Joined October 2017

- Tweets 24,308

- Following 2,338

- Followers 89,432

- Likes 145,198

4,540 Photos and videos

$SOL weekly MACD just triggered a massive bullish divergence, from the exact same structural wedge breakout that previously started the historic bullrun

18

25

152

5,971

The daily RSI bounce is officially underway for $BTC

The first accumulation phase triggered a 21.85% rally over 54 days.

The second accumulation phase pushed a massive 38% move over 89 days.

We just hit the exact same structural bottom and the daily RSI is breaking out again.

How many days until we face melt to the upside?

21

36

200

15,917

Jun 13

$BTC is 31 bars into a correction that mirrors the 2022 bear market exactly, and the MACD on the 2W is at the same depth where the last cycle bottomed.

20

30

150

15,835

Jun 13

$TAO just broke out of the descending channel that's been controlling price action since $330 and is now testing the 200 EMA at $246.

This is the level that decides whether the breakout is real or just another fakeout.

POC support remains intact below, while $290 is the first major imbalance waiting to be filled if bulls can hold this reclaim.

20

33

147

14,944

Jun 12

$HYPE head and shoulders targets $45 on a neckline break at $57 but RSI divergence at every low makes this a low conviction short.

Holds $57 and reclaims $60 and the squeeze toward $65 becomes the real trade

13

29

155

15,938

Jun 12

$BTC is forming a textbook inverse Head & Shoulders beneath descending resistance.

The left shoulder, head, and right shoulder are now in place, while buyers continue defending higher lows.

A breakout above the neckline could trigger the next expansion higher

11

30

146

16,643

Jun 12

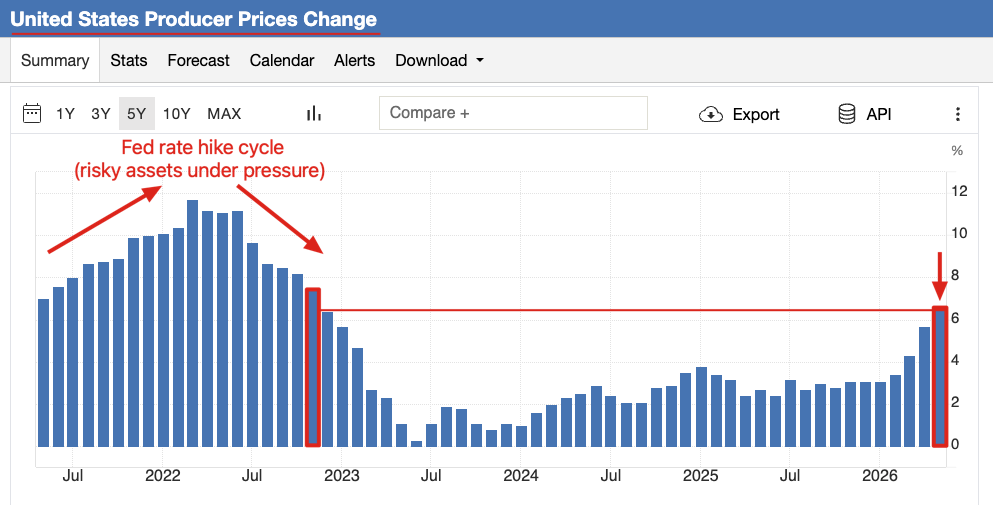

The US PPI data just came out yesterday, and things are not looking good.

Let me explain.

In short, PPI is inflation from the producer side.

PPI came in at 6.5%, now at its highest level since November 2022.

The problem is, PPI is a leading indicator, unlike CPI.

This is because producers and manufacturers are the ones at the "top." They're exposed directly to commodity markets, and they're the ones making bulk purchases.

That rising input cost takes time before it's passed on to consumers.

So, if PPI is now at its highest level since 2022, there's a big chance the CPI will catch up too in the months to come.

All the more reason for The Fed to do a rate hike.

Jun 9

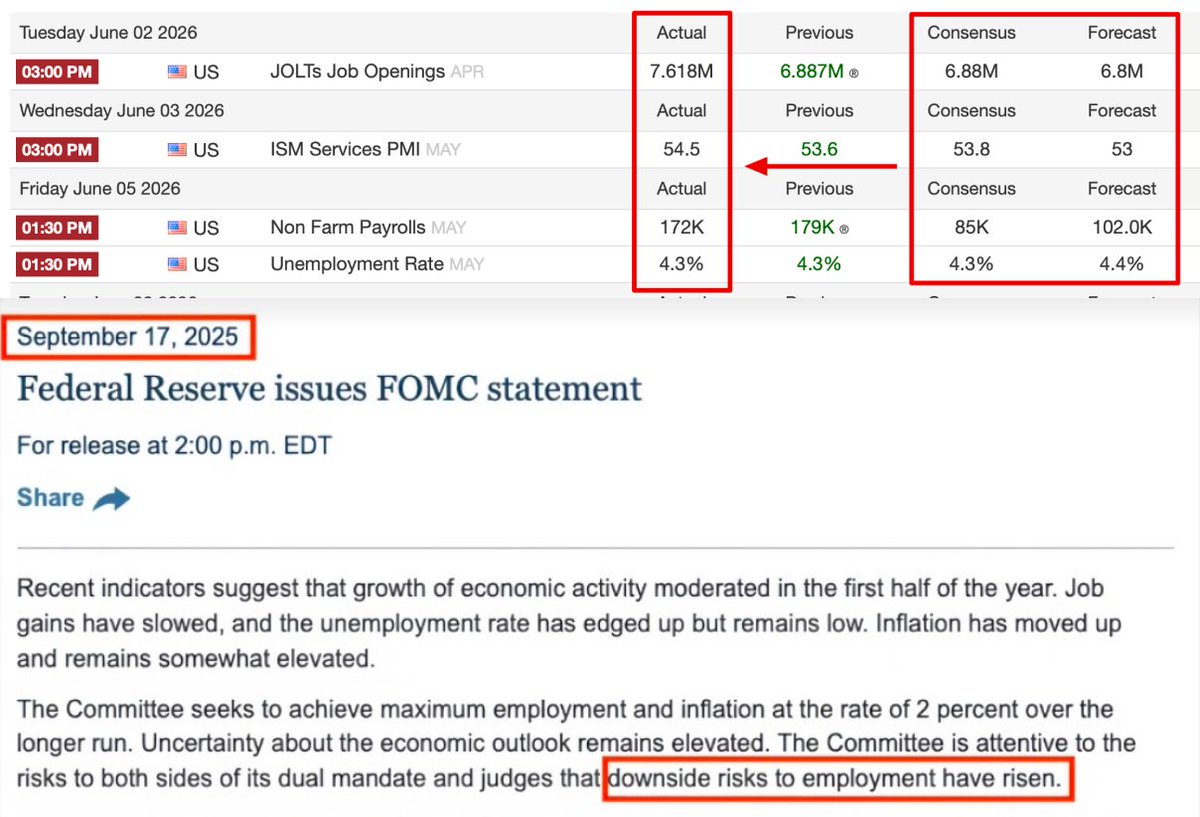

Last Friday, the S&P 500 experienced its biggest single-day loss of 2026. And funny enough, it was actually because of good news. Let me explain.

Last week, multiple US job reports came out, all beating consensus and forecasts by a wide margin, which reflects that the US economy is still going strong.

The NFP data came in at 172K, doubling the consensus estimate of 85K.

The problem is, a big reason why the Fed started cutting rates was because the job market was deteriorating. "Downside risks to employment have risen," as stated in the September 2025 FOMC statement.

With a strong job market report, there's no reason for the Fed to cut rates again.

This sparked a massive sell-off in risky assets like the S&P 500 and, in turn, Bitcoin.

So, to see a global risk-on mode once again, we need inflationary and growth data to come in soft.

12

31

128

14,314

Jun 12

There's another underlooked metric that has consistently marked Bitcoin's bear market bottoms.

That is the BTC Puell Multiple.

Won't get technical, but it takes a look at the supply side of Bitcoin, through its miners and their revenue.

Each bear market bottom, from 2011, 2015, 2019, and 2022, has been signaled by the Puell Multiple reaching 0.30-0.40.

Right now, we're at 0.58.

Close, but not quite there yet. Still good to pay attention every once in a while.

14

33

142

14,606

Jun 11

The $TRX analysis from a couple of days ago is showing solid confirmation.

The Stochastic on the 3D timeframe is at oversold levels last seen in February, just before a 30% return.

Let's see how this one goes.

Jun 9

After recently breaking out of its double bottom pattern with strength, $TRX is retesting its support zone.

Despite crypto being in a bear market, TRX showed a 40% return from February.

Now that price is back at a strong support, this should hold for the next continuation.

14

32

154

15,636

Jun 11

In only 4 days I'll be headed to the USA for the World Cup 2026. I think France is the top pick this year, but hoping for an underdog story.

Running all my predictions through @Predictstreet this tournament. Official on-chain prediction market for FWC 2026, points sit within a multi-billion dollar ecosystem. Claiming your Card early is the move.

Get yours: sprint.adipredictstreet.com/…

37

30

158

14,839

Jun 11

$BTC dominance has dropped 55% and 45% in the last two altseasons. We're only 36% into this one if the pattern holds. Alts haven't seen their real move yet

42

33

179

15,235

Jun 11

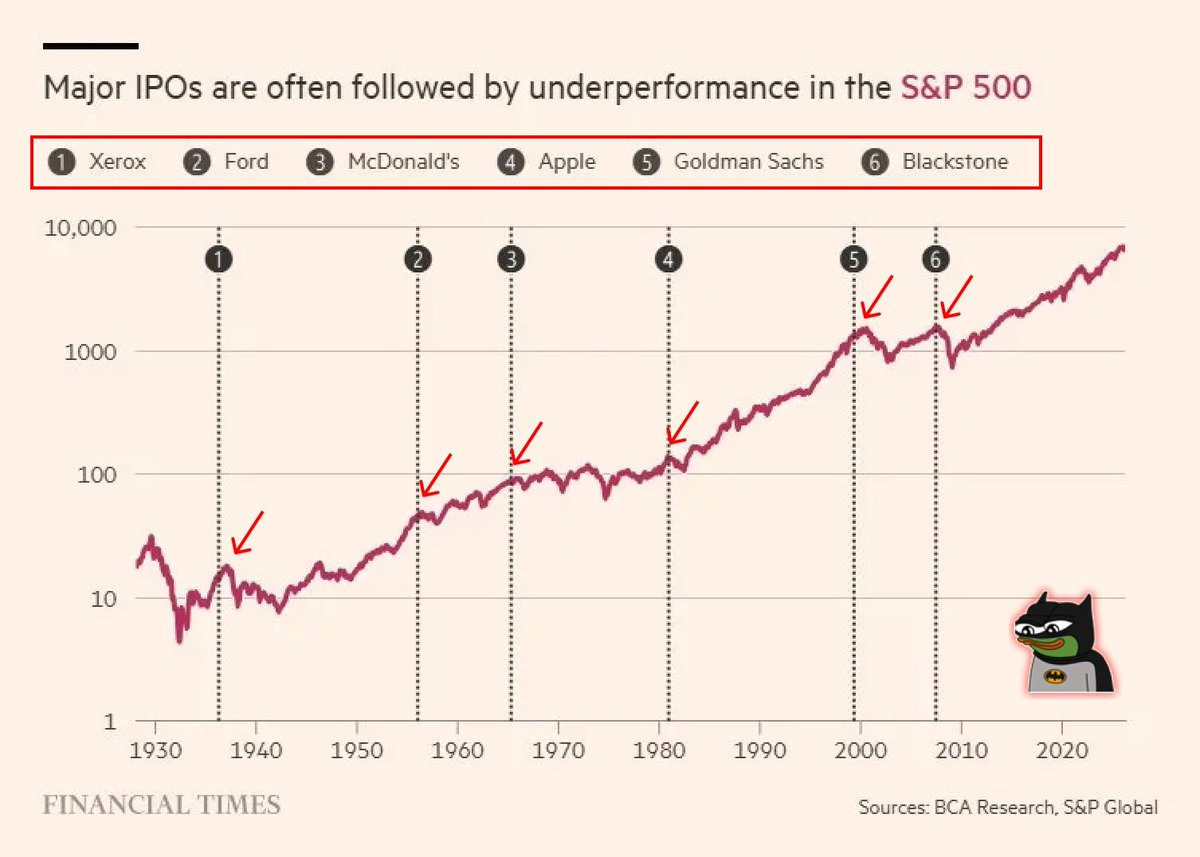

SpaceX's IPO is just around the corner.

There are a couple of things worth pointing out.

Yes, it is the biggest IPO of all time, beating all previous global IPOs, including Aramco's.

On the other hand, it creates a concentration risk, where everything is highly tied to a single entity.

Not just the index, but capital across the market would be tied to it as well.

One bad move, anything that tanks the stock price, drags everything with it.

We've seen this in past major IPOs. The market tends to pull back shortly after, as massive IPOs draw a big chunk of liquidity from elsewhere.

At the same time, it's an opportunity to buy things at a discount, if handled with proper capital allocation and positioning.

26

48

175

16,470

Jun 11

More context on the relationship between economic data and interest rates.

Higher for longer inflation, reflected by solid job and growth reports, forces the Fed to hold rates at elevated levels or potentially increase them further.

Historically, Bitcoin has never performed well in a high rate environment.

The market moves in advance of rate decisions because it is a forward-looking machine.

That's why Bitcoin and the S&P 500 are underperforming. Strong reports give the Fed more reason to hike.

Jun 10

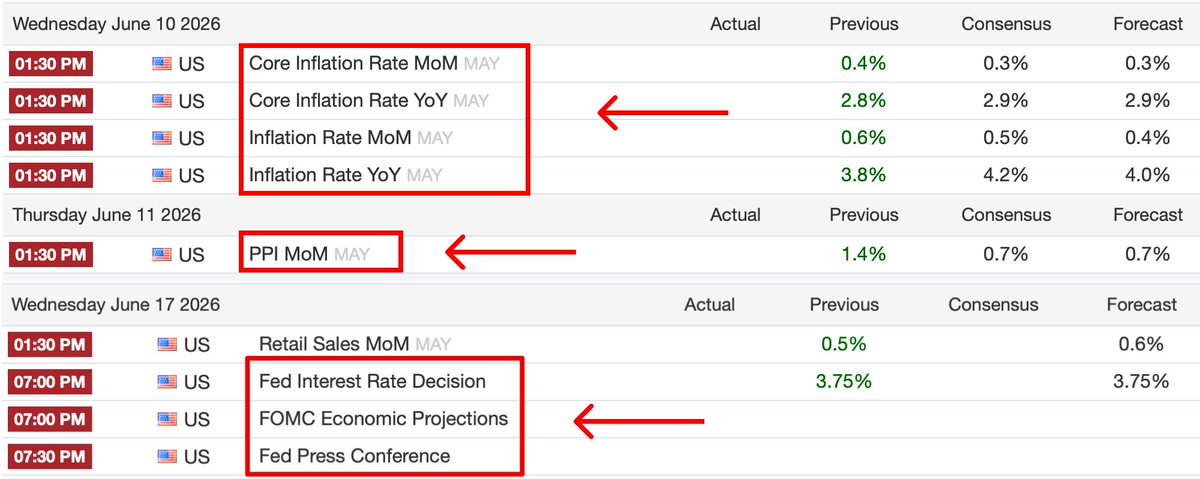

The US CPI data is coming out today.

Tomorrow, inflation from the producer's side.

The week after? FOMC along with the economic projections.

Risky assets like the S&P 500 and especially Bitcoin are going to be volatile.

12

47

150

14,355

Jun 10

The SpaceX IPO is one of the biggest stories in markets right now, and ethereum:0xb2617246d0c6c0087f18703d576831899ca94f01 lets you get exposure to it.

Created by Valora Finance, curated by ZIG Markets, powered by Ondo Finance. This one is worth paying attention to.

Jun 10

SpaceX exposure on @ZIGChain!

- Created by @Valdora_finance

- Curated by ZIG Markets

- Powered by @OndoFinance

- Value driven back to ethereum:0xb2617246d0c6c0087f18703d576831899ca94f01

Because, nothing compounds alone :)

9

28

150

14,961

Jun 10

$BTC 2021 and 2025 are the same chart. Double top, RSI divergence, red consolidation box, EMA 50 lost, and RSI now at 32.

In 2022 this red box was the last stop before the greatest accumulation zone in crypto history.

44

29

146

14,834

Jun 10

$MORPHO bounced hard off the blue support zone, broke out of the descending channel, and is reclaiming EMA 200. The red zone at $2.35 is next.

40

37

139

16,244

Jun 10

As bullish as I am on $HYPE, I can't lie, things are not looking good right now.

Price is forming a very clean head and shoulders pattern. It's mostly getting dragged by the broader market.

Based on the 1.618 Fibonacci level, $50 might be next.

40

37

168

16,176

Jun 10

The US CPI data is coming out today.

Tomorrow, inflation from the producer's side.

The week after? FOMC along with the economic projections.

Risky assets like the S&P 500 and especially Bitcoin are going to be volatile.

Jun 9

Last Friday, the S&P 500 experienced its biggest single-day loss of 2026. And funny enough, it was actually because of good news. Let me explain.

Last week, multiple US job reports came out, all beating consensus and forecasts by a wide margin, which reflects that the US economy is still going strong.

The NFP data came in at 172K, doubling the consensus estimate of 85K.

The problem is, a big reason why the Fed started cutting rates was because the job market was deteriorating. "Downside risks to employment have risen," as stated in the September 2025 FOMC statement.

With a strong job market report, there's no reason for the Fed to cut rates again.

This sparked a massive sell-off in risky assets like the S&P 500 and, in turn, Bitcoin.

So, to see a global risk-on mode once again, we need inflationary and growth data to come in soft.

16

30

152

11,941

Jun 9

With @OKX X-Perps you can rotate between crypto, stocks and commodities all from one place.

Been using it to move into NVDA and gold when crypto has been slow. No need for broker switching or extra accounts.

Long or short, up to 10x, 24/7.

20

44

171

35,283

Jun 9

Worth checking out the quoted post if you want to learn more

x.com/okx/status/20642883570…

8

17

4,716