FCF per share | Slowly slipping down the quality spectrum

Joined June 2022

- Tweets 5,959

- Following 598

- Followers 4,703

- Likes 1,997

2,673 Photos and videos

Pinned Tweet

For compliance purposes, I’ll no longer be posting.

DMs open if you want to stay in touch, chat ideas, short theses that hinge on SBC/D&A accounting, best Lil Wayne mixtapes, etc.

Obligatory blurry pic of the dog

7

52

5,122

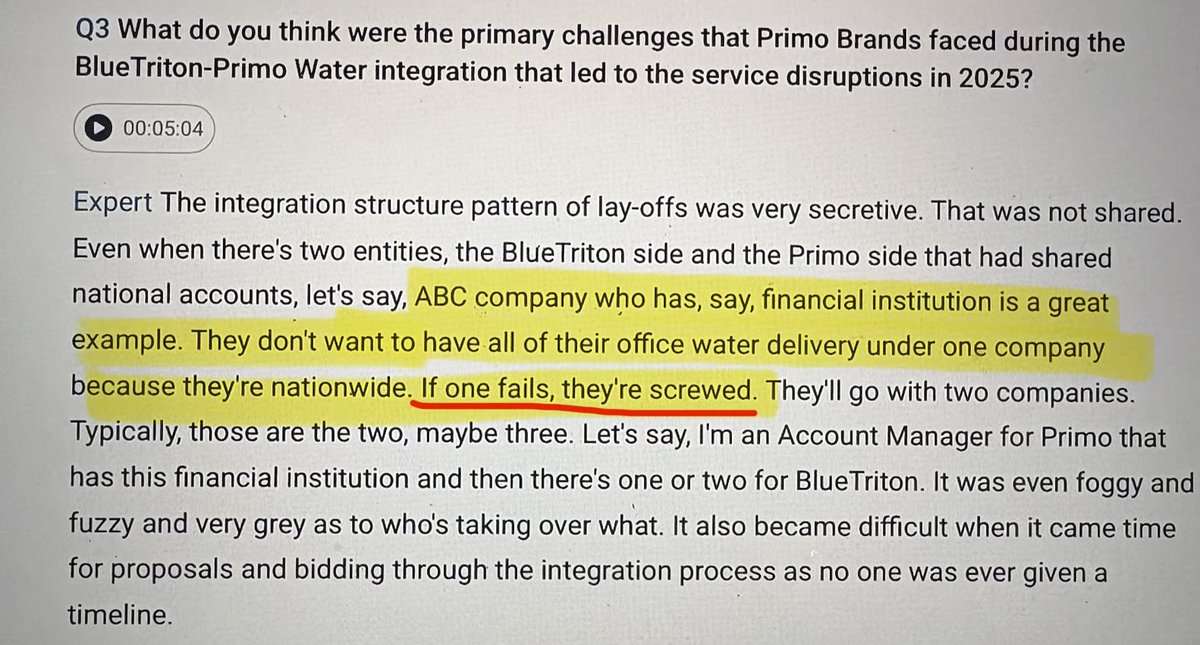

PRMB

Look, I’ve never done sales for Primo-

But I’m having a hard time believing “ABC Financial Institution” is deeply concerned about critical vendor risk from the guy who refills the break room water cooler.

Jan 23

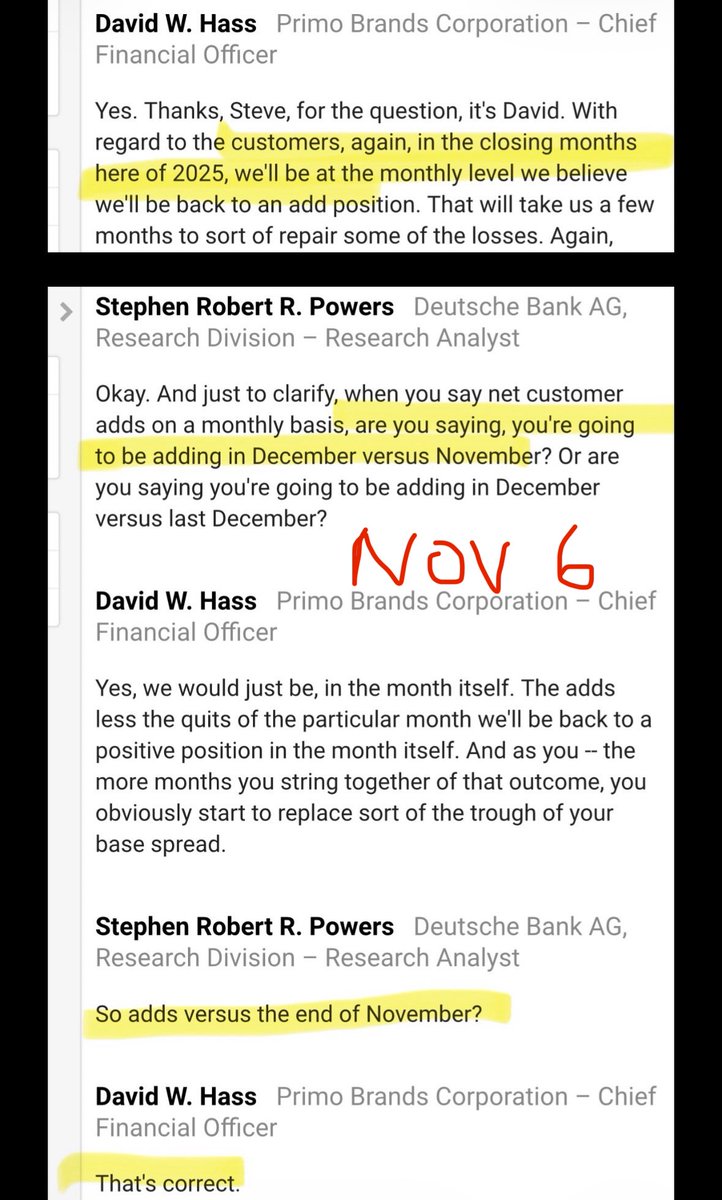

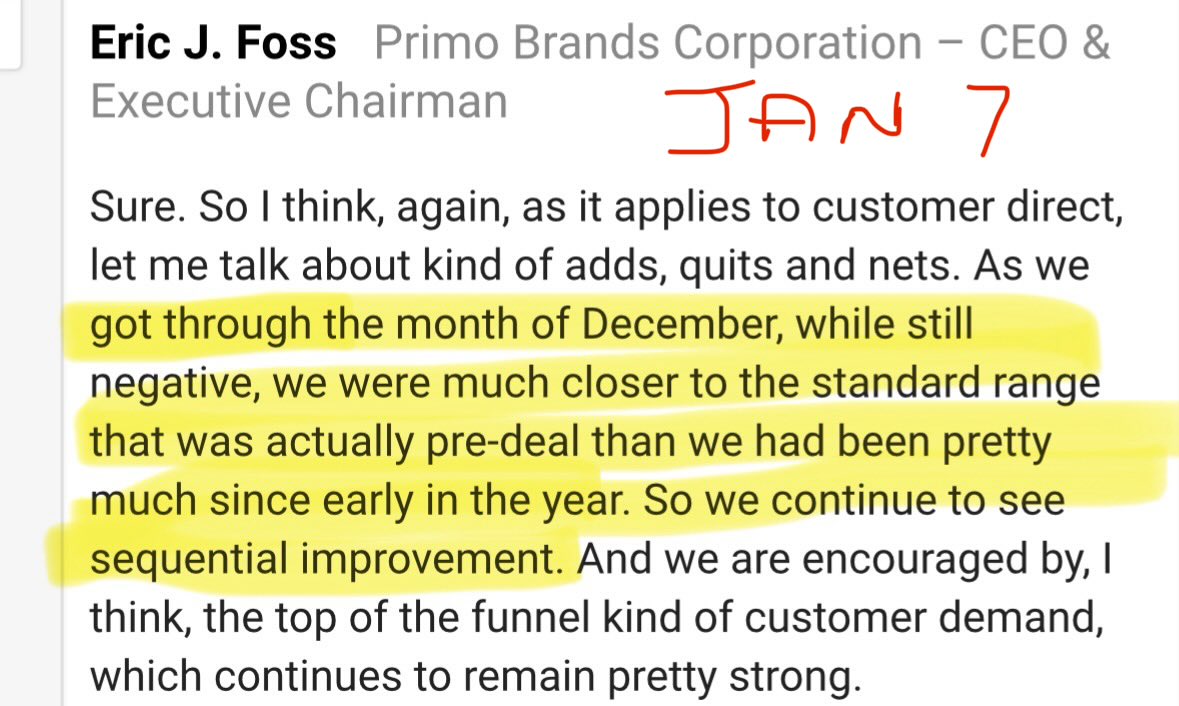

PRMB

Didn’t hit the soft guide of ve customer adds in December, but at this px (8x EBITDA), (improving) directionality is probably what matters

H1 likely will have added integration spend (SAP & WMS), so hope is that’s offset w/ improvement elsewhere-

E.g.: truck loading recovering from horrible 80% efficiency (?) to the standard 99% that aids in realizing route density, not having to deal with angry, churning customers, etc

So, mgmt’s story / street algo is back to very modest ve topline in ‘26 on volume recovery/minimial px easy comps w/ slight margin improvement

Ideally, integration is less of a headwind & mkt looks out to ‘27 on normalized LSD growth (x-sell, other advantages of scale, Foss makes good & now able to take px) w/ more margin upside

FCF’s always been the issue here (high capex leverage =bad conversion), but leverage is surprisingly inoffensive now @ 3x & can see a more palatable 2.5x by EoY ‘26.

A promise of the tie up was less capex intensity (scale adv PRMW stops doing dumb things like building nat gas fleets)

Regardless, trajectory & out year picture continues to improve:

Rerate ~$1.5B ‘26 EBITDA to 9x (I believe legacy PRMW traded around here or higher? Despite being a worse biz) >>

$25 stock, 30% upside & potential for ~20% CAGR in ‘27 w/ cash gen, bbk, & value accrual to eqy

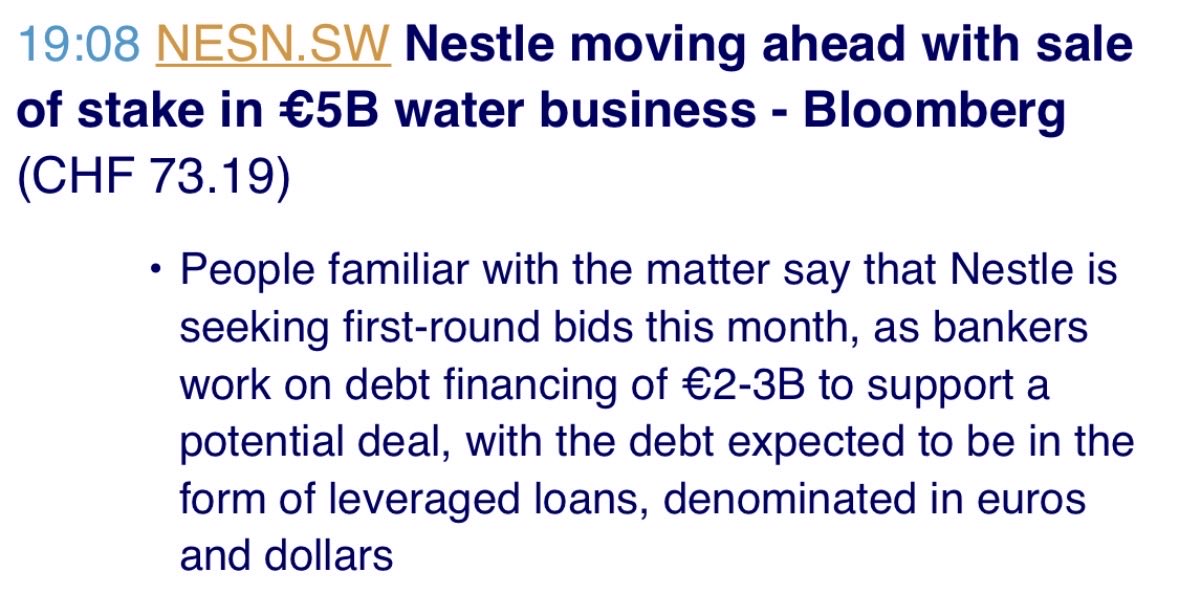

Bonus: comp coming market w/ Nestle’s water biz. Latest rumor was €5B @ 10x €500M segment EBITDA

7

2,717

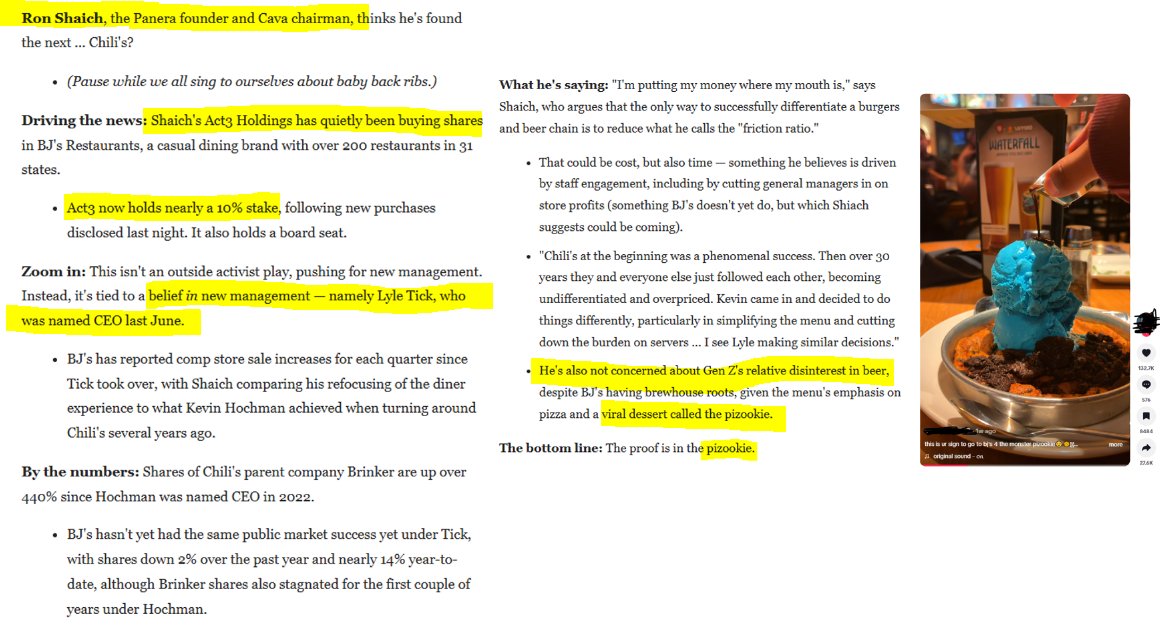

BJRI

Nice call out by Axios the other day on Shaich's large & growing stake

Shaich's been involved/a rep of his has had a director's seat since at least 2020 & I'm sure helped pick Tick

Eyeballing comps- decent & improved in '25, guiding for more of the same in '26, & largely traffic driven. If the guide holds >> accelerating comps on a 2 yr basis.

(Check decline seems mostly a mix issue- blame the growth of the late night crowd- pricing is steady to slightly up)

RL margins up 100 bps over the period, implied guide for another 40 - 50 in '26. So, not jamming promos for traffic / or can at least manage costs

And, most importantly (see: Chili's mozzarella cheese pull craze)-

BJRI has a semi-viral social media hit in its Pizookie dessert.

4

1,155

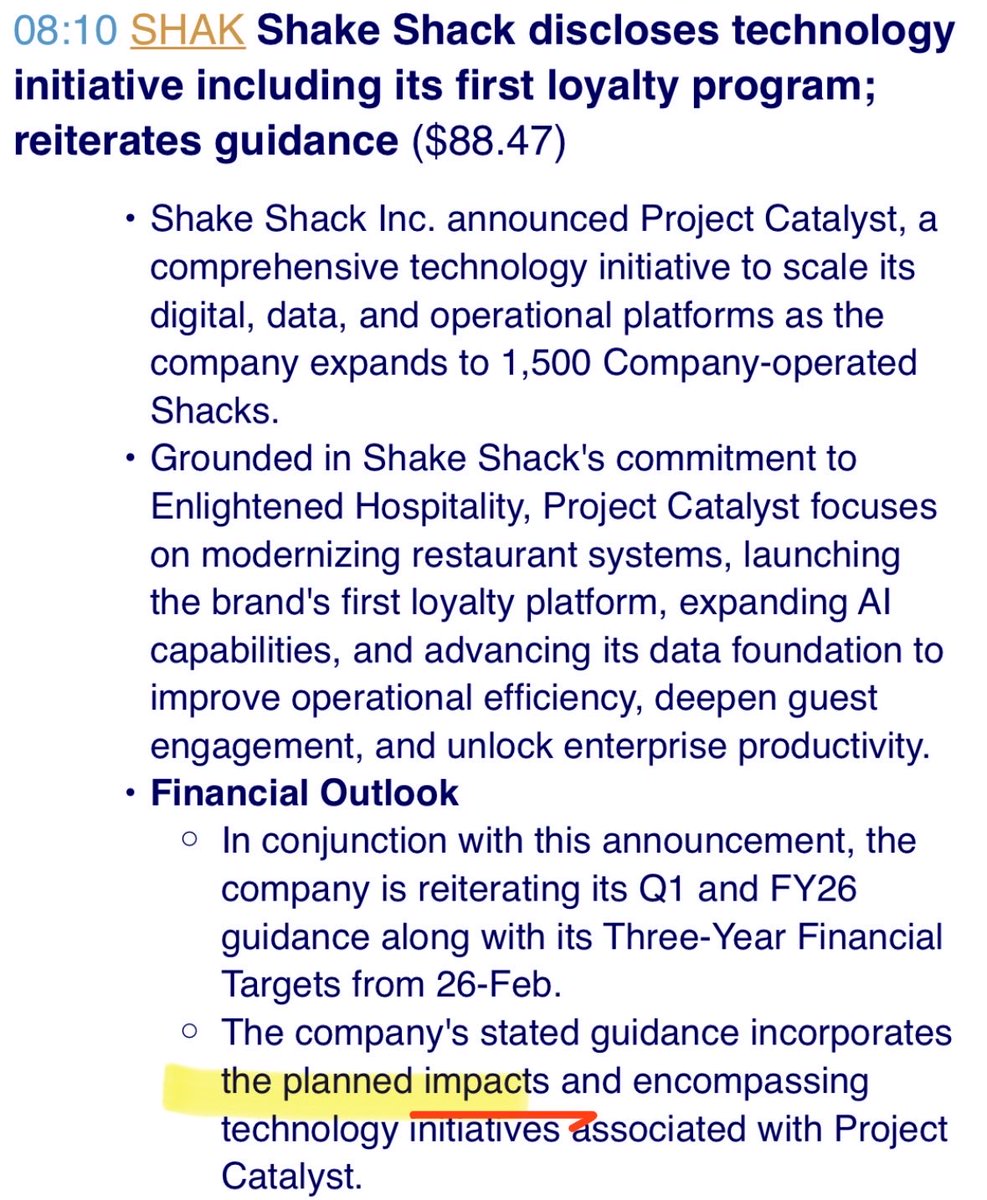

SHAK

Hmm

Skimming the presser, this has some ERP-overhaul adjacencies (read: the difficulty is always underestimated & generally tough for the stock)

Conversely, based on the language, were they tracking to nicely beat sans the costs of this upgrade program?

4

1,128

Mar 31

PWR

Investor day decks are already too long as is-

Polite request to IR teams not to pad them further w/ AI slop.

(Unless this is 4D chess: AI image query >> create demand >> more work & $ for Quanta >> capitalize that $ at X multiple >> generate shareholder value)

1

1

12

2,979

Mar 31

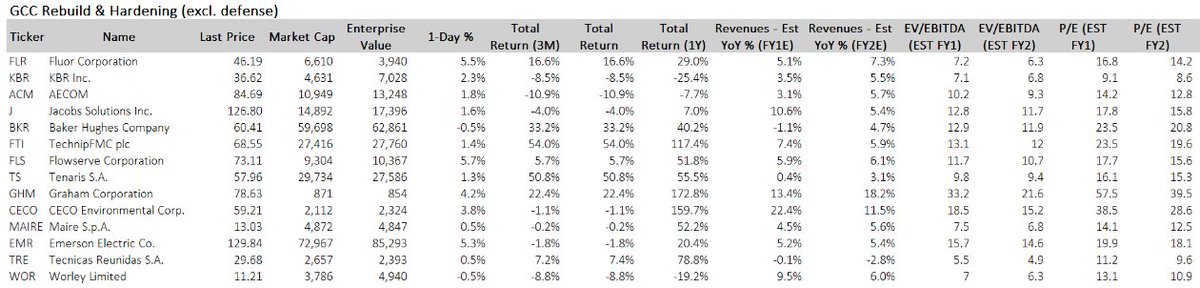

Probably several SS notes w/ similar "GCC Rebuilding Winners" lists, but here's another (mostly US) following 2 min of research

KBR's funny- theoretically both MTS (hardening work) & STS (gas, ammonia) segments/splitCos could/should benefit-

Obvi the stock px/multiple disagrees

1

5

1,174

Mar 31

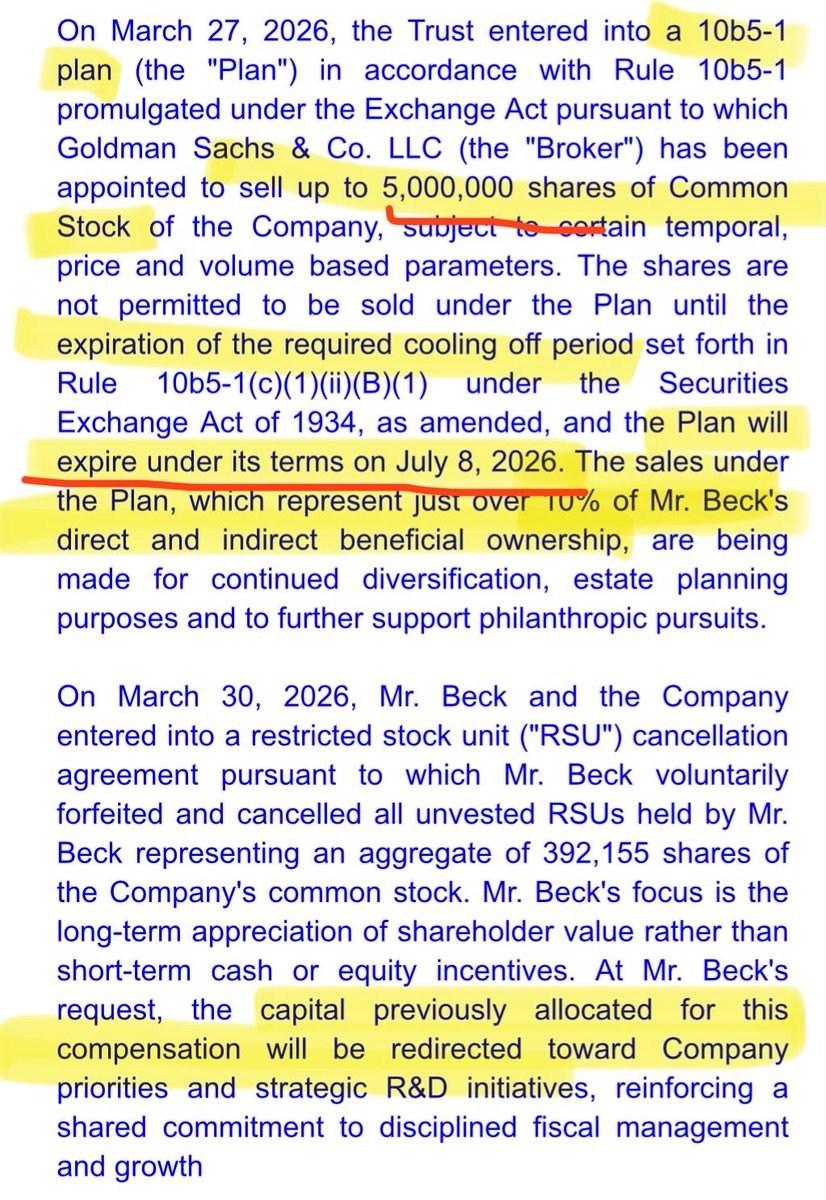

The other RocketCo

The 8-K: Beck’s giving up his base & bonus ($1.8M) plus ~$24M in RSUs

Asks to instead spend this $ on R&D

How nice.

The 13D: Beck will also be selling ~$300M of stock in a two week period starting late June

1

1

6

1,597

Mar 31

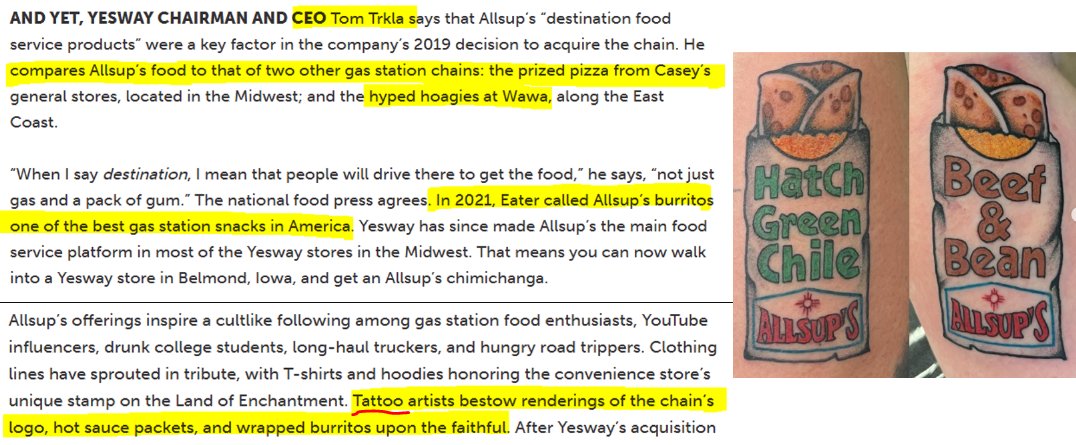

Yesway (YSWY)

Refiled its S-1

Tough time to go public...

Unless you're a value-oriented c-store (see MUSA stock MTD) that offers "destination" deep fried burritos (Eater: "one of the best gas station snacks in America") & has a quasi-cult following to the point that some people get tattoos of the store's logo

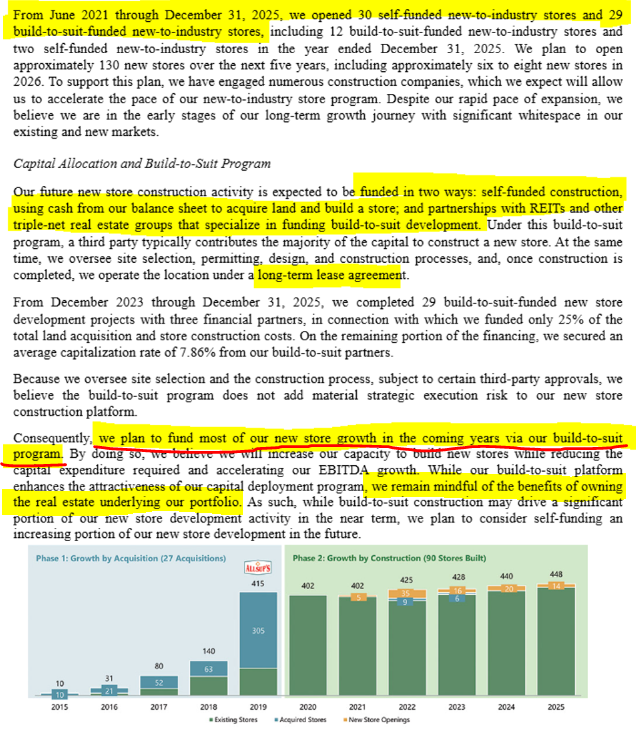

Also- anemic store growth since they last disclosed unit numbers:

403 stores in June '21 >> 419 in December '25 (net of an in-process divesture of 29 locations)

Apparently the plan now is to really accelerate growth & open 130 units over the next 5 years (ramping in '27, so ~30/yr) mostly thru a "build-to-suit" model NNN

So:

1) Can they pull this off (i.e., actually expand organically)?

2) A lease-first approach (at least for now!) is an interesting departure from their current majority-owned model (65% of units) & MUSA (~75% owned) CASY (all)

TLDR: I hope this doesn't trade day 1 with a silly CASY-level multiple

7

1,491

Mar 30

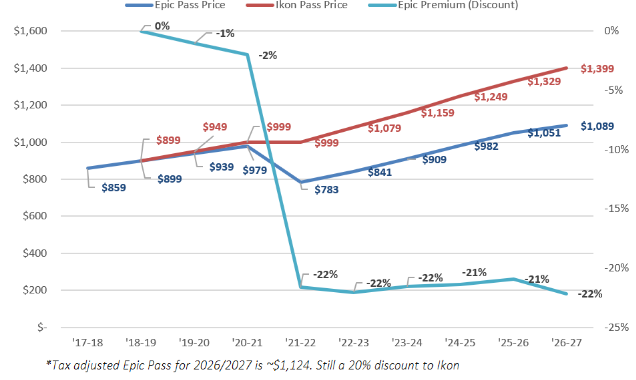

MTN

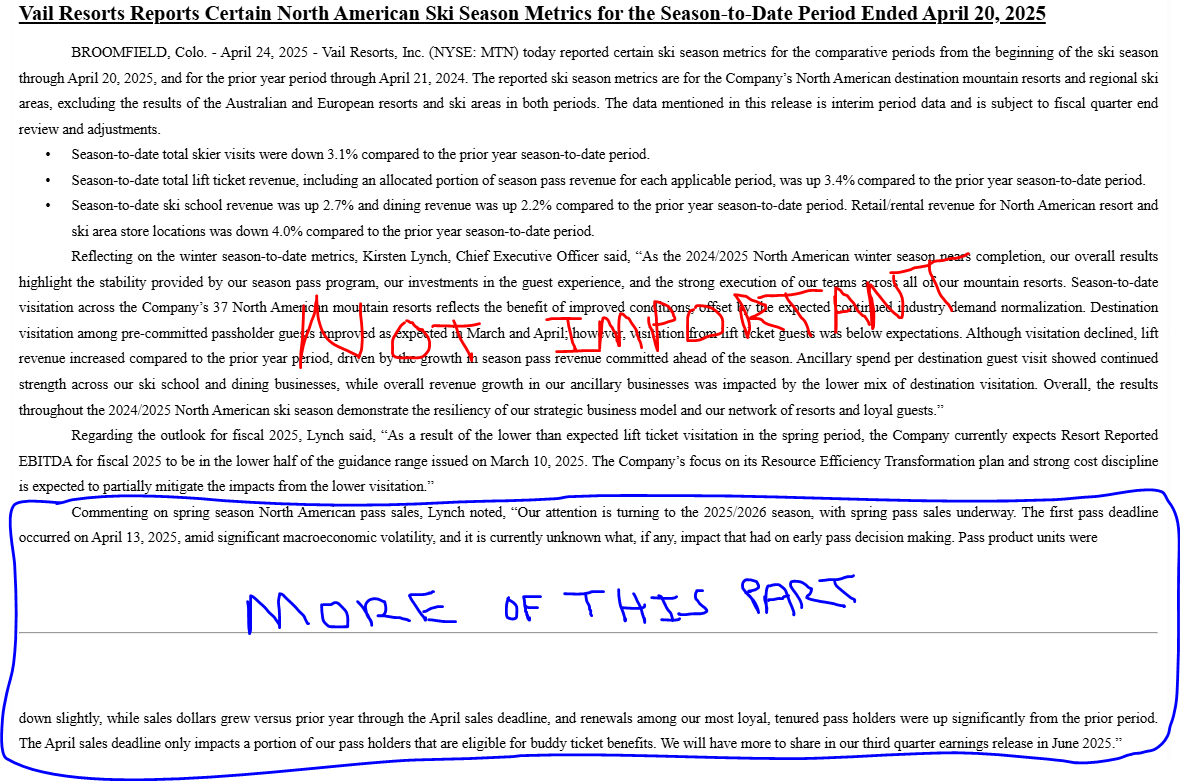

Vail typically provides an end of the season update in late April (as FY Q3 earnings aren't until early June)

Given it's:

- Katz's first April release as CEO since 2021

- This past season has been such a bust (weather) & is irrelevant for the stock

- The pass offerings for the 2026/2027 season have seen the most meaningful change in years (mostly the young adult pass, but also first full yr of Friend passes, a slightly lower px hike)

& passes will have been on sale for ~7 weeks-

*If* early pass sales are promising (read: less awful than the 2025/2026 on-mountain data), why not provide a bit more color/commentary/numbers around units, comparison to prior years, what products are resonating, etc. etc.?

Turnarounds take time & seasonality makes progressive fixes even slower/harder to see. Added transparency & update frequency can offset this some.

It's also just a presser w/o a call, meaning it's hardly a new obligation (unlike a formal KPI) & is something that's easy to simply not publish in subsequent years if/when the stock's not so depressed (& there are not calls for a breakup/asset sales)

Feb 26

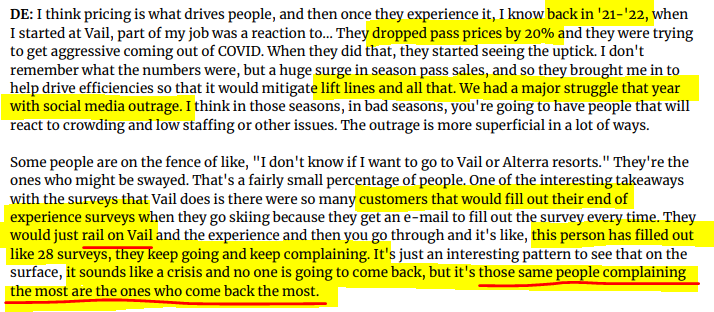

MTN

Not quite the CableCo level of "we don't have customers, we have hostages"-

But apparently not far off.

1

1

10

3,992

Mar 30

CHEF

Incrementally positive for Chef’s Warehouse if this:

A Suggests SYY’s focus is (still) on sheer scale

B. Ties up SYY’s attention, integration/M&A efforts, & balance sheet- preventing any sizable fine-dining deals or investments

2

1

11

1,854

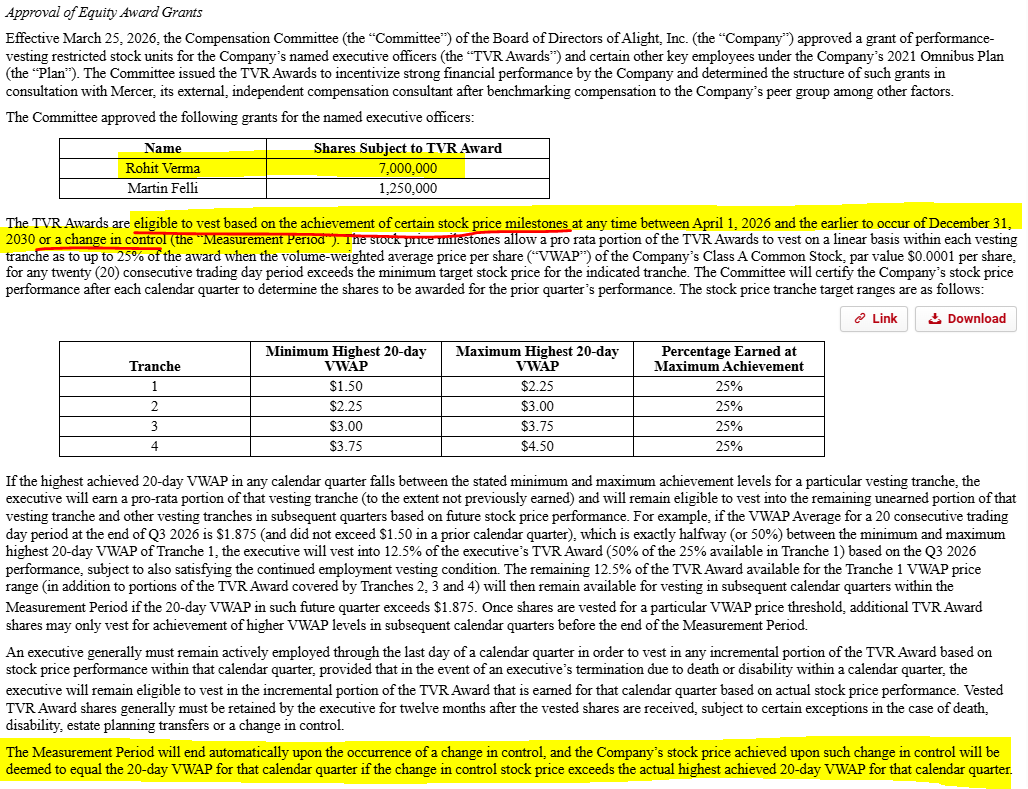

Mar 28

ALIT

Interesting very OTM comp package:

Incentive comp tranches only begin vesting at a stock px ~3x higher than today's

At the max achievement ($4.50/share), CEO stands to make >$31M

Shareholders would also see an >8x in under 5 years so, uh, think they'd be pretty happy too.

For context, this CEO started Jan 1, his comp package value w/ the stock px at the time (excl. sign on & 1 time bonuses) was ~$5.3M/yr (@ ~$2/share)

ALIT's stock has since tanked, so his annual comp is now ~$3M (bad!)

Point being this is A. meaningful $ for the CEO & B. even at the lowest end & longest time to vest, shareholders would do well (~25% 4.5yr IRR)

Kicker: this also applies in a CiC scenario >>

e.g., CEO sells for $2.25/share?

That's ~$4M from this alone, & an all in $20M - 25M payday w/ accelerated vesting.

The bad part? Literally everything else: 3x levered busted Foley deSPAC w/ revolving exec door declining sales & EBITDA

3

1,148

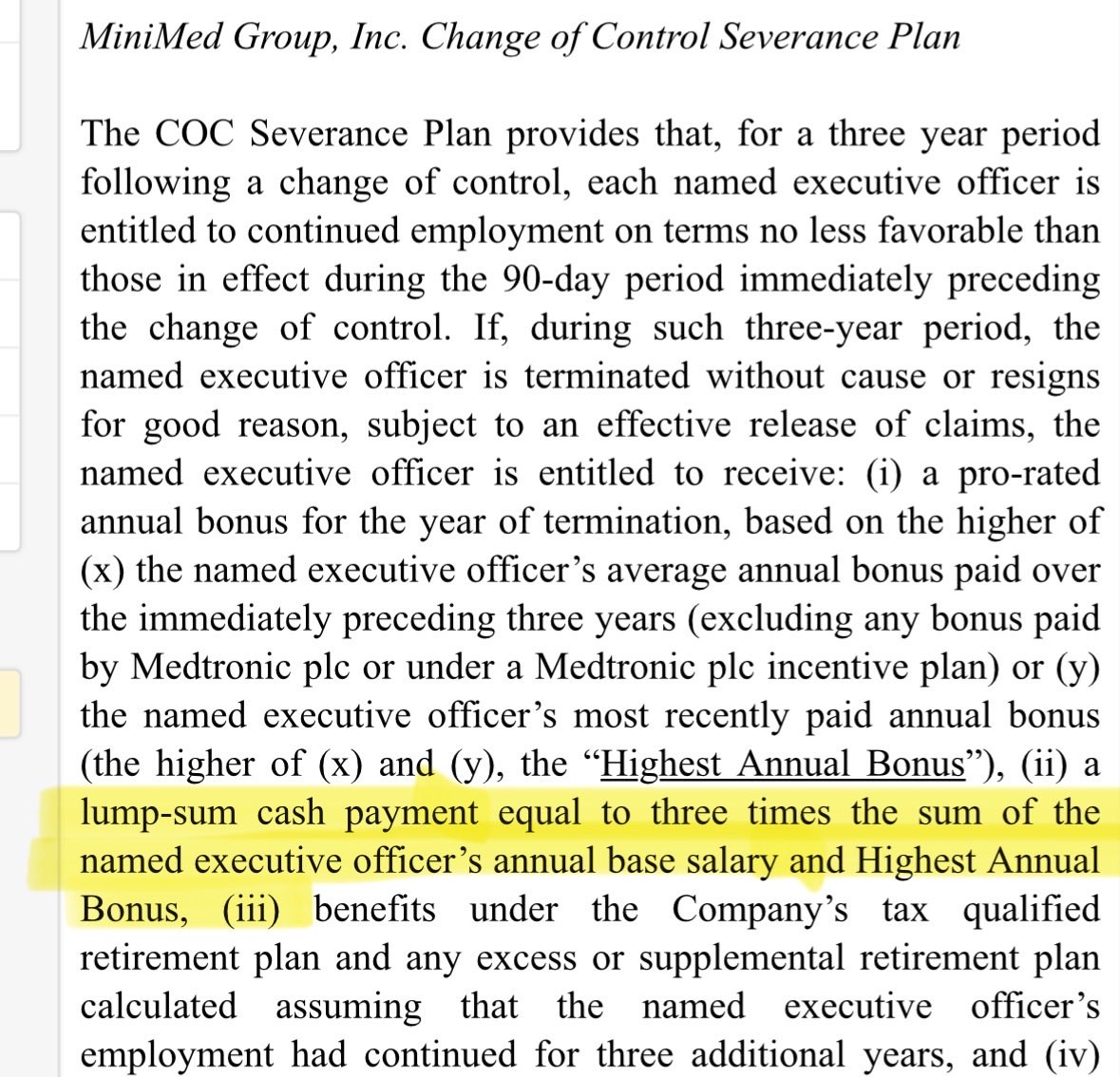

Mar 28

MMED

Tax free spin exemption period doesn’t expire until ~September ‘28 (2 yrs post split 6mo for MDT’s planned full divestiture)

But file this away as quite generous CiC severance agreement:

3x base & bonus prorated “highest” bonus (& for all NEOs, not just CEO)

3

805

Mar 27

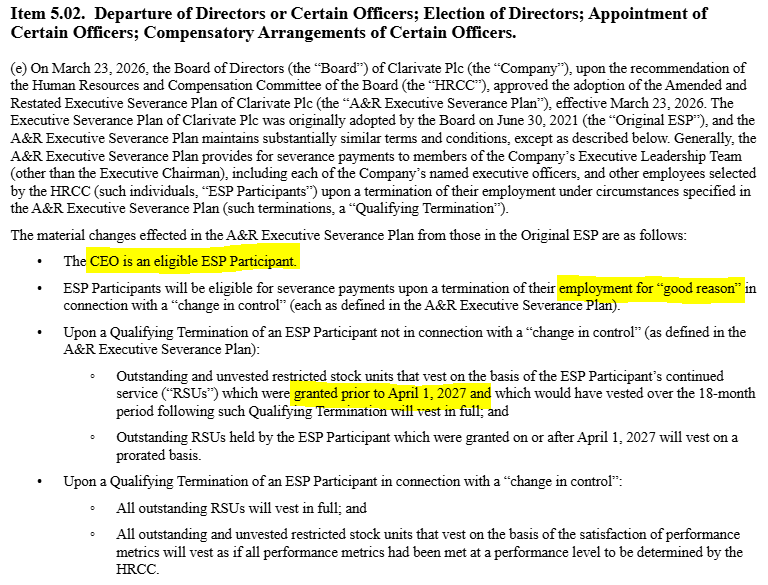

CLVT

Mildly interesting severance changes-

Launched a formal sales process for the life science & health (LS&H) biz in late Feb. Proceeds would be used to delever

RemainCo would be the govt/academia IP segments (~$2B sales & <$900M EBITDA)

Last April, there were rumors of PE interest in the IP biz. But, AFAIK, nothing serious since.

So, the relevant changes:

A. CEO now explicitly in the severance plan w/ everyone else (eliminates ambiguity for buyers, aligns incentives, yada yada)

B. "Good reason" (absent from prior plan)

- Boiler plate protection for any buyer of LS&H- team running the biz can't leave & claim severance immediately following the sale assuming the buyer offers similar comp/responsibilities (prior it was pretty ambiguous if severance could be claimed in a sale- so, now less risk for a buyer)

- Bit of a golden parachute for CLVT's exec team. Before, an acquirer could theoretically keep CLVT mgmt around w/ a large pay cut & not be on the hook for severance.

CiC is still double trigger, but CLVT's mgmt can fall back on "good reason" for the second trigger >> better incentivizes CLVT execs to push for a full (CiC) sale

C. April 2027 RSU cutoff

- For RSUs granted before April '27, there's an 18mo look forward period for vesting in the event of a *non-CIC* firing. Those granted after only get pro-rata treatment (months employed post grant/tranche vesting period * tranche).

- Net effect for CLVT mgmt is it's less attractive to sit around post April '27 as the subsequently issued equity comp isn't as protected in the event one's fired

Read: mgmt either must create value very soon or- more likely- push an aggressive sales process

TLDR: CLVT's been up for sale for years (in whole or parts). This adds incremental seriousness/urgency to the process.

And, at 4x levered & nearly a 30% FCF yield, there could be a bunch of equity upside in a monetization/deleveraging/rerate event (obviously this also means it gets nasty if it goes the other way)

2

1,490

Mar 26

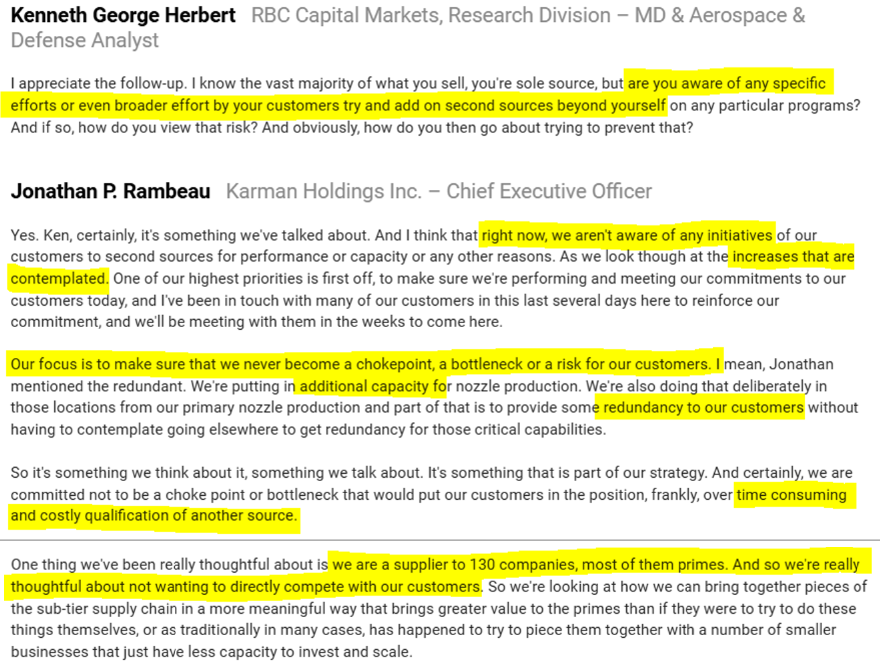

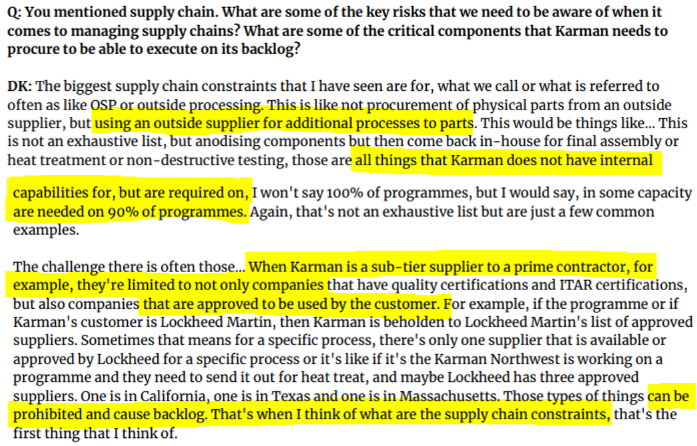

KRMN

When a stock’s at 140x PE, can entertain more remote bear arguments:

Mostly sole source now, but some primes have in-house parts that compete

KRMN’s good at what they do, but if there is a quality or (sustained) supply chain issue (even if it’s the fault of a prime’s approved subcontractor list), then it’s not unreasonable to think primes will verticalize/seek out other suppliers

Margin delta doesn’t help either- KRMN @ 30% & consolidated primes’ at half of that.

I’d assume KRMN’s parts are a small % of the total BoM (if anyone knows a rough %, do let me know), but at a certain point, the primes might want to push back on pricing, knowing KRMN has margin to give. And if not, back to the sourcing- maybe someone else can do it for cheaper.

Alternatively, a 30% margin business (or less) would be a nice uplift to have inside a prime- why don’t they start looking for & buying these smaller, high margin (or high potential margin), unconsolidated suppliers?

1

7

1,270

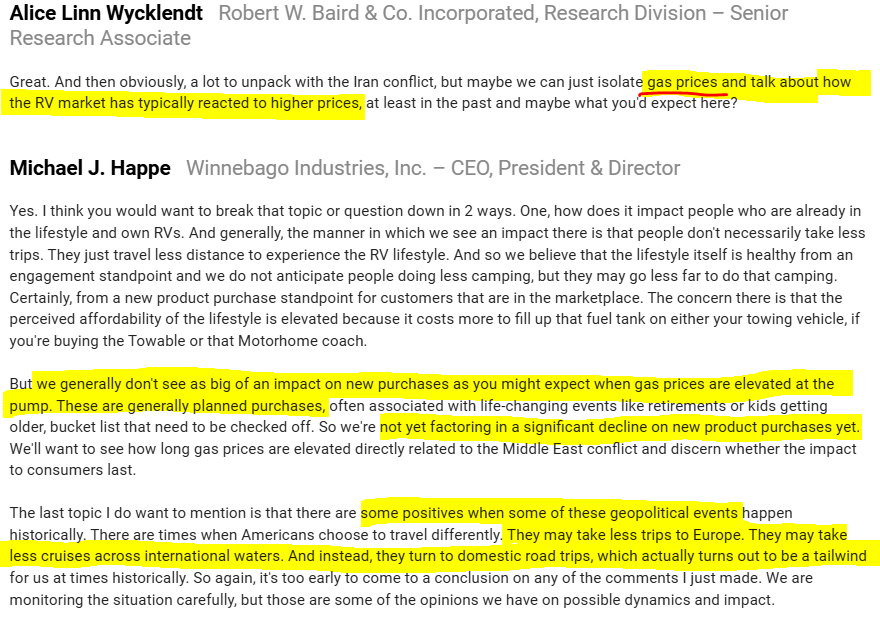

Mar 26

WGO

I love "heads I win, tails I win" spin comments like this-

"No, see higher gas px is good for RVs & here's a bunch of unquantified stories that are sorta believable to back it up"

Best part is lower or flat gas px are also great for RVs

Same story w/ rates

Undefeated biz

1

7

818

Mar 25

GO

Another $700K, $2.4M in a week

Q ends this Saturday (pretty sure)

FWIW, they’re lapping an artificially weak comp (Q1 ‘24 had benefit of Easter, which optically hurt Q1 ‘25, 4.2% two yr stack)

IDK- he all but knows how the Q will end up & either has tons of confidence in the guide-

Or doesn’t mind ruining his rep w/ investors, inviting new, uh, “involved” shareholders, risking his job, & of course- losing a bunch of his own $

Mar 20

GO

What a disaster

Ragatz has been buying all the way down since $28/sh, so another ~$500K from him means little

But CEO Potter putting down ~$1.6M so close to Q end is interesting

Skimming his employment agreement-

That’s ~150% of his base salary, can’t imagine the bonus (125% target) this yr will be great, initial sign on options (Feb ‘25) are very UW initial RSUs went from $2M grant date value to ~$750K today, & that $1.6M open market buy is still meaningful vs his annual equity grant ($1.4M of a 50/50 split of RSUs/UW options vesting this month- IDK what personal LTV you can get for that)

His recent background was running a smallish (160 unit?) grocery store prior to GO. I’m sure the pay was fine, but not Ragatz @ H&F kind of $

So, without knowing Potter’s personal financial circumstances- this *appears* to be meaningful $ (liquidity) for him.

TLDR: this looks like more than a token purchase & it was 9 days prior to the FY Q end (I think 3/28)-

Q1 comps (guiding down 2.5% to down 1.5%) coming in less bad than feared?

8

2,600