Master of EBITDA Adjusting ~ Industrials / A&D ~ SaaS / AI ~ LMEs / Rx ~ Unapologetically Catholic ✝️ ~ #GoBruins 🐻💙💛 ~ #BillsMafia ~ ≠ investment advice

Joined July 2019

- Tweets 11,147

- Following 1,383

- Followers 2,166

- Likes 32,867

199 Photos and videos

Pinned Tweet

14 Jul 2025

Officially sold all my $VRT. 730% gain realized in my ROTH IRA. Time to find the next man up! Ideas?

23

89

26,285

Rightsized CapStack Capital retweeted

Irish spent 200 years building their reputation as heavy drinkers that image was obliterated by the Scots in less than 4 days

110

490

11,739

457,369

Scotland fans win best fans of the World Cup this year. Not close.

3

379

Rightsized CapStack Capital retweeted

Jun 16

Just holding the QQQ index over the last 10 years would have generated a 22% IRR

You would have outperformed almost every venture capital and private equity fund that exists simply by owning an index and doing nothing beyond that

It is a fallacy that retail needs access to private markets to generate good returns

The reason you see many people push for this is because they want exit liquidity on their own positions. Nothing more

Jun 16

I think it’s time to revisit the accredited investor laws in the US.

Companies are staying private longer, where only accredited investors (aka rich people!) can invest. Retail investors can only come in after IPO, when much of the upside has already been captured.

These rules were created with the best of intentions, to protect regular people from scams - a noble idea. Unfortunately, in practice they've often made it illegal to get richer, unless you're already rich. A regressive tax!

We have to judge policies based on their outcomes, not on their intentions.

These are two possible routes I see:

1) Replace the rule with something merit-based, like a financial literacy test. Pass it and you're accredited. Having a qualification based on competency rather than your bank balance or income seems far more fair.

2) Remove the rule entirely. Let consenting adults assess their own risk. Disclosure requirements stay and fraud enforcement stays to punish bad actors.

90

115

1,627

207,602

Rightsized CapStack Capital retweeted

Jun 14

*Checks Futures

30

94

1,626

197,296

Tomorrow should be the Mother of Green Candles on the news of the Strait of Hormuz opening.

1

2

420

1

541

Rightsized CapStack Capital retweeted

Jun 12

Alexi Lalas just called James Corden a “fucking wanker” on live TV and the reactions were incredible. Hero moment for him, IMO. #FIFAWorldCup

Did Alexi Lalas just say “wanker” on national TV 😂😂😂

550

1,927

44,598

5,153,011

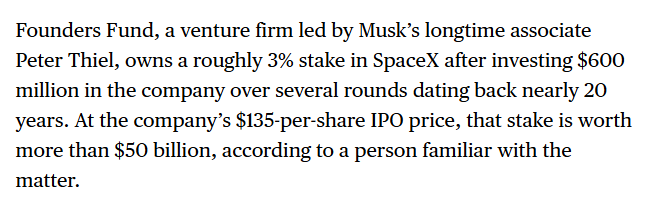

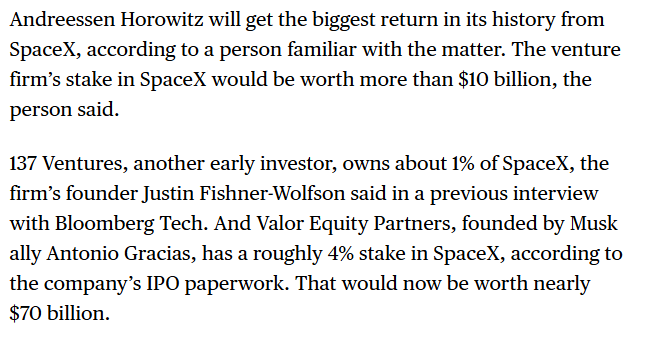

Absolutely sell the $SPCX the second your can. Realize the gains and move on to the next thing.

Jun 11

VCs such as Founders Fund and Andreessen Horowitz are set for record gains following the SpaceX IPO

2

782

$FRD is cookin’ right now!

Jun 11

$FRD Friedman Industries, Incorporated Announces Fourth Quarter and Fiscal Year 2026 Results

stocktitan.net/news/FRD/frie…

3

738

Last night by girl said to me “babe, can we have some Special Sits time and $NNBR & Chill”.

What was I gonna do, say no?

5

5

1,090

Rightsized CapStack Capital retweeted

Jun 10

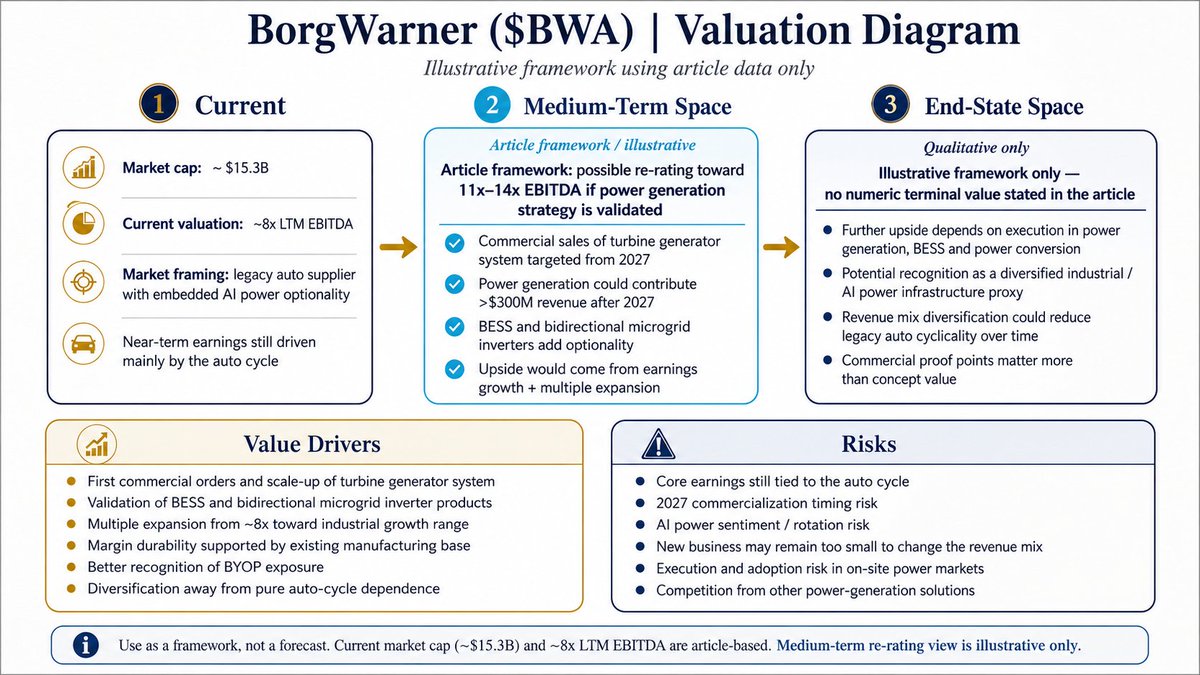

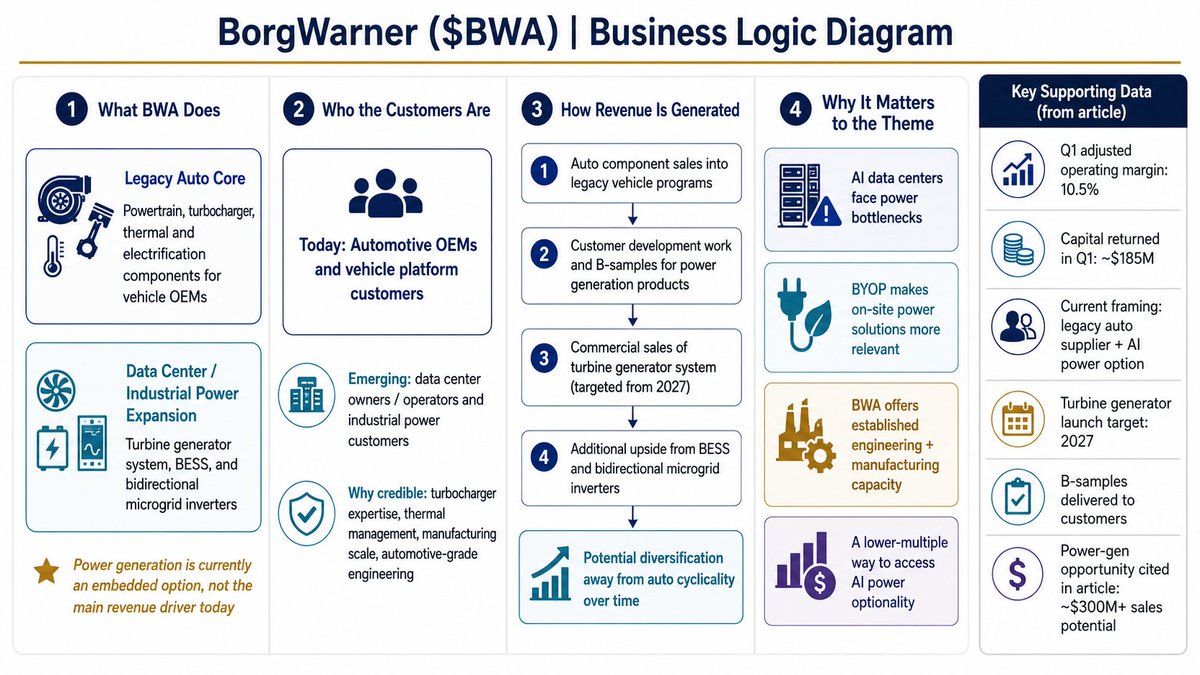

$BWA may be one of the cheaper ways to gain exposure to the AI power theme.

@CapstackCapital notes that while BorgWarner is still primarily an automotive supplier today, its growing portfolio of battery storage, microgrid inverters and turbine-generator systems creates optionality tied to future data center power demand.

3

1

4

1,197

Rightsized CapStack Capital retweeted

Jun 10

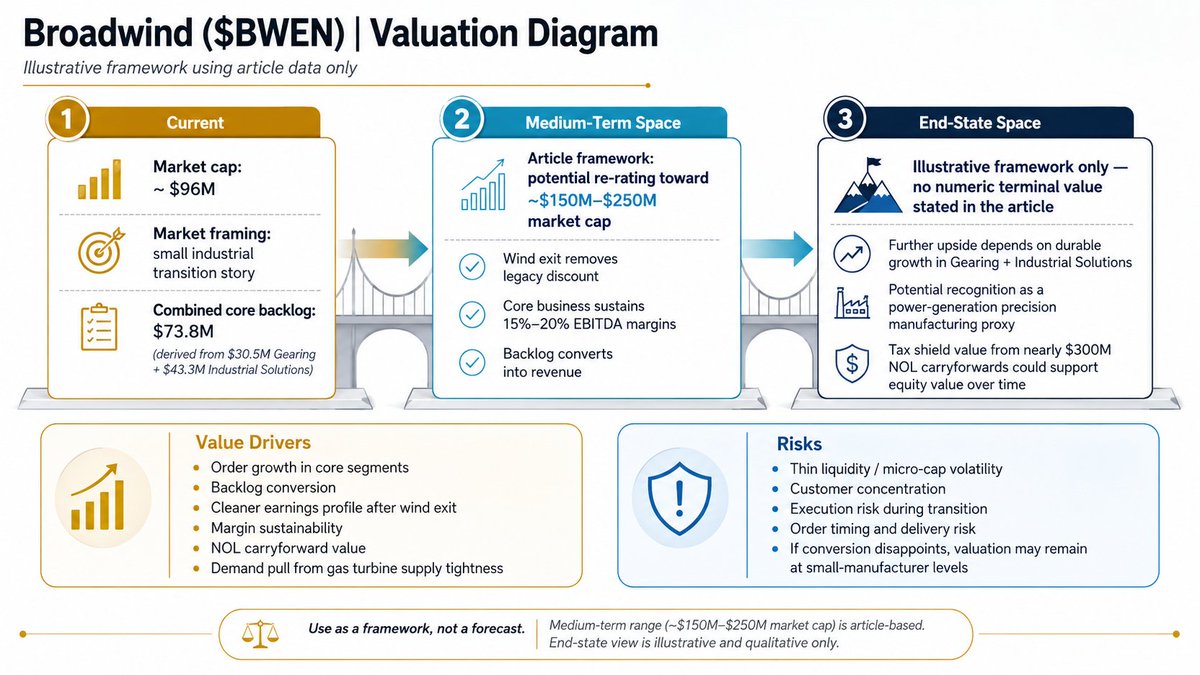

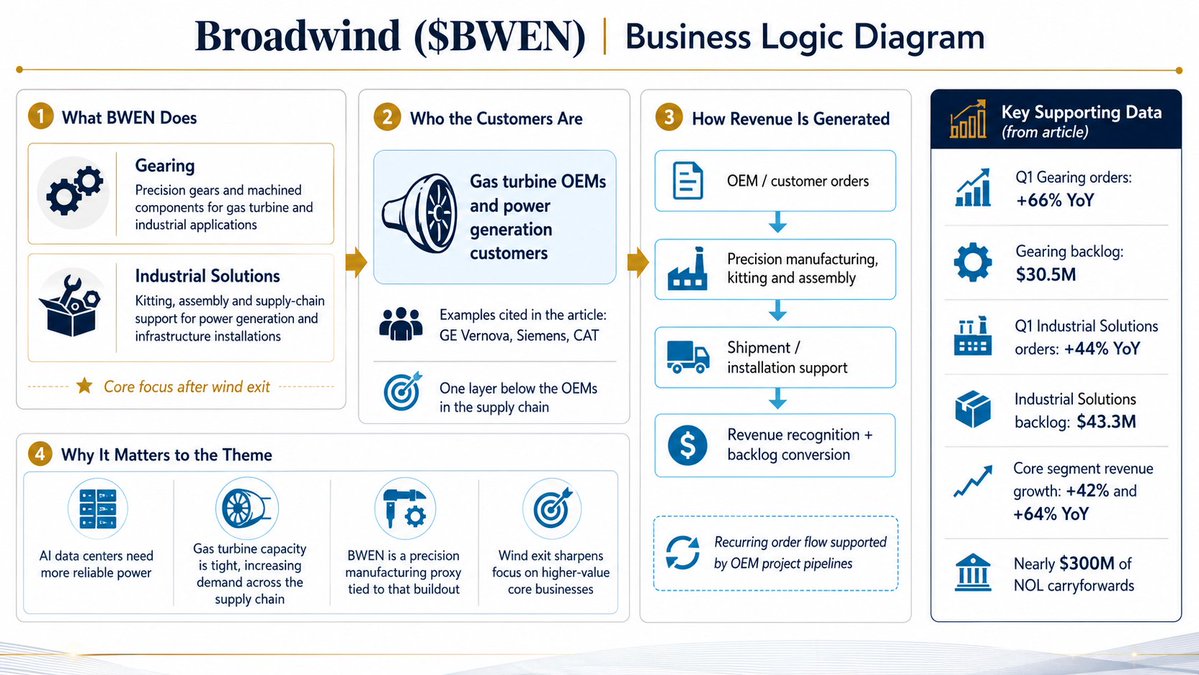

6.10 美股日记 - $BWEN / $BWA : Power Bottlenecks Alpha

一、Broadwind(Ticker: $BWEN )

1、一句话购买理由

BWEN 买的是燃气轮机供给短缺下的一层精密制造代理。

2、核心要点

业务定位:Broadwind 是美国本土精密制造商,核心变成 Gearing 和 Industrial Solutions,服务 power generation、critical infrastructure、mining 等市场。

今日新增:市场开始把它从风电塔筒公司重新看成 GEV、Siemens、CAT 等燃机供应链下游的精密齿轮、kitting 和装配供应商。

订单 / 财报:Q1 Gearing 订单同比增长 66%,backlog 达 3050 万美元;Industrial Solutions 订单同比增长 44%,backlog 达 4330 万美元;两个核心业务 Q1 收入分别同比增长 42% 和 64%。

独特性:公司退出 Abilene 风电塔筒资产,出售价格最高 1950 万美元,同时保留近 3 亿美元 NOL,未来如果核心业务盈利改善,税盾价值很重要。

Why Now:GEV 和 Siemens 燃机排产紧张,AI data center 的 BYOP 需求让“燃机一层供应链”开始被市场挖掘。

3、风险评估

流动性风险:BWEN 仍是约 1 亿美元市值小票,成交稀薄,不能市价追。

转型风险:公司退出风电后变小,2026 guidance 已撤回,Q2 后才有更干净的核心业务视图。

客户风险:增长依赖少数大型 OEM,订单强但客户集中和交付节奏仍需验证。

4、市场观点

@ThematicTrader 提到(x.com/ThematicTrader/status/…),BWEN 是 GEV / Siemens 燃机排产爆满后被忽视的一层供应商,Industrial Solutions 和 Gearing 正在受益于燃机供应链紧张,并特别提示小盘低流动性,必须用限价单。

5、估值模型

按约 9600 万美元市值看,市场仍把 BWEN 当小型工业转型股,而不是 power generation precision manufacturing proxy。若风电噪音退出后,核心业务能保持 15–20% EBITDA margin,并让 backlog 持续转收入,中期市值有机会向 1.5–2.5 亿美元重估;若订单无法放量,估值会回到普通小型制造股。

6、交易思考

只能小仓研究仓,不追高、不市价买。下一步看 Q2 是否给出无风电噪音后的核心收入、margin 和订单转化。

三、BorgWarner(Ticker: $BWA):传统汽车零部件里的 BYOP 期权

1、一句话购买理由

BWA 买的是汽车零部件商切入数据中心自备电的低估值期权。

2、核心要点

业务定位:BorgWarner 本质仍是传统汽车动力总成和电气化零部件公司,数据中心 power generation 目前是新业务期权,不是当前收入主驱动。

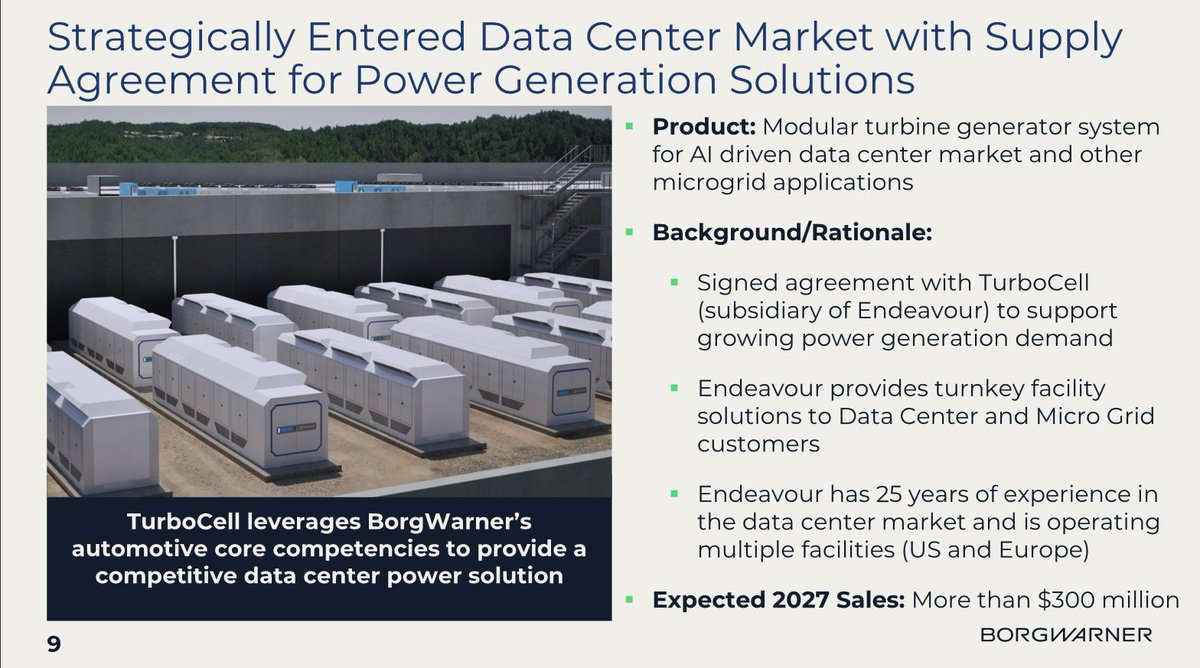

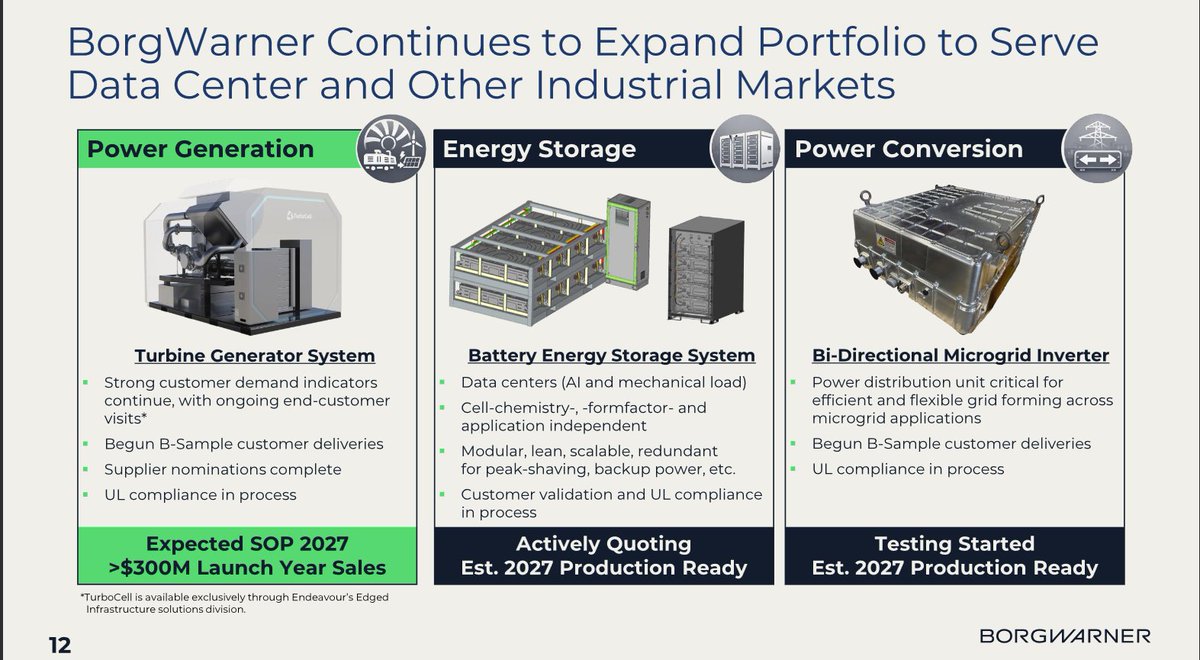

今日新增:公司确认数据中心和工业组合已扩展到 BESS 与双向微电网逆变器,2027 turbine generator system launch 仍在推进,B-samples 已交付客户。

订单 / 财报:Q1 adjusted operating margin 为 10.5%,公司当季回购和分红合计返还股东约 1.85 亿美元,说明它不是 HYLN / FCEL 这类高融资依赖小票。

独特性:BWA 的优势不是概念,而是 turbo、热管理、制造规模和汽车级工程能力,可把燃机发电系统做成可规模化工业产品。

Why Now:数据中心缺电推动 BYOP,Bloom Energy 已被市场重估,资金开始寻找更便宜、更成熟的 power generation 替代表达。

3、风险评估

主业风险:短期业绩仍主要由汽车周期决定,power generation 还不能改变当期收入结构。

兑现风险:turbine generator 预计 2027 才开始销售,2028 后才可能更明显贡献收入。

估值风险:股价已有一年大幅上涨,若 AI power 交易退潮,BWA 也会跟随回撤。

4、市场观点

@CapstackCapital 提到(x.com/CapstackCapital/status…),BWA 正从 legacy auto supplier 切入 data center power generation,预计 2027 年开始销售,power generation / BESS / power conversion 可成为 FY28 之后的增量,同时当前估值仍约 8x LTM EBITDA,市场可能尚未充分计入这部分期权。

5、估值模型

按约 153 亿美元市值看,BWA 不是小票弹性,而是低估值成熟工业股叠加 AI power call option。若 2027 后 power generation 贡献约 3 亿美元以上收入,并带动市场从 8x EBITDA 向 11–14x 工业成长估值重估,中期弹性来自 earnings growth multiple expansion;若新业务延期,则估值仍回归汽车零部件逻辑。

6、交易思考

BWA 可作为低波动 AI power 卫星仓观察,但不追一年大涨后的高位。更好的买点是市场回调或公司披露首批商业订单。

#PowerBottlenecks #Broadwind $BWEN #BorgWarner $BWA

$BWA Capitalizing on Power Generation Bottlenecks / Bring Your Own Power (BYOP) tailwinds.

A pivot from legacy auto supplier to data center power generation.

BWA strategic pivot to power generation via leveraging its expertise with turbos [chargers] is notable & impressive. Its auto exposure remains the primary performance driver as the power generation solutions are not readily available for deployment yet. However, that is expected to change soon, in 2027.

Power remains the ultimate bottleneck to bringing data centers online. And after the massive financial success of $BE fueled by BYOP (Bring Your Own Power) for BTM power generation, or even as N 1 redundancy, investors are looking for other opportunities. People are calling out $HYLN, a peak-SPAC-era de-SPAC that has pivoted its business model more than can be counted. HYLN touts a solution that is agnostic to multiple sources of inputs. Also, FinTwit has hyped $FCEL, a company I have followed on ‘n off for many many years, to which it never really did much. But maybe now it has some opportunities. But now there is a new, and potentially formidable competition entering the game.

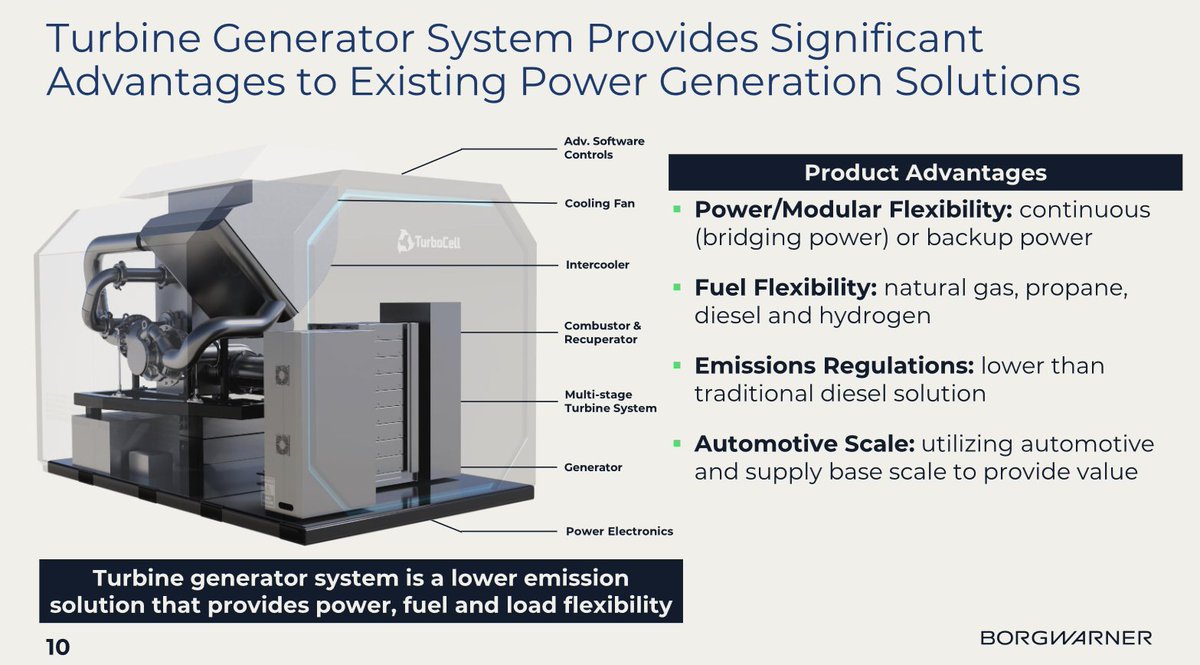

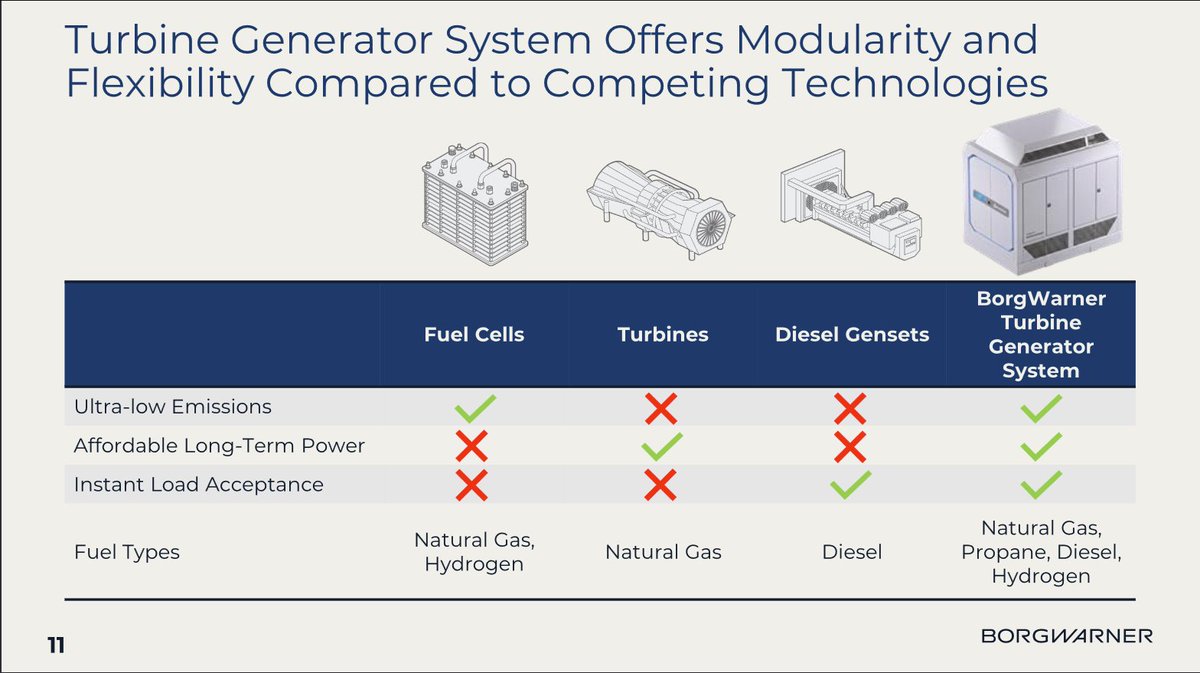

$BWA pivot is notable. Aside from $BE, the others don’t have the engineering expertise/pedigree of BWA, nor the manufacturing capabilities. The Company is offering a turbine generator system that is compatible with Natural Gas, Propane, Diesel, and Hydrogen, providing flexibility to DC owners. Additional data centers opportunities the Company is expanding into is capitalizing on the BESS opportunity and Bi-directional microgrid inverters.

The power generation solutions is expected to begin sales in 2027, forecasting sales of ~$300mm . Due the shortage of turbines with backlogs extending through the end of the decade for $CAT $SIEM.NE etc., alternatives such as $BE have been successful. That coupled with localities increasingly requiring data centers to BYOP and generate fewer emissions, $BWA entering the market to capitalize is brilliant. Its existing manufacturing footprint provides the opportunity to scale the segment pretty meaningfully and possibly faster than some might expect. The power gen solution alone could be a significant driver of growth & profitability in FY28 . It also diversifies the business away from legacy auto-market cyclicality, smoothing out revenue & earnings.

The expansion into BESS and power conversion, which are expected to be production ready in FY27 / contributor in FY28, offers additional revenue upside.

From a valuation perspective, even despite its massive 1yr run-up, BWA is still only trading for ~8x LTM EBITDA, and even cheaper on a forward basis. Most importantly, the market does not appear to be factoring in the revenue uplift from the product expansion efforts. Accounting for the valuation and anticipated growth, the R/R appears to be favorable with valuation probably limiting downside. Downside would probably be driven by a rotation out of AI-related equities to a risk-off mindset or AI market concerns. But at this point you’d be buying a business primarily an auto parts supplier with the aforementioned opportunities as a call option (cheap option with probably a high probability of hitting). It’s also an established business in comparison to $HLYN and $FCEL.

The returns would be fueled via a mix of earnings growth (NI & EBITDA) and multiple expansion via a re-rating as growth accelerates and profitability gains. One could argue BWA being a 11-14x business.

Overall, the market is presenting an opportunity to get power-gen exposure at a reasonable valuation without even treating power gen/BESS/ power conversion as call option. It does not appear to ascribe much value to the opportunity, despite having opportunities in the pipeline. And imo, $BWA execution risk is far less than that of a company like $HYLN or $FCEL as its far better capitalized and larger scale. That is on top of the aforementioned engineering expertise.

3

1

6

1,324

Elite human act right there!

Jun 9

🚨🚨HEARTWARMING🚨🚨

#Pirates phenom pitcher Paul Skenes was driving by a Little League field when he decided to stop and play catch with the kids.

Skenes stayed for over two hours, signing autographs and hanging out with the kids.

A day these kids will never forget.

🥹❤️

483

Rightsized CapStack Capital retweeted

Created another account -- @specsitsdigest -- to focus on special situations. Please give it a follow. Thanks!

2

6

20

5,856

$MRVL Big news for Marvell. Stock is 9% pre-market after the announcement it will be added to the S&P500.

$SPY $VOO

cnbc.com/2026/06/08/marvell-…

2

678

Holy hell it’s a bloodbath in Korea.

Circuit breakers triggered. Samsung & SK Hynix leading the losses.

1

2

722