Joined May 2022

- Tweets 480

- Following 522

- Followers 251

- Likes 1,174

11 Photos and videos

Pinned Tweet

8 May 2022

“All men dream, but not equally. Those who dream by night in the dusty recesses of their minds, wake in the day to find that it was vanity: but the dreamers of the day are dangerous men, for they may act on their dreams with open eyes, to make them possible.” T.E.Lawrence

6

18

139

Cryptic8VC retweeted

Know what you own.

AI demand just started moving in a meaningful way.

Stay patient.

We are still early.

4

5

27

1,303

Jun 8

C8VC Daily Brief: The same week AI signed for 10 gigawatts, a war made energy the scarcest thing on earth. Only one of those got priced.

— OpenAI and Nvidia committed to 10GW and up to $100B in systems. That order doesn't buy intelligence. It buys electrons, land, cooling, and firm power.

— Hormuz has been shut since February. Brent ran 65%. The ECB is hiking and Goldman just pulled every Fed cut left in 2026. The cost of capital on the buildout is going up, not down.

— Friday wiped ~$1T off semis. The AI capex line kept climbing the same week. Capex and equity just decoupled — the market is repricing the cost of money, not the demand for compute.

— Nuclear didn't get a climate bid this cycle. It got a compute bid from a buyer who doesn't care what a kilowatt costs, only that it's firm and it's now.

— Two forces, one input: war bids power higher, AI bids power higher, and neither blinks on price. The model layer compresses toward zero. The megawatt doesn't.

The trade everyone owns is the chip. The one still mispriced is the thing you plug it into.

3

3

103

449,815

Jun 4

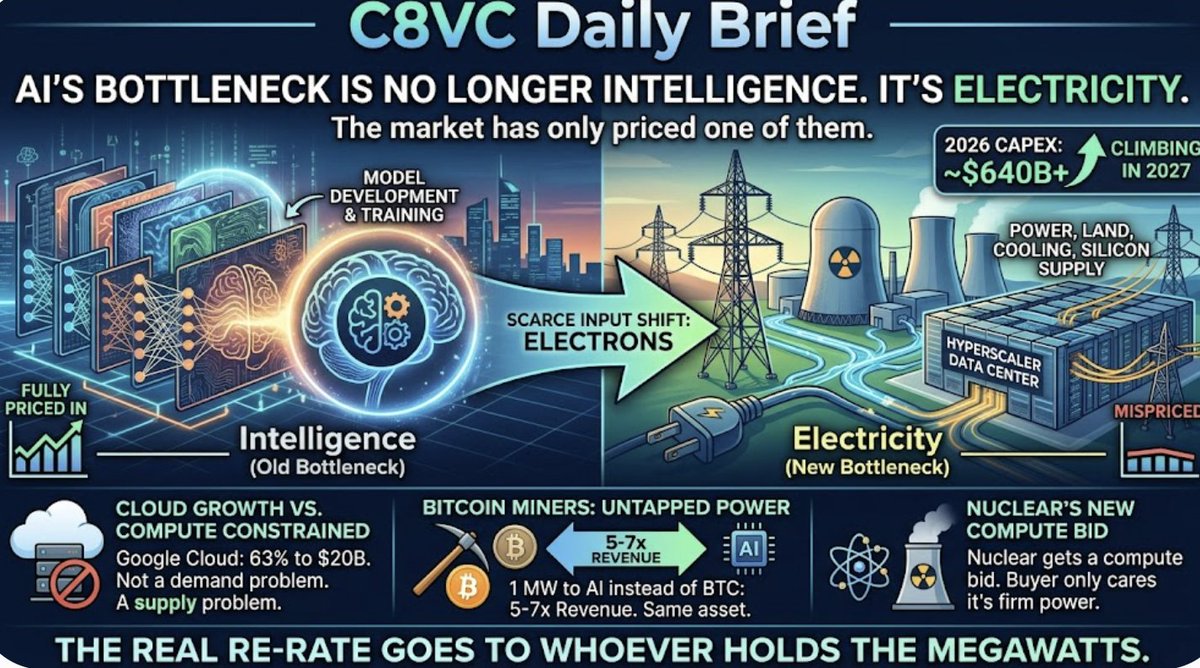

C8VC Daily Brief: AI's bottleneck is no longer intelligence. It's electricity. The market has only priced one of them.

— Google grew Cloud 63% to $20B and called itself "compute constrained." That's not a demand problem. That's a supply one.

— ~$640B of hyperscaler capex in 2026, climbing in 2027. None of it buys a smarter model. It buys power, land, cooling, silicon.

— One megawatt, leased to AI instead of hashing bitcoin: 5–7x the revenue. Same asset. The wrapper was never the value.

— Nuclear didn't get a climate bid this cycle. It got a compute bid from a buyer who doesn't care what a kilowatt costs, only that it's firm.

— Models are software. They compress toward zero. Power is physics. It doesn't.

The AI trade everyone owns is the model. The one still mispriced is the megawatt. When the scarce input is electrons, the re-rate goes to whoever already holds them.

1

5

54

456,453

Cryptic8VC retweeted

$CIFR CEO Tyler Page teases future behind-the-meter on-site generation for Cipher Digital 👀

“Hyperscalers and neoclouds are looking for ways to get power faster. The easiest way in a lot of cases is tapping the pipeline by our property and generating our own electricity.”

16

38

445

103,161

Cryptic8VC retweeted

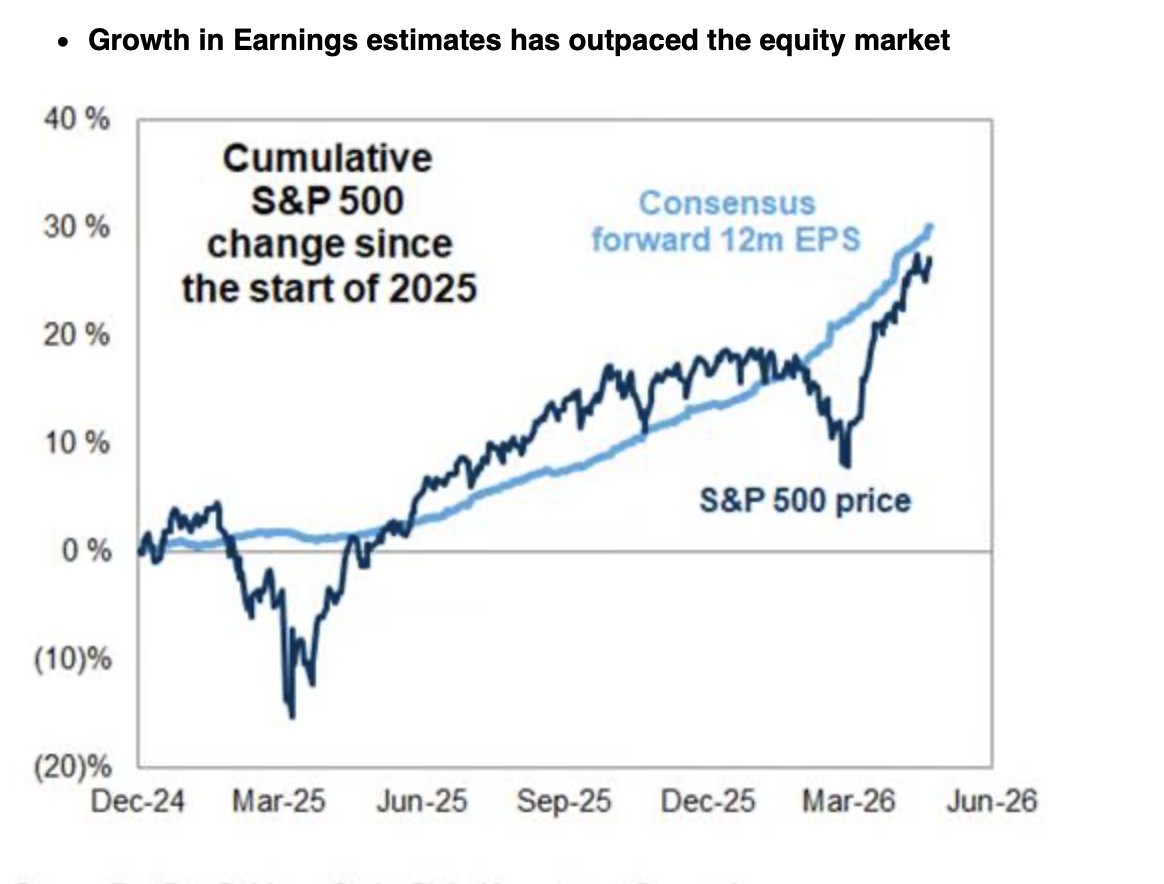

GK Daily Brief: It's The Earnings, Stupid

1

2

9

952

Cryptic8VC retweeted

May 27

I promised once our incubated companies Bitfury USA a.k.a $CIFR and Bitfury Canada a.k.a. $HUT would BOTH become DECACORNS I would make the tweet. WHAT a RIDE! Congrats to outstanding leadership by @rftylerpage and @ashergenoot and their respective teams. Next Stop - HECTACORN 🚀

9

8

128

18,986

May 27

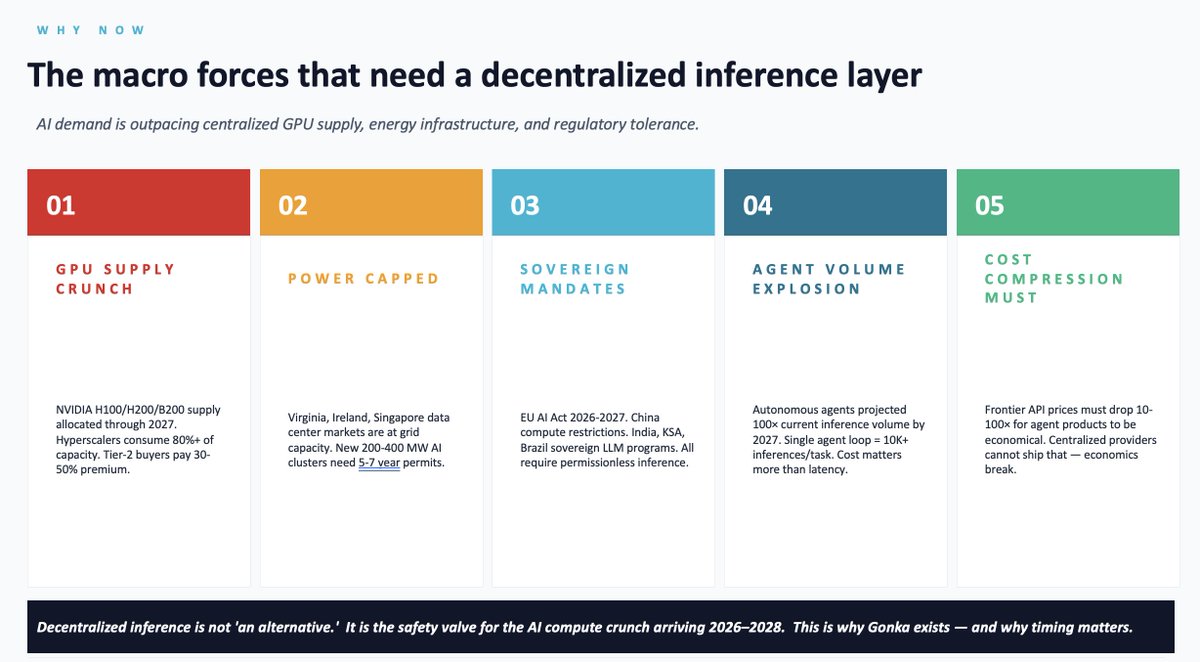

DeCentralised AI @gonka_ai Time Has Come:

1) GPU Supply Crunch

2) Power Supply Crunch

3) Sovereign Mandates

4) Agentic AI Age

5) Massive Cost Advantage

2

6

73

441,825

Here's a quick summary:

Gonka.ai tested 2 frontier AI models (Kimi K2.6 & Qwen3-235B) on their decentralized network.

Kimi correctly knew “гонка” = Russian for “race.” Qwen hallucinated it as a Tamil board game. Neither knew they were running on Gonka.

Results: super low latency (1.26–2.83s), 67–100 tokens/sec, $0.10 per 1M tokens (20–750× cheaper than big-tech APIs), zero failures—even during a mainnet upgrade.

Easy OpenAI SDK integration, no Web3 hassle. Decentralized inference is scaling fast.

1

3

71

May 26

We asked TWO AI models running on @Gonka_ai decentralized network to describe Gonka.

Kimi K2.6 correctly identified the Russian etymology — гонка means "race" — which is genuinely the origin of the network's name.

Qwen3-235B confidently invented "a traditional Indian board game from Tamil regions."

One reasoned. One hallucinated. Neither knew about the decentralized AI network they were running on.

The infrastructure is scaling out faster than big-tech training-data cutoff timelines can index it.

Setting that irony aside — here's what 30 inference calls and $0.015 of automated testing actually revealed:

• Median latency on Qwen3-235B: 1.26s

• Median latency on Kimi K2.6: 2.83s

• Sustained Throughput: 67–100 tokens/sec

• Production Task Failures: 0 of 30

• Cost per 1M output tokens: $0.10 The same Kimi K2.6 model on Moonshot's own native API costs ~$2/M. That's 20× more for identical model outputs.

Versus other May 2026 frontier models:

• Gemini 3 Pro: ~$12/M (120× more)

• Claude Sonnet 4.6: $15/M (150× more)

• GPT-5: ~$40/M (400× more)

• Claude Opus 4.6: $75/M (750× more)

Total cost of the full 30-call benchmark: exactly one and a half cents ($0.015).

All run on the same day Gonka shipped its major v0.2.13 mainnet upgrade activating its live Ethereum cross-chain bridge. Zero dropouts or stalled inferences occurred during the entire core consensus upgrade window.

The developer experience requires zero Web3 friction: call the standard OpenAI SDK, swap your base_url parameter, drop in a network key, and ship. Done in 3 minutes.

The physical compute layer is scaling out globally much faster than the public distribution layer realizes it is operational.

10

6

207

1,311,401

May 26

You can spin up your own testing containers, read the architecture logs, or grab 10M free developer onboarding tokens via the community framework gateway here:

• Access On-Ramp: gate.joingonka.ai

• Consensus Core Engine: github.com/gonka-ai/gonka

2

170

May 22

Cuban Who?. And who cares.

Bitcoin is not for tourists.

1

1

97

136,880

Cryptic8VC retweeted

May 22

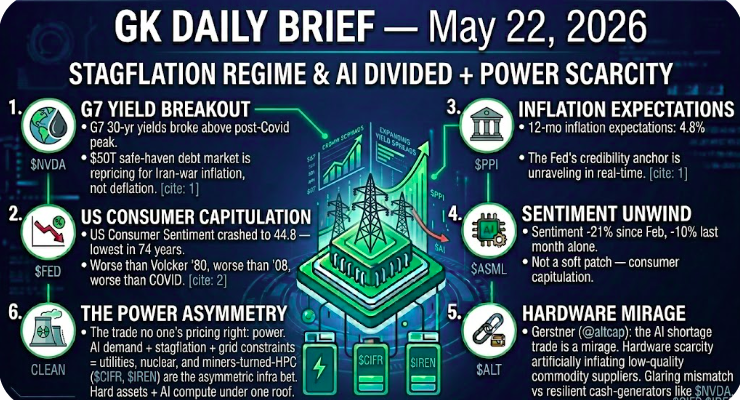

GK DAILY BRIEF - we live in intersting times.

1/ G7 30-yr yields broke above post-Covid peak. The $50T safe-haven debt market is repricing for Iran-war inflation, not deflation.

2/ US Consumer Sentiment crashed to 44.8 — lowest in 74 years. Worse than Volcker '80, worse than '08, worse than COVID.

3/ 12-mo inflation expectations: 4.8%. The Fed's credibility anchor is unraveling in real-time.

4/ Sentiment -21% since Feb, -10% last month alone. Not a soft patch — consumer capitulation.

5/ Gerstner from Altimer: the AI shortage trade is a mirage. Hardware scarcity is artificially inflating low-quality commodity suppliers. Glaring mismatch vs resilient cash-generators like $NVDA. Mandate: own structural winners, not shortage beneficiaries.

6/ The trade no one's pricing right: power. AI demand stagflation grid constraints = utilities, nuclear, and miners-turned-HPC ($CIFR, $IREN) are the asymmetric infra bet. Hard assets AI compute under one roof.

Stagflation regime AI quality divergence power scarcity. Position accordingly.

1

1

5

704

Cryptic8VC retweeted

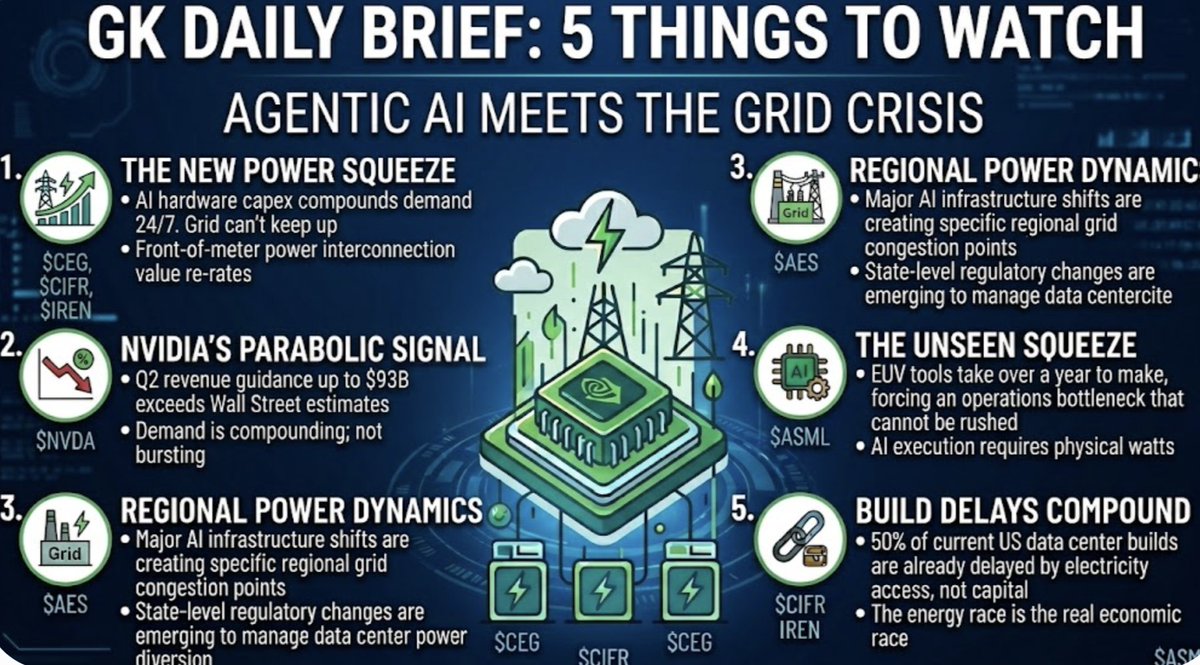

May 21

GK Daily Brief: Agentic AI Has Arrived. The Grid Hasn't.

Last night Jensen Huang said three words that change everything: "Demand has gone parabolic."

Here's what that actually means:

→ Nvidia just did $81.6B in revenue. Data center alone: $75.2B. Up 92% in a year.

→ Q2 guidance: $89–93B. Above every estimate on Wall Street

→ Agentic AI doesn't run in bursts. It runs 24/7. The compute demand curve doesn't flatten — it compounds → Hyperscalers confirmed $725B in AI capex for 2026. Six times 2022 levels !!!

→ ASML builds the machines that make the chips that power all of this. Their EUV tools take over a year to manufacture. You can't rush the choke point.

The market is still debating model benchmarks.

The real question is simpler:

Where does the power come from?

50% of US data center builds are already delayed — not because of capital or demand. Because the grid can't handle them. Transformer lead times: 5 years. Build time for a data center: 18 months.

Agentic AI running 24/7 doesn't just need more chips. It needs more watts. Every hour. Forever.

The chip race gets the headlines. The energy race gets the economics. Energy arbitrage IS the moat.

$NVDA $ASML $CEG $CIFR $IREN

2

2

5

1,228

Cryptic8VC retweeted

May 20

GK Daily Brief: The Summit Happened. And Nothing Was Solved. ⚡

Stabilisation is not resolution. The market keeps confusing the two.

→ Brent pulling back from $120 to ~$109 on summit relief — but without SPR releases, diesel yield switching, and demand destruction all activating simultaneously, OECD diesel hits critical shortage levels by August, gasoline by October. The crude pullback is a relief valve, not a fix. It snaps back the moment any of those solvers disappoint

→ CLARITY Act Senate Banking Committee hearing completed — most serious legislative progress on crypto market structure in 2026. No vote timeline confirmed yet. But committee engagement is real. Watch for Senate floor scheduling. A vote = BTC breaks $82K on regulatory clarity alone

→ Warsh is now Fed Chair as of May 15. No press conference yet. He inherits CPI 3.8%, PPI 6.0%, real wages negative, and zero cuts priced. First Warsh speech or Fed minutes due this week. His view that AI boosts supply-side productivity and preference for trimmed mean PCE — which runs below core — gives him marginally more dovish cover than the headline numbers suggest

→ Pre-summit, the market priced a grand bargain. What it got was stabilisation — trade truce extended, Boeing jets and LNG purchases agreed, Xi told CEOs China will "open wider." No tariff reductions. Taiwan warning rattled markets. Fundamental issues unresolved. The tactical rally in Chinese equities and yuan is exactly what was expected. It doesn't change the structural picture

→ Nvidia earnings Wednesday May 20 — the most important corporate call of 2026. CEO just returned from Beijing without China chip access. Blackwell ramp, US data center demand, and China guidance will drive the print. At $5.4T market cap, every line of guidance moves markets. The China question is now the primary downside risk variable going into the call.

Energy arbitrage IS the moat — and while the summit bought time, the operators with secured power don't need diplomacy to win. The grid constraint compounds regardless of what happens in Beijing.

$NVDA $CEG $CIFR $IREN $PWR $MU $VST $VRT

2

2

6

708

Cryptic8VC retweeted

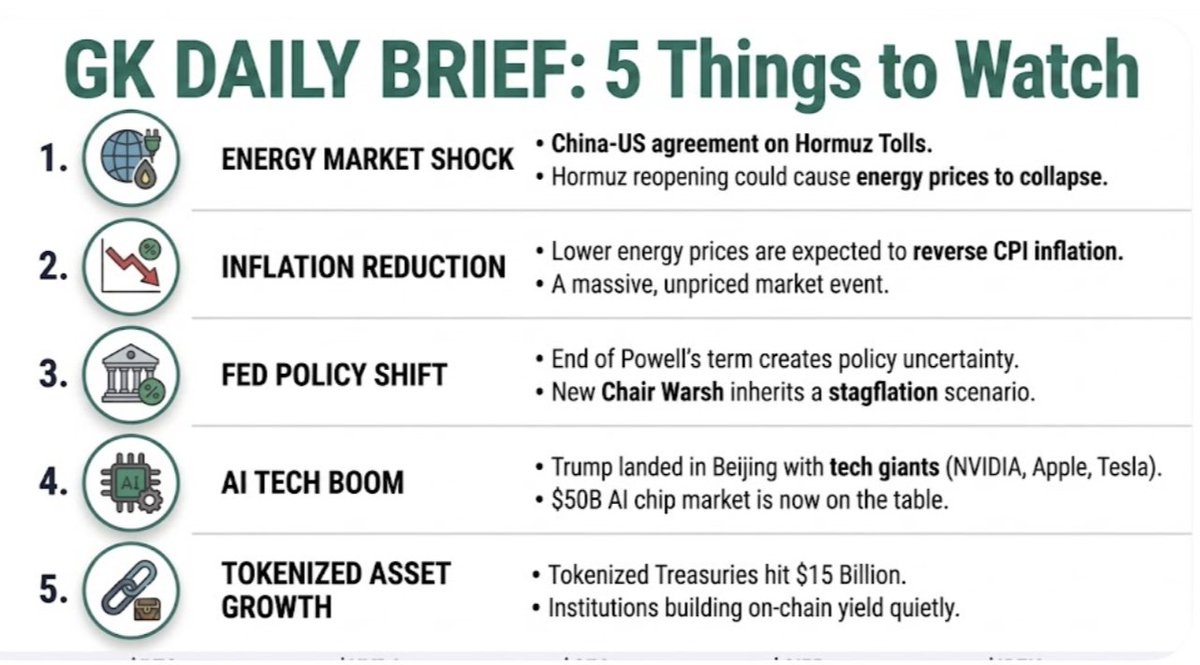

May 13

GK Daily Brief: Stagflation Is Live. Beijing Might Fix Half Of It. ⚡

The Fed is trapped. China might have the exit?

→ PPI 6.0% YoY — nearly triple expectations. Core PPI double estimates. CPI 3.8% yesterday, PPI 6.0% today. Real wages negative. Inflation pass-through is structural. The Fed cannot cut or hike without breaking something. Feels trapped.

→ China agreed to oppose Hormuz tolls — first joint US-China signal on the war. If Hormuz reopens as a Beijing summit outcome, energy prices collapse, CPI reverses, Fed cuts return. Markets haven't priced this yet. Win win.

→ Trump landed in Beijing with Jensen Huang on Air Force One alongside Musk, Cook, Fink. NVDA hit all-time high at $5.5 Trillion. China's $50B AI chip market on the table. Nvidia reports tonight while its CEO negotiates chip access in real time

→ Tokenized Treasuries hit $15 billion — near zero 18 months ago. Institutional capital building on-chain yield quietly while everyone watches the inflation print. Tokenization doesn't need a bull market. It needs rate-bearing assets and blockchain rails

→ Powell's term ends Friday. Warsh inherits 3.8% CPI, 6.0% PPI, a war, and zero cuts priced. His first press conference is the most important Fed moment in years

Question: If China and the US jointly reopen Hormuz, inflation reverses, the Fed cuts, and Warsh turns dovish what does that do to every asset class simultaneously?

2

1

5

782

Cryptic8VC retweeted

May 12

GK Daily Brief: Inflation Is Back. The Market Hasn't Fully Priced It?

Real wages just went negative. The Fed's hands are tied. And the war isn't ending.

→ CPI printed 3.8% — hotter than expected. Surprise. Suprise :) Core 0.4% MoM, highest since January 2025. Gasoline 28.4% YoY. Airline fares 20.7%. Shelter re-accelerating. The worst number: real wages fell 0.5% for the month — negative for the first time since April 2023. Fed rate hike odds now at 30%.

→ BTC holding $80,860 despite the hot print — four rejections at the 200-day MA at $82,228. One clean close above it changes the entire technical picture. Fear & Greed at 47. Retail not in yet. Three catalysts still this week: CLARITY Act hearing Thursday, Trump-Xi summit, PPI tomorrow.

→ Trump rejected Iran's peace proposal as "completely unacceptable" — four demands including war reparations and Hormuz sovereignty. War continues. Energy constraint is now structural into H2 2026. Hot CPI plus Hormuz closed plus real wages negative — this is the feedback loop that breaks consumer spending

→ PPI prints tomorrow. If core PPI accelerates alongside core CPI — tariff pass-through into producer prices is confirmed. The "transient energy" narrative collapses completely and the inflation fight is not over, it's just beginning. Watch bond yields. they ve been getting out of whack.

→ Ray Dalio says BTC is not a safe haven — gold is better. He cites 91% correlation with S&P 500 during Iran escalations. He's right on correlation. He's wrong on the monetary debasement thesis. Watch the next 30 days: if CPI keeps printing hot and BTC holds — that IS the safe haven argument. Very ironic. He probably completely forgot that at higher prices supply of gold will ramp up, with BTC supply is only diminishing. Oh well :)

1

1

3

794

Cryptic8VC retweeted

May 11

GK Daily Brief: The Biggest Capital Mobilisation in History. ⚡

→ 84% of S&P companies beat Q1 EPS — highest since Q2 2021. But half the S&P 500 is now Tech, the highest concentration in history. Earnings are strong. The base is dangerously narrow

→ AI capex in 2027 will exceed the entire US national defense budget. This is not a technology cycle. It's an industrial mobilisation at a scale the market has no historical framework to price

→ Trump-Xi Summit May 14-15 in Beijing — tariffs, rare earths, AI chip controls all on the table. Polymarket at 50/50 on a deal. This is the binary event of Q2. BTC, semis, and energy all reprice on the outcome

→ US CPI Tuesday — Morgan Stanley forecasting 3.8% headline, 2.7% core. Tariffs keeping goods inflation positive. Oil passing through to airfares. Shelter re-accelerating. If it prints hot: Fed hike discussion reopens and the spring stays compressed another month

→ BTC holding above $81K — 67 consecutive days of negative funding rates, longest streak in a decade. Futures traders have been short for two months while spot holds. When this unwinds, it doesn't move slowly

3

3

7

1,637

Cryptic8VC retweeted

Our “AI Bottlenecks” strategy is up 60%.

Most investors are chasing AI. We’re focused on what AI cannot run without. Here’s the framework the 14 stocks behind it:

medium.com/@BitfuryGeorge/st…

9

34

404

1,130,674