Crypto Strategist & Market Analyst | #Bitcoin • #Ethereum • #Solana Early Projects • Alpha Threads Web3 | AI | DeFi | Memecoin | #CryptoMarket #Crypto

Joined August 2011

- Tweets 16,217

- Following 36,274

- Followers 370,562

- Likes 194,519

3,946 Photos and videos

Pinned Tweet

1 Apr 2023

Thank you so much for answering my questions, it was really great to talk to you @elonmusk

Thank you to the @Twitter team for giving me this chance !

I got the promise that we will do the best for #Crypto World 😊

#TheCryptoGems

926

266

978

454,570

Jun 14

🚨 When 4 major asset classes are falling at the same time, this is not a normal market correction.

Crypto is falling.

Gold is falling.

Stocks are falling.

Even bonds and oil are weakening.

Historically, this type of environment usually points to one thing:

The real question investors should be asking today is not:

“Which sectors are declining?”

The real question is:

“Who is liquidating portfolios on a massive scale?”

Because when assets that traditionally have little or no correlation start falling together…

This is no longer an ordinary pullback.

For generations, the rule was simple:

When stocks fell, money flowed into bonds.

When the dollar weakened, gold rallied.

When inflation increased, commodities surged.

Today, however, those traditional macroeconomic relationships are breaking down.

And when there are fewer safe places to hide…

Large institutions and hedge funds often choose a single path:

They sell everything.

At that stage, it no longer matters whether an asset is fundamentally strong or purely speculative.

This is a forced deleveraging event.

There is a name for it:

A desperate race for global liquidity.

When financial panic begins and everyone shifts into defense mode, cash becomes the most valuable asset.

The objective is no longer to generate returns.

The objective becomes preserving capital.

That is why we are witnessing an unusual environment:

Gold is pulling back.

Bitcoin is selling off aggressively.

Stocks are correcting.

Government bonds are losing value.

This is not necessarily because long-term fundamentals have deteriorated.

The primary reason is that institutional players urgently need cash.

The epicenter of this financial tremor may be Japan, but its aftershocks are hitting Latin America particularly hard.

As Japanese interest rates rise, the global carry trade that financed high-yield strategies begins to unwind.

Funds that borrowed cheap yen to exploit stablecoin and currency arbitrage opportunities in Latin America are rapidly closing positions.

Whenever the center of global finance shakes, emerging markets tend to experience the most violent volatility.

At the heart of the problem are highly leveraged portfolios.

When investors build large positions using low-cost global debt and the market suddenly turns against them…

Margin calls begin.

Forced liquidations follow.

To meet collateral requirements, funds must sell whatever they can.

Both losing positions

and profitable assets that remain liquid enough to sell.

This is where an uncontrollable chain reaction begins.

One forced sale triggers another.

The pressure spreads into additional markets.

Market depth evaporates.

Strong hands step aside and wait.

As demand disappears, falling prices intensify the panic.

The current turmoil is also exposing a structural weakness in modern markets.

As assets such as Bitcoin become increasingly institutionalized through ETFs and derivatives, price discovery shifts toward Wall Street.

When large trading desks need immediate protection, they can liquidate these digital instruments within seconds.

And when liquidations are controlled by institutional algorithms, decentralization becomes largely irrelevant in practice.

At the same time, there is a macroeconomic trigger that receives far less attention:

U.S. government debt.

Historically, it has been viewed as the world’s ultimate safe-haven asset.

But when Asian interest rates and currencies experience significant volatility…

Even that safe haven can come under pressure and become part of the broader institutional unwinding process.

As options become increasingly limited, an unusual scenario emerges:

Risk assets decline sharply.

Traditional safe havens weaken as well.

And the average investor is left asking:

“If nothing is holding up, where is the money going?”

The answer is far simpler and far more strategic than many assume.

3

2

2

20,452

Jun 14

The money is not flowing into some mysterious digital asset.

Nor is it rushing into the latest miracle investment.

Institutions are moving into cash.

They are waiting.

From a technical perspective, this behavior is entirely predictable.

Markets constantly change narratives, but human psychology in the face of fear has remained remarkably consistent for centuries.

Price action reveals when the crowd is approaching capitulation.

Those who can read the structure of market sentiment often discover order within the chaos.

Historically, the greatest wealth transfers never occur during periods of extreme optimism.

They usually emerge when panic has paralyzed the majority.

That is when strong hands accumulate cash and begin hunting for opportunities among distressed assets.

This pattern repeats throughout every major period of volatility.

When everything appears to be falling apart, new fortunes often begin to form.

While the majority panic and sell, a small minority steps back and analyzes the broader macroeconomic picture.

2

4

14,394

Jan 26

Hey #TheCryptoGems Community !

$BTC / USDT – Daily Structure Breakdown ⭕️📉

Bitcoin just printed a textbook distribution → breakdown sequence.

Let’s read what the chart is really telling us 👇

1️⃣ Major Top Formation 🏔️

BTC topped around 97.9k

→ Strong rejection near 100k 💥

→ Long upper wicks

→ Momentum started to fade

Classic blow-off top behavior.

2️⃣ Trend Structure Shift 🔄

After the top:

•Higher highs stopped ❌

•First lower high formed

•Then a clean lower low break ⬇️

This confirms a daily trend shift: Bullish → Bearish.

Impulse → Distribution → Markdown 📉

3️⃣ Moving Averages Signal 📊

MA(5) crossed below MA(10)

Price is below both MAs

➡️ Short-term momentum = bearish

➡️ Any bounce = relief rally for now.

4️⃣ Volume Tells the Truth 🔍

On the breakdown:

•Selling volume expanded 🔴

•Bounces came with weak volume 🟢

➡️ Sellers in control

➡️ Buyers are reactive, not aggressive.

5️⃣ Key Levels to Watch 🎯

Current: ~87.6k

🟥 Resistance:

•89.7k – 90.5k

•92.6k

🟩 Support:

•86.0k

•83.7k (major)

If 86k fails ❌

➡️ Next magnet = 83k 🧲

6️⃣ Market Context 🌍

This is not a random dip.

This is:

•Post-euphoria cooling ❄️

•Leverage flush 🧨

•Distribution after a vertical move

Healthy in bull markets dangerous if you’re over-leveraged ⚠️

7️⃣ Scenarios 🔮

🟢 Bullish:

•Hold above 86k

•Reclaim 90k with volume

•Range: 86k–92k

🔴 Bearish:

•Daily close below 86k

•Acceleration to 83k → 80k

8️⃣ Final Thought 🧠

Short-term trend = bearish

Long-term trend = still bullish

This is a correction inside a bull market,

but timing matters ⏱️

Trade structure, not emotions.

Manage risk. Respect levels.

Chart never lies. People do. ⭕️📉

27

1

26

90,352

Jan 26

Hey #TheCryptoGems Community !

This is what most people miss 👇

While others chase hype 🚀

this ecosystem is quietly compounding through real usage ⚙️

🎮 Games live

🔁 Transactions real

👥 Holders growing

You don’t need perfection to win.

You need momentum and this already has it ⚡️

⏳ Early phases don’t stay early for long.

Jan 25

Quick reminder: the ecosystem is live 🔥

143,458 holders are already inside.

13B G Coin is moving across real games and platforms.

$27.79M market cap, built on usage - not noise.

11,692% growth, and the pace hasn’t slowed.

If you’re watching this now, you’re early enough to matter.

If you’re not paying attention, the system keeps moving without you.

This is what a live ecosystem looks like 🤩

10

46

55,925

Jan 26

Good Morning #TheCryptoGems ☕️

AI infra is quietly becoming one of the most important layers in #crypto. ⚙️

@dgrid_ai lets builders route across multiple LLMs instead of locking into a single provider optimizing both cost and performance.

For anyone building #AI-native apps on #BNB Chain, this is a solid piece of foundational infrastructure to watch.

Infra > hype.

Builders > narratives.

🚀 DGrid is now live on DappBay!

DGrid is an AI compute & routing infrastructure that helps builders access multiple LLMs with better cost efficiency and flexibility.

Built on @BNBCHAIN, we're focused on lowering the barrier for AI-native applications and infra builders in the BNB ecosystem.

🔗 Explore DGrid on DappBay:

dappbay.bnbchain.org/detail/…

#AIonBNB #BNB #DGrid #AI

11

10

62,401

Jan 26

Hey #TheCryptoGems Community !

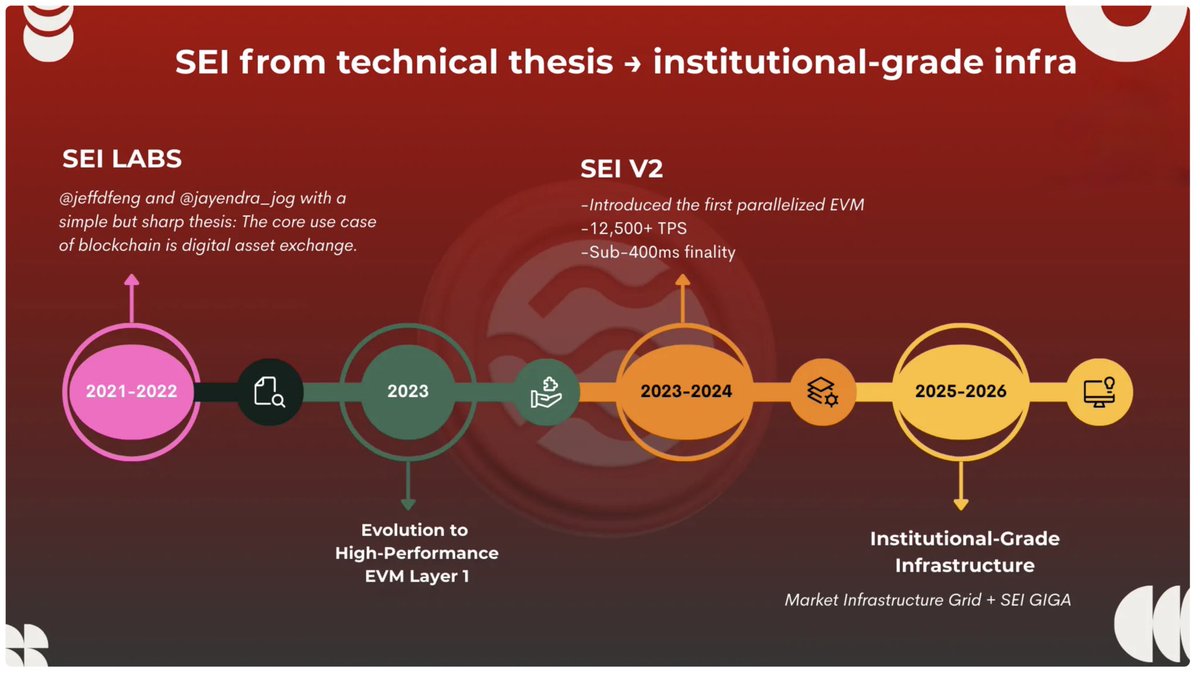

After the SEI GIGA upgrade in Q1 2026, I think @SeiNetwork has almost completed its evolution from a pure technical thesis into true institutional-grade infrastructure ⭕️

Let’s rewind and walk through how Sei got here 👇

Sei Labs was founded in 2021–2022 by @jeffdfeng and @jayendra_jog with a sharp idea:

💡 The core use case of blockchain = digital asset exchange.

At the time:

→ Ethereum struggled with speed & MEV

→ DeFi needed low latency & high throughput

So early Sei was all about performance:

⚡️ Trading-optimized L1

⚡️ Parallel execution

⚡️ Sub-second finality

⚡️ Built for DEXs, perps, arbitrage

Great for devs & degens… but not enough for institutions.

High TPS alone doesn’t attract long-term capital.

So Sei expanded from “fast chain” → “market infrastructure.”

Timeline ⏳

→ 2023: Mainnet launch as a trading-first chain

→ 2024–2025: Sei v2

🚀 First parallelized EVM

🚀 12,500 TPS

🚀 ~400ms finality

🚀 Shift to EVM-only for mass adoption

This was the turning point.

From a niche Cosmos chain → a hyper-scalable, general-purpose EVM.

By late 2025 / early 2026, the final transformation began 🧩

Two pillars:

1⃣ Market Infrastructure Grid

🤝 @Binance validator security

🤝 @Circle native USDC (CCTP)

🤝 @Chainlink oracles

🤝 Crypto.com custody

🤝 @OndoFinance tokenized treasuries

Plus RWA exposure via BlackRock, Apollo, Hamilton Lane.

Use cases:

→ Regulated funds

→ Trading & lending

→ Asset management

→ $30M RWAs tokenized

→ DeSci funds like $65M Sapien Science

2⃣ SEI GIGA Performance Leap

⚡️ 200K TPS

⚡️ ~400ms finality

⚡️ Ultra-low fees

This is no longer just “fast.”

It’s:

🏦 Deterministic performance

🏦 Regulation-friendly tooling

🏦 Built for real financial flows

@SeiNetwork’s story mirrors crypto itself:

From:

🛠 Technical experiment

→ 🧱 Hardened infrastructure

→ 🌉 Bridge between DeFi & institutional capital

$SEI isn’t just a chain anymore.

It’s becoming market infrastructure.

$/acc ⭕️

14

2

20

66,364

Jan 25

Good Morning #TheCryptoGems ☕️

#Bitcoin faced a strong rejection from the 97.9K area and is now in a clear correction phase. Price is currently trading around 88,576, after breaking the short-term bullish structure.

1) Market Structure

•The move from 83.8K → 97.9K has completed.

•After the rejection, BTC formed a lower high, signaling trend weakness.

•The previous short-term uptrend is now broken.

•Current structure suggests pullback / consolidation rather than continuation.

2) Key Support Levels

•89,300 – 88,000 → First and very important support zone (currently being tested)

•86,200 → If this breaks, downside momentum can accelerate

•83,800 → Major macro support (origin of the last impulse)

A daily close below 88K would open the door for a deeper correction.

3) Resistance Levels

•92,400 → First resistance for any relief bounce

•95,500 → Trend recovery zone

•97,900 → Main top / without a breakout, new ATH is unlikely

4) Moving Averages

•Price is trading below short-term MAs.

•MA(5) is turning down → momentum is weakening.

•MA(10) has been lost → short-term control is with sellers.

5) Volume Analysis

•Selling pressure increased on the drop from the top.

•This confirms the move is distribution-driven, not just a shallow pullback.

•Buyers are passive for now.

6) Scenarios

🔴 Bearish Scenario:

Daily close below 88K →

Targets: 86.2K → 83.8K

🟢 Bullish Scenario:

If 88–89K holds and a strong reaction comes →

Targets: 92.4K → 95.5K

Trend can only turn bullish again with a daily close above 95.5K.

Conclusion:

•Short-term structure is weak

•88K is a critical decision zone

•No aggressive longs without confirmation

•Patience is key here

📌 Not financial advice. Manage your own risk.

10

1

27

72,463

Jan 25

🌞 Place Where Yield Is Yours @solsticefi

The next step in DeFi is here.

Institutional-grade yield, for everyone. 🏛️➡️🌍

Built on Solana for speed, transparency, and accessibility ⚡🔗

You invest your assets Solstice finds the best yield for you.

No more searching. No more guessing. 🤖💰

Permissionless yield. Real returns. No black boxes. 🔓✨

➛ USX : Synthetic Stability

Fully collateralized, dollar-pegged stablecoin 💵

The core of Solstice’s transparent yield ecosystem

➛ Flares : Engage, Earn, Grow 🔥

Earn Flares, unlock SLX airdrops, fuel adoption

The more you contribute → the more you gain 🚀

➛ SLX : The Power Token ⚙️

Governance, rewards, and true community alignment

Built for everyone.

From retail to funds one seamless on-chain experience 🌐

No-code setup. Smooth UX at every step. 🧩

The yield era is already here.

Stay Solstice. 🌞💎

4

21

57,452

Jan 25

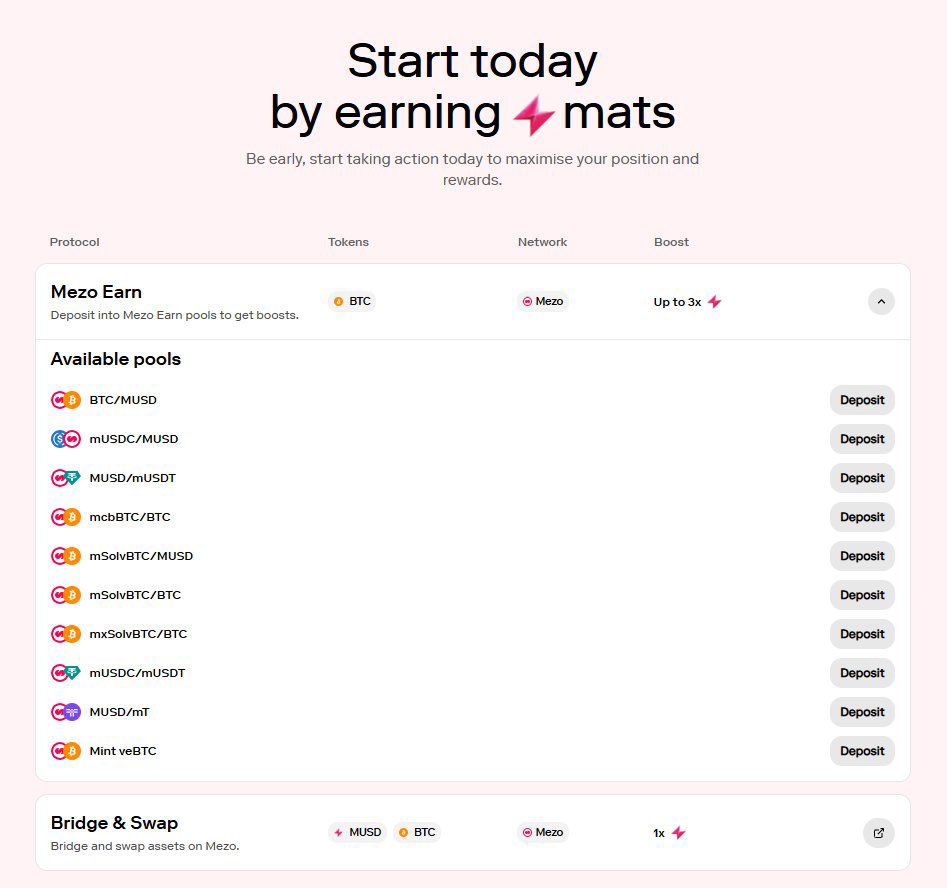

👀 February warm-up: Mezo

@MezoNetwork = a full Bitcoin banking experience

Store • Earn • Borrow • Spend fully onchain 🟠

They’re running Bankfree right now:

A leaderboard season before the wider distribution phase 🏁

The loop is simple 👇

🔹 Do onchain tasks (deposit BTC, collateralize, vaults, LP…)

🔹 Earn MATS

🔹 MATS = boost your rank future upside 🎯

🔹 Earlier in = more time to stack ⏳

This is real proof-of-participation:

Not last-minute capital, but early consistent players win 🧠

With $28.5M backing (Pantera, Multicoin, GSR…)

the setup looks very clean for early participants 💎

And honestly…

I’d be surprised if this doesn’t lead to something bigger after 🚀

Already farming MATS.

Think you can beat my rank? Prove it 👇😈

🔗 bankfree.mezo.org

7

14

59,236

Jan 24

Hey #TheCryptoGems Community !

🚀 @trylimitless Explained Simply 🚀

Limitless is a decentralized high-frequency prediction market built for fast traders.

⏱️ Trade hourly & daily crypto traditional price forecasts on a short-term basis.

💼 Backed by:

Coinbase Ventures • 1confirmation • Arthur Hayes

✨ Why Limitless?

📊 Central Limit Order Book

→ Tighter spreads than AMMs

⚡ Capital Efficiency

→ Merge & split outcome shares to unlock collateral instantly

⏳ High-Frequency Markets

→ Expirations as short as 1 hour

🧩 Multi-Outcome Trading

→ Reuse “No” positions across multiple outcomes

🧭 Quick Guide

🔗 Connect your wallet to Base

🎯 Pick a market (e.g. BTC > $100k?)

🟢 Buy Yes / 🔴 Buy No with market or limit orders

💰 Redeem winning shares for $1.00 or sell early for profit

📈 Current Status

• $700M in volume processed

• $LMTS token is live

🔥 The future of high-frequency prediction markets.

7

1

33

64,978

Jan 18

Good Morning #TheCryptoGems ☕️

DeFi isn’t becoming one big liquidity pool.

It’s splitting into lanes 🛣️

The question is no longer how much liquidity?

It’s who is trading, how risk is priced, and what execution requires.

🔹 Retail → access & distribution

🔹 Pro → speed, capital efficiency, control

🔹 Risk → isolated vs shared

🔹 Yield → risk as a product

🔹 RWAs → permissioned rails

This isn’t fragmentation.

It’s sorting 📐

And that’s why Arbitrum matters 👇

⚡ Perps

🏦 Advanced lending & risk isolation

📊 Yield structuring

🏛️ Institutional & RWA flow

🧩 Retail without execution tradeoffs

Fewer clicks.

Bigger checks 💰

DeFi’s next phase isn’t more liquidity.

It’s right-sized liquidity.

Capital doesn’t chase noise.

It chooses structure 🧠

18

18

51,298

The Crypto GEMs retweeted

30 Dec 2025

FoxVerse 2026: Content Creation Challenge 🦊

Create. Post. Trade. Earn.

💰 $1,000,000 prize pool

🥇 Win up to 2,026 USDT

Play on social media. Get rewarded. Join the challenge: kucoin.com/campaigns/FoxVers…

#KucoinFoxVerse2026 #KuCoinFutures

168

116

950

408,582

28 Dec 2025

Hey #TheCryptoGems Community !

🚀 $EMI is on the move.

Momentum is building fast. 📈

The community grows stronger every single day 🤝

This is only the beginning.

Early stage. ⚡ Real energy. Real holders. 💎

If you’re here now you’re early 🧠

If you’re watching… don’t blink 👀

join.pump.fun/HSag/k7dgdumd

$EMI 🚀🔥

15

46

52,226

28 Dec 2025

Hey #TheCryptoGems Community !

After TGE, most teams either go silent… or double down on narrative.

Talus Labs did the opposite 👀

Nexus v0.3 is live, focused on things that are hard to market but actually matter:

🛠 Stability

⚡ Performance

🧩 Infra polish (dev experience reliability)

Placed on the roadmap, the strategy is clear 👇

🔹 Foundation-building before Vision → mainnet

🔹 Vision devnet demo is open for builders

🔹 Nexus v0.3 = tightening bolts, reinforcing the engine

🔹 The memory layer (via Walrus Protocol) turns agents from short-lived demos into

🧠 stateful products that improve the longer they run

Everyone’s chasing “agent hype,” but real agent economies win on execution:

✅ Systems that run reliably

✅ Verifiable workflows

✅ Memory that compounds over time

When those are in place, ecosystems grow on their own 🌱

If v0.4 is the mainnet push,

v0.3 feels like gear farming before the boss fight 🎮⚔️

Builders should jump into Vision and feel how solid the engine really is 👀🚀

12

3

63

68,929

25 Dec 2025

Hey #TheCryptoGems Community !

🚨 BTC/USDT Technical Analysis 🚨

📉 Macro Structure:

Bitcoin is still trading in a clear downtrend after the major rejection from the $126K peak. The strong sell-off broke multiple key supports, confirming a bearish market structure.

📍 Current Price: ~$88,200

🧱 Key Levels:

•Support:

•$88,000 → short-term demand zone

•$80,600 → major liquidity support (critical)

•Resistance:

•$98,300 → previous breakdown level

•$108,400 → strong supply zone

•$118,400 → trend invalidation area

📊 Moving Averages:

•Price is trading below key MAs, showing weak bullish momentum

•Short-term MAs are flat → consolidation phase after the dump

📉 Volume Analysis:

•Huge volume spike during the drop to $80.6K 📛

•Current volume is declining → no strong buyers yet

🧠 Market Psychology:

This looks like distribution → capitulation → consolidation.

Smart money is waiting. Retail is exhausted.

🔮 Scenarios:

✅ Bullish case:

If BTC holds above $88K and reclaims $98K, we may see a relief rally toward $108K.

❌ Bearish case:

Loss of $88K opens the door to $80K–$78K range fast ⚠️

📌 Conclusion:

Bitcoin is at a decision zone. Volatility is loading…

Next move will be aggressive 🚀 or brutal 🩸

#Bitcoin #Altcoin #Crypto

8

5

41

71,374

23 Dec 2025

Good Morning #TheCryptoGems !

🚨 TONSO Signal Protocol for Crypto Telegram

Have you tried it yet? 👀

Diving into Tonso today 🔍

An early-stage project built on Telegram & TON, combining AI 🤖 Attention Economy 👁️ InfoFi.

No speculation here only info from @tonso_ai and the official site 👇

🧠 What is Tonso?

Tonso is building a “Signal Protocol” for Crypto Telegram.

An AI-powered SuperApp that turns attention into a measurable & tradable asset.

It indexes thousands of Telegram channels to track mindshare, helping users:

• Spot alpha early ⏰

• Monetize creators 💰

• Understand narrative momentum 📊

📈 Why Telegram > X?

✔️ Longer content lifespan

✔️ Less algorithmic noise

✔️ Quiet but high-signal alpha flows

⚙️ Key Features

🔥 Buzz & Earn

• Creators earn internal points for quality content

• Users get rewarded for network growth & discovery

🎁 Campaigns & Rewards

💰 $1M Tonso Earn Pool

Partners include:

• A Solana yield protocol ($300M TVL)

• IntoTheSpace (team behind UFO Gaming, $1.5B ATH)

• Tria (self-custodial neobank)

📅 Campaign runs Dec 2025 – Feb 2026

📌 Telegram creators & X-linked users get bonuses

(Yaps / Ethos boosts ⚡)

🤖 AI Layer

• Merit-based mindshare tracking

• Strong anti-spam signal filtering

🚀 Onboarding

Via @TonsoAIBot:

🔗 Connect wallet X

✅ Complete tasks

🎟️ Use code TONSO for extra bonuses

👀 Telegram alpha might be quieter but it often moves first.

38

3

23

75,961

22 Dec 2025

🚨 BREAKING 🚨

Baron Trump has launched the presale for his own Coin $USA/$USD1

🌎 Official Presale: usaofficialcoin.com

📯 Tg: t.me/ lN4ipMOSe_4xNWMy

I was the first to post $TRUMP coin (at $0.69) and i’ll be the first to share this one too, we’re gonna make millions together.

Those that aren’t following me will regret

4

1

16

45,209

22 Dec 2025

Hey #TheCryptoGems Community!

🚀 $WOD keeps accelerating!

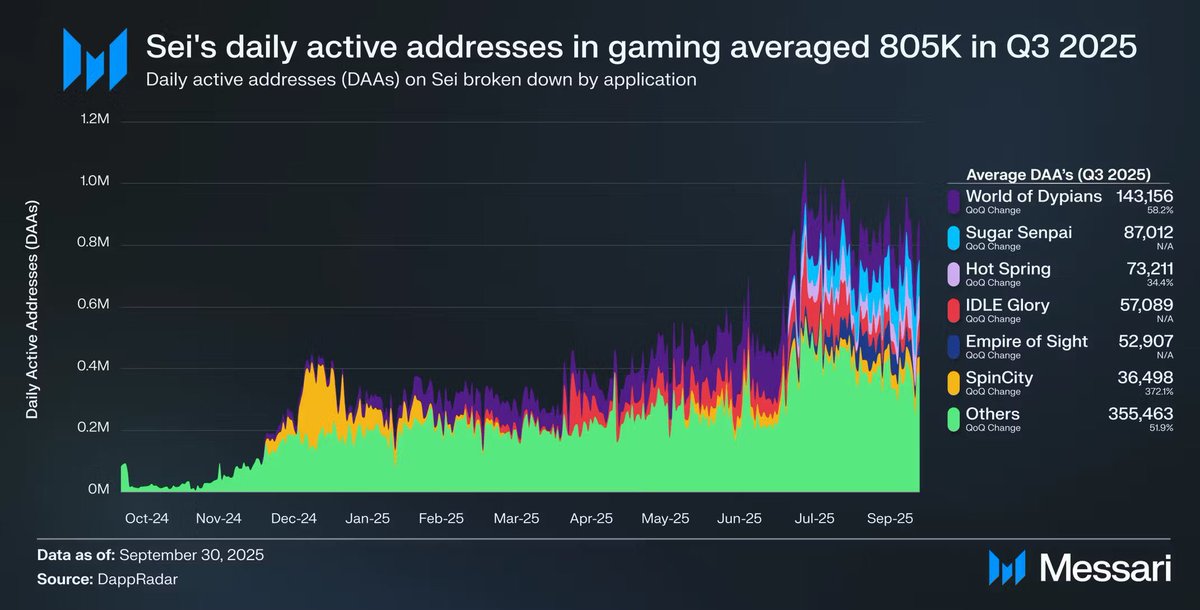

@worldofdypians is setting massive on-chain records across multiple networks 🔥

📊 $44.3B in volume on @BNBCHAIN

🎮 Ranked Top GameFi project on Sei, according to @SeiNetwork stats

And this is only the beginning…

The team is building far beyond GameFi, with multiple products in the pipeline and major updates coming soon 🧠⚙️

👀 Definitely one to keep on your radar.

21 Dec 2025

🔥 $WOD keeps breaking limits!

We’ve officially surpassed $44.3 BILLION total volume on @BNBCHAIN, marking another major milestone for the ecosystem.

Real activity. Real momentum. Real growth.

And the journey is only getting started.

4

2

8

62,823

22 Dec 2025

Hey #TheCryptoGems Community !

🚨 @Agentia_ is officially LIVE! 🤖🎮

And honestly? This is shaping up to be one of the most exciting AI-gaming plays on Solana right now. ⚡️

This isn’t a boring click-to-farm game.

You step in as an Operator 🧠

→ build your squad

→ optimize agent synergy

→ grind real progression

Getting started is fast & smooth:

🔹 Visit the app

🔹 Connect your SOL wallet 💼

🔹 Enter invite code: AGENTDBD4NJ

🔹 Buy a base agent & start assembling your team

Early-game setup:

🏠 Room 1 → 4 agents

🏠 Room 2 → 6 agents

💡 My tip:

Fill Room 1 with 4 different agents first to lock in stable output early synergy, then expand into Room 2 for scaling. 📈

Early entry = time advantage ⏳

If you want that edge, get in early and start building your AI squad now. 🚀🔥

19 Dec 2025

AGENTIA IS LIVE 🔥

JOIN VIA: app.agentia.games/

CODE: AGENT000001

OPERATORS, LET'S MAKE HISTORY TOGETHER!

🚀🚀🚀

3

9

58,209