Quantitative Developer||Derivative pricing & market microstructure||half a decade experience in the financial markets||github.com/ay007008||

Joined August 2022

- Tweets 956

- Following 56

- Followers 107

- Likes 5,710

34 Photos and videos

Pinned Tweet

Apr 24

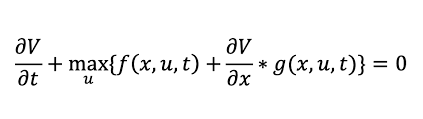

***Options theory

Solid understanding of greeks

***Stochastic calculus

Personal derivation of itô's calculus using Maclaurin

***Market Making Engine

Deployed live on @baysemarkets

Solid understanding of risk mgmt techniques in market making

GitHub projects @ay007008

28 Sep 2025

Linear Algebra✓

Numerical methods✓

Scripting language✓

Version control✓

Python✓

Python DSA (weak)✓

Python data visualization libraries ✓

C software design and Derivative pricing (project going on)

Mathematical finance(can do a lot of derivations)✓

Mql5 language ✓

2

3

660

Jun 13

For the assumption associated with poisson arrivals where crossings are dependent,we know that volatility clusters and we could get moves in one direction and we're working on how gamma capture handles autocorrelation.

1

25

Jun 13

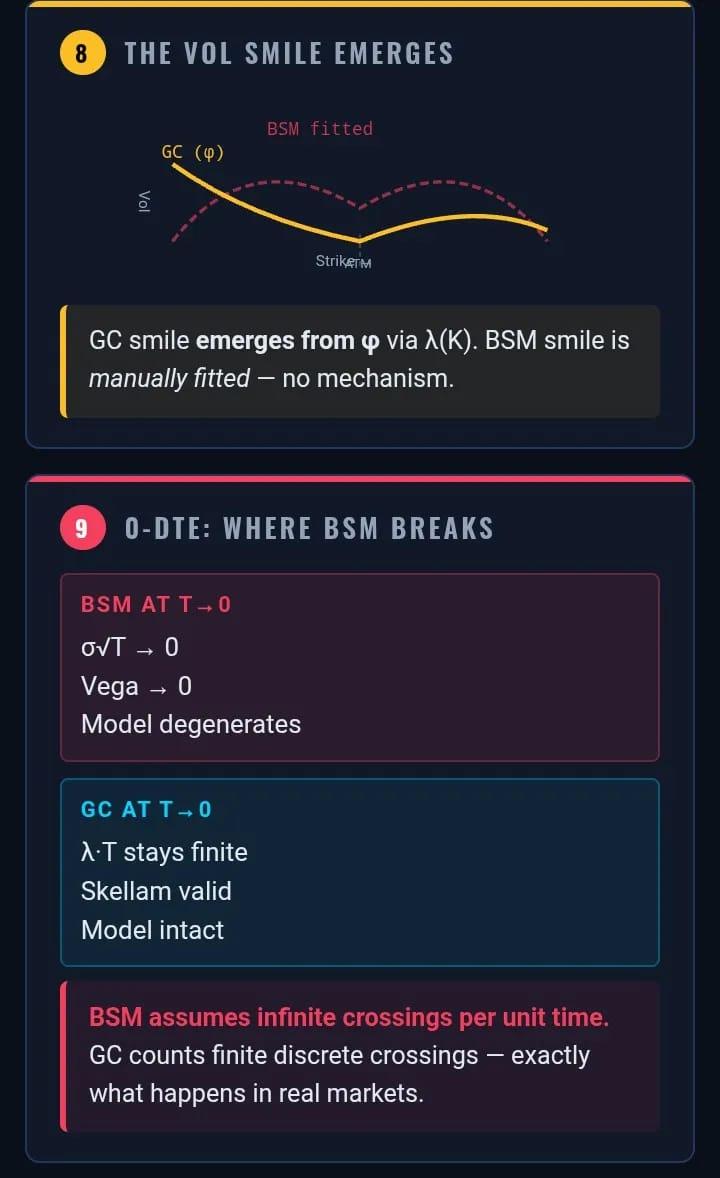

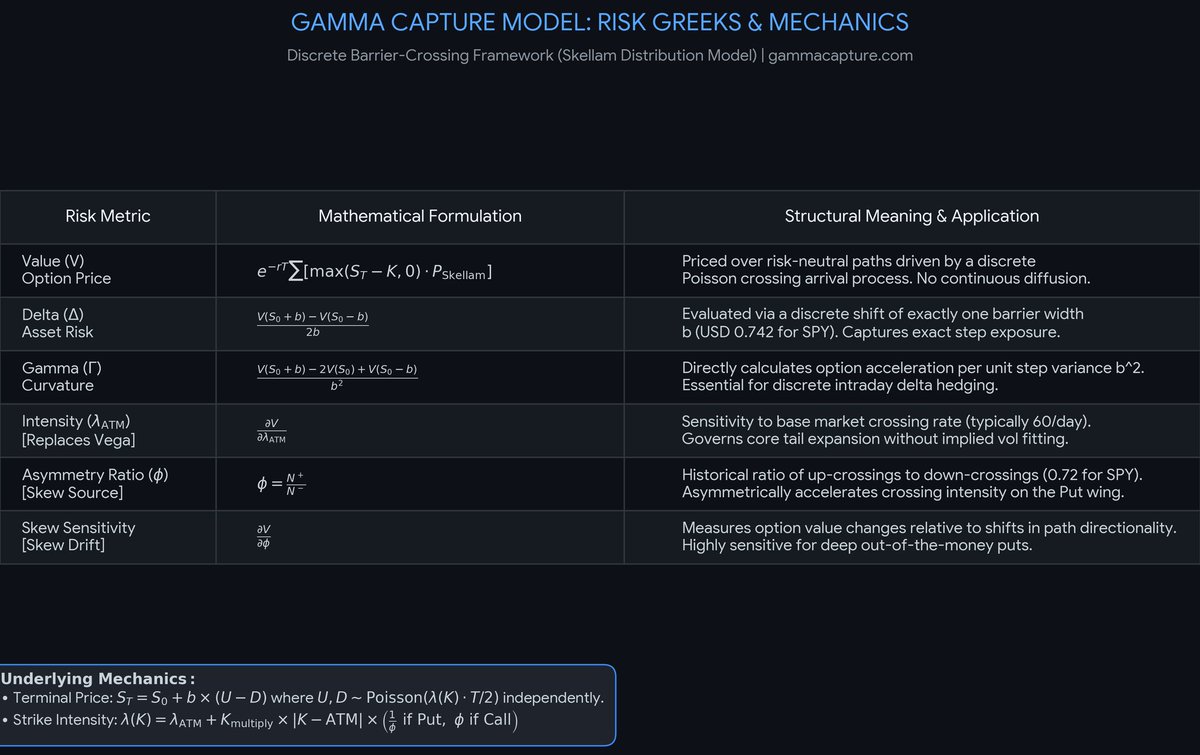

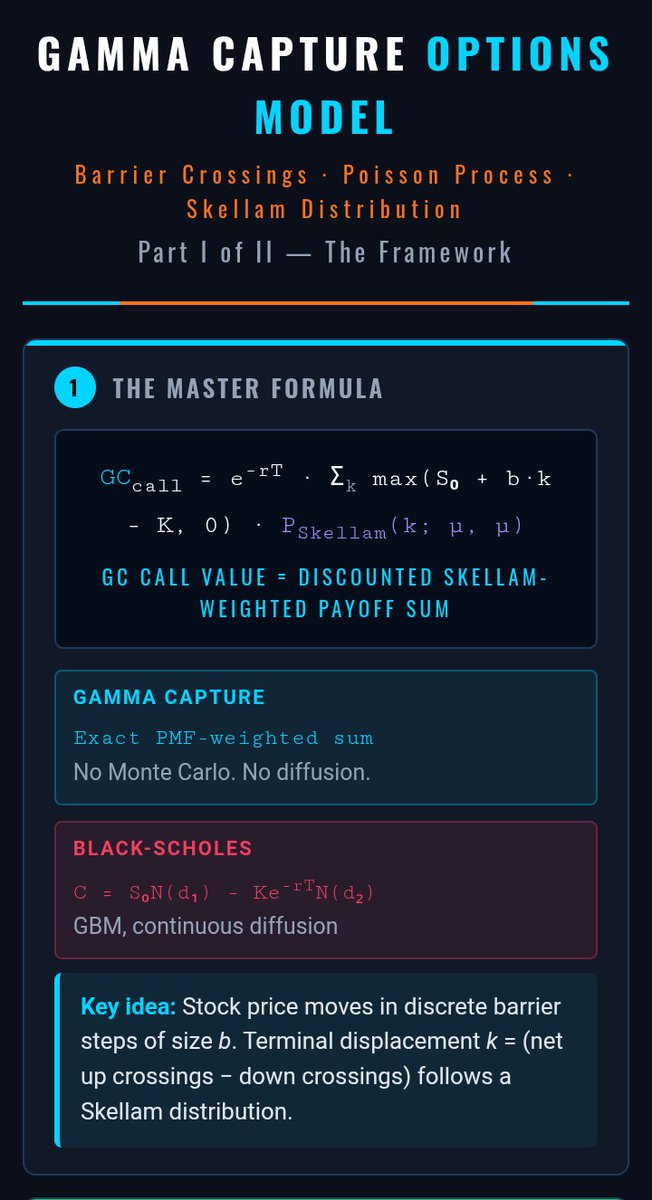

We all know that BSM doesn't produce useful option price at T->0.

A discrete poisson model with observable crossing rates produces real non zero OTM option prices without parameter inflation.

The discrete approximations is closer to market microstructures reality than GBM

Jun 13

SPY price on a 1 min chart is effectively discrete

The barrier width b(t)=$0.76 is larger than the min tick.

Every 0-DTE practitioner knows that the real question isn't whether price is technically continuous,it is if a continuous gaussian assumption produces useful option price

1

30

Jun 13

SPY price on a 1 min chart is effectively discrete

The barrier width b(t)=$0.76 is larger than the min tick.

Every 0-DTE practitioner knows that the real question isn't whether price is technically continuous,it is if a continuous gaussian assumption produces useful option price

Jun 13

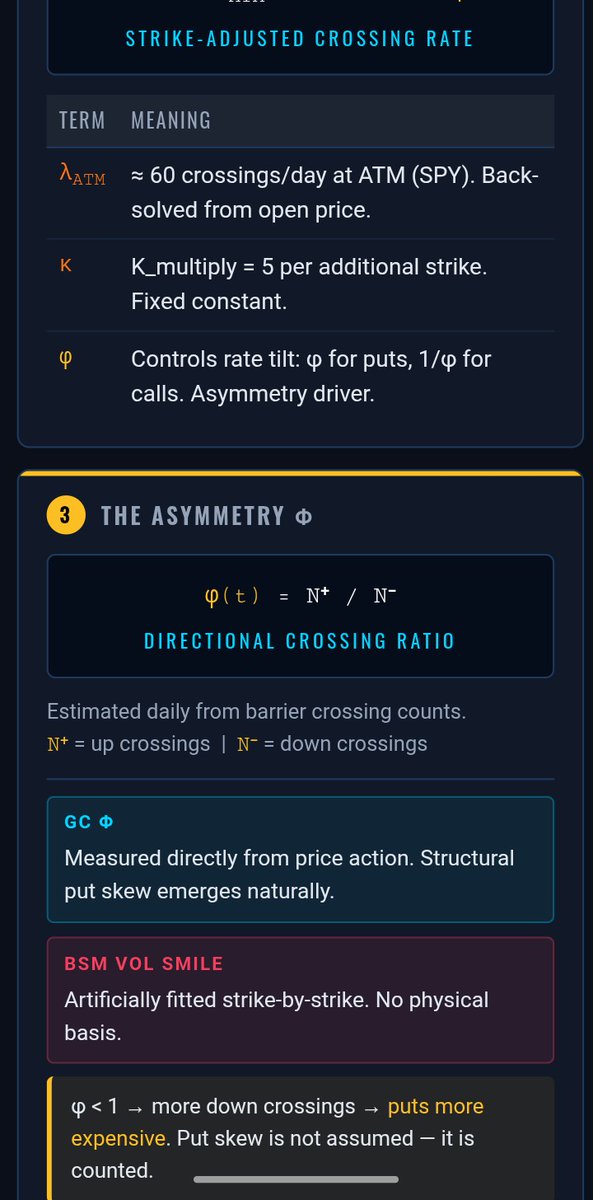

You might be thinking that our terminal distribution is skellam and markets don't close at a discrete integer number of barrier crossings so how are we able to justify a discrete model for continuous price process?

59

Jun 13

You might be thinking that our terminal distribution is skellam and markets don't close at a discrete integer number of barrier crossings so how are we able to justify a discrete model for continuous price process?

51

Jun 13

We've shown it prices in the correct neighborhood on 220 real trading days without any curve fitting whatsoever.

Where BSM requires rebuilding vol surface every morning.

GCM also use observable parameters directly.

Jun 13

You should know BSM wasn't validated for the last 50yrs ,it is been used despite being wrong at 0-DTE.

Practitioners know it is broken,they inflate implied volatility to compensate

As for GCM, I'm claiming it's a better theoretical model for short dated options with real data

1

29

Jun 13

You should know BSM wasn't validated for the last 50yrs ,it is been used despite being wrong at 0-DTE.

Practitioners know it is broken,they inflate implied volatility to compensate

As for GCM, I'm claiming it's a better theoretical model for short dated options with real data

Jun 13

Black-scholes has been stress-tested for 50yrs across billions of trades and we have validation for gamma capture on one year of instruments and you're wondering why it should be trusted?

55

Jun 13

Black-scholes has been stress-tested for 50yrs across billions of trades and we have validation for gamma capture on one year of instruments and you're wondering why it should be trusted?

49

Jun 11

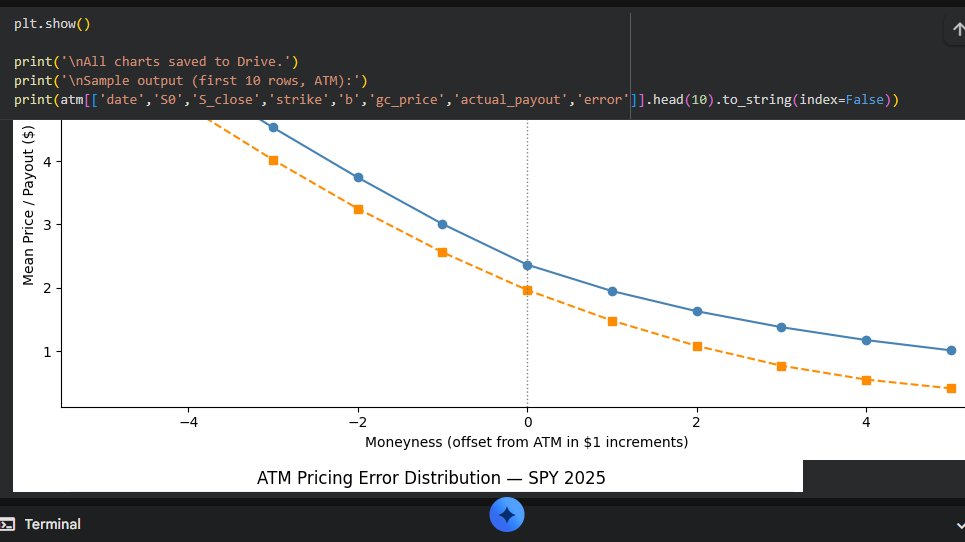

Priced SPY 0-DTE options at 9:30 AM using a Poisson barrier-crossing model

(Gamma Capture) instead of Black-Scholes.

Ran 220 trading days,2,420 strike-day observations.

ATM result:

→ Model price: $2.36

→ Actual terminal payout: $1.96

→ Systematic $0.40 bias across ALL strikes

1

2

59

Ayomide retweeted

Jun 8

Gamma Capture Replaces Black Scholes

1

1

2

226

Jun 8

Don't say I didn't tell you about the gamma capture model

Research reference available on request

May 28

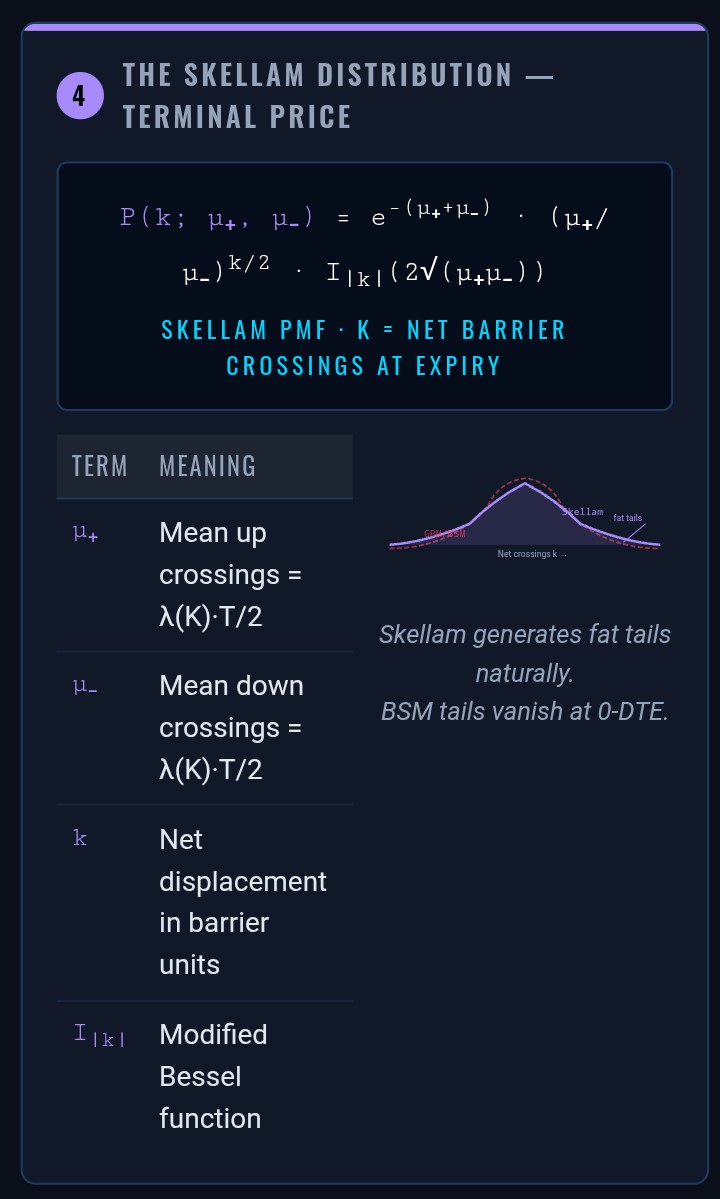

BSM assumes a lognormal terminal distribution.

Gamma Capture derives a Skellam distribution the difference of two independent Poisson variables counting up and down crossings.

Skellam has fatter tails than Gaussian at the same variance.

2

1

3

81

Jun 8

The only flaw found in @I_Am_The_ICT trading models

Speaking of models,gamma capture model is a model you need to look out for

It is the only model that can replace the black scholes

Been having talking to louis pellathy @carbonreports about the validation and it's implementation

Jun 8

Baffled why a trend sometimes breaks structure but never pulls back to an FVG?

In fast moving trends, letting price pull back deep invites more opposing orders, worsening the MM's deficit. The engine performs a micro-pause, layers limit orders at the high, and resumes.

1

2

175

Jun 8

Baffled why a trend sometimes breaks structure but never pulls back to an FVG?

In fast moving trends, letting price pull back deep invites more opposing orders, worsening the MM's deficit. The engine performs a micro-pause, layers limit orders at the high, and resumes.

1

1

212

Jun 8

This forced mechanical buying creates the sharp "spike" past daily highs.

The moment that liquidity pool is exhausted & price ticks down,the dealer's negative delta crashes.

They must instantly UNWIND their hedges by dumping assets,printing the 2nd leg.

This is called gamma flip

1

1

53

Jun 8

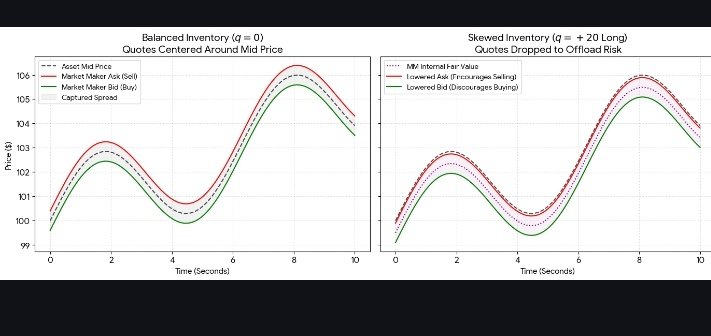

On derivatives desks, the engine shifts to managing options Greeks (Delta & Gamma).

When price approaches a macro high, dealers holding short calls hit severe Short Gamma exposure. To stay Delta-Neutral, their algorithms are forced to aggressively buy the underlying asset.

1

2

37