Advanced APIs, intelligent visualizations, and transformative narratives. Complexity simplified, intelligence amplified.

Joined October 2024

- Tweets 194

- Following 4

- Followers 505

- Likes 174

83 Photos and videos

DeepDiveData retweeted

Jun 4

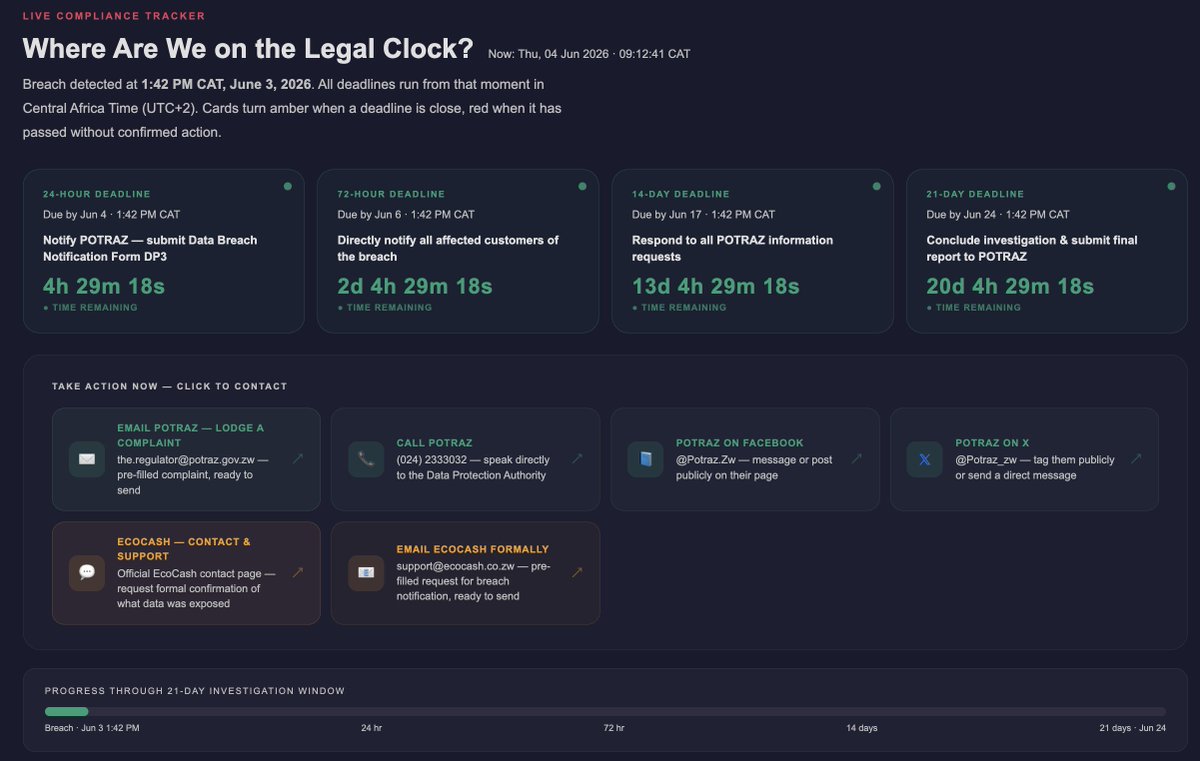

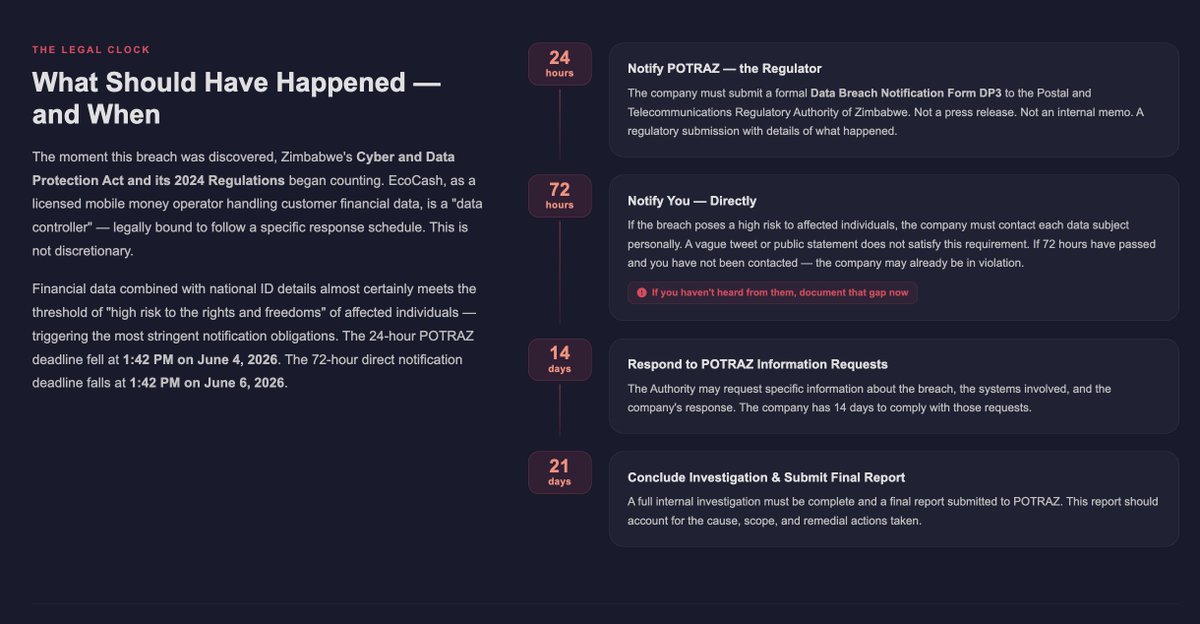

@DeepDiveDataZW built a live compliance clock tracking EcoCash's legal obligations after yesterday's X account breach.

The 24-hour POTRAZ notification deadline expires today at 1:42 PM.

Every card turns red the moment a deadline passes without confirmed action.

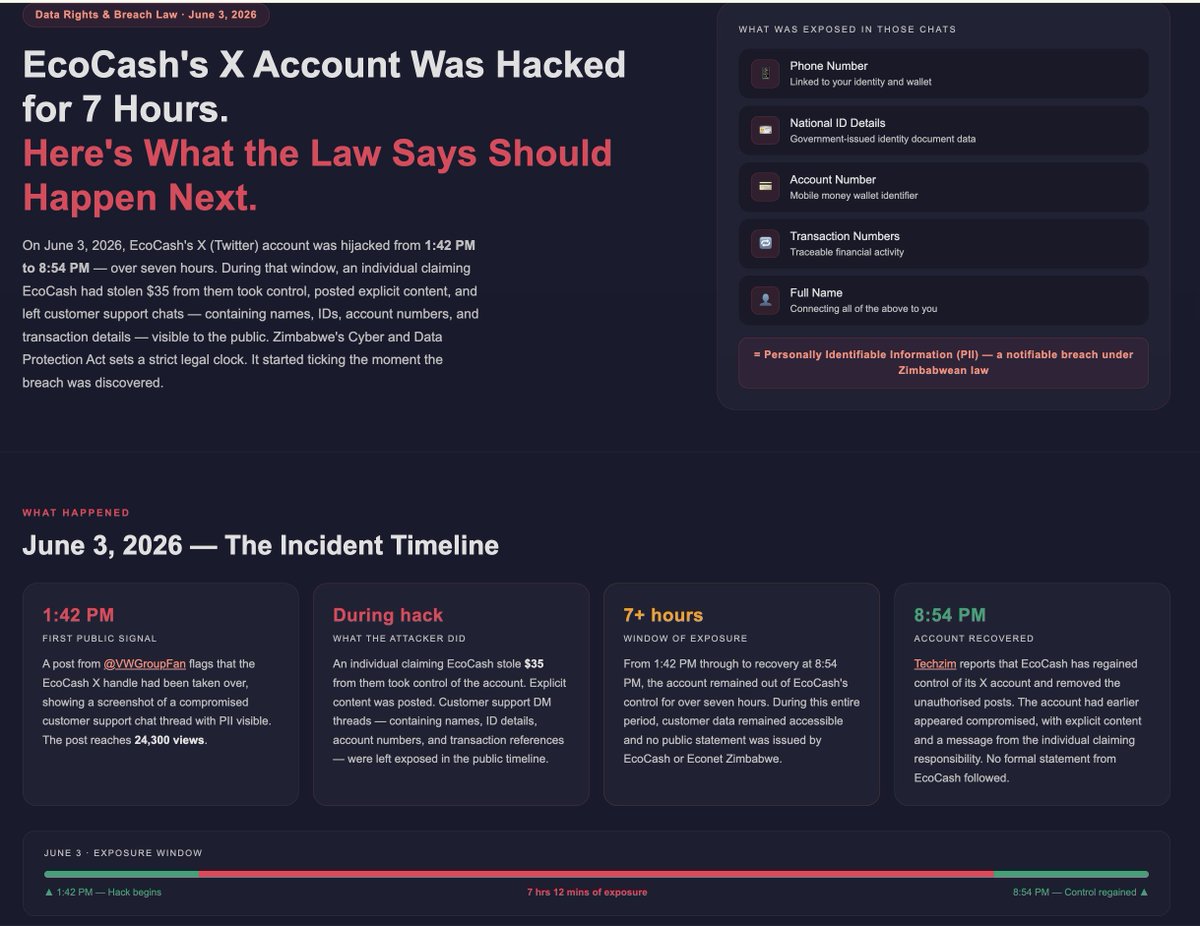

1/ @EcoCashZW 's X account was hacked on June 3, 2026.

For 7 hours and 12 minutes, customer names, IDs, account numbers and transactions were exposed via the public support chats.

Here's what the law says should happen next — and a live clock tracking whether it does. 🧵

1

3

142

1/ @EcoCashZW 's X account was hacked on June 3, 2026.

For 7 hours and 12 minutes, customer names, IDs, account numbers and transactions were exposed via the public support chats.

Here's what the law says should happen next — and a live clock tracking whether it does. 🧵

11

41

67

18,347

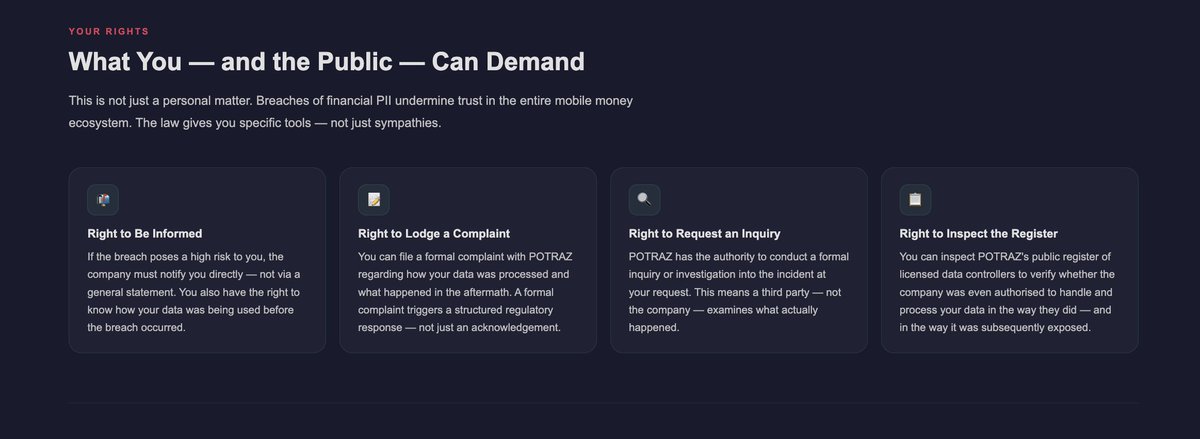

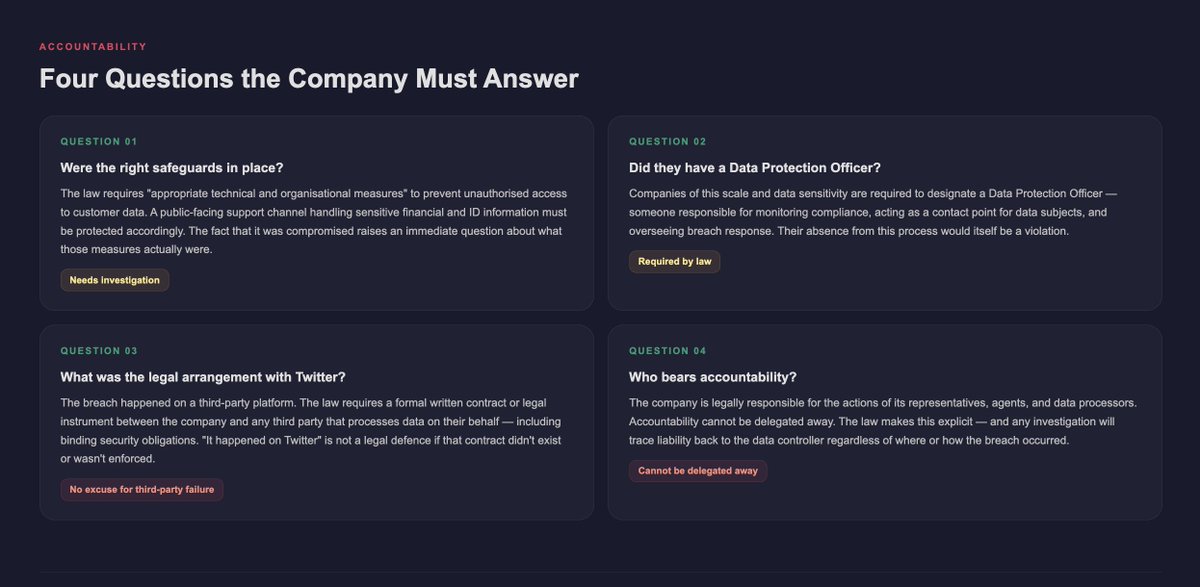

6/ If your data was in those chats, you have four rights under Zimbabwean law:

📬 Right to be notified directly

📝 Right to lodge a formal complaint

🔍 Right to request a POTRAZ inquiry

📋 Right to inspect the data controller register

1

5

6

1,843

7/ If EcoCash hasn't contacted you and 72 hours have passed — that silence is itself a reportable violation.

✉️ the.regulator@potraz.gov.zw

📞 (024) 2333032

🐦 @Potraz_zw

Full article live clock pre-filled complaint emails 👇

deepdivedata.co/articles/twi…

2

2

16

1,725

DeepDiveData retweeted

Jun 3

Normally I talk about businesses and their operations.

Today, I'm talking about their future customers.2027 is shaping up to be a landmark year for Zimbabwe's youth dividend.

By July 2027, the country will have added its second million new 16-year-olds since 2022.

The period from 2027–2029 is the fastest-growing phase of the cycle, peaking at more than 37,000 young people entering adulthood every month. At that pace, Zimbabwe adds a million new 16-year-olds in just 28 months.

The question is simple:Are you building for the Zimbabwe that exists today, or the one that is about to arrive?

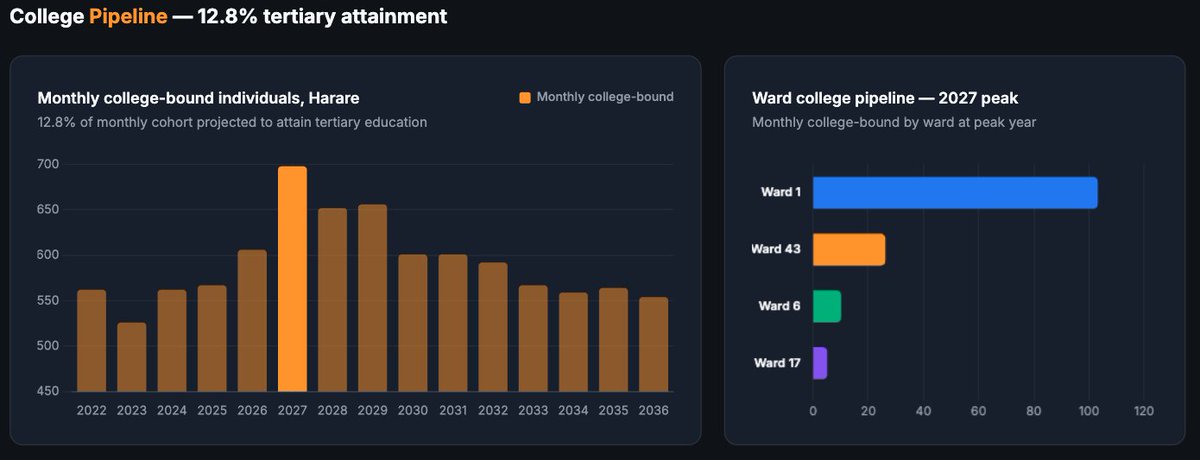

At @DeepDiveDataZW , we've mapped 121 youth-focused indicators across Zimbabwe's 10 provinces, 89 districts (60 rural and 29 urban), and 1,962 wards.

From smartphone adoption and education pathways to migration readiness and financial inclusion, we're tracking how Zimbabweans aged 16–21 will shape the next decade.Our dashboard and customised ward, district, and provincial reports will be available soon.

P.S. The screenshots feature four very different Harare Province wards: Ward 1 (Harare Rural), Ward 43 (Budiriro), Ward 17 (Mount Pleasant area), and Ward 6 (Chitungwiza). Together they show how differently the youth dividend will play out across peri-urban, high-density urban, and low-density urban communities. The full dataset covers all 1,962 wards in Zimbabwe.

For today, I'm giving away 3 FREE ward reports covering 5 key indicators.

Reply with the ward you'd like to see, and I'll post screenshots from the data 👇

1

4

4

402

DeepDiveData retweeted

@DeepDiveDataZW The full article was a really good read. Great content well delivered.

May 28

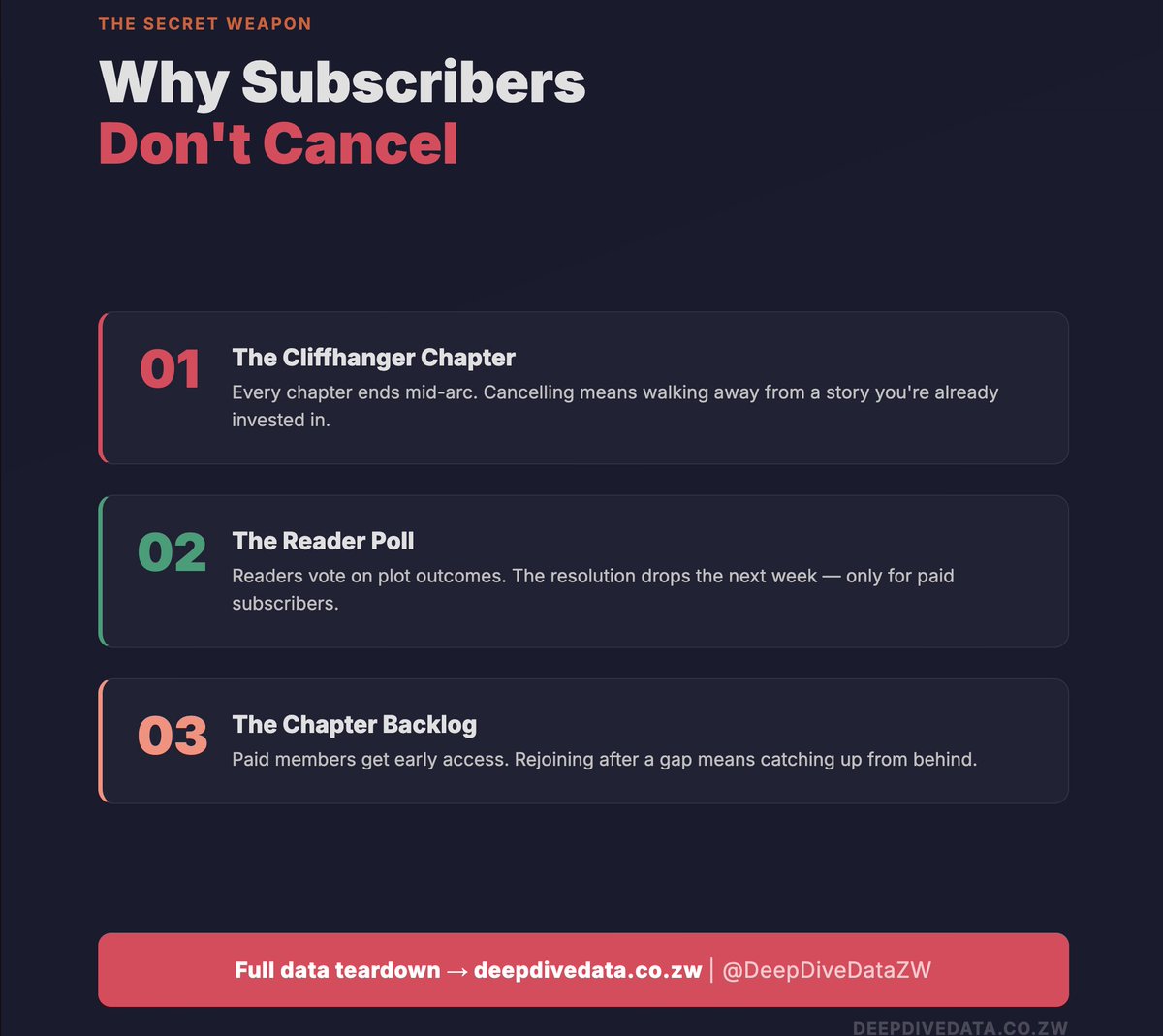

4/The retention strategy is the most interesting part.

-Every chapter ends on a cliffhanger.

-Readers vote on plot outcomes.

-Paid subscribers get the resolution the following week.The content format itself makes churn structurally difficult.Full teardown: deepdivedata.co/articles/wha…

1

2

130

DeepDiveData retweeted

May 28

One of the more interesting things I've read on Zim 🇿🇼 internet of late

May 28

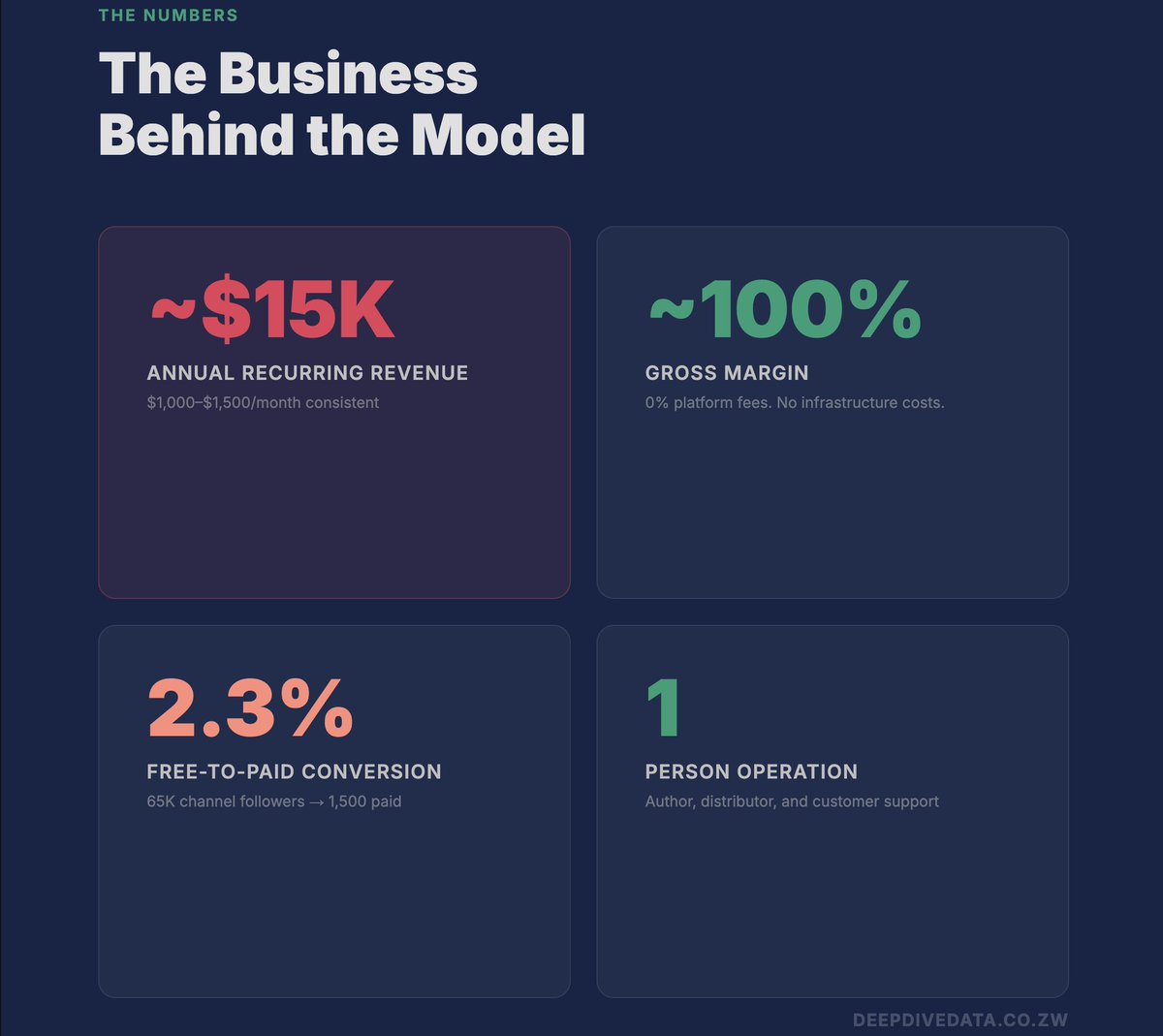

1/ A Zimbabwean novelist built a ~$15K/year subscription business entirely on WhatsApp.

No website. No app. No payment processor.

Just one phone number and 1,500 paying subscribers. 🧵

2

4

7

1,887

May 28

1/ A Zimbabwean novelist built a ~$15K/year subscription business entirely on WhatsApp.

No website. No app. No payment processor.

Just one phone number and 1,500 paying subscribers. 🧵

1

6

10

2,546

May 28

3/The economics are what make this model hard to ignore:

~$15K annual recurring revenue

~100% gross margin

2.3% free-to-paid conversion

Run entirely by one person.

No platform fees.

No infrastructure costs.

No paid acquisition.

1

1

3

262

May 28

4/The retention strategy is the most interesting part.

-Every chapter ends on a cliffhanger.

-Readers vote on plot outcomes.

-Paid subscribers get the resolution the following week.The content format itself makes churn structurally difficult.Full teardown: deepdivedata.co/articles/wha…

2

5

385

DeepDiveData retweeted

May 14

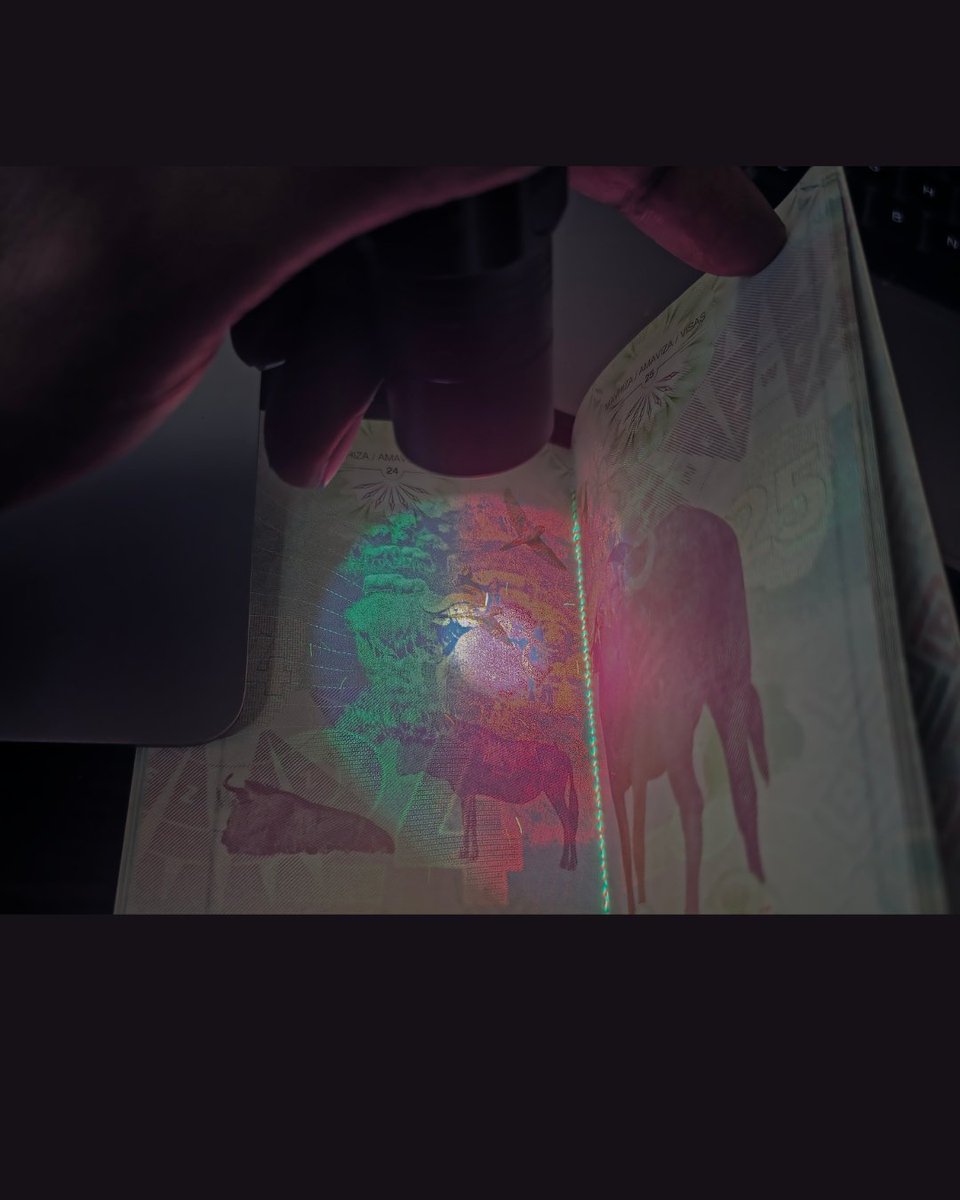

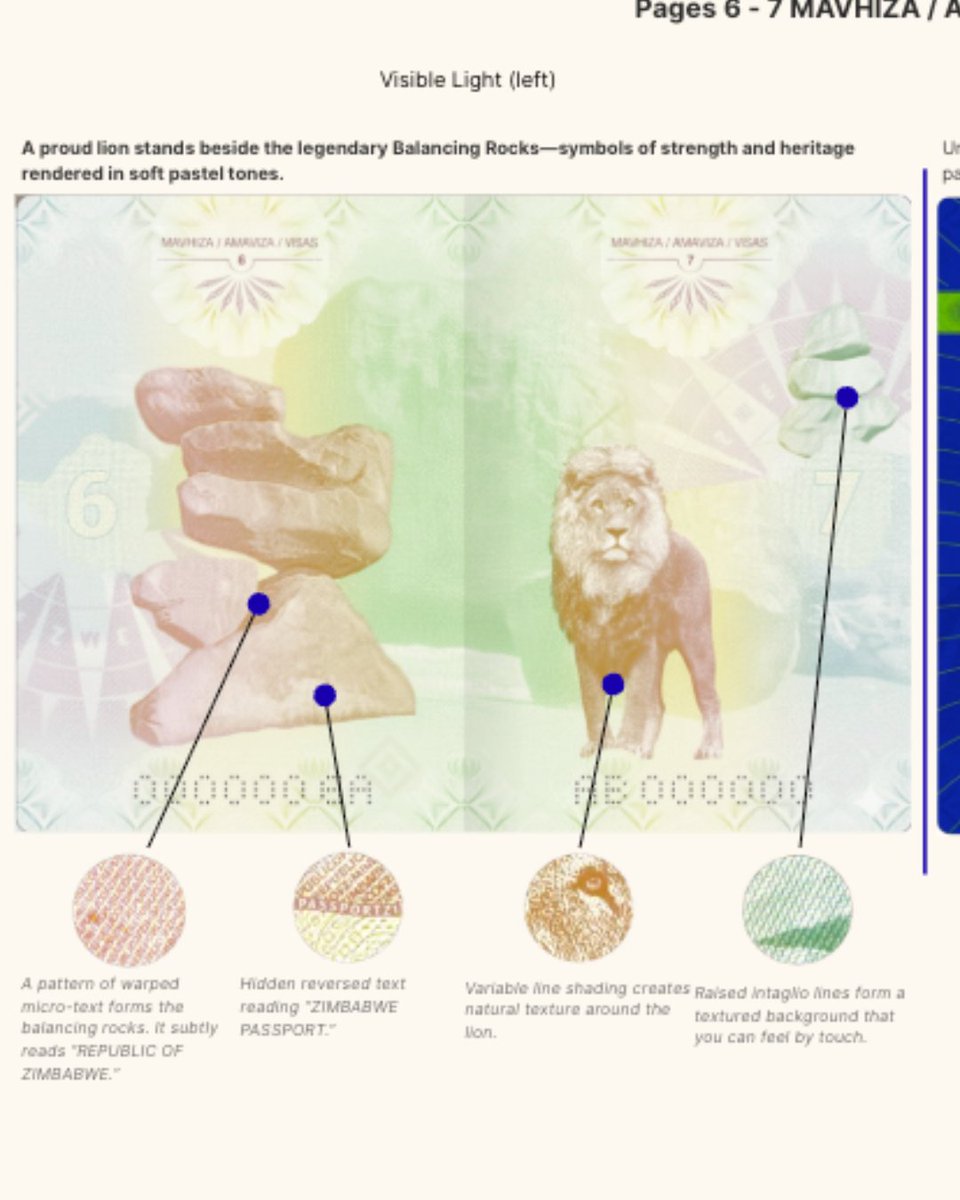

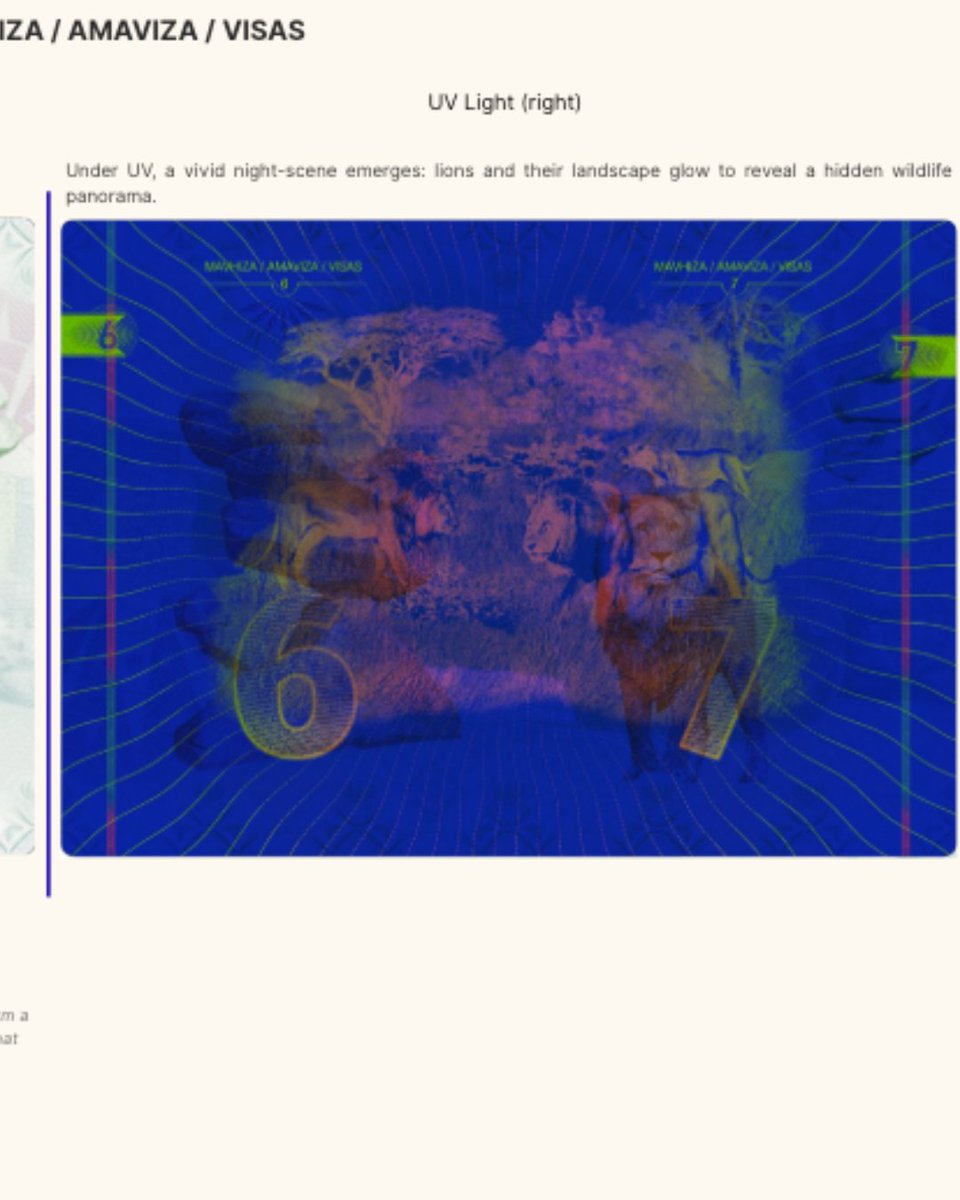

I’ve been researching how modern e-passports combine security engineering, national identity, advanced print systems, and embedded digital identity structures into one of the most sophisticated physical products people use every day.

This project documents:

• UV-reactive security features

• microtext systems

• intaglio printing

• tactile authentication layers

• and the visual language of secure travel documents.

Alongside the physical document research, @DeepDiveDataZW has also been exploring some of the data structures and identity architecture associated with modern e-passport chips and secure document systems.

This booklet is an offshoot, a labor of love adjacent to a deeper technical report.

Using the Zimbabwe e-Passport as a case study, I turned complex passport security features into a coffee-table-style editorial booklet exploring national symbols, wildlife motifs, security-print artistry, and the visual language of identity documents.

For the complete PDF:

reports@deepdivedata.co

4

9

683

DeepDiveData retweeted

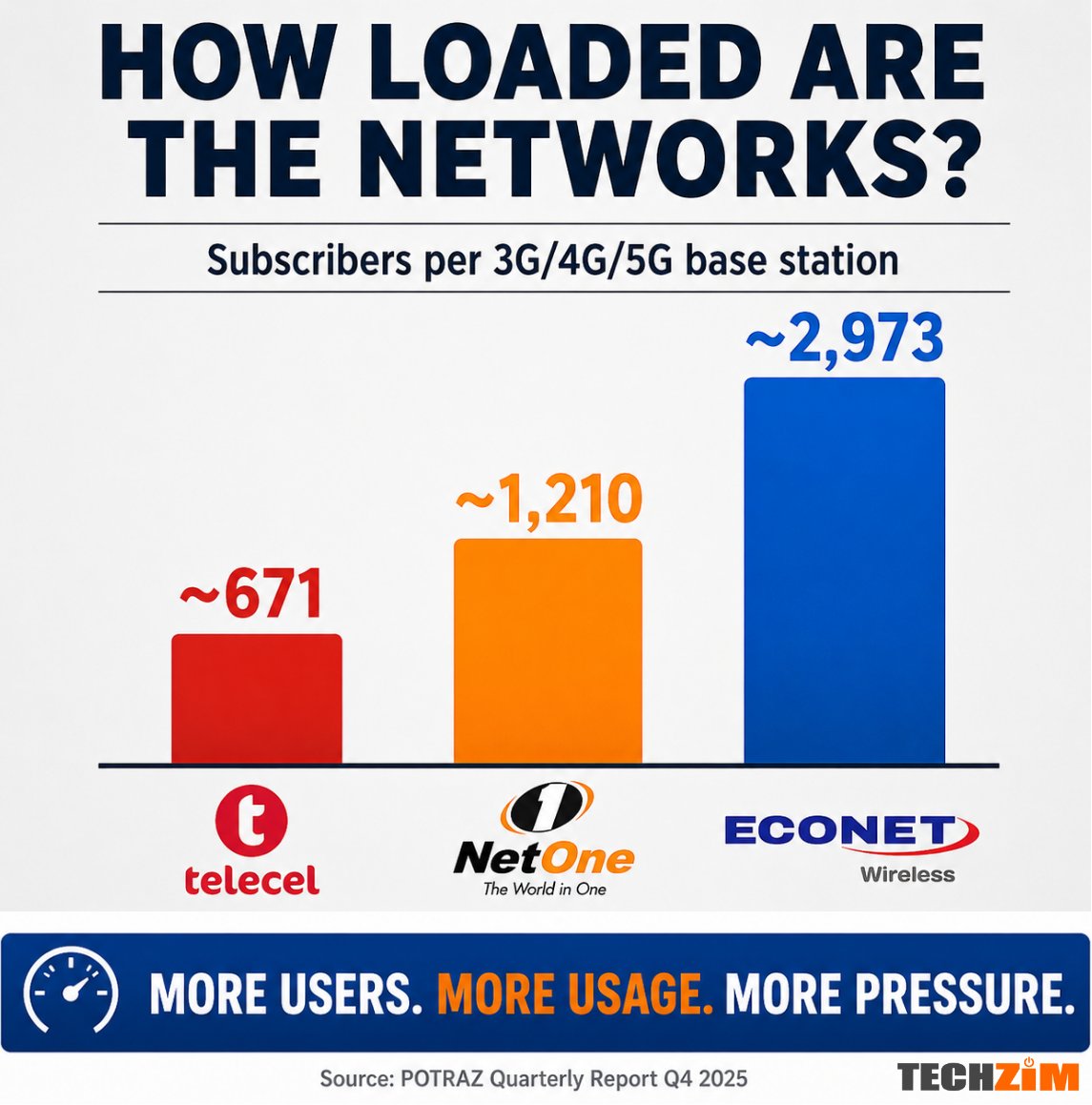

May 9

Yes Econet carries more load per site. But "more" doesn't tell you where. One corridor. 750 homes → 3,900 in five years. Same 3 base stations serving all of it. Throw in Food Lovers on a Saturday and the maths stops working completely.

As we were saying, this doesn’t prove Econet is overloaded everywhere

But when one network has far more users per data-capable site, and those users also generate far more traffic, it helps explain why some areas feel unusable at peak hours

2

4

14

3,043

DeepDiveData retweeted

Apr 29

@memorynguwi The data actually explains why this happens.

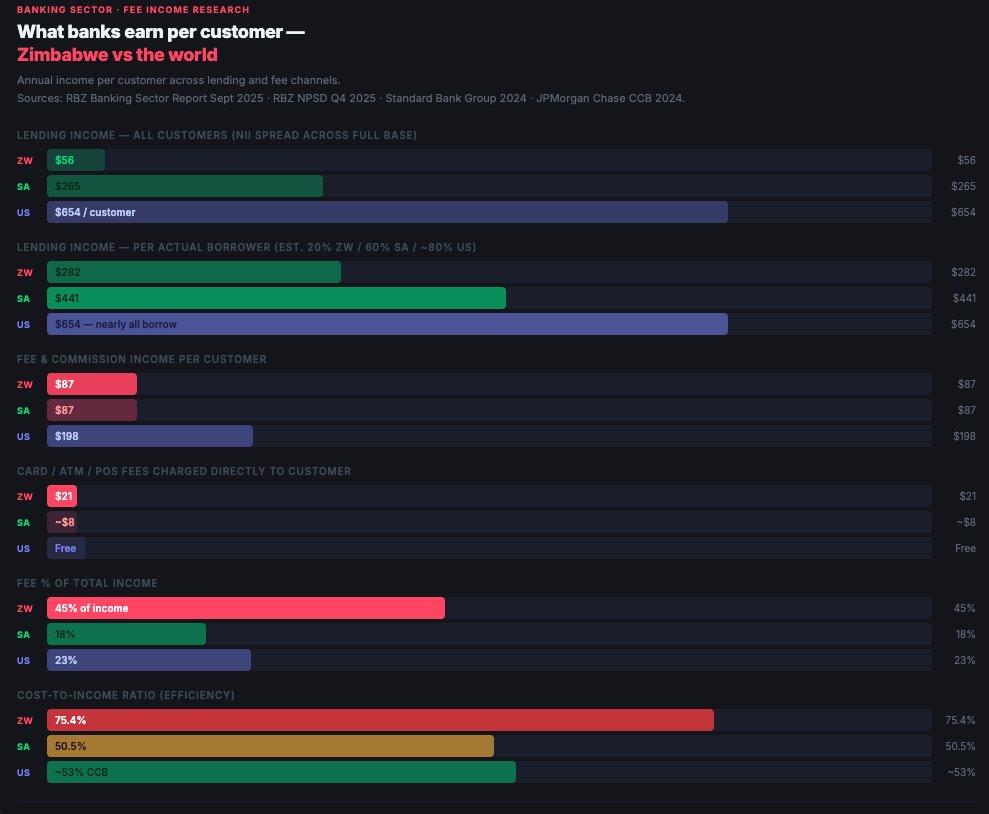

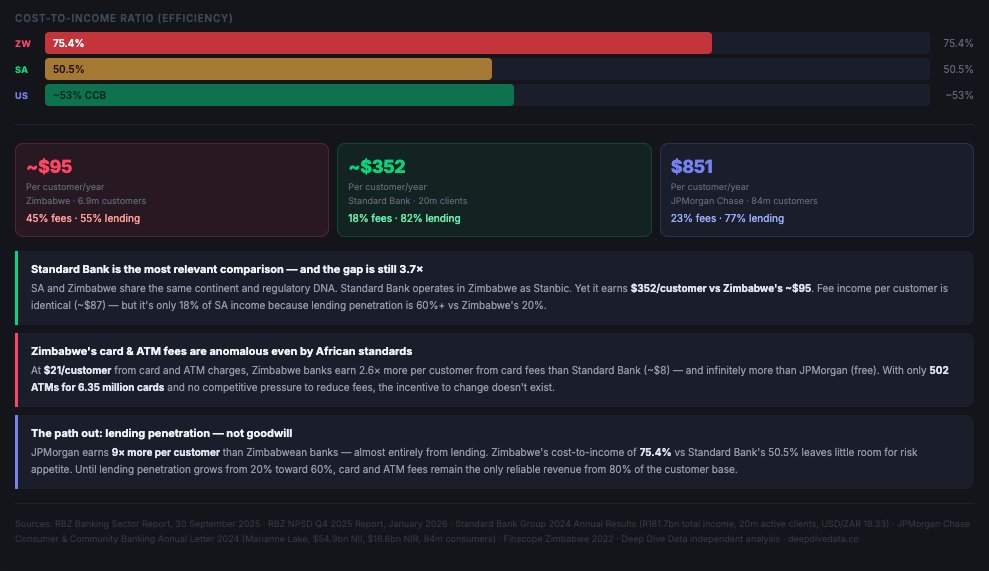

Zimbabwe banks earn ~US$95/customer/year.

45% of that comes from fees, card charges, ATM withdrawals, and POS swipes. Only 20% of customers have loans.

So the 80% who don't borrow? Fees are the only way the bank makes money from them. That's why the spread between lending rates (20% ) and deposit rates (<5%) is so wide banks aren't competing for deposits; they're monetizing transactions instead.

Compare: Standard Bank SA earns $352/customer. Fees are only 18% of income because 60% of customers borrow. More lending = less pressure to charge fees on everything.

Until ZW banks grow their lending book beyond the current 20% borrower base, fees will stay high and deposit rates will stay low. The incentive to fix it doesn't exist yet.@DeepDiveDataZW

1

11

39

3,259

DeepDiveData retweeted

Apr 29

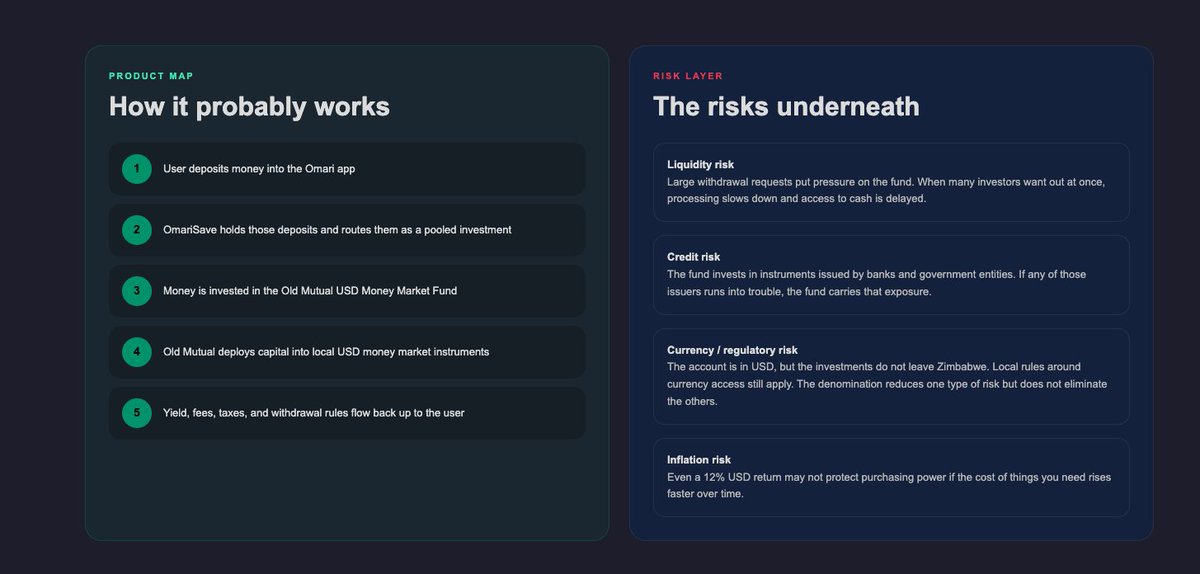

Worth noting: OmariSave isn't a savings account. It's a pooled investment into a money market fund with liquidity risk, credit risk, and USD that never actually leaves Zimbabwe. The 12% headline also shrinks after fees and withholding tax. Broke it down here: deepdivedata.co/articles/oma… @DeepDiveDataZW

2

3

190

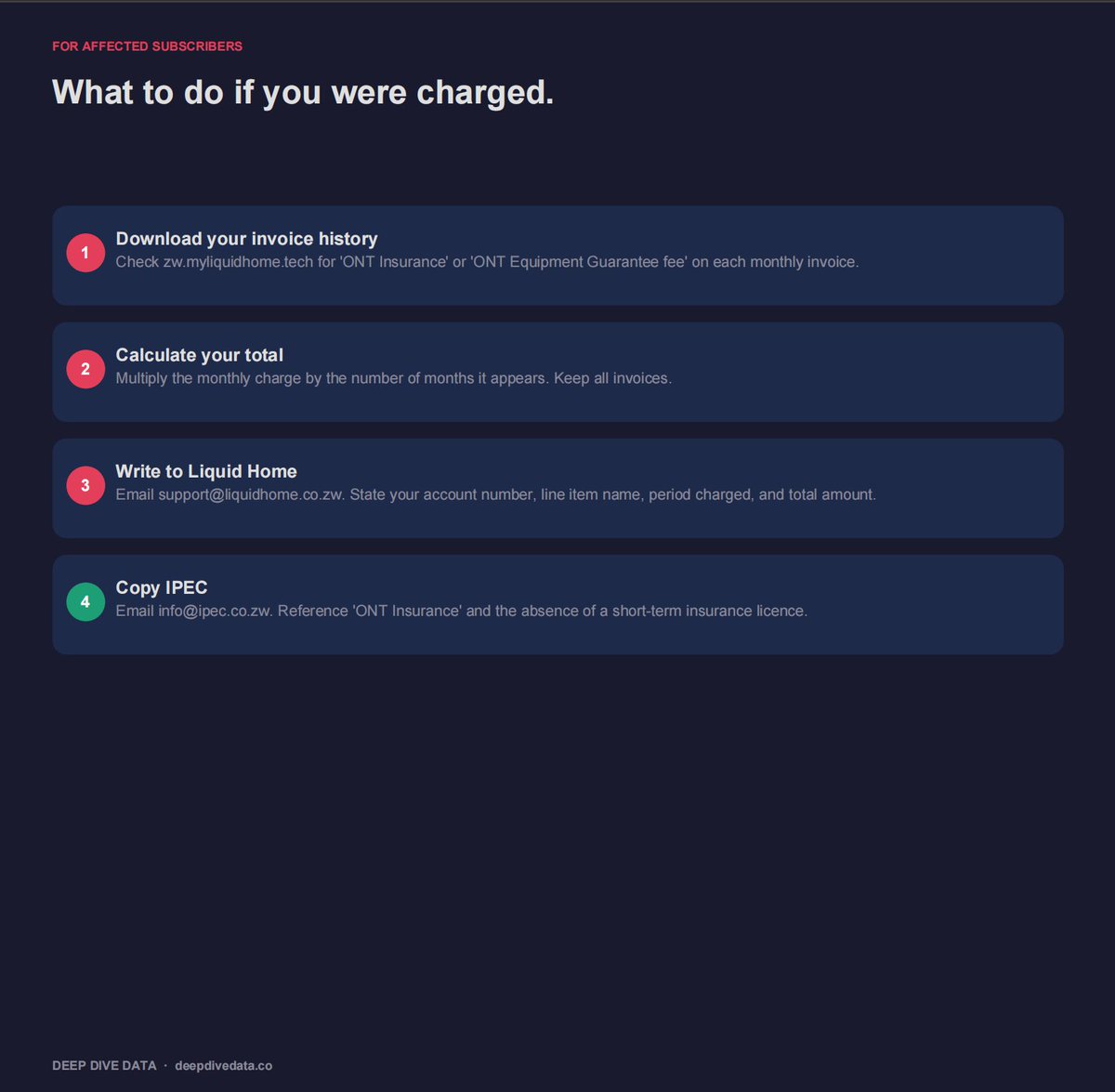

Apr 27

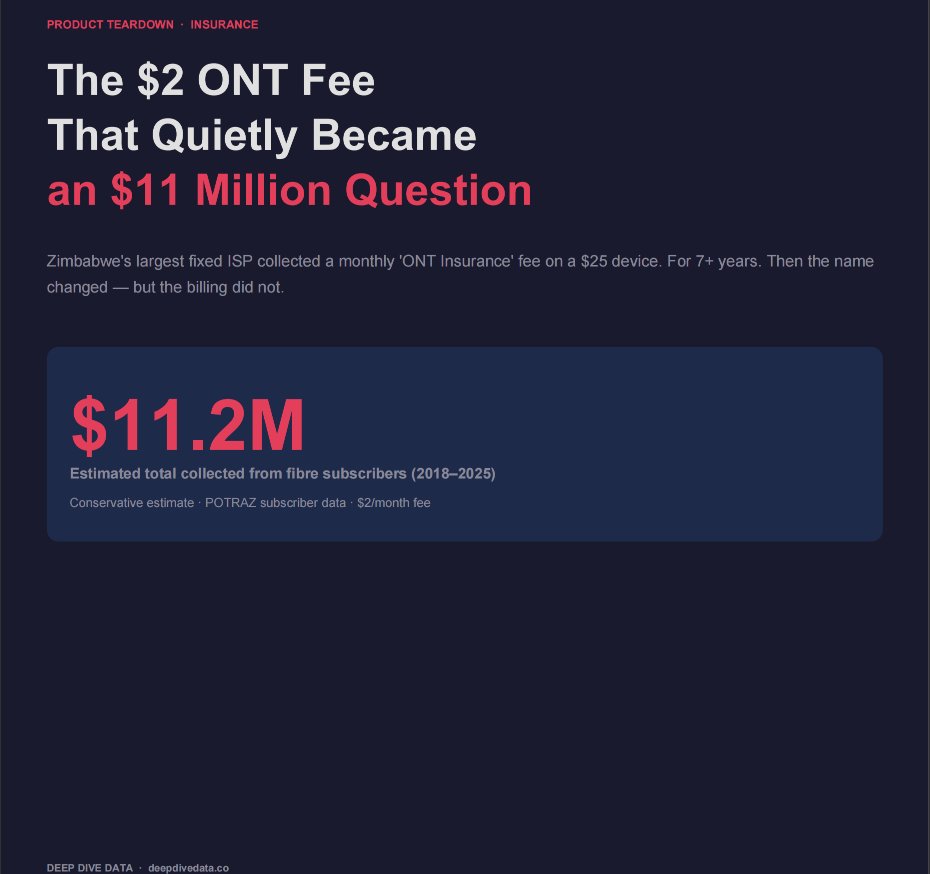

1/ ~$11.2 million.

That’s a conservative estimate of what a $2/month fee generated from fibre subscribers in Zimbabwe.

It was called “ONT Insurance.”

The device is worth ~$25.

🧵👇

1

1

6

947

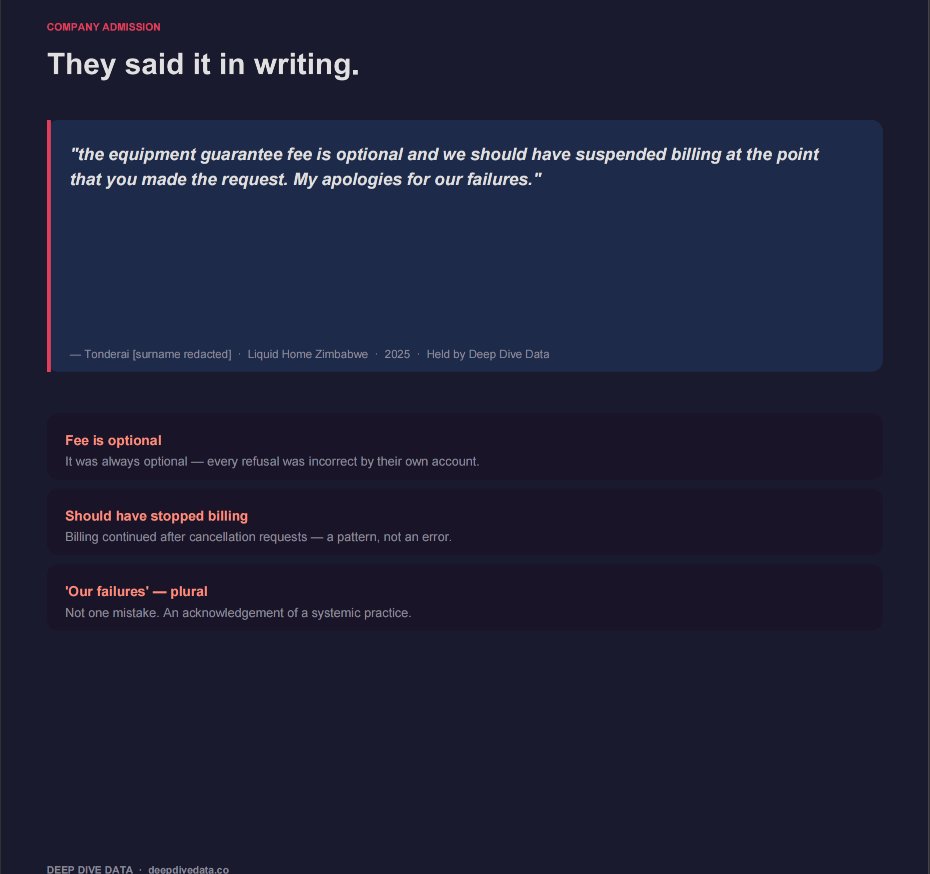

Apr 27

7/ Regulatory engagement later clarified: 👉 This was not an insurance product Despite being billed as “insurance” for years.

The structure raises questions: • Not priced like insurance

• Not aligned to asset value

• Not consistently cancellable

• Not described as optional

1

4

123

Apr 27

8/ It starts as $2/month. It scales into ~$11 million. That’s the power of:

• small recurring fees

• large customer bases

• time

Full breakdown: 👉 deepdivedata.co/articles/liq…

If you’ve ever used ZOL/Liquid Home, it’s worth checking your old invoices.

6

114