The deal and funding database built for biopharma. Curated deal comps, company profiles, pipelines, dedicated analyst support so you do better research faster

Joined January 2017

- Tweets 426

- Following 251

- Followers 432

- Likes 100

150 Photos and videos

Jun 10

Cancer dealmaking in Q1 2026 points to a healthy, broadening financing environment, with capital concentrating in later-stage, higher-conviction assets.

Read our research

na2.hubs.ly/H063NKt0

1

1

162

Jun 9

DealForma data cited by The New York Times shows China has rapidly become a major source of biopharma dealmaking and oncology innovation, intensifying concerns about U.S. competitiveness in drug development.

Read it here

na2.hubs.ly/H0629lL0

1

105

Jun 4

Biopharma therapeutics and platform financing activity in Q1 2026 reflected a strengthening IPO market alongside more selective follow-on and PIPE funding conditions.

Read our research

na2.hubs.ly/H05YM5X0

1

65

May 28

Biopharma therapeutics and platform financing activity in Q1 2026 reflected a strengthening IPO market alongside more selective follow-on and PIPE funding conditions.

Read our research

na2.hubs.ly/H05P4-20

18

May 20

Q1 2026 biopharma therapeutic and platform M&A shifted toward fewer, larger, and higher-quality acquisitions, with buyers prioritizing late-stage, commercially validated, and strategically differentiated assets.

Read our research

na2.hubs.ly/H05DXnW0

1

21

May 12

We’re excited to share that Chris Dokomajilar, Founder & CEO of DealForma, will be speaking at the CELS Canada in the Valley Showcase 2026 on May 14.

Chris will lead a session titled “Biopharma Venture, Licensing, IPOs, and M&A Trends Through Q1 2026.”

na2.hubs.ly/H05rLK00

36

May 12

WSJ cited DealForma data showing that China and Hong Kong companies accounted for 50% of large pharma in-licensing deals with at least $50 million upfront so far this year, underscoring rising global pharma interest in China-originated assets.

na2.hubs.ly/H05rzNr0

29

May 12

Our Q1 2026 review reflects a shift toward fewer, larger, higher-quality biopharma R&D partnerships, with stronger upfront capital deployment and sustained deal flow, reinforcing disciplined investment.

Read our research

na2.hubs.ly/H05rzJz0

41

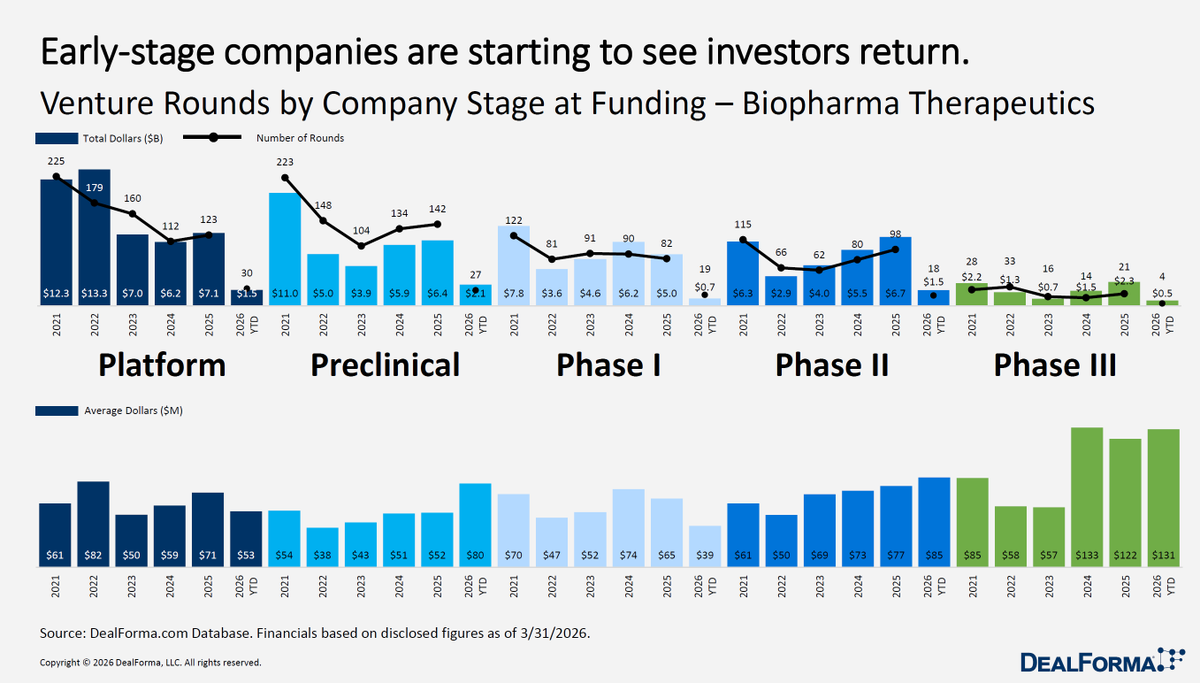

Apr 29

Early-stage biopharma funding rebounded in 2025, but Q1 2026 is mixed: softer at platform/preclinical, while Phase II–III remains resilient with dollars and check sizes holding near 2025 levels.

1

45

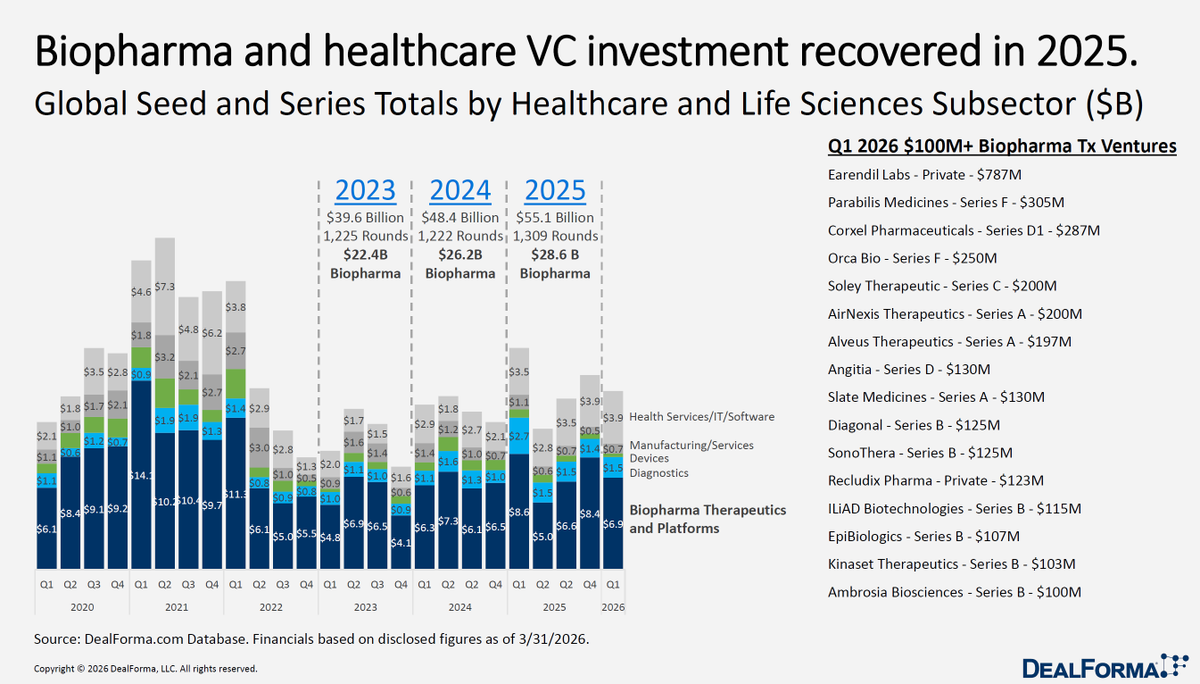

Apr 28

Biopharma and healthcare VC investment rebounded in 2025 to $55.1B (1,309 rounds), up from $48.4B in 2024, with biopharma specifically increasing to $28.6B. Momentum has carried into Q1 2026 with several large $100M rounds.

87

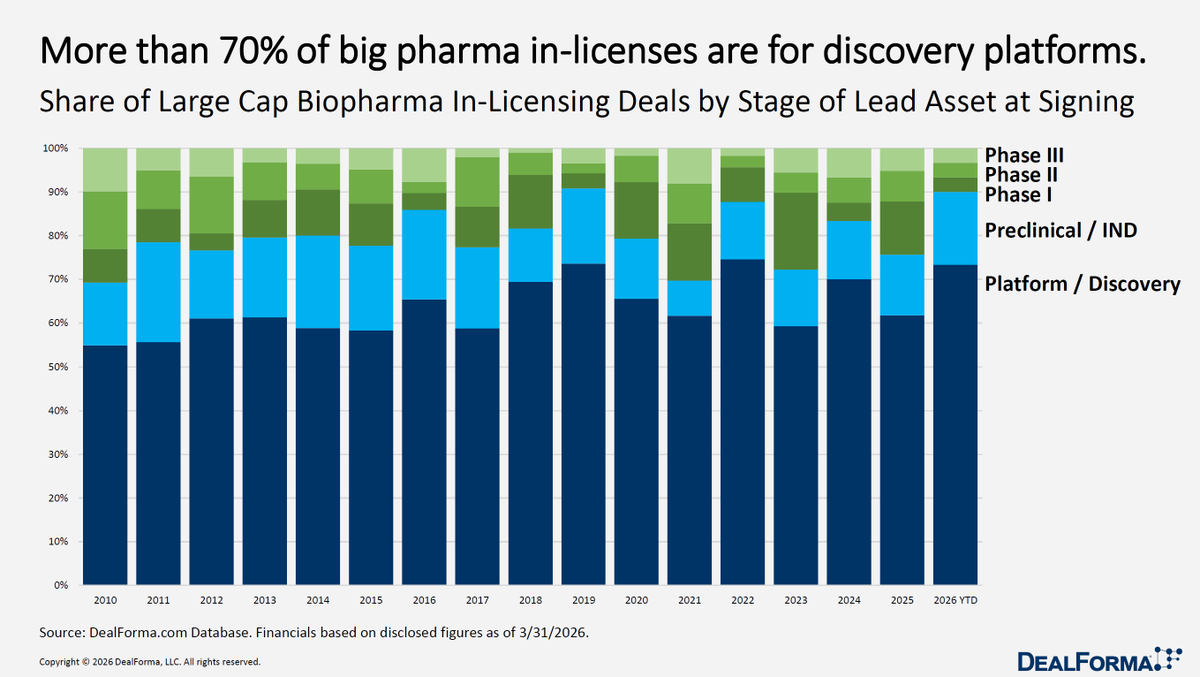

Apr 28

Big pharma in-licensing remains heavily skewed toward early-stage assets, with platform/discovery deals consistently making up ~60–70% of activity, rising to ~75% in 2026 YTD. Late-stage (Phase II–III) deals continue to represent only a small share.

1

1

93

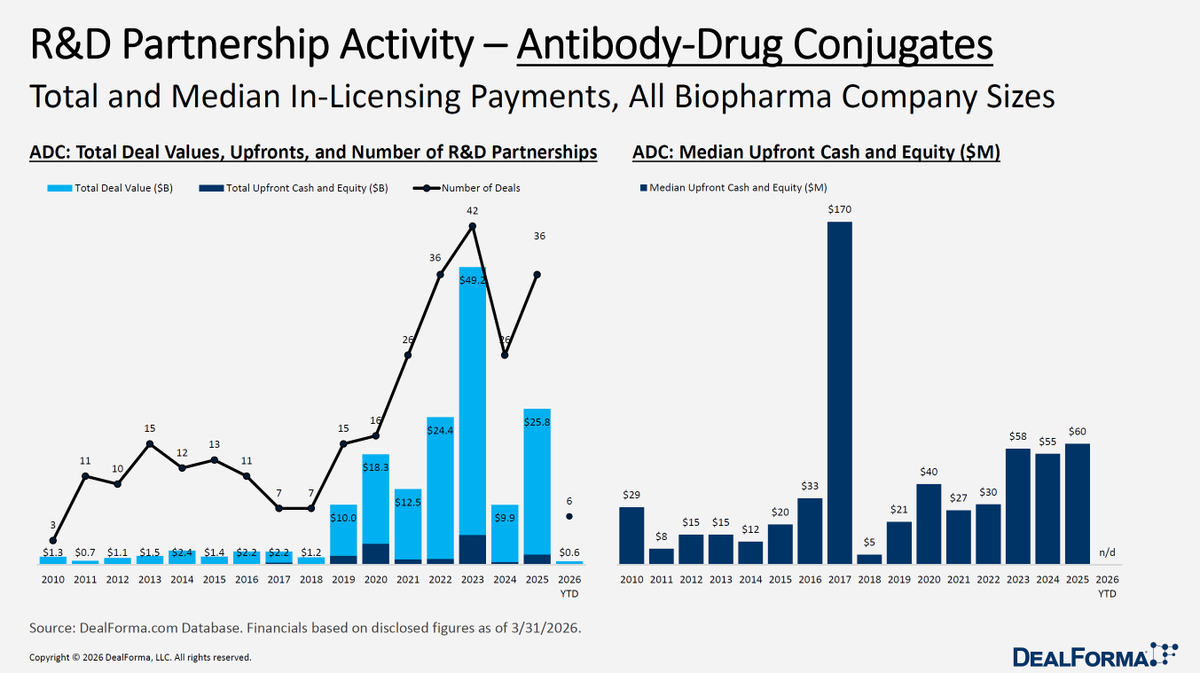

Apr 27

ADC deal activity remained strong in 2025, with total value reaching ~$25.8B across 36 deals and median upfronts rising to ~$60M, signaling continued demand for high-quality assets. In 2026 YTD, activity is more muted (~$0.6B; 6 deals)

1

88

Apr 24

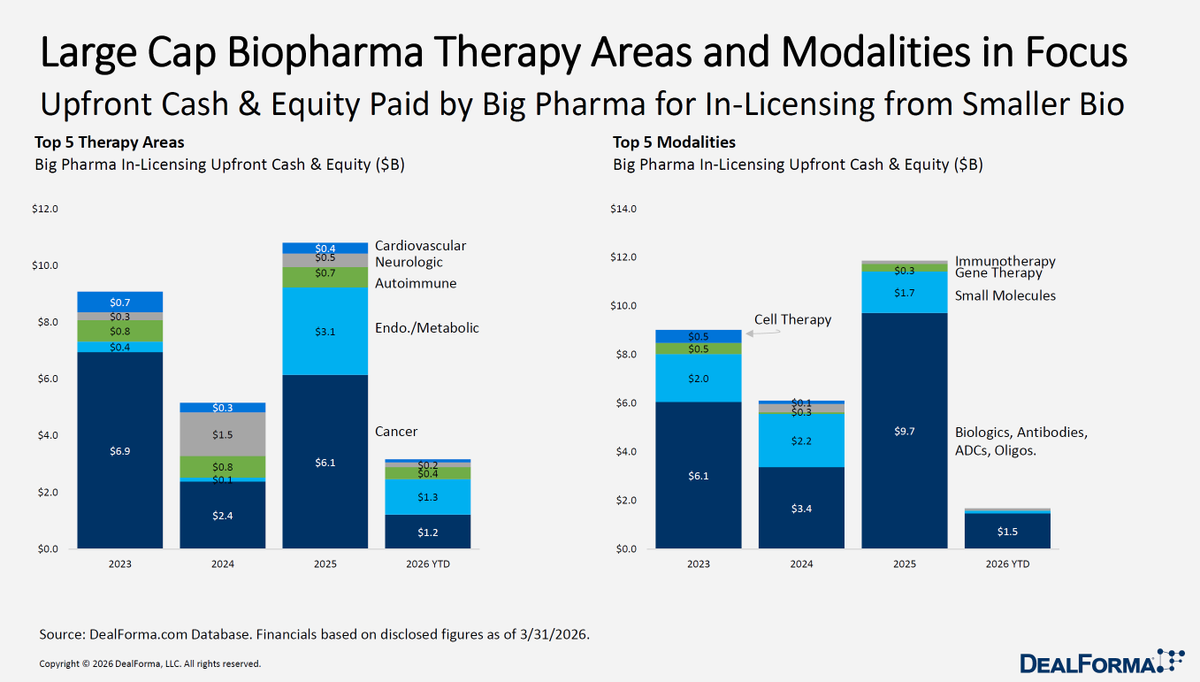

Big pharma in-licensing spend is heavily concentrated in oncology and biologics, with cancer driving the majority of upfront payments each year and biologics/antibodies/ADCs dominating modality spend (peaking at ~$9.7B in 2025).

33

Apr 24

Biopharma & medtech entered 2026 with selective momentum, with J.P. Morgan’s reports — powered by DealForma — highlighting strong licensing, M&A, and early IPO recovery.

Download the full reports for deeper insights.

na2.hubs.ly/H054J2k0

1

22

Apr 24

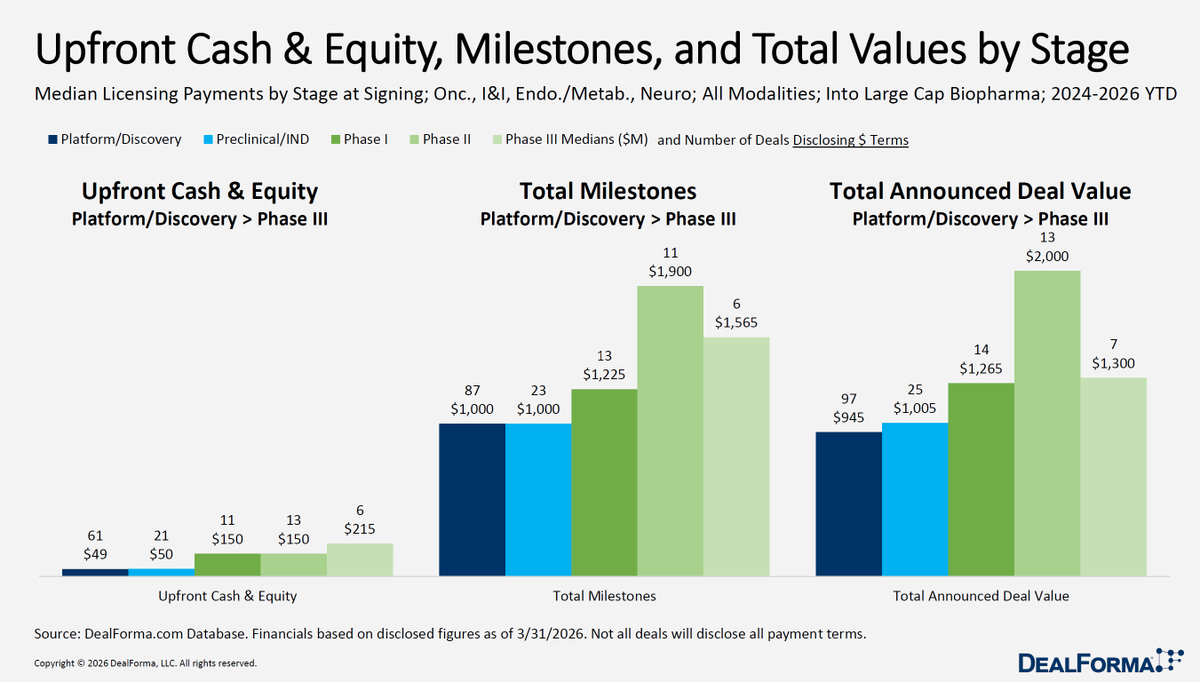

Upfront payments remain relatively compressed across stages (~$49M–$215M), but total deal value expands significantly in later stages, driven by milestones—peaking around ~$2.0B in Phase II and ~$1.3B in Phase III.

1

1

33

Apr 23

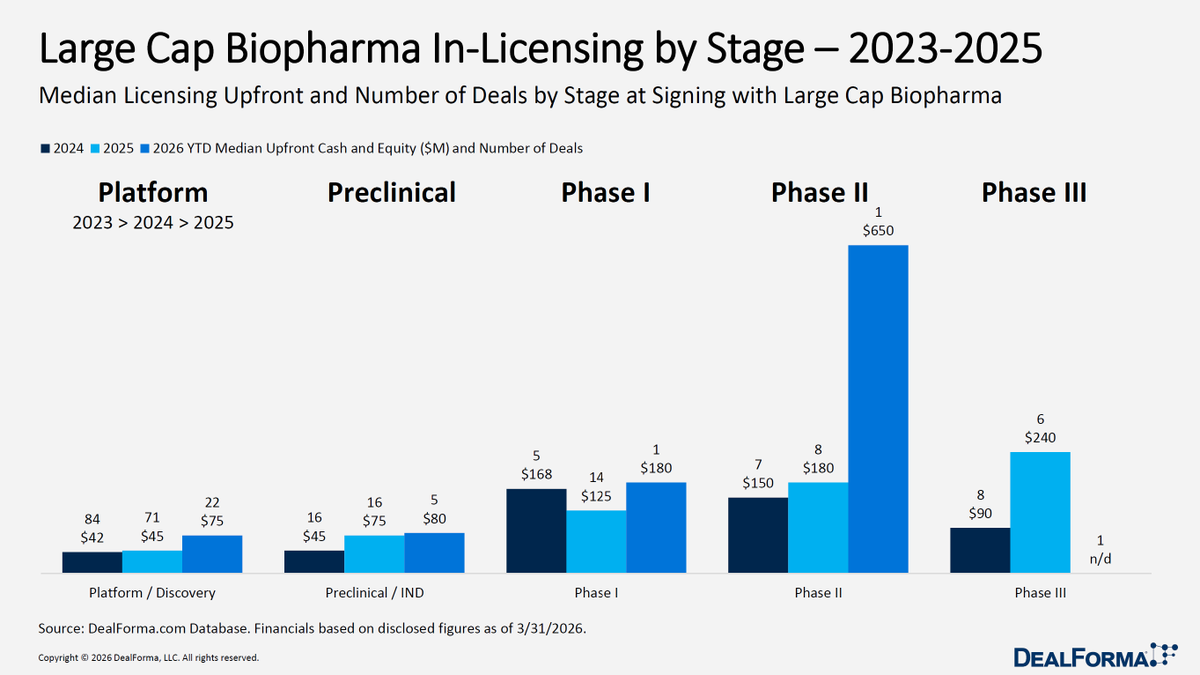

From 2023–2025, upfronts increased with stage, with later-stage deals commanding the highest premiums. In Q1 2026, this trend accelerated—Phase II median upfront hit ~$650M (single deal) and Phase I ~$180M—showing a shift toward fewer, high-value later-stage deals.

43

Apr 23

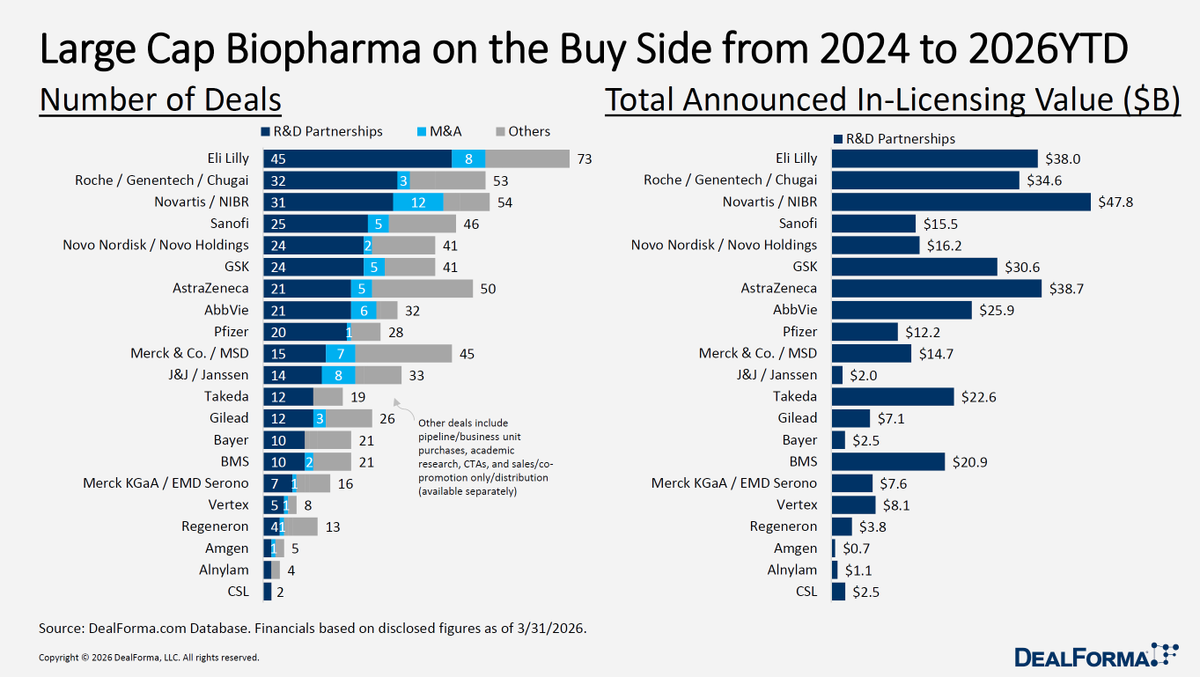

Large-cap biopharma dealmaking from 2024–2026 YTD is led by Eli Lilly, Roche, and Novartis in volume, with activity heavily skewed toward R&D partnerships over M&A. In terms of value, Novartis ($47.8B), AstraZeneca ($38.7B), and Eli Lilly ($38.0B) lead in in-licensing spend

1

68

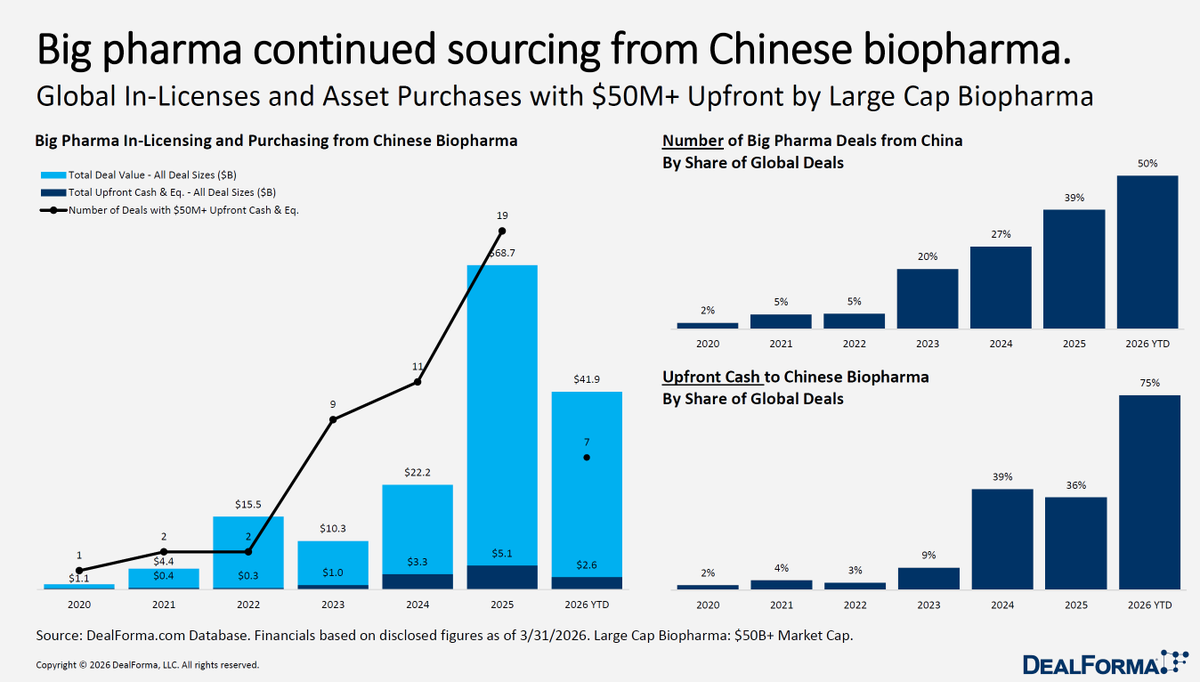

Apr 22

Big pharma significantly increased sourcing from Chinese biopharma through 2025, with deal value rising to $68.7B across 19 large transactions, alongside growing upfront payments. In Q1 2026, China accounted for ~50% of big pharma deals and ~75% of upfront capital.

1

558

Apr 22

Licensing upfronts in 2025 were relatively balanced across regions (~$5.0B U.S., $5.1B EMEA, $7.3B APAC), with APAC leading overall. In Q1 2026, activity shifted sharply toward APAC, which generated $3.4B in upfronts, compared to $1.4B in the U.S. and just $0.4B in EMEA.

1

91

Apr 22

Neurology deal activity in 2025 was mixed, with weaker R&D partnerships offset by strong M&A growth, steady venture funding, and improved IPO activity, signaling confidence in later-stage and clinically validated assets.

Read our research

na2.hubs.ly/H0509x_0

1

100