Investing📈| Building an early retirement portfolio💰| Not financial advice |

Joined December 2023

- Tweets 41,254

- Following 361

- Followers 4,274

- Likes 37,931

2,823 Photos and videos

Pinned Tweet

May 30

$TMDX earnings “miss”

Many investors looked at $TMDX’s latest earnings and saw margin pressure, higher costs, and weaker profitability.

What they missed is that these results largely reflect aggressive investment to expand a future opportunity, not evidence of a deteriorating business.

For years, $TMDX has been transforming from a traditional medical device company into a logistics-enabled healthcare platform.

That shift comes with higher fixed costs, heavier capital requirements, and lower reported margins today but it unlocks a market that simply couldn’t be addressed through the legacy organ transplant infrastructure.

Organs die if you go slow. The logistics network is the moat.

This is a playbook we’ve seen before.

The best compounding businesses sacrifice current profitability to build scale and lock in competitive position. The accounting looks worse before the economics get better.

The mistake many investors make is evaluating $TMDX on reported earnings without adjusting for the growth investments embedded in those numbers.

Today that includes:

• OCS 2.0 development and trial enrollment

• CHOPS cold perfusion development and regulatory approvals

• OCS Kidney trials targeting a 2027 launch

• International expansion beginning in Italy

• Building a European NOP network, including a strategic investment in a German aviation company

• A new Boston headquarters

Every one of these carries upfront costs with little or no immediate revenue contribution. They pressure margins, earnings, and EPS today while laying the groundwork for future growth

That investment showed up clearly in Q1 2026.

$TMDX is now building its European platform, replicating the infrastructure that drove adoption in the U.S.

Rather than repeating its early reliance on costly third-party aviation providers, management is vertically integrating key logistics capabilities from the outset through long-term lease arrangements.

These obligations appear as liabilities on the balance sheet, but economically they are investments in the infrastructure required to serve a much larger market.

Meanwhile, heart, lung, and kidney programs are absorbing R&D expense today while much of the revenue opportunity remains ahead.

As volumes scale, those costs should be spread across a larger revenue base, improving utilisation, margins, and returns on capital.

Fuel costs and other short-term operating pressures are noise. They may affect quarterly results, but they do little to alter the long-term thesis.

The market is focused on today's earnings.

The opportunity lies in understanding what those earnings are being sacrificed to build.

6

826

Ceres Power $CRW.L operates an asset light licensing model built around its proprietary solid oxide technology.

Rather than manufacturing fuel cells or electrolysers itself, Ceres develops and owns the intellectual property, then licenses it to large industrial partners that manufacture, scale and commercialise the products globally.

This approach creates a highly scalable business model. Ceres avoids the heavy capital expenditure associated with building factories, instead generating revenue through licensing fees, engineering services and, ultimately, royalties on partner production. As a result, the company has historically maintained gross margins of 70-80%.

The timing looks increasingly interesting as two major demand drivers begin to converge: AI data centres requiring reliable, low emission power generation, and industrial decarbonisation driving demand for green hydrogen.

Some of Ceres Power’s most important commercial partners and customers today include:

> Doosan Fuel Cell – The most advanced commercial partner. Doosan has begun mass production of fuel cell stacks based on Ceres’ technology and generated Ceres’ first royalty revenues in 2025.

> Delta Electronics – Developing solid oxide fuel cell systems, including applications for distributed power and data centres.

> Shell – Collaborating on solid oxide electrolyser technology for green hydrogen production.

> Denso – Developing solid oxide fuel cell products for power generation applications.

> Thermax – Licensed Ceres technology for decarbonisation and distributed energy applications in India.

Ceres’ technology platform consists of two core products:

> Solid Oxide Fuel Cells (SOFCs), which convert fuels such as hydrogen, natural gas and biofuels into highly efficient electricity and heat, making them well suited for distributed and behind-the-meter power generation.

> Solid Oxide Electrolyser Cells (SOECs), which use electricity to split water and produce green hydrogen. Ceres claims its SOEC technology can achieve hydrogen production at approximately 37 kWh/kg, around 30% more efficient than incumbent lower-temperature technologies.

Recognising the growing energy demands of AI infrastructure, Ceres began actively marketing its SOFC technology to the data centre market in mid-2025 as a potential solution for providing reliable on-site power.

The business model follows a phased revenue structure. Partners initially pay engineering and development fees during joint technology programmes, followed by substantial upfront licence and technology transfer payments. The final and most valuable stage is recurring royalties, where Ceres receives ongoing payments for every unit or megawatt of capacity its partners manufacture and sell.

This royalty layer is where the long-term investment thesis becomes most compelling.

Ceres generated its first royalty revenue in 2025 as Doosan commenced mass production of fuel cell stacks in South Korea.

However, management has cautioned that royalty revenues are likely to remain modest through 2026, with more meaningful contributions expected from 2027 onwards as manufacturing volumes scale.

The potential upside is significant. Management has indicated that a single partner producing 1 GW of annual capacity could generate £50-100 million of annual royalty revenue for Ceres.

The opportunity is clear: an asset-light technology company with industry-leading efficiency, exposure to AI power demand and hydrogen growth, and a business model that becomes increasingly attractive as partners move from development into mass production.

The key risk is equally clear. Ceres’ success is heavily dependent on the execution, deployment timelines and commercial success of its partners. The royalty engine exists, but investors are still waiting for it to reach scale.

144

Jun 12

Big W to whoever changed the Spotify app back🫶🏼

That disco ball was annoying as hell 💀

151

Jun 10

Very interesting!

Jun 10

Visa and OpenAI are expanding their partnership to let AI agents make online purchases after user permission.

$V payment services will be integrated into OpenAI’s platform so retailers can accept agent-driven transactions.

Visa says the goal is trusted, secure, and seamless payments as AI agents become active participants in commerce.

2

198

Jun 10

Choosing to pay almost 3x the amount of money for Gordon instead is pretty wild

Jun 10

🚨 BREAKING: Barcelona will NOT pay €30m buy option clause for Marcus Rashford, expiring in 5 days.

Rashford formally set to return to Man United but Barça remain open to new solutions, like another loan deal. ❗️

Barça are open to discuss again if #MUFC open doors. 🔵🔴

3

226

Jun 10

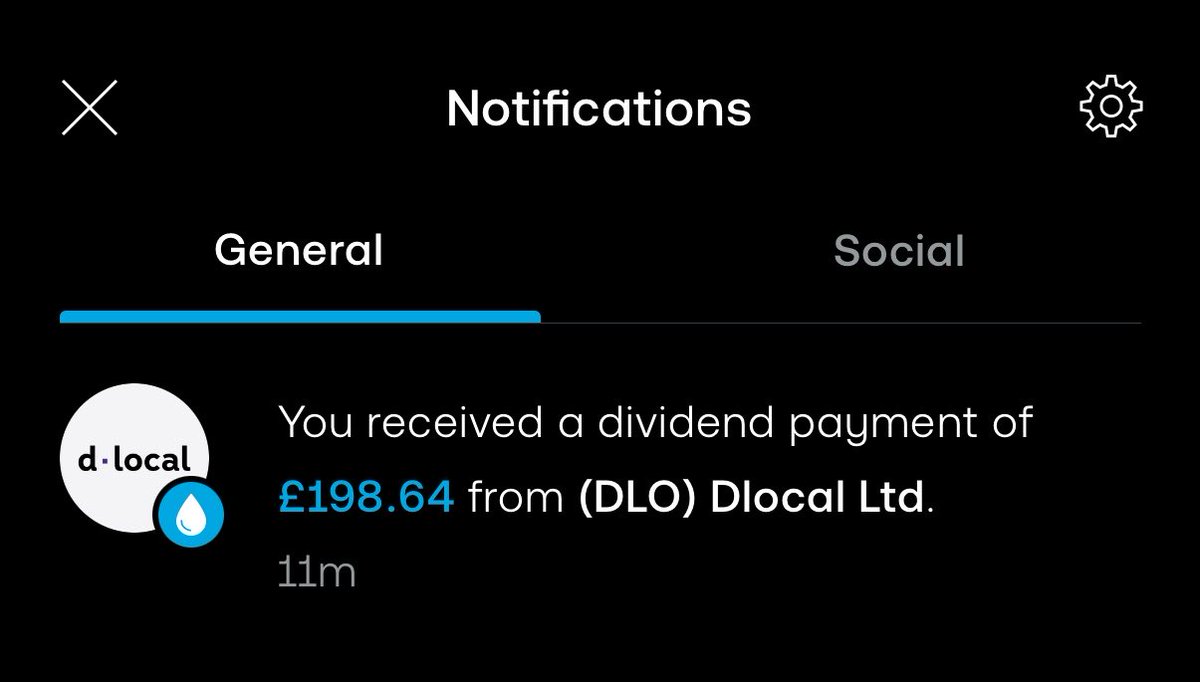

Dividend day compliments of dLocal $DLO

£198.64 - which will be reinvested back into the portfolio - compounding away 📈💷

1

5

433

Jun 10

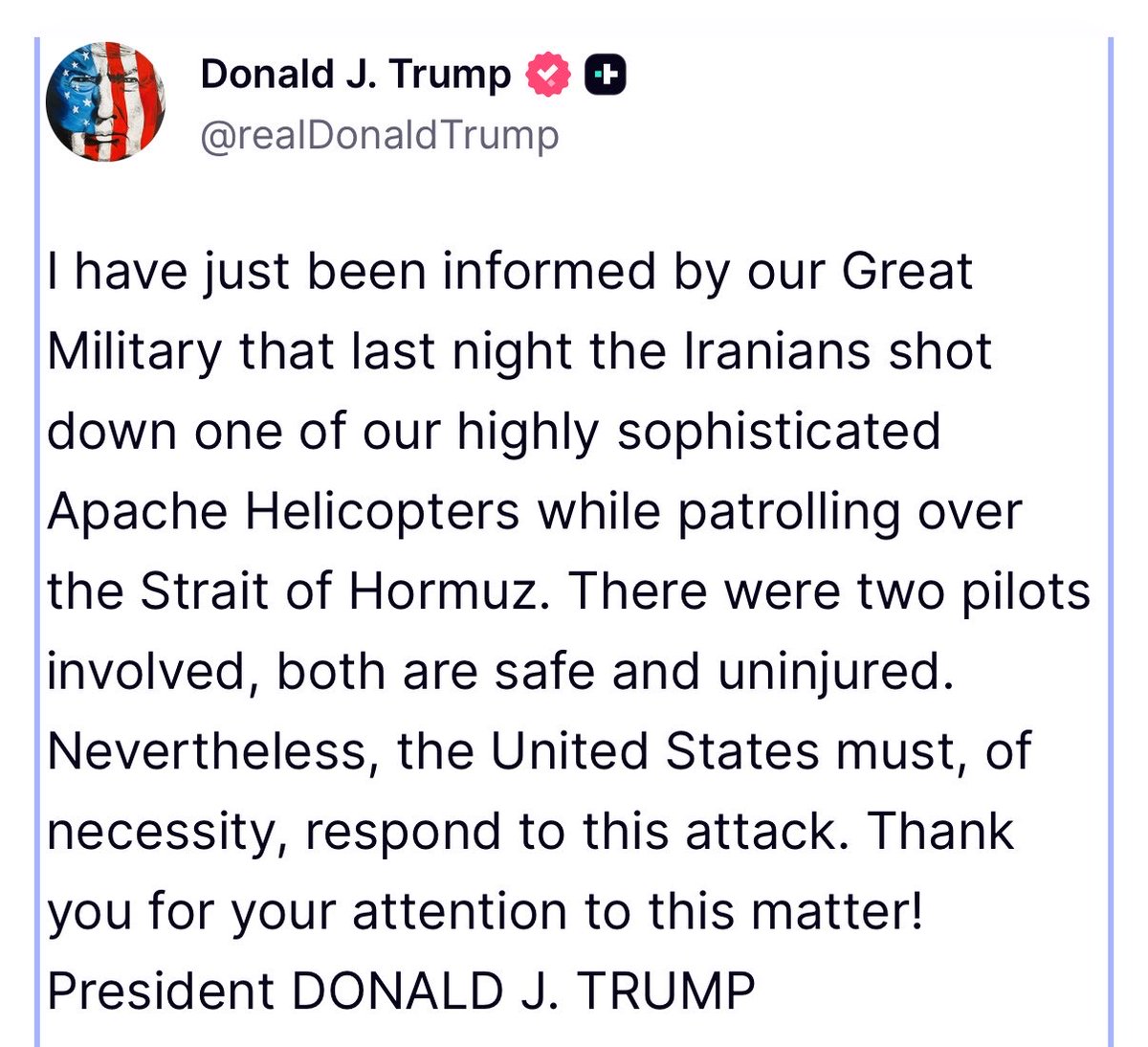

BREAKING: President Trump says Iran has taken too long to negotiate a deal and “now they will have to pay the price.”

1

142

May 29

A great end of the week with $ZETA my largest position closing the day 13%😎

Just getting started!!🚀

Have a great weekend all🫶🏼

2

17

735

May 29

$INV press release

Innventure is aware of a recent short seller report about the Company which contains selective and misleading interpretations that do not fairly reflect the facts of Accelsius’ technology, the nature of its customer engagement or Innventure’s broader business strategy. Innventure strongly disagrees with the report’s characterization, as its business and technologies have been validated by leading multi-national corporations and it maintains robust processes in connection with vetting potential customers, transactions and pipeline coverage. The Company remains focused on driving growth across its operating companies and building long-term shareholder value. Innventure is committed to maintaining a high level of transparency and will continue to constructively engage with shareholders and communicate material developments through SEC filings and other authorized disclosure channels.

1

748

May 29

This is insane.

🤯

May 29

BREAKING: 🇳🇱 The Netherlands just approved a 36% tax on unrealized gains.

Your Bitcoin goes up on paper.

You didn't sell. You owe 36% anyway.

Stocks, bonds, crypto, all of it.

Taxed every year on gains you haven't even cashed in.

No country on earth does this. The Netherlands wants to be the first.

This is how you make capital leave.

142

May 29

$ZETA having a strong end of the week

Up 10% today and 23% over the last week🟢

Still another ~40% to go before it reaches current fair value though😃

LFG🚀

1

7

314

May 29

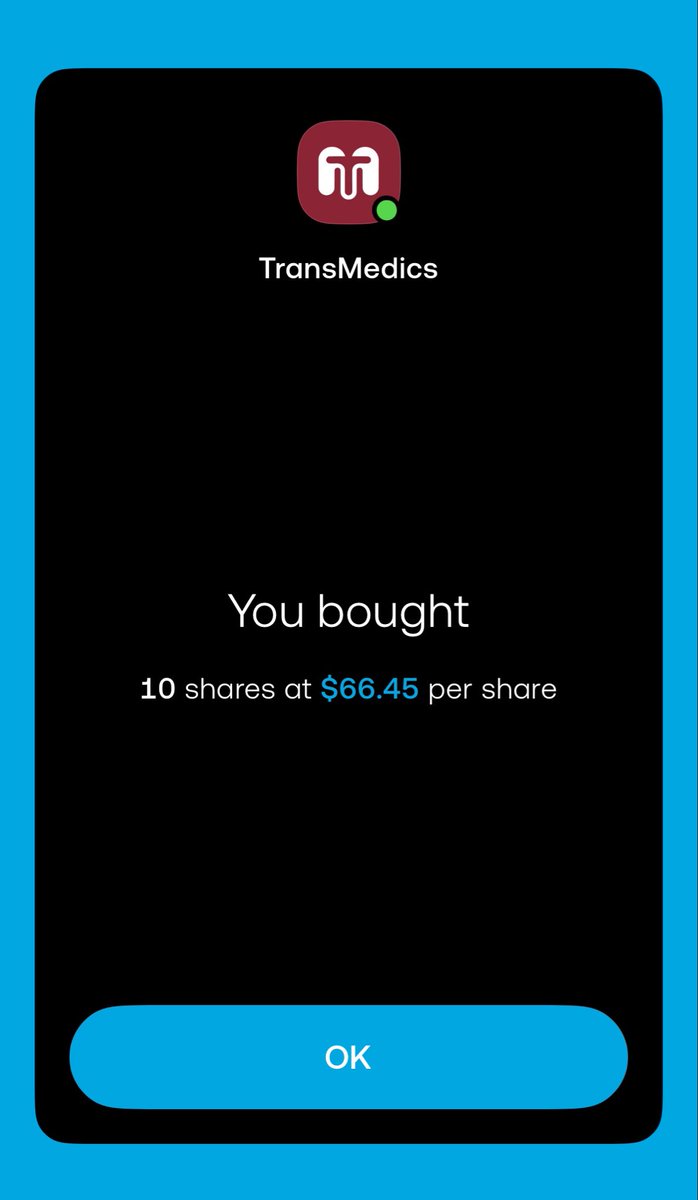

First payday buy locked in🔒

10 shares of $TMDX @ $66.45 per share

What have you been buying lately?

1

378

May 28

Is this a typo? Damn $DELL crushed it

May 28

$DELL Q1’27 EARNINGS HIGHLIGHTS

🔹 Revenue: $43.8B (Est. $34.81B) 🟢; 88% YoY

🔹 Adj. EPS: $4.86 (Est. $2.88) 🟢; 214% YoY

🔹 AI-Optimized Servers Revenue: $16.1B; 757% YoY

FY Guide:

🔹 Revenue: $165.0B-$169.0B (Est. $143.9B) 🟢; 47% YoY

🔹 Adj. EPS: $17.90 (Est. $13.16) 🟢; 74% YoY

🔹 AI-Optimized Servers Revenue: ~$60B; 144% YoY, up from ~$50B

Q2 Guide:

🔹 Revenue: $44.0B-$45.0B (Est. $35.4B) 🟢; 49% YoY at midpoint

🔹 Adj. EPS: $4.80 (Est. $3.01) 🟢; 107% YoY

Segment Performance:

🔹 ISG Revenue: $29.0B; 181% YoY

🔹 AI-Optimized Servers Revenue: $16.1B; 757% YoY

🔹 Traditional Servers & Networking Revenue: $8.5B; 92% YoY

🔹 Storage Revenue: $4.3B; 8% YoY

🔹 ISG Operating Income: $3.1B; 206% YoY

🔹 CSG Revenue: $14.6B; 17% YoY

🔹 Commercial Client Revenue: $13.0B; 18% YoY

🔹 Consumer Revenue: $1.6B; 9% YoY

🔹 CSG Operating Income: $1.2B; 79% YoY

Financials:

🔹 AI Orders: $24.4B

🔹 Operating Cash Flow: $4.1B; 46% YoY

🔹 Operating Income: $3.656B; 214% YoY

🔹 Non-GAAP Operating Income: $4.235B; 154% YoY

🔹 Net Income: $3.438B; 256% YoY

🔹 Adjusted FCF: $3.165B; 42% YoY

Capital Return:

🔹 Shareholder Returns: $2.1B through repurchases and dividends

Commentary:

🔸 “Our record Q1 performance reflects strong in-quarter demand, as well as our pace of innovation across the full stack of PCs, compute and storage.”

🔸 “We booked $24.4 billion in AI orders and recognized $16.1 billion of AI server revenue.”

🔸 “We’re increasing our AI server revenue expectations for FY27 to $60 billion, which only goes to show the AI opportunity shows no signs of slowing.”

🔸 “We entered FY27 with clear momentum, raising our full-year revenue outlook to $167 billion at the midpoint, up nearly 50% year over year.”

1

2

276

May 28

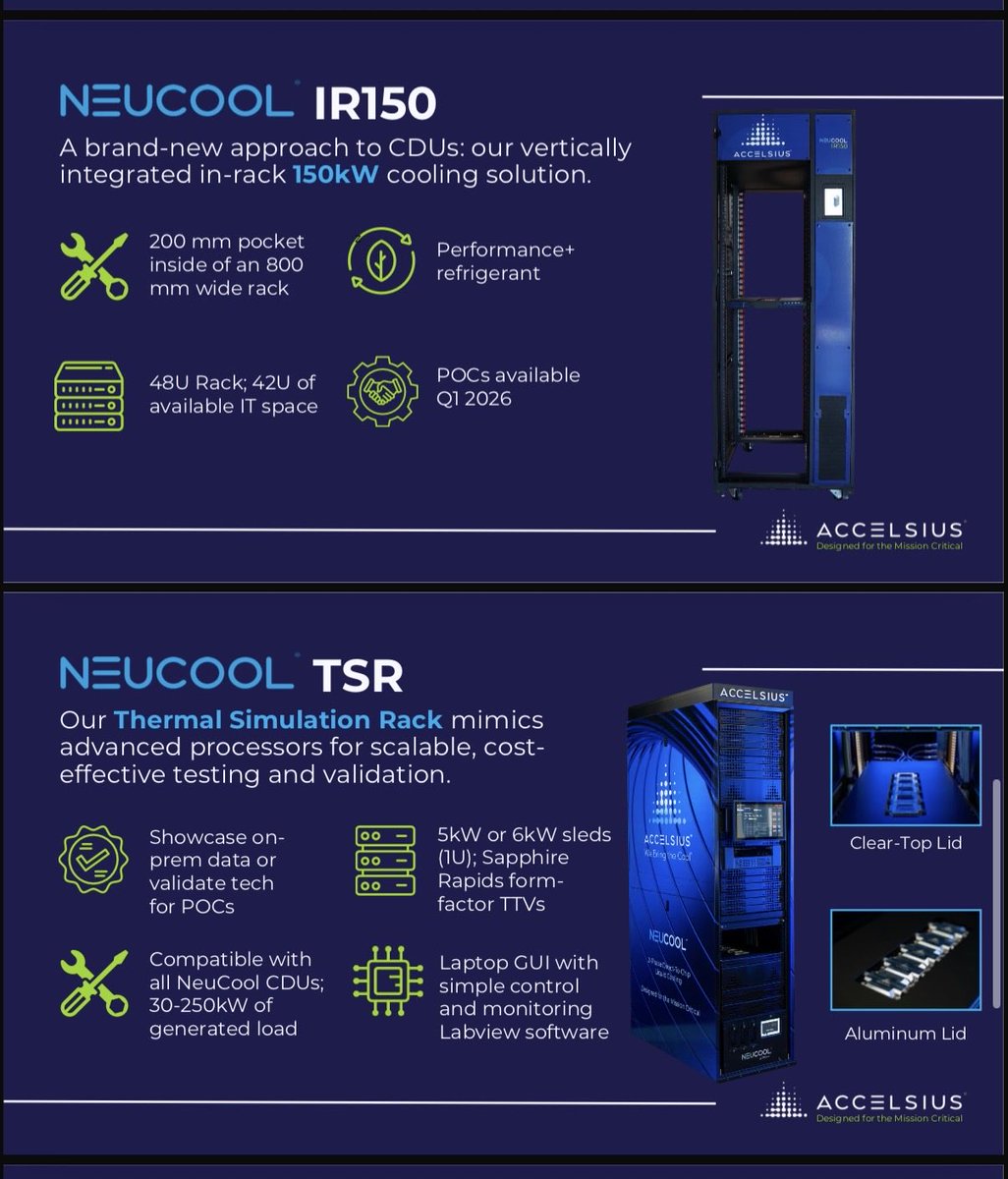

$INV — Innventure, Inc.

A listed vehicle giving you exposure to Accelsius, a private AI data centre cooling company, at a discount to its own private market valuation.

Accelsius was founded by Innventure in June 2022. It specialises in two-phase, direct-to-chip liquid cooling for AI and HPC data centres, its proprietary NeuCool platform can handle over 4,500W per socket using safe, low-pressure dielectric refrigerants.

Traditional air cooling consumes up to 40% of a data centre’s power. That model is breaking down under modern GPU loads. Two-phase liquid cooling is the fix.

In December 2025, Accelsius closed a $65M Series B led by Johnson Controls and Legrand — valuing the business at ~$665M post-money.

Crucially, that valuation was set by two global industrial companies deploying their own capital. Not a VC. Not a financial sponsor.

$INV’s market cap today is ~$510M.

The entire listed company — including subsidiaries and cash — is being valued below the implied worth of its Accelsius stake alone.

The latest quarterly earnings show the commercial ramp is real:

• $50M in new Accelsius bookings in Q1 2026 — production volume orders, not pilots

• $100M annualised revenue run rate targeted by December 2026

• Cash flow positive expected by year-end

Revenue was only $1.6M in 2025. The inflection is happening now.

The discount exists for legitimate reasons, which is worth being honest about:

• INV has funded itself via convertible debentures, SEPAs and equity placements, dilution is real

• Needs ~$50M over the next 12 months to execute

• Material weaknesses in internal controls flagged

Governance has been messy. That’s the gap.

But activist pressure is forcing the cleanup.

Two 13Ds landed in February 2026 — Commonwealth Asset Management and Ascent Capital — both calling for overhead cuts, board refreshment, and capital focused on Accelsius.

By May, G&A was down 35% YoY. New independent directors appointed.

The conglomerate discount isn’t just a drag, the other subsidiaries represent additional upside if you think the model works:

AeroFlexx — sustainable flexible packaging. $400B TAM, nearly $30M near-term pipeline with ~⅓ in final negotiations, four anchor customers signed.

Refinity Olefins — converts mixed plastic waste into circular hydrocarbons and sustainable aviation fuel. Early stage but addressing a massive global waste problem with growing regulatory tailwinds.

Neither is Accelsius. But both could be meaningful at scale — and right now, the market is pricing them at essentially zero.

Innventure’s precedent: it previously founded PureCycle, grew it to an $835M pre-market valuation in under 7 years, and took it public via deSPAC at $1.2B post-money — a 26.8x return for early investors.

Bull: Accelsius hits $100M run rate, reaches cash flow positive, moves toward IPO or Series C at a step-up valuation. Governance improvements reduce the conglomerate discount. AeroFlexx pipeline converts. INV re-rates.

Bear: Dilution continues to erode per-share value before the ramp materialises. Competition from Schneider Electric intensifies. Corporate overhead remains excessive. INV’s Accelsius stake shrinks with each future raise.

This is not a clean business. The vehicle is messy, the dilution risk is real, and execution still needs to be proved at scale.

But the underlying asset is genuinely compelling and right now you can buy it below private market value with activists already pushing for the changes needed to close the gap.

Not financial advice. DYOR.

7

700

May 28

Damn no love shown for $TTD by Rothschild

May 28

Rothschild Redburn initiated The Trade Desk at Sell with an $11 price target, implying ~50% downside.

The firm argues $TTD's position as only one link in the ad supply chain is being pressured by three forces:

1. Walled gardens’ AI-based media tools

2. Amazon’s discounted programmatic buys

3. Agencies building agentic buying platforms and going more direct with SSPs

Rothschild expects market share loss and/or take-rate compression that is not yet reflected in consensus.

1

612