Joined December 2020

- Tweets 1,720

- Following 110

- Followers 371

- Likes 5,897

538 Photos and videos

Pinned Tweet

Apr 1

Smart market participants almost have to be the "observers" first and foremost. Strong opinions often get in the way of making money.

1

1

19

6,077

🅰️DJ🦑 retweeted

Encapsulation complete.

BlueBirds 8, 9, and 10 are now secured inside Falcon 9's fairing ahead of launch.

A stacked configuration powered by advanced carbon fiber structures, engineered to withstand ascent forces comparable to carrying a fully loaded space shuttle orbiter during launch. 💪

Next stop: launch. 🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀

Built in Texas. Broadband from space. Designed to connect directly to everyday smartphones. 🌎📶📱

#ASTSpaceMobile #Broadband #ConnectingtheUnconnected #BlueBirds

149

586

3,238

338,888

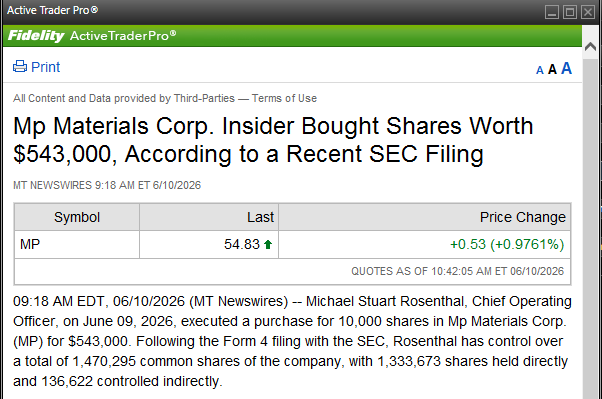

Jun 10

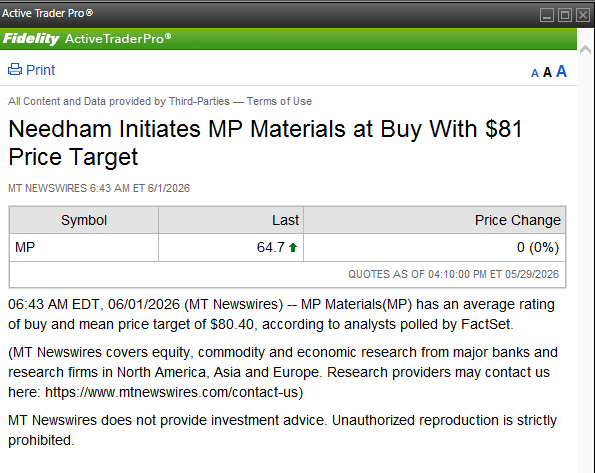

$MP - Mp Materials Corp. Insider Bought Shares Worth $543,000, According to a Recent SEC Filing

1

2

123

Jun 10

$PLTR - Live On CNBC, Palantir Technologies CEO Alex Karp Says "Most Of The Things Anthropic Talks About In Public Are Running On Palantir"

1

153

Jun 9

$ASTS - SpaceX open war on GLOBAL MNOs, shots fired!

🔫"All you do is put famous actors on your Ads or structure iPhone subsidy"

🔫"We are about to bring an actual Product, unlike you"

🔫"We want to make all your customer switch to StarLink Mobile"

🔫"We are pretty special, unlike you"

🔫"We are a game changer for entre mobility sector"

🔫"You have to come up with a solution to compete"

🔫"We are better for the consumer than you"

🔫"1.5T TAM per year and we about to take it from you"

🔫"We are attacking terrestrial markets that exist today on earth, from space"

🔫"OUR PRODUCT IS BETTER FOR EVERYBODY!"

Your move, $T $VZ $TMUS !

x.com/spacanpanman/status/20…

2

1

17

660

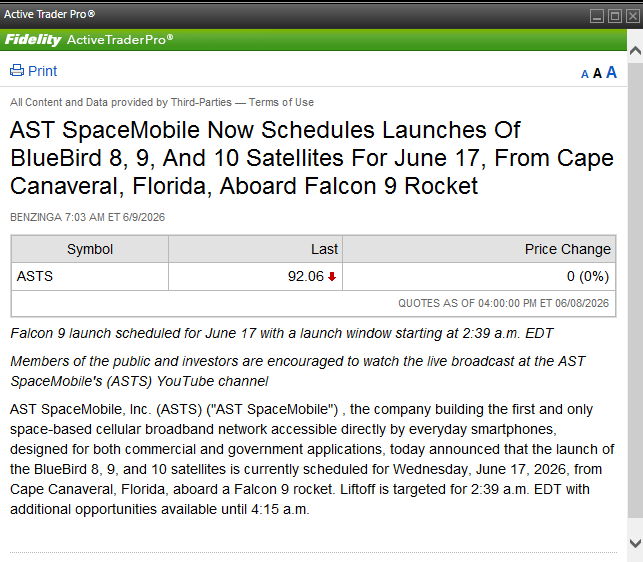

Jun 9

$ASTS - AST SpaceMobile Now Schedules Launches Of BlueBird 8, 9, And 10 Satellites For June 17, From Cape Canaveral, Florida, Aboard Falcon 9 Rocket

13

219

🅰️DJ🦑 retweeted

AST SpaceMobile Announces Launch Date for BlueBird Satellites 8, 9, and 10

businesswire.com/news/home/2…

204

579

3,124

473,463

Jun 9

$ASTS - biggest takeaway here is loud and clear acknowledgement of being "2 years away". The fact $SPCX was going after the MNOs we knew, but the market for the most part did not.

Are we still worried about "delays"?

Jun 8

$ASTS $SPCX:🚨 SPACEX CFO BRET JOHNSEN DISCUSSES PLAN TO ROLL OUT STARLINK MOBILE GLOBALLY TO COMPETE WITH MNOS OVER THE NEXT 2 YEARS

Starlink is focused on "attacking terrestrial markets" from space

Starlink Mobile will become "table stakes" and “others (MNOs)” will have to come up with comparable solutions to compete

Connectivity overall is a $1.6 trillion a year TAM

2

5

58

4,854

Jun 9

$ASTS - aged well and still spot on.

Jan 1

I believe $ASTS has a more effective scaling strategy compared to Starlink.

While Starlink has to sell to the consumer, through providers or direct, AST has to sell to providers/MNO. Once adopted, providers are incentivized to integrate the capability into their own Brand and make it available and included for all existing customers.

- Single "sale" for AST = millions of subscribers and immediate scale of revenue.

- Single "sale" for Starlink = 1 customer and small incremental scale of revenue.

The Starlink D2C model calls for rendering MNOs/Providers obsolete by going directly to the consumer. While on the surface it sounds like a great idea, the time to execute this (providing the tech is in place and scaled up to provide competitive service) is long and capital intensive.

AST D2C model calls for immediate scale, an "ON" switch that can be flipped to ALL customers in Provider's base. The only question for Providers becomes the "go to market strategy" - try and sell this as an "add on service" for an extra fee, or incorporate this into their network at no cost/minimal cost to the consumer, basically covering the revenue sharing side of AST and wait for the next pricing cycle update to integrate the cost into the plans.

Starlink's partnership with MNOs/Providers is dead. They all realize now that this is a clear attempt to circumvent them to access their existing customer base. Hence the strong Starlink brand push.

2

11

1,180

🅰️DJ🦑 retweeted

Jun 8

$ASTS $SPCX:🚨 SPACEX CFO BRET JOHNSEN DISCUSSES PLAN TO ROLL OUT STARLINK MOBILE GLOBALLY TO COMPETE WITH MNOS OVER THE NEXT 2 YEARS

Starlink is focused on "attacking terrestrial markets" from space

Starlink Mobile will become "table stakes" and “others (MNOs)” will have to come up with comparable solutions to compete

Connectivity overall is a $1.6 trillion a year TAM

72

90

736

350,404

Jun 8

$PDYN - Palladyne AI Collaborates With Israel Aerospace Industries To Produce, Integrate, Market HARPY, HAROP, Mini HARPY Loitering Munition Systems To U.S. Department Of War

237

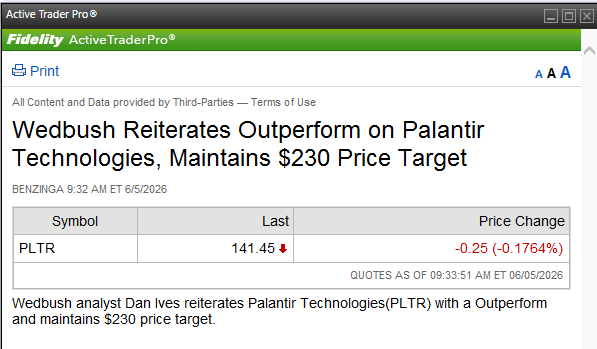

Jun 5

$PLTR - Wedbush Reiterates Outperform on Palantir Technologies, Maintains $230 Price Target

109

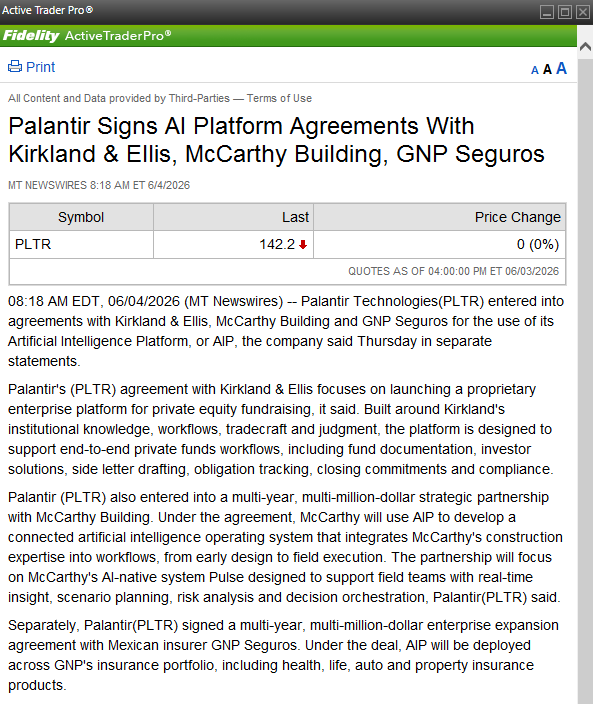

Jun 4

$PLTR - Palantir Signs AI Platform Agreements With Kirkland & Ellis, McCarthy Building, GNP Seguros

112

Jun 4

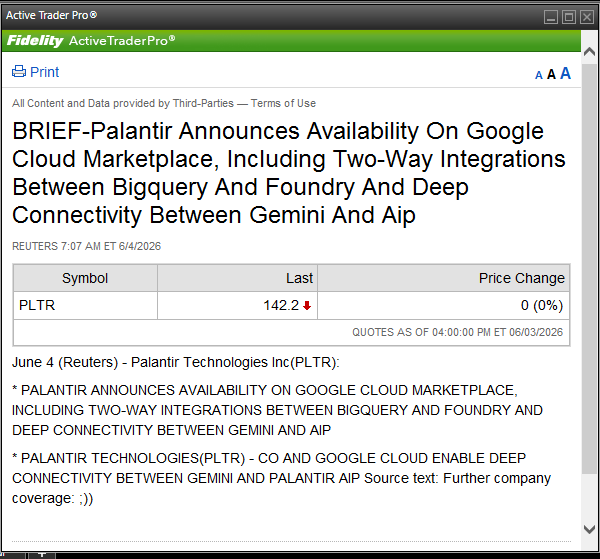

$PLTR - Palantir Announces Availability On Google Cloud Marketplace, Including Two-Way Integrations Between Bigquery And Foundry And Deep Connectivity Between Gemini And Aip

1

234

Jun 3

$ASTS - IMO the comment from the William Blair note:

"AST reiterated that it has a handful of launches over the remainder of the year with launch providers other than Blue Origin"

- is the reason stock is reacting now.

@AST_SpaceMobile - needs to clarify "handful" with a number and note if it includes the upcoming launches with SpaceX or the "handful" refers to ADDITIONAL launches.

7

1

33

4,549

Jun 3

$ASTS - first, this is what we were pricing in when BO blew up. So this is expected and actually MUCH better timeline that we got earlier. Second, I think this information should be disclosed to investors through filing or PR and not through an analyst .

@AST_SpaceMobile @scottwisniews

4

5

93

6,978

Jun 2

$ASTS - we had our pause/fud moment, its time to continue. While management did not provide color, the community, the #Spacemob did. As mentioned before, the trajectory here remained unchanged.

-"ATHs breed more ATHs". 🚀🎯

May 29

$ASTS - So the stock ended up reacting to the tune of 15% finding a bottom at $105 and bouncing back. While this creates a pause, it does not change the trajectory much. Look for management to shed some light on the "multiple launch vehicles negotiations". We did not get much detail on that other that the statement, but perhaps now the company will reveal the nature of these negotiation.

1

14

1,158

May 29

$ASTS - So the stock ended up reacting to the tune of 15% finding a bottom at $105 and bouncing back. While this creates a pause, it does not change the trajectory much. Look for management to shed some light on the "multiple launch vehicles negotiations". We did not get much detail on that other that the statement, but perhaps now the company will reveal the nature of these negotiation.

May 29

$ASTS - as soon as I type this we have an event. Seems like the stock will react to this.

"Blue Origin's New Glenn just blew up at LC-36 while attempting to Static Fire ahead of NG-4."

vxtwitter.com/nasaspacefligh…

12

2,529