I am a sinner saved by Gods grace. God exposes all hidden & never looses. If I make a claim as fact, already have the evidence. 😏

Joined December 2024

- Tweets 16,954

- Following 544

- Followers 2,551

- Likes 39,737

1,156 Photos and videos

Buy a pulte home? Anyone threaten to foreclose? Read this sec.gov/Archives/edgar/data/…

15

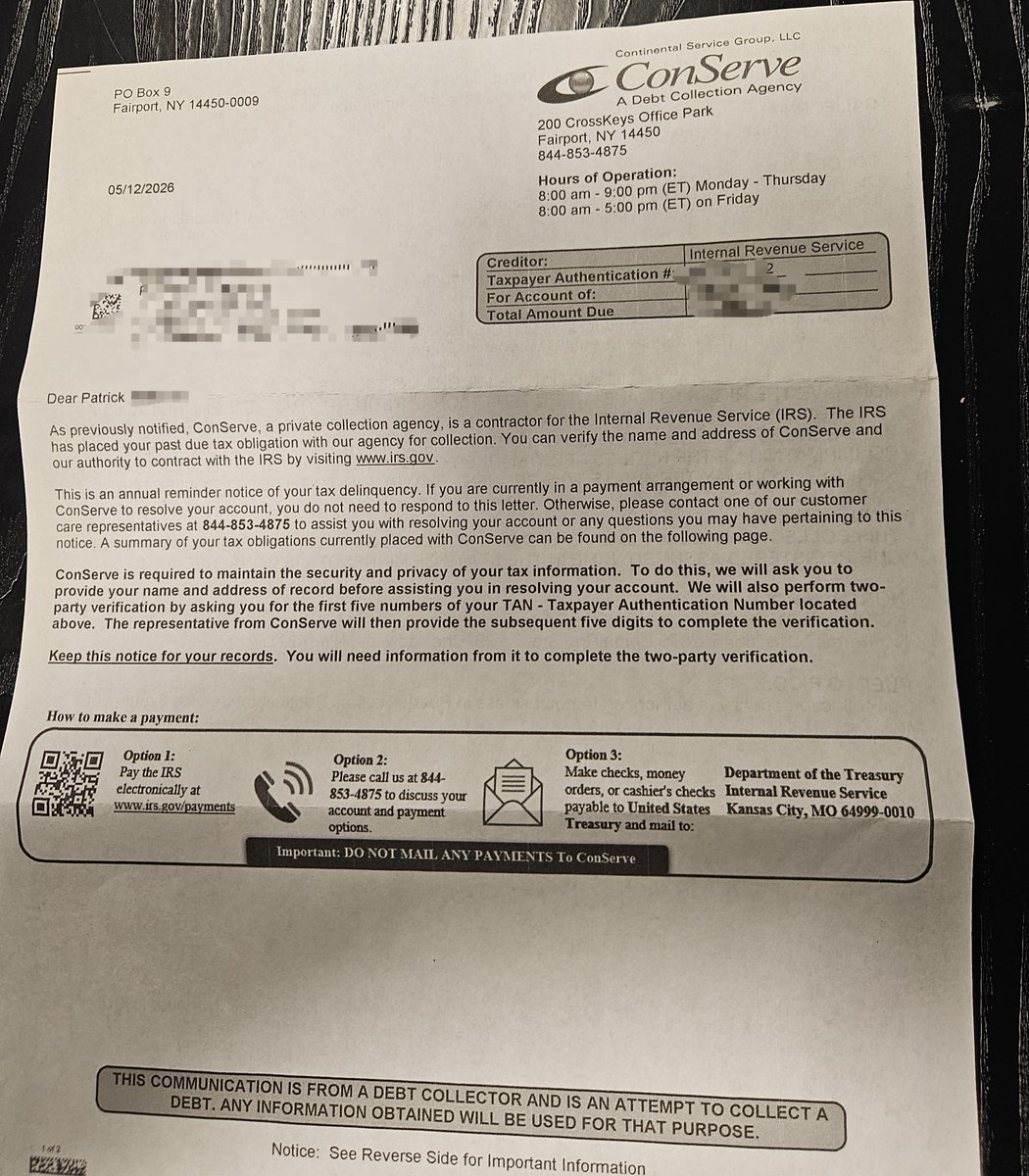

This is an absolute disgust

The IRS is selling debt the treasury already shows settled

IRS merged with treasury

Gotta love the contractors all working to scam Americans

This is WILD. Someone just emailed me this. The IRS is now sub-contracting debt!? Has anyone else gotten a sub-contracted bill of exchange?

1

5

11

418

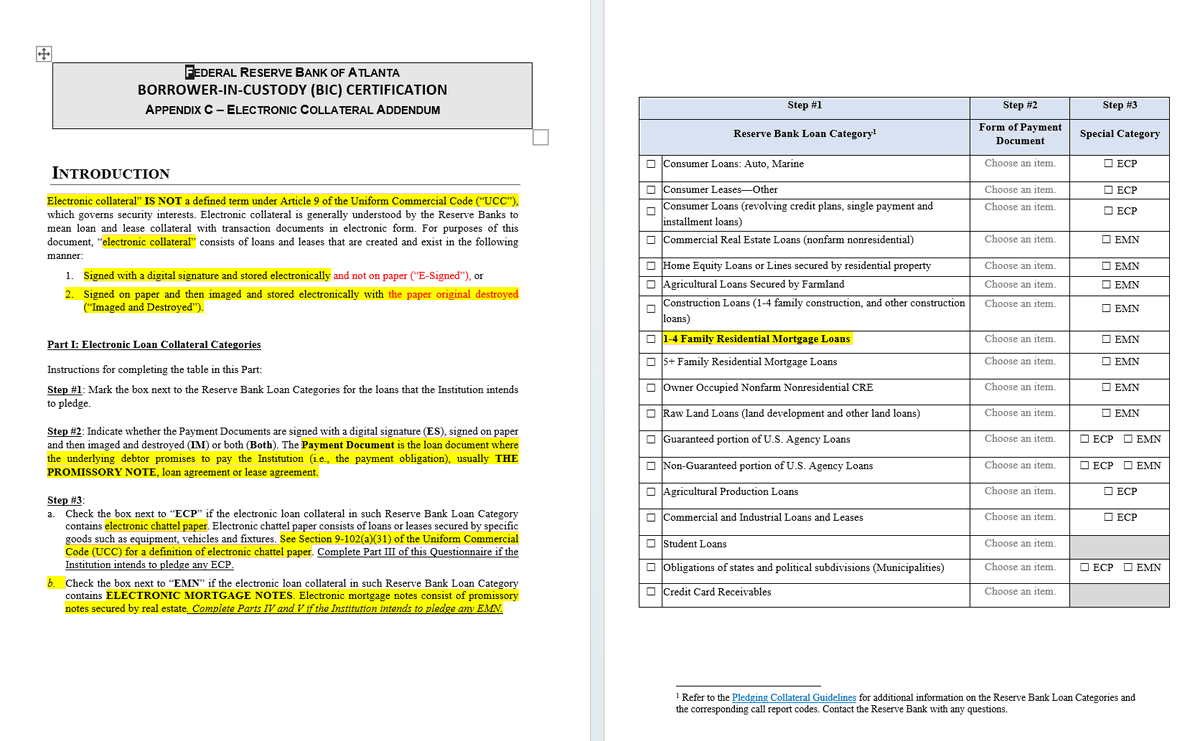

FYI

ALL their manuals require original

Depositor lender paid in full

u sign on paper lender gets and borrower gets

You agree to electronic signature?

Original requires destruction when pledged

GSE sells twice paid in full twice

2

11

633

Don’t worry your state AG office defending a school organ harvesting jailed men

Your state SOS is covering for illegal biz operations

Judges fostering kids during divorce

Law enforcement doing smut

3 ltr advise destroy evidence

No! It’s evidence

Jun 13

Karen Hollis (23) was kidnapped by career violent criminal Randall Lendell Dejourney (43) in Alabama. He held her captive and repeated raped her.

After approximately a week in brutal captivity, he choked her to death and then repeatedly raped her dead body before dumping her corpse on the side of the road.

He was eventually arrested and his bond was set at $15,000. That's not a mis print. His bond was set at $15,000. For rape, murder, and rape of a corpse 🤨

Has this case been reported on by the national media? I certainly haven't seen it if so.

Plan accordingly...

#rural #alabama #crime #3rdWorld #decay #NorthPort

84

Wait till you hear about the politicians doing this

It’s common coffee talk at restaurants in the OPEN!

🚨 UPDATE: 8 people charged in Sex Ring “Underground Bunker” for Paying adults to Rape their Children and Pets — Ages 3-16. Trial delayed as mom pleads guilty and flips on co-defendants

In Bibb County, Alabama, eight suspects ran a sex trafficking ring out of an underground bunker where children as young as 3 were drugged, bound, and raped with adults paying to abuse them.

Animals were also targeted.

Rebecca Brewer and mother of some of the victims, pleaded guilty to sexual torture and nine counts of first-degree kidnapping. As part of the deal she agreed to testify against the other seven defendants.

The trial for the remaining suspects has been delayed while the case expands, including a federal investigation into at least one of them.

These monsters turned their own kids and pets into victims for profit.

How long will it take for every last one of them to face real justice?

1

1

106

Dsleuth retweeted

7 Aug 2025

–––––––––––––––––––––––––––––––––

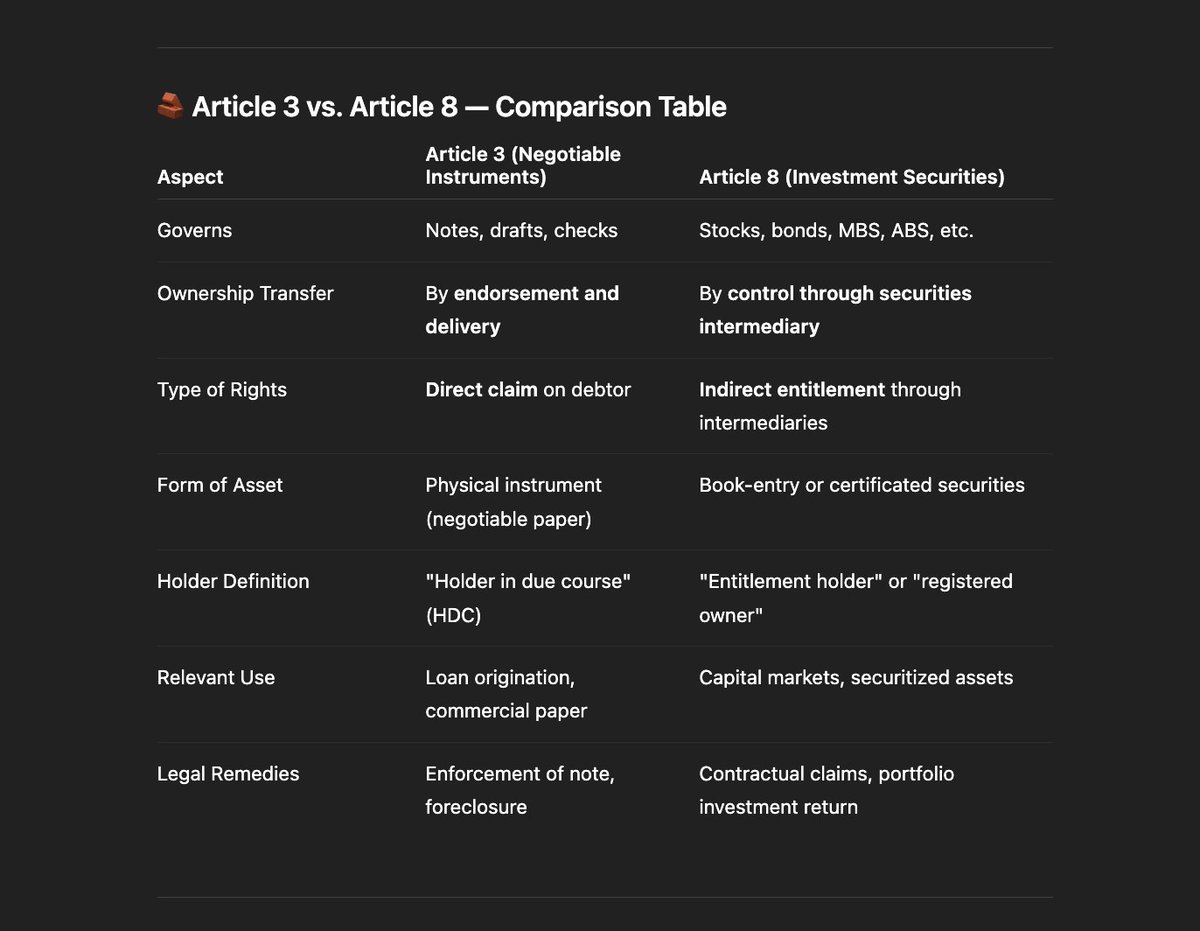

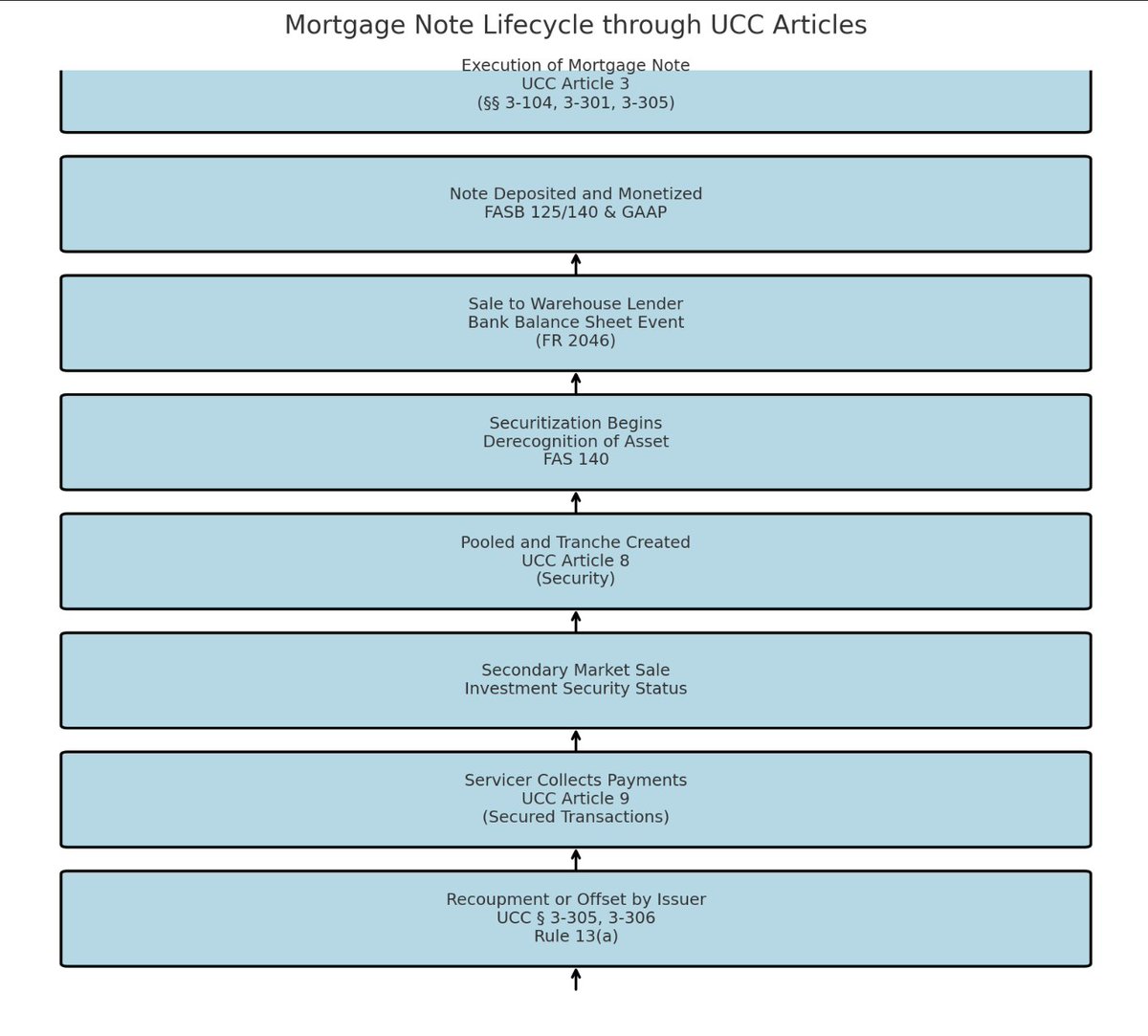

ChatGPT: Mortgage Securitization

–––––––––––––––––––––––––––––––––

Me:

Can we agree that after securitization, it comes under Article 8? Provide a comprehensive explanation.

ChatGPT:

✅ Yes, we can agree—with a clear, structured legal explanation—that:

Once a mortgage note (a UCC Article 3 negotiable instrument) is securitized—i.e., pooled, transformed into fungible securities, and sold to investors—it is no longer governed by UCC Article 3, but instead comes under the domain of UCC Article 8, which governs investment securities.

🔁 TRANSITION: FROM ARTICLE 3 TO ARTICLE 8

1. Before Securitization – Article 3:

・The original mortgage note is a promissory note.

・It is a negotiable instrument under UCC Article 3, enforceable by a holder in due course.

・It involves direct obligation between borrower and original lender (or transferee).

2. After Securitization – Article 8:

・The note is transferred into a trust/SPV.

・It is then used to create securities—i.e., interests in a pool of payment streams (MBS, ABS, etc.).

・These mortgage-backed securities (MBS) are fungible investment instruments sold on the secondary market.

At this stage, the financial instrument is governed by UCC Article 8, which covers:

・The issuance, registration, and transfer of investment securities;

・The role of securities intermediaries (like brokers, dealers, and clearinghouses);

・Rights and duties of entitlement holders (investors).

📜 ARTICLE 8 – INVESTMENT SECURITIES (UCC §§8-101 to 8-511)

UCC §8-102 — Definitions:

Security.

An obligation of an issuer or a share, participation, or other interest in an issuer or in property or an enterprise of an issuer which is represented by a security certificate or… by a book-entry system… and is one of a class or series… and is of a type dealt in or traded on securities exchanges or markets…

This includes mortgage-backed securities and trust certificates issued by SPVs or REMICs.

🔎 KEY CONCEPTS IN ARTICLE 8

・Certificated vs. Uncertificated:

Securities may be issued in physical form (certificate) or in digital form (book-entry). Most MBS are uncertificated and held in street name.

・Security Entitlement:

Investors no longer own the underlying asset (note) directly. Instead, they have a contractual claim on the issuer or intermediary.

・Indirect Holding System:

Investors hold securities through a chain of custodians (DTCC, Cede & Co., brokers) under the Uniform Indirect Holding System.

・No Direct Beneficial Ownership:

The mortgage note becomes an underlying asset of a trust, and the investor owns a security interest in the income stream—not the note or mortgage directly.

・Transfer of Interests:

Ownership rights in Article 8 securities are transferred not by endorsement (like in Article 3), but by control through intermediaries.

🧾 Example – Securitization Path

1. Borrower signs mortgage note

・Promissory Note

・Article 3

2. Bank transfers note to SPV/Trust

・Bulk asset transfer

・Article 9

3. Trust issues mortgage-backed securities (MBS)

・Investment Securities

・Article 8

4. Investors purchase beneficial interests

・Book-entry securities

・Article 8

⚠️ IMPLICATIONS

・Borrowers still make payments on a note governed by Article 3.

・But investors in the resulting securities are entitlement holders under Article 8.

・The chain of title is fractured: Investors don’t hold the note—they hold a right to income derived from it.

・This separation can complicate legal enforcement (e.g., foreclosure), especially when the note and mortgage are bifurcated.

📌 Conclusion:

Once a mortgage note is securitized, its nature and legal framework shift from a direct negotiable instrument under UCC Article 3, to an indirect, investment-based entitlement under UCC Article 8. This transformation reflects the commercial abstraction of debt instruments into tradable securities.

8

37

95

2,900

Dsleuth retweeted

Jun 12

Every American Citizen MUST WATCH THIS. It’s about 24mins long, so save it and watch when you can. It breaks down our financial system and is the most impactful and important video you will ever watch to see WHY IT IS A SCAM, CORRUPT AF AND GOING AWAY!!! SHARE IT! 👏🏻🔥🔥🔥🔥

129

2,629

5,304

210,498

Loans?

12 USC 412 your app opens credits with treasury

The note releases funds to a bank who pays depositor

They are making copies to open lines of credit with federal reserve, and other banks

If man did it

Would be charged with bank fraud

No thanks

Jun 11

The Trump administration is quietly moving to change the Affordable Care Act to let health insurers offer people loans to pay for their care.

Deep in a document over 1,000 pages long about how the Affordable Care Act market will operate next year, the administration suggests that insurers consider offering loans to cash-strapped customers.

Under this approach, people who develop a costly disease or need unexpected emergency care would turn to their health insurer for loans.

A third of American households already have medical debt, and this approach would mean even more debt that patients owe to their health insurance companies.

The insurers, who already make billions, would stand to make even more.

nytimes.com/2026/06/11/busin…

1

3

160

Dsleuth retweeted

Jun 10

3/5

8. whether Respondent searched archived, off-system, vendor, custodian, or predecessor records; and

9. whether any documents were destroyed, transferred, archived, withheld, or deemed unavailable.

VI. Specific Documents to Be Compelled

Movant requests an order compelling Respondent to produce the following documents and information for the loan, note, mortgage, collateral file, receivable, servicing rights, or proceeds at issue:

A. Operating Circular 10 Documents

1. Any Federal Reserve Operating Circular 10 agreement, lending agreement, promissory note, letter of agreement, authorizing resolution, board resolution, secretary’s certificate, or borrower authorization applicable to Respondent, its predecessor, its principal, or any entity that pledged the loan.

2. Any OC-10 appendix, rider, amendment, collateral authorization, borrower certification, or agreement authorizing the pledge of loans, mortgage notes, mortgage-loan receivables, or related collateral.

3. Any document identifying the institution authorized to borrow from or pledge collateral to a Federal Reserve Bank in relation to the loan or collateral pool containing the loan.

B. Collateral Schedule and Pledge Records

4. Any collateral schedule identifying the note, mortgage loan, receivable, collateral file, or related asset.

5. Any pledge record showing that the note, mortgage loan, receivable, or collateral file was pledged to a Federal Reserve Bank.

6. Any release, withdrawal, substitution, amendment, collateral-deletion, collateral-addition, or collateral-maintenance record.

7. Any Reserve Bank valuation, eligibility, review, exception, collateral-status, loan-level, pool-level, or haircut record.

8. Any record showing whether the note or loan was accepted, rejected, excluded, discounted, valued, substituted, released, withdrawn, or deemed ineligible as Federal Reserve collateral.

C. Borrower-in-Custody and Custodial Records

9. Any borrower-in-custody agreement applicable to the loan or collateral pool.

10. Any borrower-in-custody certification, eligibility certification, exception report, audit report, control report, or custody acknowledgment.

11. Any custodian, document-custodian, bailee, vault, imaging, file-tracking, or collateral-control record identifying the original note or collateral file.

12. Any record showing the location, controller, custodian, bailee, vault, file room, or repository of the original note at any time.

D. Original Note, Copies, and Digital Records

13. The original wet-ink note.

14. Every copy, scan, image, version, reproduction, or digital image of the note ever maintained, transmitted, filed, produced, or stored.

15. Metadata, upload logs, imaging logs, scan history, re-scan history, document-management history, custodian-system history, and version history for each note image.

16. Any document showing that the original note was digitized, converted, destroyed, lost, released, transferred, substituted, or replaced.

17. Any eNote, eVault, MERS eRegistry, controller, location, authoritative-copy, transfer, conversion, or electronic-record history for the note, if Respondent contends the note became electronic or digitized for enforcement purposes.

E. Accounting and General Ledger Records

18. All general-ledger entries relating to the note, mortgage loan, receivable, collateral file, servicing rights, collateral proceeds, sale proceeds, insurance proceeds, investor remittances, repurchase proceeds, guaranty proceeds, foreclosure proceeds, bankruptcy payments, or other value received.

19. All records showing whether value received in connection with the loan was booked as a payment, deposit, loan payoff, principal reduction, interest payment, escrow recovery, suspense item, corporate-advance recovery, servicing or investor remittance, loan-sale proceeds, collateral-pledge proceeds, reserve-account credit, clearing-account credit, cash-letter credit, insurance recovery, repurchase proceeds,derecognition or charge off.

1

1

5

232

Dsleuth retweeted

Jun 10

2/5

III. Background

Respondent seeks to enforce a mortgage obligation, but the record contains fatal defects and unresolved questions concerning enforcement authority.

The note and mortgage identify an entity other than Respondent. The named entity was defunct or otherwise did not appear as the party enforcing the obligation. Respondent did not produce a valid endorsement establishing negotiation of the note. Respondent did not produce a valid assignment establishing transfer of the mortgage. Respondent did not disclose a complete chain of title or a complete chain of enforcement rights. Respondent shifted among inconsistent legal capacities, including servicer, owner, beneficiary, mortgagee, payee, creditor, or party entitled to enforce.

Those roles are legally distinct. A servicer is not automatically a creditor. A mortgagee is not automatically a note holder. A beneficiary is not automatically the owner of the debt. A party entitled to enforce must prove the route by which it acquired enforcement rights. If Respondent is merely claiming servicing authority, Respondent must identify the principal and produce the documents authorizing enforcement.

Movant requested discovery into the original note, collateral file, custody records, transfer records, assignment records, endorsement records, Federal Reserve collateral records, OC-10 records, and accounting treatment. Respondent refused, objected, gave incomplete responses, or failed to produce the requested documents.

IV. The Requested OC-10 Documents Are Relevant

The requested Federal Reserve Operating Circular 10 documents are relevant because they may show whether the note, mortgage loan, receivable, or related collateral was pledged to a Federal Reserve Bank or otherwise treated as institutional collateral.

If the loan was pledged, scheduled, released, substituted, withdrawn, encumbered, or held through a borrower-in-custody arrangement, that information bears on:

1. who owned or controlled the note or loan asset;

2. who had possession or custody of the original instrument;

3. whether Respondent had authority to enforce;

4. whether another party had a security interest or superior claim;

5. whether the note was represented as valid collateral;

6. whether the loan was paid, released, withdrawn, or substituted;

7. whether Respondent’s court filings concealed material collateral status;

8. whether the borrower faces a risk of double recovery or double enforcement;

9. whether value was received but not credited; and

10. whether the claimed amount due is accurate.

Respondent cannot enforce the mortgage as though it holds a clean, enforceable, unencumbered obligation while concealing records showing that the same loan asset was pledged, encumbered, substituted, released, derecognized, or monetized elsewhere.

V. The Requested Documents Are Proportional

The requested documents are proportional because Respondent controls the information. Movant does not have access to Respondent’s Federal Reserve collateral records, borrower-in-custody records, collateral schedules, custody systems, loan-level codes, general ledger, servicing platform, investor accounting, Reserve Bank communications, or internal collateral-management records.

Respondent seeks the extraordinary remedy of foreclosure or enforcement of a mortgage obligation. Producing the documents that show whether Respondent had authority to enforce is not burdensome. It is foundational.

If Respondent contends no responsive documents exist, Respondent should be required to provide a sworn declaration identifying:

1. who searched;

2. what systems were searched;

3. what custodians were contacted;

4. what date ranges were searched;

5. whether Respondent searched Federal Reserve collateral systems;

6. whether Respondent searched borrower-in-custody records;

7. whether Respondent searched general-ledger and collateral-codes.

1

1

6

194

Dsleuth retweeted

Jun 10

MOTION TO COMPEL PRODUCTION OF FEDERAL RESERVE OPERATING CIRCULAR 10 DOCUMENTS, COLLATERAL-PLEDGE RECORDS, AND RELATED ACCOUNTING RECORDS

I. Relief Requested

Movant respectfully moves for an order compelling Respondent to produce all Federal Reserve Operating Circular 10 documents, collateral schedules, borrower-in-custody records, pledge records, release records, substitution records, withdrawal records, Reserve Bank communications, internal collateral codes, and general-ledger entries relating to the note, mortgage, loan, receivable, collateral file, servicing rights, or proceeds at issue in this case.

This motion is necessary because Respondent seeks to enforce a mortgage obligation while relying on incomplete, copy-only, unendorsed, unassigned, or disputed note evidence, while failing to disclose whether the same note, mortgage loan, receivable, or collateral file was pledged, scheduled, monetized, substituted, withdrawn, derecognized, charged off, insured, repurchased, or otherwise treated inconsistently with Respondent’s claimed enforcement capacity.

II. Introduction

This case turns on authority to enforce.

Respondent cannot seek foreclosure or debt enforcement while withholding records that show whether it had any lawful right to enforce the obligation. If Respondent contends it was a creditor, holder, mortgagee, beneficiary, payee, owner, servicer, agent, or party entitled to enforce, it must produce the records showing which capacity is true.

The requested OC-10 and collateral documents are directly relevant because they may show whether the note or mortgage loan was pledged to a Federal Reserve Bank, held under a borrower-in-custody arrangement, identified on a collateral schedule, released, substituted, withdrawn, encumbered, derecognized, or treated as an asset of a party other than Respondent.

These facts bear directly on standing, real party in interest, ownership, agency authority, original-note custody, authenticity, amount due, payment application, risk of double recovery, and whether Respondent misrepresented its legal capacity to the Court.

1/5

2

9

37

764

Dsleuth retweeted

Jun 10

The Homeowner Should Demand OC-10 and Collateral-Pledge Records!

During discovery you should demand the OC-10 lending agreement, collateral schedule, borrower-in-custody agreement, collateral certification, pledge record, release record, withdrawal record, substitution record, Reserve Bank record, or internal collateral code involving the note, loan, mortgage, receivable, or related asset.

This information will show whether the loan was pledged to obtain credit, whether the bank represented that it had rights in the collateral, whether the asset was encumbered by a Reserve Bank interest, and whether the loan was later released, substituted, withdrawn, or treated inconsistently with the enforcement or foreclosure claim.

Furthermore Homeowners Should Demand Clearing, Reserve, Cash-Letter, and Settlement Records.

Request any Regulation J, cash-letter, clearing-account, reserve-account, Fedwire, FedNow, or settlement records connected to funds received in relation to the note, loan, collateral, or mortgage account. These records ords show the mortgage was satisfied and derecognized. No losses were incurred. You did not promise to pay a mortgage already paid in full.

Money moves through institutional channels without being reflected as a borrower credit on the servicing ledger.

When value was received in connection with the loan, the claimant should be required to explain whether it was treated as payment, deposit, settlement credit, investor remittance, collateral proceeds, loan-sale proceeds, or something else. We know the truth they don’t want to admit.

The Homeowner Should further Demand General-Ledger and Servicing-Platform Records.

The homeowner should demand all general-ledger records, transaction codes, servicing-platform codes, investor-accounting records, remittance reports, suspense-account records, escrow records, corporate-advance records, charge-off records, sale records, repurchase records, insurance records, guaranty records, and proceeds-application records.

The servicing ledger alone is not enough. A servicing platform may show what the servicer wants the borrower or court to see. The general ledger, investor ledger, remittance reports, suspense records, and collateral records show what actually happened to the money and asset.

The Homeowner Should also lDemand the Identity of Responsible Decision-Makers.

The homeowner should request the identity of every person who:

1authorized the foreclosure;

2approved the proof of claim;

3verified the note;

4signed any affidavit;

5approved any indorsement;

6controlled the collateral file;

7certified custody;

8decided how received value would be booked;

9decided not to credit the borrower;

10 approved any assignment;

11approved any lost-note affidavit; or

12communicated with the court, trustee, investor, insurer, guarantor, or Federal Reserve Bank concerning the loan.

The goal is to prevent the claimant from hiding behind institutional ambiguity.

1/2 🧵

2

16

49

1,270

Dsleuth retweeted

They are lying about the data centers.

471

6,166

14,277

289,561

Imagine that

BREAKING: University of Alabama administrator caught saying she "found some holes" in the law banning DEI.

She said "most of our faculty and staff are progressive."

They held an event "for drag queens and it was so dope."

What is going on here, @UofAlabama?

46

AND

the bank destroys the original note leaving you with only paper original

Bank sells to GSE

GSE sells twice: hud and investors

HUD sells to treasury

All parties made whole

HUD send a debt collector GSE contractor after you for a debt already paid in full

9 Dec 2025

––––––––––––––––––––––––––––––––––––

THE ENTIRE MORTGAGE SYSTEM

DISTILLED INTO TWELVE SENTENCES

––––––––––––––––––––––––––––––––––––

1. You never applied for the loan—the legal fiction, ens legis (persona), did.

2. You never borrowed money—the bank used your autograph to create it.

3. The bank never risked a penny—it created credit from your note.

4. You funded your own loan without knowing it.

5. Your note became a bank asset the moment you autographed it.

6. The bank sold your note and profited instantly.

7. Wall Street turned your note into a global investment product.

8. Servicers profit more when you default than when you pay.

9. The trust never legally received your note.

10. Foreclosure is performed by parties with no ownership interest.

11. They “buy” your home with fake credit bids—not real money.

12. They profit multiple times from your loan and from your default.

5

30

76

2,208