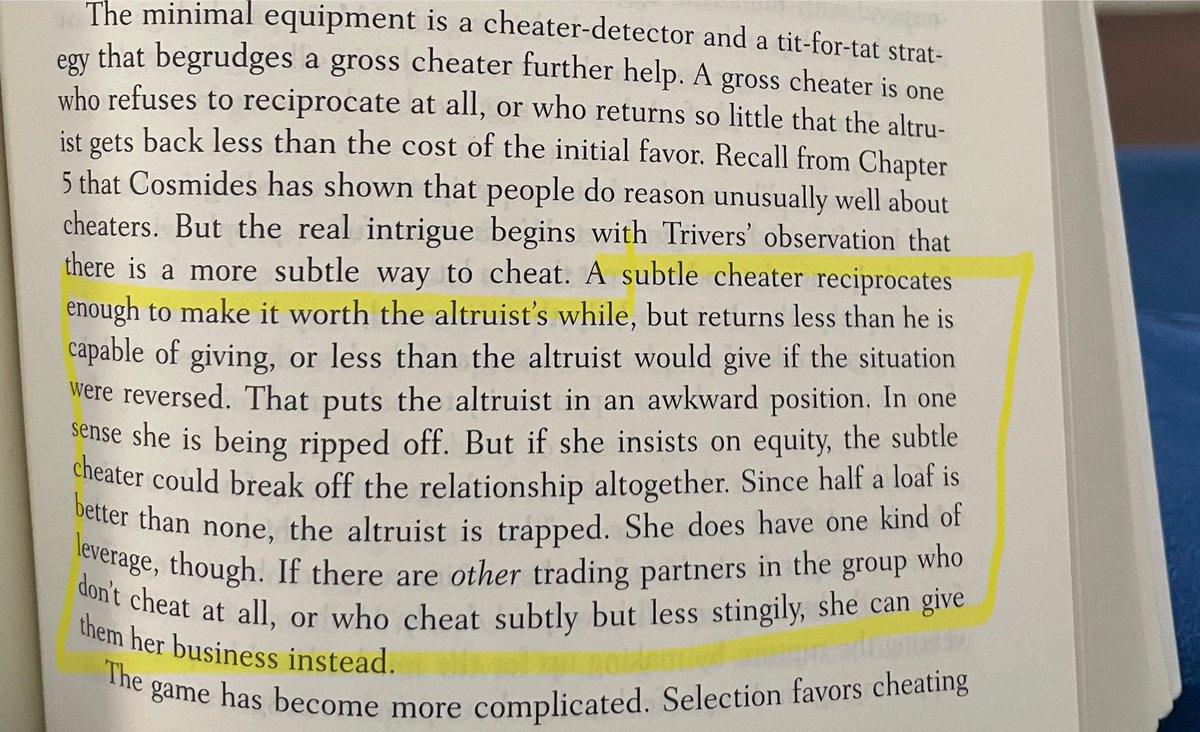

Excerpt I just read from Pinker’s "How the Mind Works" which can be perfectly applied to current trade wars. Tariffs from any party puts the altruist in an awkward position that can only be remedied by friend-shoring

1

116