—— Quant Dev | Crypto hft —— “Give a man an alpha, feed him for a day. Teach a man to find alpha, feed him for a lifetime."

Joined October 2021

- Tweets 578

- Following 122

- Followers 4,731

- Likes 1,030

73 Photos and videos

Jun 6

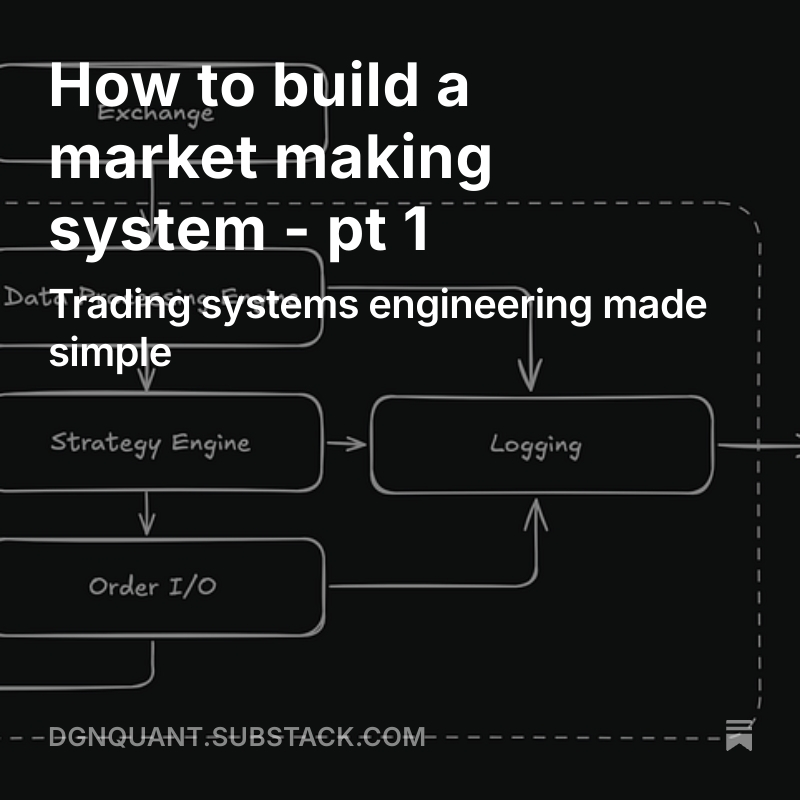

Thinking about getting back to writing the series on building trading systems!

4

17

825

May 28

It’s kind of insane how much work it’s been to build out systematic strategies on prediction markets. Definitely the most nuanced trade I’ve ever worked on

3

16

2,437

May 24

It really doesn’t feel bad picking off vibe coder mm’s in a market with a 250ms taker speedbump

6

117

15,377

Mar 8

If someone calls their trading system a bot, ignore everything they have to say

3

12

1,495

Jan 15

Working in rust over c was definitely the worst career decision I’ve ever made.

The job market for rust is pretty much dead, feels like I’ve just wasted years of my life

11

82

14,797

19 Dec 2025

For quant trading, it isn't necessarily -EV in the long run even if you're a losing trader initially. The experience gained in trying to run a systematic trade on your own is arguably the best education (coding, research, data analysis, system design).

18 Dec 2025

This is correct advice. For 99.99% of people, if you are not a professional trader (as in, you are employed by a firm to trade their capital, or you run such a firm) then active trading is -EV for you, and the more you trade, the more -EV it is.

1

6

3,018

19 Dec 2025

In the process you'll sharpen your skills and figure out what you're good at. I originally thought I wanted to be a quant researcher, but in the process of building maker strats I realized I'm far better at coding and designing systems than I am at math.

1

3

1,230

19 Dec 2025

Trading on my own (systematically) gave me the experience which ultimately allowed me to land a job as a quant dev. If you're interested in trading, do it on your own, make sure the inevitable lessons learned don't bankrupt you.

2

1,151

8 Sep 2025

I find it hilarious when engineers / researchers from other industries think they can just build a trading system and print money. There are a lot of smart, hard working people trying to make money in hft, do not underestimate how difficult it will be to compete.

10

2

115

9,709

2 Sep 2025

c is the ugly girl who’s dad is a PM at tier 1 hedge fund / prop shop, you don’t really want her but it’s prob in your best interest to tell yourself you do

6

4

172

12,472

26 Aug 2025

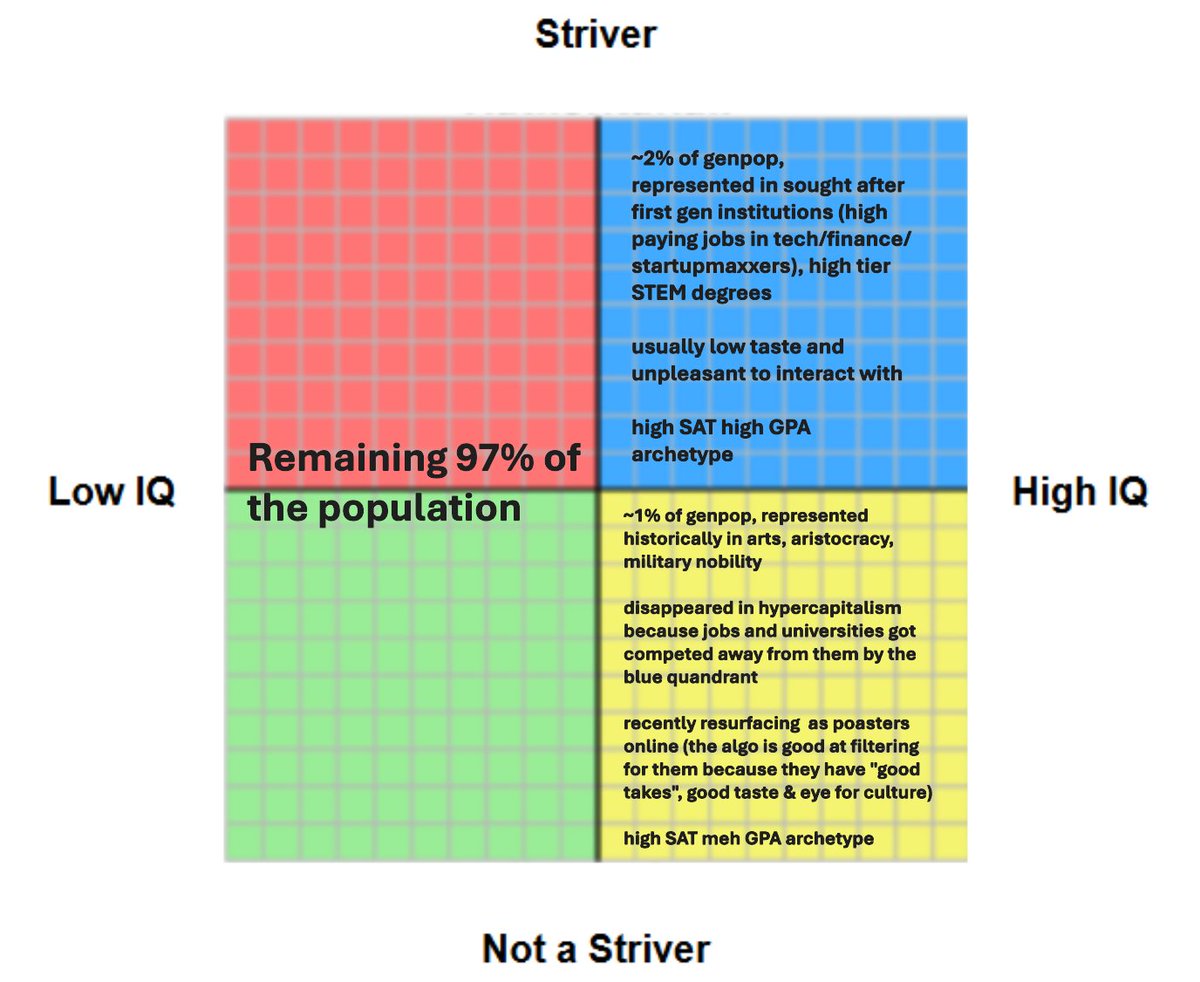

“unpleasant to interact with”, this is just cope, being a self proclaimed intellectual doesn’t preclude you from developing a personality. Being abrasive objectively makes your life and career worse, if you were so smart you’d figure out how to be both competent and personable.

25 Aug 2025

before the 2020s, you only had two options:

1. filter your environment through traditional institutions and interact with the blue quadrant

2. don't filter at all and interact with the statistical average (red/green quadrants)

everyone justifiably preferred the former, lesser of two evils

the internet has gone mass-mainstream now, and the algo has allowed for a third option -- the yellow quadrant -- which has made everyone realize how much they actually hate the blue quadrant

3

29

4,727

17 Aug 2025

There won’t be a second date, but at least now she knows what a matching engine is

16 Aug 2025

There won’t be a second date, but at least now she knows what a leveraged buyout is

23

3,064

17 Aug 2025

I wouldn’t say fitting a linear regression is premature optimization. Complexity isn’t about how many lines of code it takes. Fitting a 100,000 dimensional second order cone is immensely over complex when you should just model the data that matters directly.

16 Aug 2025

Agreed.

One requires modelling of exogenous variables though which is a lot of work while this can be done in literally just 3 short lines of code.

Always test the simplest solution to something first and if you get positive results *and* can improve on the simple method significantly then you can move on to more comlex methods.

Premature optimization is the root of all evil.

3

17

4,786

17 Aug 2025

With a pure time series approach like an ema, there’s a trade off between a half life so short that you trade on noise and so long that your model is slow to adjust when breaks occur.

1

2

1,175

17 Aug 2025

Trying to identify breaks and adjust your model’s half life based on the time series alone, which is effectively what you’re doing, is something that doesn’t work well and overfits in practice because you’re not conditioning on data that is actually driving the fair value

4

1,137