Joined December 2024

- Tweets 5,661

- Following 418

- Followers 1,117

- Likes 7,531

1,410 Photos and videos

Pinned Tweet

Jun 11

⚽ Something big is coming to CryptoThreads.io!!

More details dropping soon. Stay tuned!

👇Follow @CryptoThreadsX so you don't miss the announcement.

21

7

29

3,027

Jun 12

📊 INSIGHT ARTICLE – JUNE 12

🏦 Stablecoins in Asia Are Becoming a Banking Business

Hong Kong, Japan, and South Korea are all converging on a "bank-anchored" model but each in their own way, and all three are running into the same paradox.

🔍 3 very different versions of the same label:

🇭🇰 #HongKong → Only 2 licenses granted: HSBC and a Standard Chartered Animoca joint venture. TradFi holds the keys Web3 only gets a minority seat at the table.

🇯🇵 #Japan → A tiered system open to banks, fintechs, and trust companies alike. Fintech (JPYC) actually launched first ahead of any bank back in October 2025.

🇰🇷 #SouthKorea → Gridlocked. The central bank wants banks to hold ≥51% ownership. The FSC and fintechs are pushing back hard. The bill is in parliament but going nowhere fast.

⚠️ The central paradox:

These frameworks exist partly to fight "digital dollarization" yet >98% of global stablecoins are USD-pegged. Users can swap local-currency coins into USDT in a few clicks on any DEX. Regulation controls who can issue, not why people want dollars.

💡 Who actually wins?

Not whoever gets the license to mint but whoever owns the users and a real use case. HSBC isn't strong because it can issue an HKD coin. It's strong because it already has 3.3M PayMe users to pipe it into.

🔑 The most important question isn't "who is allowed to issue?" it's "why would anyone hold local currency instead of USDT?"

Until a local-currency stablecoin can answer that, every license is a necessary condition but not a sufficient one.

📖 Full research:

👉 cryptothreads.io/research/as…

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

15

12

29

2,825

Jun 12

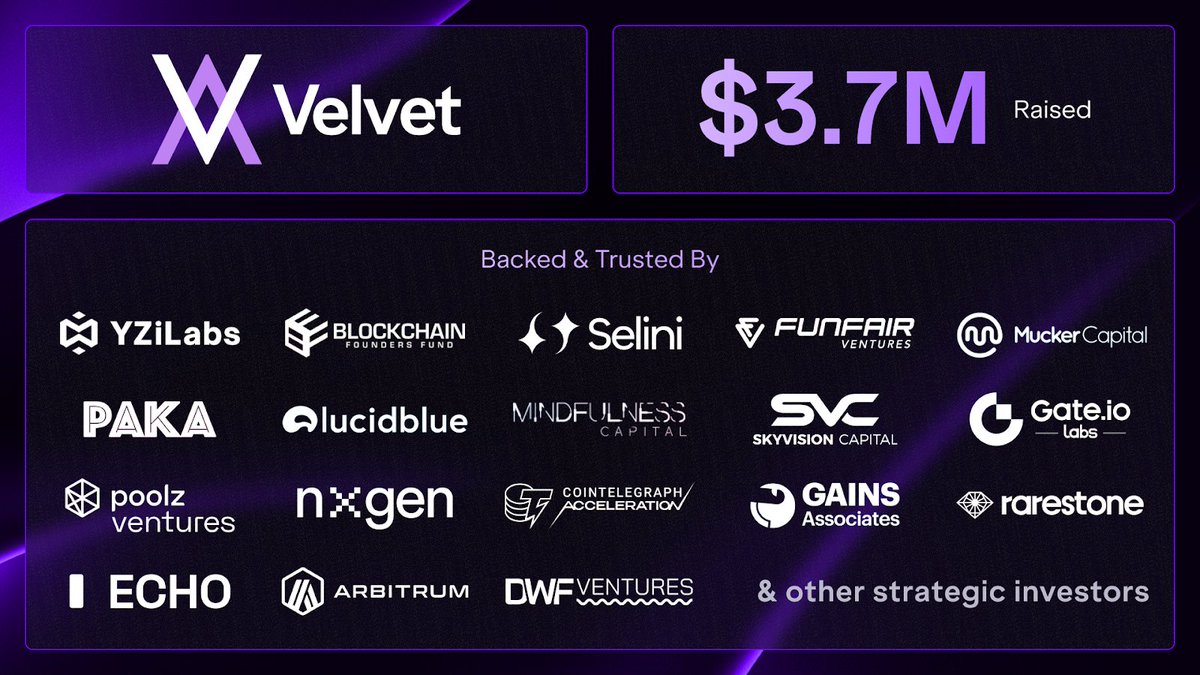

🚀 velvet:native just pumped ~130% in 24h - here's everything you need to know

📊 Market Snapshot (June 12, 2026)

• Price: $1.77 | 24h: 92.3%

• Market cap: ~$748M | 24h Volume: ~$100M

• Rank: #82 | Above ATH: 2.2%

🔍 What's happening?

In just 24 hours, velvet:native ran from $0.76 → $1.78 (~x2.3). This is a textbook momentum breakout, often fueled by FOMO and breakout chasing once a new ATH is printed.

Volume/MCap hit ~13% elevated for a midcap. MC/FDV is only 0.42, meaning circulating supply is still small → price is highly reactive to incoming buy pressure.

The exact catalyst hasn't been confirmed possible triggers: new listing, launchpool, IDO, or an AI-DeFi narrative play.

📈 Scenario 1 - Momentum continues (~40-50%)

If price holds $1.65–1.70 and volume stays strong, a retest of $1.85–2.00 is on the table.

📉 Scenario 2 - Sharp correction (~50-60%)

After a ~130% 24h move, a pullback is the more likely outcome.

Key support levels: $1.40 → $1.15 → $0.95

⚠️ Key Risks

• TVL ~$709K vs MCap ~$748M → price driven by sentiment, not real usage

• MC/FDV = 0.42 → significant unlocks still ahead

• Large spread & slippage likely given extreme volatility

Chain: BSC Base | Listed on: Gate, Bitget, KuCoin, MEXC, Kraken...

⚡ Research only · Not financial advice · DYOR

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

15

11

26

2,522

Jun 11

🚀 $BEAT just hit an ATH of $7.92 that's 10,000% from its $0.068 low in Nov 2025.

💰 Real revenue, not just hype. #Audiera posted $2.87M in weekly earnings burned 770k BEAT on-chain. Every. Single. Week.

🎵 AI music studio rhythm #GameFi on BNB Chain where humans AND AI agents earn, create & compete as equals.

🏆 World Cup 2026 collab: users generate AI football anthems for $5,000 USDC in prizes. Product in real use.

⚠️ Risk: OI near $200M, heavy leverage one bad candle could cascade liquidations fast.

🔒 NFA. DYOR.

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

17

8

27

2,994

Jun 10

🚨 ethereum:0xcf5104d094e3864cfcbda43b82e1cefd26a016eb ( Humanity Protocol) just got wrecked.

💸 $32M drained across 17 wallets on $ETH & $BSC

🪙 ~447M tokens stolen or minted by attackers

📉 Token crashed 90% from $0.70 → $0.05

🔓 The protocol wasn't hacked. A team member's private key was.

🕵️ ZachXBT thinks it may have been staged token unlock was due next week. Convenient timing.

⚠️ Whether hack or exit the real failure is structural: a $1B protocol with no multisig discipline, no timelock, and a single point of human error. That's not bad luck. That's a design choice.

🔑 Key management is the new smart contract bug.

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

17

8

23

3,436

📘 DAILY LEARN – JUNE 9

🔓 You can now trade leveraged crypto without giving anyone your funds.

Perp DEXs (Perpetual Decentralized Exchanges) are changing how traders access derivatives markets.

Here's what you need to know:

→ Trade long/short with up to 50x leverage, no expiry date

→ No KYC. No account. Just connect your wallet

→ Smart contracts handle everything execution, liquidation, settlement

→ Your funds never touch a company's wallet (RIP FTX victims)

Top players right now:

⚡ Hyperliquid ~34% of total perp DEX volume

📊 dYdX - Cosmos-based, 220 markets

🔵 GMX - Arbitrum/Avalanche liquidity pool model

☀️ Jupiter Perps - Solana's dominant venue

The tradeoff? Smart contract risk replaces counterparty risk. And leverage still liquidates fast a 10x position is gone on a 10% move.

Perp DEX volume hit $7.9T in 2025 alone. The space is growing but it's not for beginners.

Which do you trust more with your trades a CEX with better liquidity, or a perp DEX where you keep custody? 👇

Read more: cryptothreads.io/learn/what-…

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

20

3

93

3,149

📊 INSIGHT ARTICLE – JUNE 8

AI agents can't use credit cards. Here's what replaces them. 🤖💳❌

Traditional payment rails were built for humans billing accounts, business hours, and fees that make $0.31 transactions completely unworkable.

AI agents operate 24/7, execute thousands of micro-payments per hour, and can't open a bank account. Legacy rails fail all three tests simultaneously. ⚡

Stablecoins especially USDC on Base and Solana solve this:

✅ Sub-second settlement at fractions of a cent

✅ No human account required

✅ Fully programmable, 24/7, no gating

The proof is already there. 📊 x402 protocol hit 165M transactions and $50M in volume across 69,000 active agents by April 2026 — growing from zero in under a year.

Smart accounts (ERC-4337) add the safety layer 🔐: hard spending caps, session keys, and allowlists enforced on-chain not in code an agent can bypass.

📈 Juniper Research projects agentic payment volume reaching $1.5 trillion by 2030.

The rail problem? Largely solved. ✔️

The real gap? Regulatory clarity on liability and a trust/identity layer that enterprises can actually rely on. ⚖️🏛️

💬 If AI agents are becoming economic actors, who's responsible when one makes a prohibited payment — the developer, the platform, or the wallet?

Read more: cryptothreads.io/insights/wh…🔗

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

20

9

21

3,448

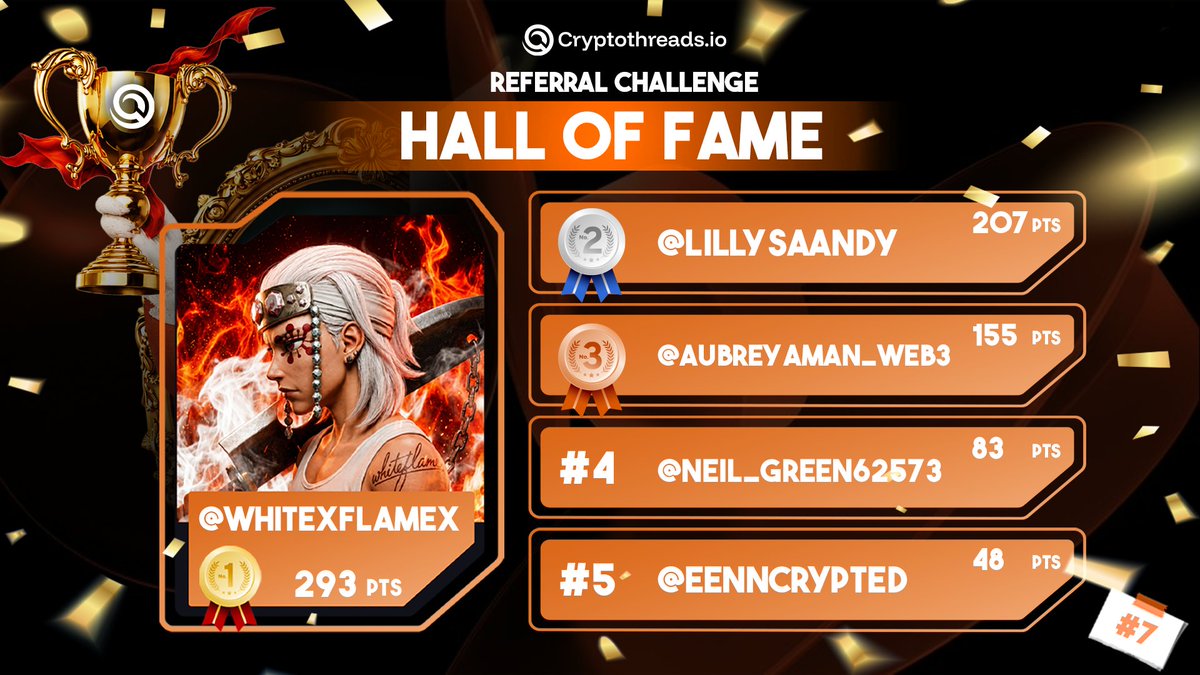

📣 CryptoThreads.io Partner Growth Campaign — HALL OF FAME 🏆

The wait is OVER. Here are your OFFICIAL WINNERS! 🎉

🥇- @WhiteflameX → 💰 $100

🥈 - @Lillysaandy → 💰 $40

🥉 - @AubreyAman_Web3 → 💰 $30

4️⃣ - @neil_green62573 → 💰 $20

5️⃣ - @eenncrypted → 💰 $10

🎊 Congratulations to ALL winners! You earned it!

📌 HOW TO CLAIM YOUR PRIZE:

All winners have 48 HOURS from this post to DM your wallet address to @NG_Harry on Telegram.

⚠️ Miss the deadline = forfeit your prize. Don't wait!

🙏 A huge THANK YOU to everyone who participated in this campaign. Your support means everything to us.

Stay tuned — more campaigns & bigger prizes are coming! 🚀

22

9

26

4,035

📊 INSIGHT ARTICLE – JUNE 6

🚨 Not all tokenized assets are created equal and the difference could cost you everything.

Owning a tokenized stock ≠ owning the stock.

There are 2 models dominating RWA tokenization right now:

✅ Cooperative Issuer integrates blockchain into the official shareholder register. You get real equity, voting rights, dividends, direct claims.

⚠️ Non-Cooperative - A third party wraps the asset without issuer involvement. You get price exposure. That's it.

🏛️ The SEC made this clear in Jan 2026: only issuer-sponsored tokenization creates true equity ownership.

📊 Real-world stakes:

→ 🖤 BlackRock BUIDL ($2.85B AUM) = cooperative, institutional-grade ownership

→ 🟣 Ondo Global Markets (200 tokenized stocks, 3.2M daily users) = custodial exposure, zero shareholder rights

⚔️ Meanwhile, Coinbase is pushing back - arguing mandatory issuer consent is anticompetitive and stifles innovation.

📈 The market is at $35B and heading toward $18.9T by 2033.

🔍 Before you buy any tokenized asset, ask 3 things:

1️⃣ Who issued this token?

2️⃣ Is it linked to the official shareholder register?

3️⃣ What happens if the intermediary fails?

❗️If those answers are hard to find - that's your answer.

💬 Do you think non-cooperative tokenization should be allowed for retail investors, or is the ownership risk too high?

🔗 Read more: cryptothreads.io/insights/co…

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

19

9

19

3,770

📢 THE OFFICIAL END - CryptoThreads.io Partner Growth Campaign

The Referral Challenge has officially come to an end. Thank you for participating and supporting! 🙏

🏆 What's Next?

The FINAL LEADERBOARD & prize results will be officially announced TOMORROW. Stay tuned!

⏳ In the meantime, sit still and get ready for the big reveal. Good luck to all participants! 🍀

📌 Follow @CryptoThreadsX for the latest updates.

Stay tuned - there are plenty of exciting surprises coming your way.

🏆 CryptoThreads.io Partner Growth Campaign - FINAL LEADERBOARD 🏆

📊 The official results have been updated!

📌 Important Notes:

✅ The results shown are officially recorded by the system.

⚠️ Appeal Policy:

• If you believe the results are incorrect and an appeal would change your position on the leaderboard - contact @NG_Harry on Telegram.

• Appeal window: 24 HOURS from the time this post is published.

• After 24 hours, no further appeals will be accepted.

⏰ Check your results and reach out promptly if needed!

17

8

19

4,311

🏆 CryptoThreads.io Partner Growth Campaign - FINAL LEADERBOARD 🏆

📊 The official results have been updated!

📌 Important Notes:

✅ The results shown are officially recorded by the system.

⚠️ Appeal Policy:

• If you believe the results are incorrect and an appeal would change your position on the leaderboard - contact @NG_Harry on Telegram.

• Appeal window: 24 HOURS from the time this post is published.

• After 24 hours, no further appeals will be accepted.

⏰ Check your results and reach out promptly if needed!

1

10

20

6,834

📊 INSIGHT ARTICLE – JUNE 4

🚨 Trading AI company perps? You might be in the SEC's crosshairs.

⚡ OKX, #Hyperliquid & Injective now offer leveraged synthetic futures on #OpenAI, #Anthropic & #SpaceX - no shares, no equity rights, just price exposure on crypto rails.

🤔 Sounds clean. The legal picture isn't.

⚖️ Under Dodd-Frank, contracts tied to a single issuer's valuation may qualify as security-based swaps putting both platforms AND traders in regulatory gray zone.

📊 Key facts:

🏦 Anthropic hit a $965B valuation & filed a confidential S-1 on June 1

💰 OpenAI closed at $852B post-money in March

🤝 SEC-CFTC signed a new coordination MOU in March 2026

🌐 Geo-blocks ≠ compliance ask Falcon Labs

❌ You hold zero shareholder rights. And if regulators act, your trade gets disrupted before the IPO thesis ever plays out.

🎯 The exchanges collect fees while uncertainty lasts. Traders absorb the shock when it doesn't.

💬 If synthetic AI perps get classified as security-based swaps, which platform do you think faces the biggest regulatory heat and will this kill the pre-IPO trading meta entirely?

🔗 Read more: cryptothreads.io/insights/pr…

#Cryptothreads – Crypto Threads for the Best Crypto Insights, Research & Knowledge Platform in Asia

17

10

19

4,089

⏳ FINAL HOURS — CryptoThreads.io Partner Growth Campaign

The campaign officially closes at 11:59 PM UTC, June 4.

⚠️ Registrations submitted after the deadline will not be counted.

🔥 The leaderboard is still live, and the competition is getting intense. Keep pushing, protect your position, and stay focused rankings can change at any moment.

🏆 Final results will be announced after verification is completed.

18

12

25

4,755

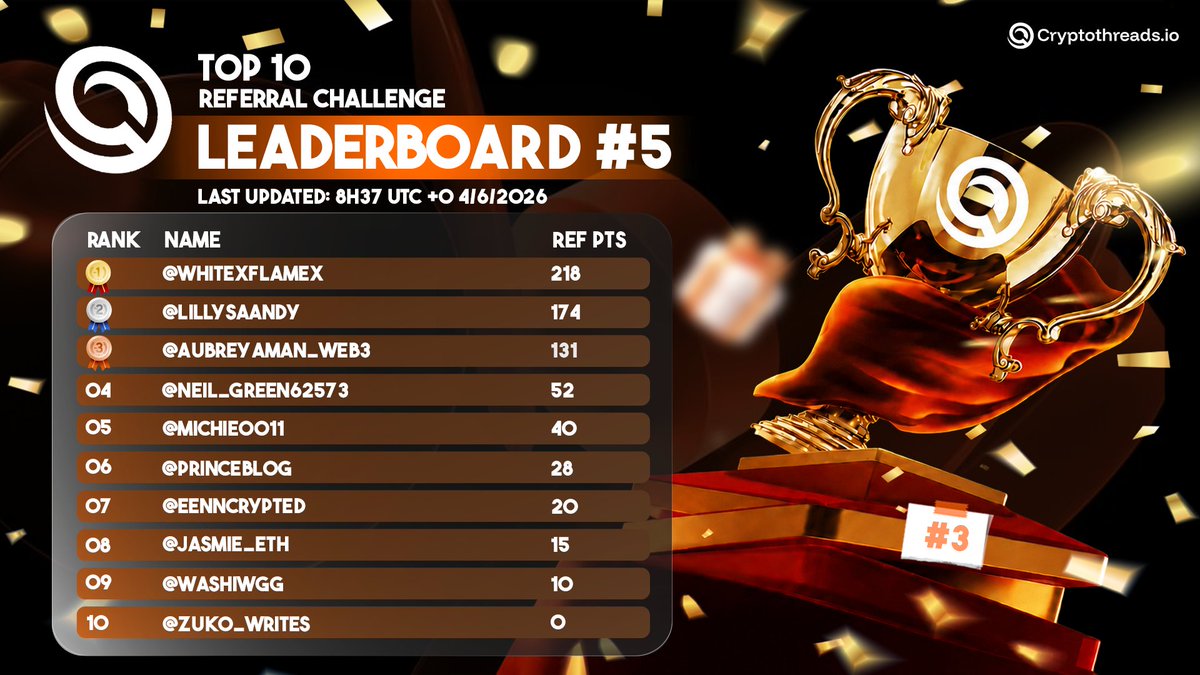

LEADERBOARD #5

Top 10 - Referral Challenge

Last Updated: 8h37 UTC 0 4/6/2026

15

2,602

📊INSIGHT ARTICLE – JUNE 3

Tokenized Private Equity Is Not What You Think It Is 🧵

Buying a token linked to #OpenAI or #SpaceX doesn't mean you own a piece of them. 🚫

Here's what most retail investors are missing 👇

🔒 Private company shares have transfer restrictions built into their legal DNA. Blockchain can speed up settlement — it cannot override a company's right to reject who owns its equity.

📌 When #Robinhood launched OpenAI tokens for EU retail users in July 2025, OpenAI publicly rejected any link to its equity. Those tokens? Derivative contracts against Robinhood Europe not OpenAI shares.

⚖️ The SEC drew the line in Jan 2026: → 🟢 Issuer-sponsored tokens = real ownership potential → 🔴 Third-party synthetic tokens = price exposure only

🏗️ An SPV label doesn't fix this. "Exposure to OpenAI" ≠ "Ownership in OpenAI"

✅ Before buying any private-company token, ask: ☑️ Did the company actually approve this structure? ☑️ Where do your legal rights run against the

company, or just the platform?

☑️ What happens if the platform becomes insolvent?

💡 Tokenization is powerful. But consent gaps, counterparty risk, and documentation failures can leave investors holding a narrative not equity.

💬 If a token tracks a private company's value but the company never approved it should platforms still be allowed to sell it?

📖 Read more: cryptothreads.io/insights/wh…

19

10

26

4,629