Price Theory. Co-Chair, Abaxx Markets. Formerly Goldman, currently Director at Aleph, Borr, Energy Aspects, iPulse and Advisor at Carlyle, U Chicago EPIC.

Joined September 2021

- Tweets 97

- Following 155

- Followers 72,026

- Likes 285

18 Photos and videos

Jun 11

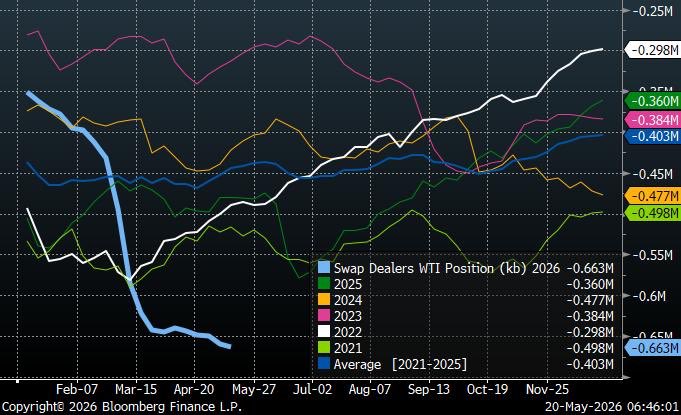

The real reason oil is below $100/bbl. It isn’t fundamentals. It’s capital aversion. Policy uncertainty has made oil too volatile to hold. Investor VaR has collapsed by c.$5B. Open interest is at the lowest level in years. Global oil stocks are still drawing 5-6mb/d; however, investors say they don't care.

Start with investor VaR - the best measure of how much capital is willing to engage with oil. It has collapsed to $1.4B (see chart). Not forced out by rising rates, sanctions or external margin calls. Investors are simply choosing not to hold. The policy noise - deal on/off, attack, not attack - has made the carry uncompensable.

VaR compression has one direct consequence: it drains open interest. Contracts are closed. Market depth disappears. 2026 YTD open interest decline is the worst on record. Unlike 2022, there’s no rates shock or sanctions forcing the exit. This is capital aversion.

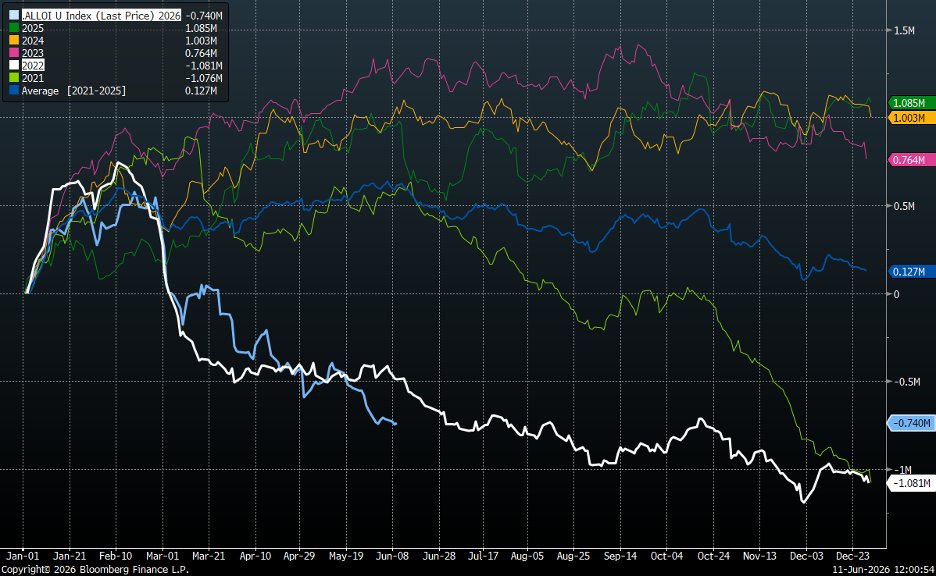

Managed Money VaR and YTD OI Change

132

440

1,883

280,899

Jun 11

The New Joule Order is here, an era in which energy security has become a dominant force shaping investment, geopolitical alliances and commodity prices.

It marks a shift from a world where energy policy was driven by efficiency and cost to one where it is driven by security and resilience.

The thesis rested on a simple observation: the world had underpriced physical energy security for a decade, and the repricing would be non-linear.

The Strait of Hormuz crisis is the first major test of this new era.

My latest piece in the @FT explores the New Joule Order in depth and is available to read below.

Jun 11

The ‘new joule order’ is here. The west is last to realise ft.trib.al/wqV7SSR | opinion

10

55

309

47,856

Jun 11

You can read the original New Joule Order, co-authored by @jamesgutman, below.

carlyle.com/sites/default/fi…

5

9

58

9,399

Jun 10

The abundance illusion.

Carter admitted the scarcity. It was honest. It was politically fatal.

Every Administration since drew the obvious lesson: never admit to scarcity. Talk the price down. Release the reserves. Call it abundance and hope the problem resolves itself. It has worked for the past 50 years.

839 institutional investors. Record two-thirds expect oil prices to fall further. Even retail: oil ETF shorts exceed longs for the first time ever.

The template is working.

It has always worked. Until the buffer runs out.

SPR 415→349mb. Global stocks drawing 6mb/d.

That’s not supply responding to price. That’s inventory responding to price. And inventory, unlike production, has a floor.

You cannot destock your way to energy security.

See my latest note carlyle.com/carlyle-compass/…

57

189

1,162

101,196

Jun 8

Thanks again to @MarioNawfal for having me on his X show yesterday to discuss, amongst other things, the economic impact of the Iran War potentially going hot again, the latest on the Hormuz crisis and what it all means for oil and commodities in the near future.

A great discussion that you can listen to in full below.

Jun 7

INTERVIEW: GULF BOMBED, HORMUZ CLOSED, RED SEA NEXT: OIL'S PERFECT STORM – w/ Economist Jeffrey Curie (@CommodMkt)

18

54

322

81,101

Jun 2

Thank you to @zerohedge for inviting me on to join @AshBennington and @ArjunNMurti for a great discussion on US oil reserves and where we are headed.

Long before Iran, we were already seeing the consequences of years of underinvestment across global energy and commodity supply chains. Spare capacity has become increasingly concentrated, inventories remain tight and physical markets are far less resilient than many assume.

The Iran War didn’t create these conditions, it exposed and accelerated them.

18

63

426

116,045

May 26

Confirming the demand for Abaxx’s financial-physical settled contracts in global gas which we have long argued will likely become the most important marginal molecule in the global energy complex over the next decade. This growth trajectory is set to continue as gas entrenches itself as the swing molecule.

May 25

Today Abaxx traded a record 6,600 LNG contracts :

🔹66 million MMBtu

🔹1.277 Million tonnes

🔹18.9 LNG cargo ships equal to Prism Courage below (350 contracts per ship), in 1 day!!

18

51

409

78,759

Jeffrey Currie 🆔 retweeted

May 25

Distinguished UChicago Prof. John Mearsheimer on Iran’s leverage:

“Time is not on our side. Time is on Iran's side. And if you're playing Iran's side, what you want to do is string this out for a bit longer and bring more pressure to bear on Trump to cut a deal.”

12

52

338

47,522

May 25

Five "deal" announcements, zero closed (yet). That's a trend. Sell the tweet, buy the molecule. Iran's leverage increases with every day that passes and inventories decline, while it decreases for the West.

Thank you to @SquawkCNBC Asia for having me on this morning. Attached is the clip: 50 years of efficiency made oil cheaper per unit of GDP but more irreplaceable in function -- it is the rare earth of the macro system.

cnbc.com/video/2026/05/25/je…

71

245

1,398

387,465

Jeffrey Currie 🆔 retweeted

May 20

Jeff Currie sees gold price pullback before $10,000 run

Gold may see a short-term pullback due to easing geopolitical tensions and slower central bank buying, but veteran strategist Jeffrey Currie says the long-term bullish outlook remains strong.

northernminer.com/news/jeff-…

8

26

163

30,017

May 23

Thanks @tomkeene. So why did Rockefeller stop vertically integrating at the gas pump and never build the car? I knew you would come back on this...

Rockefeller followed one rule: never put a dollar where you're a price-taker. Only own the bottleneck where you set the price. It's the same rule the hyperscalers are breaking.

He stopped integrating beyond the pump, as owning Detroit would have meant pouring capital into a competitive, capital-intensive, price-taking manufacturing business. Gasoline and cars are complements, not substitutes, and you want your complement industry fragmented and competitive. Cheap, abundant cars from Ford and GM meant more fuel sold at higher margin.

The artificial muscle (AM) revolution was ultimately about oil, not the cars planes and trucks that did the heavy lifting. Decades ago, Buffet called them the worst kinds of businesses: ones that grow fast, devour capital and earn little on it. He said if he would have been at Kitty Hawk he would have shot Orville down because "Karl Marx couldn't have done as much damage to capitalists as Orville did." This is exactly the charge now being levelled at the hyperscalers: rapid growth, insatiable demand for capital, and returns that don't clear the cost of it.

But the key here is that Rockefeller wanted the cheap abundant trains, planes and automobiles as he controlled the choke point. The ability to turn crude into gasoline, diesel and aviation fuels.

Similarly, the AI revolution will likely be about atoms, not bits, as that’s where the choke point ultimately is. Chips, turbines, transformers – hence critical minerals. In the new AI race the actual chokepoint has moved off bits entirely, onto atoms: silicon, where Nvidia sets the price, and the commodity complex underneath it: copper, steel, gas, uranium, the metals and molecules.

With the exception Google’s TPU, they own very little of this. Think of Google with its TPU as the Gulf Oil/Mellons that became Chevron.

So who is the Standard Oil of the AI story: Its Nvidia. Both with c.85% market share. I am sure Jensen keeps a copy of Dan Yergin's The Prize for nighttime reading as he has played it to the tee.

But unlike Standard Oil, Nvidia doesn’t control its crude supply. It has TSMC and ASML to contend with. So what does the AM revolution tell you about what could happen to Nvidia, TSMC and ASML in the AI revolution?

‘Why did Rockefeller stop at the gas station and not vertically integrate into cars?’ CURRIE. Read the HedgieMarkets piece; read and re-read Currie.

35

100

757

128,643

May 22

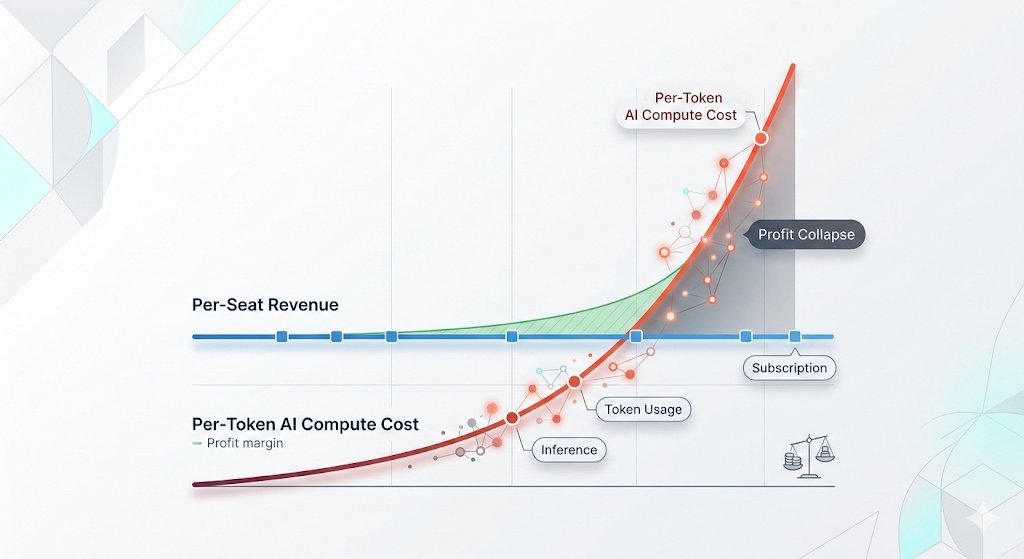

This @HedgieMarkets post illustrates where the infinity scalable asset-light technology model meets the physical realities of an asset-heavy business that faces an upward sloping supply curve.

We have long argued that AI compute is just another bit-atom commodity (like crypto) that uses a lot natural resources to create a valuable (unlike crypto) virtual asset.

On the bit side, Big Tech is a price-maker with fat margins. On the atom side, a price-taker.

Big Tech grew up in bits — search, social, e-commerce, office software: asset-light, infinitely scalable, natural monopolies. Build once, serve billions, watch costs fall every year. So they assume AI is the same game and will spend whatever it takes to own the market.

But inference is also atoms, i.e. land, critical minerals and electrons, which are mostly molecules. In the commodity world, competition drives price to marginal cost: P = MC, which is upward sloping as volume rises. The better the models get, the faster they compete their own margins down to the physical floor which rises with volume.

You can already see it. Microsoft just cancelled Claude Code because the cost to run it exceeded the value it returned — demand retreating the moment price met real cost. The irony: the customer pulling back was itself a hyperscaler. In April, Uber confirmed once again that AI compute demand is price elastic.

Bottom line: they assumed AI costs would keep falling like they always did on the bit side; however, on the atom side, there is a hard floor that likely rises in the short run.

I am not denying that the margins are still fat. But it’s not the same model. These guys are running towards obsolescing their own pricing power. Why did Rockefeller stop at the gas station and not vertically integrate into cars?

May 21

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

40

184

919

240,926

Jeffrey Currie 🆔 retweeted

May 21

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

1,076

4,000

19,921

8,324,361

May 21

You cannot print molecules. You cannot print the rigs $BORR that lift them either.

In a gold rush, the money isn't in the gold. It's in the picks and shovels.

Shale is likely finished as a source of growth. The remaining short-cycle barrels now sit in shallow water — and the Middle East has spent fifteen years drilling its way offshore as its onshore fields deplete. Saudi, the UAE, Qatar: all the growth is offshore now.

That barrel needs one thing above all else: a jack-up fleet. However, there are zero new orders and zero new-yard slots for years. Unsurprisingly the global fleet only shrinks — a third of the rigs on the water are over thirty years old and aging out. At $BORR they average seven. A newbuild theoretically costs $300m, and the dayrates haven’t come close to justifying one — rates must double, and lengthen, before a single rig gets ordered.

Now layer the demand. The buyers are National Oil Companies (NOCs) in countries GDP is heavily exposed to the barrel — the most inelastic clients in any market. The fleet was already above 90% utilized and rising before the war. After the fighting stops: pent-up Gulf tenders, field declines to offset, shut wells to bring back. And the order book already tells you where this goes — energy-security pushing work in Vietnam, Malaysia, Suriname, Gabon.

The security premium is no longer theoretical. It’s in the contracts. Either Hormuz reopens and pent-up demand from Saudi Arabia and the UAE skyrockets, or oil pushes into uncharted territory and the international NOCs pick up the tab.

Few other energy assets are this exposed to both tails. Low-breakeven shallow-water barrels are the supply the world needs to meet the coming crunch. And pick-and-shovel maker gets paid whether or not the miner strikes.

Now the part the market is missing. The whole enterprise trades at roughly forty cents on the cost of replacing its own steel. Enterprise value is about $4bn, split almost evenly — half debt, half equity. The debt is fixed. It does not re-rate. So every dollar the fleet gains as it runs toward newbuild parity falls straight through to the equity.

That is the engine. The debt does not move; the steel does. Re-rate the fleet to what it would cost to rebuild, and the equity does not double — it quadruples. The equity does not track the steel. It multiplies it. The 4x leverage is not the risk in this trade. In the upcycle, the 4x is the trade.

You can buy an irreplaceable strategic asset at less than half its replacement cost — with the leverage thrown in for free. The market is selling the quarter. We're buying the decade.

$BORR is down 14% today on a delayed rig start-up and a one-time receivable provision — operational noise, not structural damage. Utilization held at 97%. Full-year coverage rose to 71%, and the back half of the year jumped from 48% to 65% booked. Nothing in the supply, the demand, or the steel has changed.

The one thing that did move — the Middle East conflict — barely touched the financials and made the multi-year case stronger. Every affected rig is back at work. Tenders keep progressing. Management is more confident on 2027 and 2028, not less.

The market is selling the noise and ignoring the signal. The dislocation is the entry.

Get long. Buckle In. HALO.

57

99

786

134,963

May 19

Everybody talks about the Magnificent 7, but my focus is on the “Munificent 7”. Who are they?

They are oil companies and asset-heavy businesses generating real free cash flow yields in an AI sector that is trying to achieve breakout despite increasing constraints by energy, materials and physical scarcity.

Those oil company yields are 15.5%, whereas the AI hyperscalers are 0%. Read that back again.

The Munificent 7 are named that for a reason.

33

146

1,067

131,344

May 18

You can’t print molecules (or atoms or joules). $Abaxx is a physically settled commodities exchange that will drive true price discovery and the flow of commodities globally.

As the picks and shovels play of the most asymmetric trade in financial history, $ABXX has exponential volume growth and a game-changing technology that can enable tokenization of real world assets.

The Abaxx Exchange has been setting new trading volume records, highlighted by its first 50k contract day. The 50k volume level positions ABAXX as an emerging global benchmark exchange while signalling that operating breakeven economics are within reach.

Additionally, $ABXX will be uplisted to the Toronto Stock Exchange this Thursday, opening up potential index inclusion in the weeks or months ahead driving more liquidity and lower cost of capital.

Volumes were primarily driven by the Singapore #Gold Kilobar (SGK) & our emerging flagship #LNG (GOM, NPA) benchmarks.

CEO Josh Crumb and I will be on an ATB client call this Thursday at 11am ET. Please contact your ATB representative for details.

May 14

Abaxx Exchange single-day trading volume surpasses 50,000 contracts, led by Gold Singapore futures, and surpassing the previous single-day record set on April 9, 2026.

Read Release

abaxx.exchange/newsroom/pres…

16

76

546

122,038

May 18

Thank you to @SquawkBoxEurope for inviting me on this morning to discuss the structural shifts reshaping commodities and energy markets, as well as a deeper dive into AI and the problems we face with the commodities that fuel it.

A lot covered off but a pleasure as always Steve Sedgwick and co: cnb.cx/4fpHZsb

26

130

848

106,395