Joined April 2020

- Tweets 1,645

- Following 18

- Followers 113

- Likes 353

717 Photos and videos

Pinned Tweet

31 Dec 2025

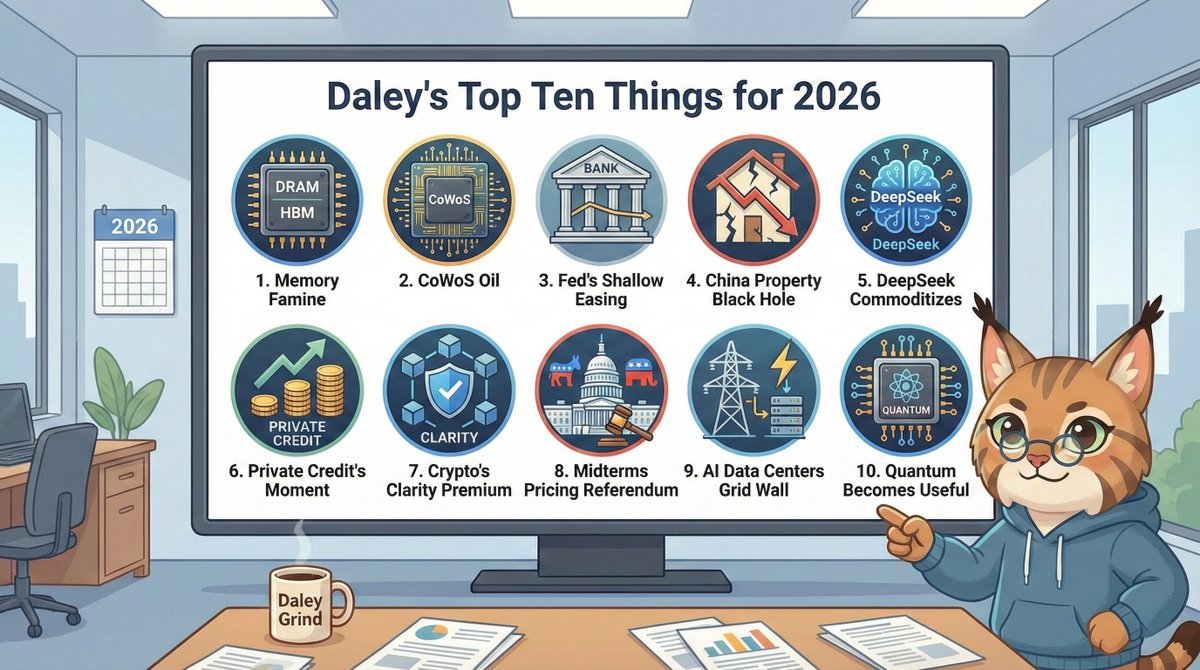

😼Daley's Top Ten Things to Happen in 2026

Welcome to the year when liquidity meets lithography, when tariffs collide with terabytes, and when the gap between what CNBC tells you and what actually matters becomes a chasm you can measure in billions.

While talking heads debate whether the S&P hits 7,200 or 7,500, the real story of 2026 is being written in wafer fabs, packaging lines, and the quiet offices where sovereign wealth allocators decide which nation-states get to build the future.

Let me show you where the leverage actually lives.

1) The Great Memory Famine

AI HBM demand keeps DRAM supply “significantly below demand” through at least 2027, forcing PC/phone OEMs to eat higher memory costs or cut specs, and making secured memory contracts a real competitive moat.

2) CoWoS as the New Oil

TSMC’s CoWoS capacity rises to 100k wafers/month by end-2026, but demand still requires roughly a 3x capacity jump, leaving Nvidia and a handful of hyperscalers with a structural packaging advantage while everyone else fights for scraps.

3) The Fed’s Shallow-Easing Regime

Goldman and BofA both see two cuts in 2026 toward a 3–3.25% terminal rate, while the Fed’s own dots only show one cut, locking in a higher-for-longer cost of capital that exposes stretched equity valuations.

4) China’s Property Black Hole

With home prices projected to fall another 2.8% in 2026, inventory in lower-tier cities at ~40 months, and local government debt near $18.9T (~100% of GDP), China’s housing bust quietly morphs into a long-tail sovereign and growth drag.

5) DeepSeek Commoditizes the Model Layer

DeepSeek’s V3.2 models match or beat GPT-5/Gemini-class systems on tough maths and coding (e.g., 96% AIME, IMO gold-caliber performance) at far lower training cost, accelerating the shift of value from proprietary models to infra and distribution.

6✋) Private Credit’s Late-Cycle Moment

With AUM heading toward $1.7T and an addressable market north of $30T, private credit floods the wealth channel even as rating agencies slap a negative outlook on 2026 due to margin compression and rising leverage.

7🤚) Crypto’s “Clarity Premium”

CLARITY plus GENIUS Acts and an SEC “innovation exemption” pivot crypto from regulation-by-enforcement to rulebook-integration, making regulated stablecoins and tokenized assets the institutional on-ramp while the unregulated fringe gets structurally discounted.

8) Midterms as a Pricing Referendum

Trump frames 2026 around “pricing,” but with Democrats holding a ~5.3% generic-ballot lead and his approval stuck at 15–29% among key blocs, odds tilt toward a Democratic House flip and two years of market-favored legislative gridlock.

9) AI Data Centers Hit the Grid Wall

U.S. data-center power demand climbs from 176 TWh in 2023 to 325–580 TWh by 2028, pushing usage to 6.7–12% of U.S. electricity and making power contracts, grid access, and storage/nuclear exposure as critical as GPU access.

10) Quantum Computing Becomes Actually Useful

With the market on track for $20.2B by 2030 (41.8% CAGR) and real deployments like 34% better bond-trading predictions and drastic scheduling gains, 2026 marks the pivot from lab demo to ROI case study, especially where quantum and AI co-pilot each other.

3

639

2h

The Half-Life benchmark on ReactOS is being celebrated as a gaming milestone.

It is actually a sovereign infrastructure story dressed in a Valve game from 1998.

Let me connect some dots.

The global push for sovereign AI is generating enormous capex conversations around data centers, compute, and energy. Everyone is focused on the hardware layer, chips, racks, cooling, power. That is correct and the infrastructure bull thesis is intact.

But sovereign AI without sovereign OS is a house with bulletproof walls and a screen door.

You cannot have a truly independent national compute stack if the operating system kernel is licensed from a corporation headquartered in Redmond, subject to US export controls, subject to US sanctions policy, subject to Microsoft's product roadmap decisions.

This is not hypothetical. Ask any sanctioned nation-state trying to run Windows Update right now.

ReactOS achieving DirectX hardware acceleration on real silicon is the open-source community proving that the OS layer is not a permanent monopoly. It is an engineering problem with an engineering solution.

The funding implication is obvious once you see it.

Some government, probably not American, is going to look at what ReactOS volunteers accomplished with no budget and ask

1

18

6h

Let me translate "fixed annuities can outperform the market" into plain English.

Under specific, cherry-picked, historically rare conditions, during a brutal multi-year equity drawdown, a fixed annuity's guaranteed 3-4% does beat a portfolio sitting in cash-equivalent panic mode. That is the data point these seminars are built on. One true sentence surrounded by an ocean of omission.

The omission is the entire game.

Fixed indexed annuities, the product most commonly pushed at these events, come with participation rates, spread fees, and annual caps. You might hear "linked to the S&P 500." What you do not hear is that your upside is capped at 6-8% in a year the index returns 26%. Your "participation" in good markets is surgically limited. Your exposure to insurance company solvency risk is total.

The compounding math is brutal over time.

A 65-year-old putting $500K into a fixed annuity versus a boring 60/40 portfolio does not need exotic modeling to see the outcome. Drag the assumptions out to age 85 and the gap is generational wealth versus adequate income. The annuity buyer is not poor. They are just meaningfully less wealthy than they could have been.

Here is what nobody in that banquet room says out loud.

Insurance companies are not charities. They pool your premium, invest it in investment-grade corporate bonds and yes, private credit and CLOs, earn a spread above what they credit you, and keep the difference as profit. You are the raw material. The insurance company is the carry trade.

That carry trade funds the steak.

The genuinely useful version of this conversation is about sequence-of-returns risk. If you retire in 2000 or 2008 and draw down aggressively in year one of a crash, the math on your portfolio never fully recovers. That is a real problem. Annuities as a partial solution to that specific problem, covering baseline fixed expenses so you never have to sell equities at the bottom, that is legitimate financial planning.

But that nuanced, boring, fee-only conversation does not require a free dinner.

The ribeye is always the tell. Commission-based salespeople disgu

11

10h

Political journalists are calling this a contradiction.

Macro traders should call it a regime signal.

Here is the actual information embedded in this Iran episode.

The White House has a principal-agent problem so severe that it cannot maintain message coherence on a nuclear negotiation for a week.

That is not a communications failure. That is an organizational failure at the command level of the most consequential foreign policy apparatus on earth.

Now run that insight through the lens of every other open negotiation on the board.

US-China trade framework. NATO burden-sharing. Gulf security guarantees. South Korea and Japan extended deterrence conversations.

Every single one of those counterparties just updated their models.

Not because Iran is the center of the universe. But because this contradiction reveals the variance around any given Trump administration signal is extremely wide.

Wide variance on superpower commitments means counterparties demand a risk premium.

That risk premium shows up in commodity prices, in sovereign bond spreads, in the cost of writing long-dated infrastructure contracts that depend on geopolitical stability assumptions.

Data center developers doing 20-year power purchase agreements in the Middle East just got a new line item in their risk models.

Sovereign AI buildouts in the Gulf that depend on implicit US security guarantees just got a new discount rate applied to them.

The Iran contradiction is not a one

50

14h

Everyone is building AI agents.

Nobody is talking about the interface layer that actually makes them useful.

Telegram is quietly becoming the most underrated enterprise operating system on the planet. Not because of the app. Because of the bot API. It is persistent, cross-device, notification-native, and frankly more reliable than half the SaaS dashboards charging you $400/month for a pretty chart.

I consolidated 13 agents into one bot. Sales alerts. Deploys. Finance summaries. Approval flows.

My entire company command center fits in a chat thread.

The real insight here is not "Telegram is cool." The insight is that the abstraction layer above AI agents is the actual product now. The agent itself is commodity infrastructure. The interface that lets a solo operator or a lean team command that infrastructure from anywhere, at any time, with zero friction, that is where the value accrues.

Legacy SaaS never solved this. They gave you dashboards that required a laptop, a login, and a moment of focused attention.

Agentic chat interfaces require none of that.

The bathroom is not a joke. It is the proof of concept. If your operational stack runs cleanly on a phone in a 90-second window, your cognitive overhead is genuinely low. That is a competitive advantage most funded startups with 40-person ops teams do not have.

Where are you running your company from?

30

18h

The Goldman-SpaceX headline is getting the wrong treatment everywhere.

Reporters are writing about the fee. Investors should be reading the subtext.

When Goldman locks up the lead left role on an asset this singular, it reshapes their relationships across every sovereign wealth fund, every family office, and every institutional allocator they cover globally. This is not a transaction. This is a decade of deal flow leverage wrapped in one mandate.

SpaceX is also the clearest example of a company that broke the traditional IPO

15

22h

Everyone is treating the Warsh Fed like it's just Powell with a different face.

That is the single most dangerous assumption in markets right now.

Warsh was the loudest institutional critic of QE when QE was religion.

He wrote the dissents nobody wanted to read.

He watched the Fed balloon its balance sheet and called it what it was: a fiscal transfer dressed up as monetary policy.

That ideological DNA does not disappear when you sit in the chair.

The market is pricing a dovish pivot because it always prices a dovish pivot.

Pavlov's traders, every single time.

But Warsh has a credibility problem that is actually an opportunity for him.

He needs to prove the Fed is not a White House instrument.

The easiest way to do that is to hold longer than anyone expects.

Inflation is not dead.

Services sticky, shelter re-accelerating, fiscal impulse still loose.

The 10-year is telling you something the front end refuses to admit.

A Warsh Fed that defends the institution's independence means one thing for your portfolio: duration is a trap, credit spreads are too tight for what's coming, and the "soft landing" consensus is trading at a valuation that assumes perfection.

Nothing in macro trades at perfection for long.

Fade the pivot narrative until Warsh gives you an actual reason not to.

#macro

51

Jun 13

A confession from someone who watches macro data for a living.

The most dangerous thing in markets right now is not the yield curve. It is not tariff escalation. It is not even the shadow inventory of stressed CRE debt sitting on bank balance sheets waiting for refinance cliffs.

The most dangerous thing is your news feed.

Here is a number worth tattooing somewhere: 68%. That is the historical frequency with which US equities close a calendar year in positive territory. Not cherry-picked. Not adjusted. Raw

9

Jun 13

The Iran sanctions story has a second-order effect nobody is talking about loudly enough.

If this blockade actually bites, and the evidence is mounting that it is, you do not just remove Iranian barrels from the market. You accelerate a reordering of how China thinks about energy security architecture going forward.

Beijing has been quietly building out long-term supply relationships with Gulf producers, Russian pipeline capacity, and domestic upstream development precisely because the Iran channel was always structurally fragile. A serious enforcement cycle just turbocharges that diversification spend.

That is medium-term bullish for anyone exposed to energy infrastructure investment in non-sanctioned geographies. Saudi Aramco upstream JVs, Russian ESPO pipeline volumes, Kazakh transit through alternative corridors. The capital will find a path.

For Tehran the math is genuinely brutal right now.

Iran needs oil revenue to fund imports, to subsidize domestic fuel, to service whatever internal financial obligations keep the political structure intact. There is no obvious substitute revenue stream. The regional influence budget, the proxy network financing, all of it runs through oil dollars. Fiscal compression here is not abstract, it is a direct input into regional stability calculations.

The sanctions-don't-work consensus was always lazy analysis. It conflated adaptation with immunity. Iran adapted brilliantly to every prior enforcement cycle. Adaptation is not the same as being unaffected. The cumulative damage has been severe and this cycle looks structurally different because the enforcement is hitting demand destruction and supply blockade at the same time.

That is a pincer movement. And Tehran does not

30

Jun 13

Here is the pattern that repeats every single infrastructure cycle.

Phase one: Everyone chases the flagship. Valuations go parabolic. FOMO capital floods in.

Phase two: The boring enablers quietly sign contracts nobody notices.

Phase three: The boring enablers re-rate violently when an analyst finally connects the dots in a 47-page initiation report.

Phase four: Retail discovers them and ruins the trade.

SpaceX has firmly entered phase one territory on the secondary market. The question for serious allocators is where phase two is happening right now in the public markets.

The answer is in the terrestrial infrastructure layer that makes the satellite economy actually function.

Starlink terminals need to be manufactured at scale. The supply chain for phased array antennas is not infinite. The companies that cracked the manufacturing process for affordable flat-panel satellite receivers are sitting on an extraordinary competitive moat that the market is valuing like a legacy hardware business.

That is the disconnect.

The revenue profile looks like old hardware. The demand trajectory looks like early cloud. The market is using the wrong comparable.

When institutions start building Starlink ecosystem models and working backward through the supply chain, these names get discovered fast.

They are not discovered yet.

Low float, thin coverage, government contract visibility, and a secular demand driver that is just getting started across defense, maritime, aviation, and emerging market connectivity.

#Space

22

Jun 12

Everyone's melting down over the tape right now.

Stop. Pull up a longer timeframe.

Since 1950, the S&P 500 finishes positive roughly 68% of calendar years. That's not a bull case. That's base rate. That's the floor you're supposed to build conviction on before you even open your newsfeed.

The machine is designed to make you feel like this year is different.

It never is, until the one time it is, and you won't know which one that is until it's over anyway.

Here's what actually matters right now.

The narrative cycle is running at maximum velocity. Tariff headlines drop, futures gap down, permabears get 200k impressions, retail panics, institutions quietly accumulate at better basis. Repeat. This is not new. This is the playbook.

The people screaming loudest about macro catastrophe are also the people who missed the 2023 rally, the 2024 melt-up, and every other face-ripper that followed a wall of worry.

Your edge is not being smarter than the market.

Your edge is having a longer time horizon than the person on the other side of your trade, who is reacting to a Bloomberg alert they only half-understood.

The fiscal situation is genuinely messy. Twin deficits are real. Bond market vigilantes are sharpening their pitchforks. Private credit is doing things that would make a 2006 CDO blush.

None of that means you blow up your allocation because a headline scared you on a Tuesday.

Discipline is the alpha. Staying power is the alpha.

The 68% stat does not mean markets go up every year. It means the default assumption, before you have any other information, is that patient capital gets rewarded. You need a very high conviction reason to deviate from that prior.

Noise does not qualify as high conviction.

13

Jun 12

Hot take that will age well: gold at a 6-month low during an inflation scare is not a paradox.

It is a positioning flush.

Here is what actually happened. Funds that loaded up on gold as a geopolitical and inflation hedge through Q1 are now sitting on crowded longs. The moment rate hike talk re-entered the conversation, risk managers started trimming. Not because gold is wrong. Because the carry cost of holding gold versus yielding assets just got punishing again.

This is the structural trap gold always falls into. It has no yield. In a zero rate world it shines. The second the cost of capital rises, every institutional allocation model starts questioning the position size.

Meanwhile the dollar is catching a bid because rate differentials are moving in its favor. Gold and the dollar are roughly inversely correlated over any meaningful timeframe. You do not need to be a macro wizard to see where this goes when the DXY starts running.

The physical demand story out of central banks remains intact. That is the real long term bid under gold. But it does not matter in a tape like this. Flows eat fundamentals in the short run.

The trade is not to panic sell here. The trade is to understand what is actually driving this and stop reading inflation headlines as a gold buy trigger.

#gold

13

Jun 11

The silver trade is not complicated. The market is just choosing to ignore it.

Sovereign AI buildouts require massive grid expansion. Grid expansion requires transformers, cables, and inverters. Solar and wind capacity additions require photovoltaic panels. Every single one of those supply chains runs through silver offtake contracts.

Meanwhile the fiscal situation in the US is not improving. Twin deficits are structural, not cyclical. Real yields are capped politically even if not formally. That is historically the environment where monetary metals outperform everything except maybe energy.

Silver sits at the exact intersection of those two macro regimes.

Physical AI infrastructure buildout is a silver demand story. Dollar debasement risk is a silver demand story. Both are happening at the same time with no meaningful supply response on the horizon.

The gold-silver ratio is your positioning signal, not a chart pattern.

When that ratio compresses, it compresses fast and it compresses violently. Late entrants in that move get punished. The time to understand the thesis is before the ratio breaks, not after the headlines arrive.

$GOLD

36

Jun 11

Everyone screaming about inflation but selling gold.

That contradiction is not a paradox. It is a tell.

Here is what is actually happening. The market is pricing rate hikes, and rate hikes mean real yields climb. Gold pays nothing. When your alternative is a 5-handle on short duration paper, the opportunity cost of holding a inert yellow rock becomes very real, very fast.

This is the 2022 playbook running again in slow motion.

The retail crowd bought gold as an inflation hedge because that is what the YouTube permabulls told them. The institutional crowd is quietly exiting because they understand the actual driver is real rates, not CPI prints.

CPI up plus real yields up equals gold down. The math is not complicated.

What makes this moment genuinely interesting is the technical breakdown. When gold loses key support levels during a period of macro fear, it signals forced liquidation, not fundamental re-rating. Managed money was historically long. Those positions are now unwinding whether the funds want them to or not.

Margin calls do not care about your macro thesis.

The more contrarian read here is actually bullish for gold over a 12 to 18 month horizon. Central banks, especially in the Global South, are still accumulating physical at a pace that has no modern precedent. China, India, Poland, Turkey. These buyers do not trade on COMEX. They do not care about your 200-day moving average.

Sovereign accumulation is structural. COMEX liquidation is cyclical.

The paper market is setting a discount on the physical market. That spread eventually closes, and it never closes in the direction you think it will when you are caught short.

The real question is not why gold is down. The question is who is buying the dips at the sovereign level while Western funds panic-sell on a Reuters headline.

Watch the PBOC reserve data. Watch the RBI import numbers. That is where the actual signal lives, not in the daily spot price.

#gold

1

89

Jun 11

Trump just told the world he is comfortable with 4.2% inflation.

Most people heard a gaffe. Bond traders heard a policy signal. I heard a Fed independence funeral march.

Here is what nobody is connecting: Warsh does not need to crush inflation to 2% to look like a hawk. He just needs to look hawkish relative to where Trump set the new Overton window.

The 2% target was always a Volcker-era theological commitment dressed up as a technical benchmark. The moment a sitting president publicly reframes 4% as acceptable, the entire political calculus for the incoming Fed Chair shifts.

Warsh gets to run 3.5% and be celebrated as a disciplined steward of price stability.

That is not a small deal. That is a regime change disguised as a slip of the tongue.

The 10-year is not pricing this yet. Real yields are still anchored to a world where the Fed fights to 2% with religious conviction. If the terminal inflation target quietly migrates to 3.5% with bipartisan tolerance, every duration trade in the book gets repriced.

Pension funds are structurally short real assets. Endowments are overweight nominal bonds. Both get carved up in this scenario.

The dollar smile breaks down too. A Fed that is functionally comfortable with 3-4% inflation while the fiscal deficit runs at 6% of GDP is not a Fed that commands a safe-haven premium forever.

This is the de-dollarization catalyst people keep waiting for. It does not come from a BRICS announcement. It comes from a president saying 4.2% is fine on a Wednesday afternoon.

#macro

1

23

Jun 11

Hot money is not loyal to any asset class.

It is loyal to asymmetry. And right now crypto does not have the best asymmetry on the board.

Think about what made Bitcoin legendary as a trade. Thin institutional participation. Massive information asymmetry. Evangelical early adopters creating narrative pressure. A structural supply constraint baked into the protocol.

Now run that checklist against AI infrastructure.

Institutional participation in physical compute buildout: still early. Most generalist funds cannot even spell "colocation." Information asymmetry: enormous. The people who understand power procurement, cooling density, and GPU depreciation schedules are a tiny tribe. Evangelical early adopters: every hyperscaler CEO is now publicly committed to spending levels that would have sounded de

12

Jun 11

Most pharma services companies buy revenue and call it strategy.

Indegene did something rarer: they bought capabilities and let revenue follow.

There is a massive difference between those two things.

When you acquire revenue, you get a P&L boost, a press release, and an integration headache. When you acquire capabilities, you get compounding. Each new layer makes the existing stack more defensible, more sticky, more margin-accretive over time.

The pharma commercial stack is brutally complex. Medical, regulatory, legal sign-off. HCP engagement. Payer data. Launch execution. Digital content at scale. Most vendors own one slice and pray the client does not consolidate.

Indegene's move was to own the whole chain.

Start with execution. Prove you can deliver. Then walk up the value curve to strategy, where pricing power lives and switching costs become existential for the client.

That is how you go from vendor to infrastructure.

The market still prices most pharma tech and services businesses on near-term earnings multiples. It almost always underweights the compounding optionality that comes from owning a full commercial stack at a moment when every major pharma is under pressure to cut costs, accelerate launches, and do both simultaneously.

That tension, cut costs and go faster, is exactly the problem Indegene is architectured to solve.

Worth reading the full breakdown before forming a view.

1

72

Jun 11

The best trade in a vol spike is not what CNBC is telling you.

Every fast-money desk is buying optionality right now. Tail hedges, long straddles, VIX calls. The whole panic toolkit. And they are paying through the nose for it because supply has dried up and demand is vertical.

Someone has to sell that vol.

The sophisticated answer is to identify businesses with fortress balance sheets, recession-resistant revenues, and cash generation that is essentially mechanical. Utilities, certain defense primes, dominant infrastructure operators. Names where the fundamental volatility does not justify the options market pricing.

Sell covered calls. Sell cash-secured puts at levels you would genuinely own the stock. Run a wheel on something you actually want to own.

This is not a complex strategy. It is a discipline strategy.

The irony of a vol spike is that it simultaneously makes option buying feel urgent and option selling feel terrifying. That psychological inversion is the entire edge.

Khouw is not being contrarian for the sake of it. He is being rational while the market is being emotional.

Implied vol mean-reverts. It always has. The question is whether you are positioned to collect that reversion or pay for it.

Right now the crowd is paying. You do not have to be the crowd.

23