Not a guru. Not an advisor. Just a retail investor with 20 yrs in Indian markets. I share what I notice. Your views welcome. Not SEBI registered.

Joined April 2020

- Tweets 1,061

- Following 26

- Followers 402

- Likes 6

493 Photos and videos

Pinned Tweet

Apr 22

What 20 years of reading charts AND balance sheets taught me:

1. Charts show direction. Results show truth. You need both.

2. A great chart with weak fundamentals = a trap.

3. Strong fundamentals with a broken chart = a patience test.

4. The best trades happen when technicals AND earnings align.

5. Most people chase price. Few study what drives it.

🧵

1

2

665

Edge Over Hype retweeted

ICICI Lombard Clarifies Motor Insurance Coverage with E-20 Fuel Usage

ICICI Lombard General Insurance reaffirms that motor insurance policies remain fully valid by the use of E-20 fuel. We further clarify that we do not treat usage of E-20 fuel in older vehicles as a negligence and we consider E-20 fuel program as a progressive environment friendly step .

Our insurance policies are designed to cover accidental damages, theft, personal accident for owner-drivers and co-passengers, as well as third-party liabilities, depending on the covers opted by the insured.

Claims are admissible based on the occurrence of insured perils such as vehicle accidents or theft. The type of fuel used in the vehicle such as Petrol, Diesel, CNG & so on is not a determining factor in claim admissibility. Accordingly, if a claim is admissible with conventional fuel, it is equally admissible with E-20 fuel and ICICI Lombard does not reject claims merely on the basis of fuel usage.

We remain committed to our ethos of customer trust and centricity.

1

10

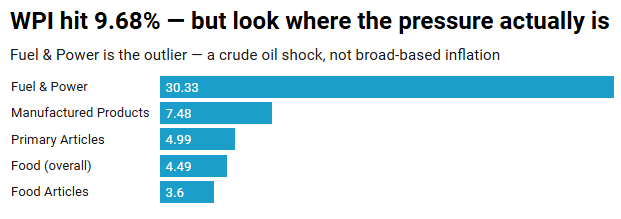

Wholesale inflation just jumped to 9.68% — the headline looks scary.

#WPI #Inflation #CrudeOil

But before you panic: almost all of it is coming from ONE place.

Here's the clear version 👇

Where the pressure actually is (May 2026, YoY):

→ Fuel & Power: 30.33% 🔴

→ Manufactured products: 7.48%

→ Primary articles: 4.99%

→ Food articles: 3.60%

See it? Fuel is the outlier. Everything else is far calmer.

The reason:

The West Asia crisis the effective blockade of the Strait of Hormuz — where most of India's crude oil comes in — has sent oil and petroleum prices soaring. That's spilling into chemicals and metals too.

So this is a crude oil shock, not broad-based inflation.

One thing to keep clear:

WPI is wholesale (factory-gate) prices — NOT what you pay at the shop. That's CPI, a different number. Food at 3.6% wholesale is the part that affects your kitchen more directly, and that's still moderate.

The catch:

If crude stays high, fuel costs eventually pass through into manufactured goods and food over the coming months. That's the transmission risk to watch.

Also worth bookmarking — India quietly debuted:

→ A new WPI base year (2022-23)

→ A new Output Producer Price Index (PPI)

→ Items expanded from 697 → 957, with solar, wind & nuclear now in the basket

So today's reading is also the first under a refreshed series — keep that in mind when comparing to old data.

Watch: crude / Hormuz situation — that's the single biggest swing factor here.

Next: whether high fuel starts leaking into core goods over the next 1–2 prints.

What matters more for the months ahead — this fuel spike, or whether it spreads into everything else?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

87

Important distinction a lot of people mix up: WPI ≠ CPI.

WPI tracks wholesale/factory-gate prices, CPI tracks what consumers actually pay — and RBI sets rates looking at CPI, not WPI.

So a hot WPI doesn't automatically mean a rate move.

The real bridge is whether this fuel spike eventually shows up in CPI.

11

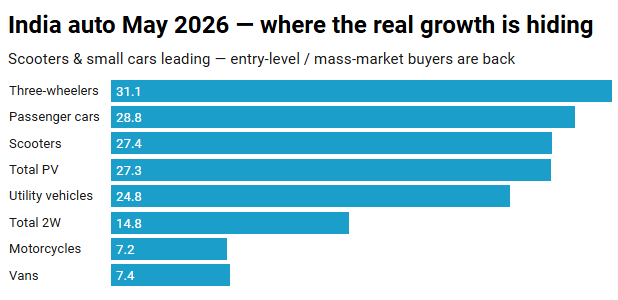

Auto sales just hit "record May" numbers — PV up 27.3% YoY.

#AutoSales #SIAM #IndianEconomy

But the headline number is a bit flattered. The real signal is inside the mix.

Here's what most people will miss 👇

First, the caveat:

Two reasons the % looks huge —

→ weak base last May (low comparison)

→ GST cut easier loans pulling demand forward

So 27.3% isn't pure organic strength. SIAM itself flagged the base effect.

Now the actually interesting part — WHO is buying:

→ Scooters 27.4% YoY

→ Passenger cars 28.8% YoY

→ Three-wheelers 31.1% YoY

Compare that to:

→ Motorcycles 7.2% YoY

→ Vans 7.4% YoY

See the split?

Scooters and small cars are firing. Motorcycles are crawling.

That's the signal: the mass-market / entry-level buyer — who was weak for years — is finally coming back. Three-wheelers ( 31.1%) usually track small-business and last-mile demand, so that's a healthy sign too.

Focus: not the 27.3% headline — the segment mix.

Watch: does this hold once the GST base-effect tailwind fades?

Trigger: next 2–3 months of data — that's when you separate real recovery from a one-off pull-forward.

The story isn't "auto is booming." It's "the bottom end of the market is waking up" — and that matters for who benefits.

What matters more to you — the record headline number, or which segment is actually driving it?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

33

One thing to keep in mind: these are dispatches (company → dealer), not retail sales. So part of this can be dealers stocking up ahead of festive/demand expectations. Worth cross-checking against retail (FADA) numbers before calling it a full-blown recovery.

10

Oswal Pumps just bagged a ₹500 Cr Bihar solar deal — but the headline number hides the real story.

$OSWALPUMPS #SolarEnergy #PMSuryaGhar #RenewableEnergy

Only ~half of it is a one-time install order.

The other half? Recurring income spread over 10 years.

Here's what actually matters 👇

The breakdown:

→ ₹247 Cr one-time install order

→ ₹257 Cr energy revenue over 10 years (annuity-style)

→ 63 MW rooftop solar, 57,492 homes in Bihar

So this isn't a lumpy "book it once" order. Half of it is a slow, steady income stream under the RESCO model — Oswal builds, owns, runs it for 10 years and gets paid over time.

The bigger signal:

Oswal's core business so far leaned heavily on the PM Kusum scheme (solar pumps).

This deal is a clear push to NOT depend on one scheme — moving into PM Surya Ghar residential rooftop instead.

Focus: not the ₹500 Cr — the shift toward recurring, diversified revenue.

Watch: execution. 57k installs to commission in 9 months is no small ask.

Trigger: PPA signing how fast they hit that 9-month commissioning timeline.

Context: stock already 9% today at ₹435, on top of a strong Q4 — PAT up 43.9% YoY, REVENUE up 39.8% YoY.

So the quarter was good. But the more durable story is whether annuity income diversification actually reduces lumpiness over the next few years.

What matters more to you here — the one-time order size, or the 10-year recurring income underneath it?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

101

One nuance worth flagging: under the RESCO CAPEX model, Oswal also carries the financing 10-yr O&M burden. So the ₹257 Cr annuity isn't "free" — margins depend on financing cost and how clean the 57k installs are. Recurring revenue is great, but watch the cost side too.

10

India's ethanol push is sold as a clean win: blend more ethanol with petrol → cut oil imports → save forex → help the rupee → boost farm income.

#Ethanol #SugarStocks #EnergyPolicy

The numbers tell a different story.

The catch nobody leads with:

India needs 10–11 billion litres of ethanol to meet its E20 blending target.

Installed capacity already hit ~20 billion litres by Nov 2025 — and may grow another 15% next year.

So the current target absorbs barely HALF the capacity already built.

The problem has quietly flipped. It's no longer "make more ethanol." It's "find demand for the ethanol we've already built capacity for."

Why this happened:

This capacity wasn't accidental. It was pushed via government soft loans and interest subsidies — catalysing investment of over ₹40,000 Cr.

Once that money is committed, idle plants kill returns. So higher blending targets are now needed partly to rescue capacity that's already been built — not purely for energy security.

We built the supply. Now we're manufacturing the demand to justify it.

Then there's the import story — which doesn't hold up cleanly:

Yes, ethanol replaces some petrol → less oil imported.

But making ethanol at scale needs more sugarcane, maize, rice → which needs more fertiliser (urea, DAP, potash) → which needs imported natural gas.

It also pulls farm land toward cane/maize/rice and away from oilseeds and pulses — where India ALREADY imports heavily.

So oil imports fall, but dependence doesn't vanish — it shifts to fertiliser, gas and edible oil. Plus consumers get lower mileage (ethanol has less energy per litre).

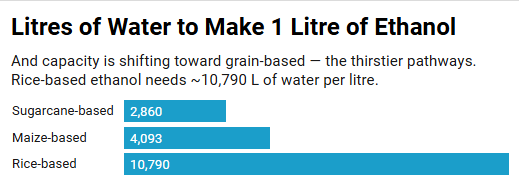

And the part that should worry everyone — water:

→ Sugarcane ethanol: ~2,860 litres of water per litre

→ Maize-based: ~4,093 litres

→ Rice-based: ~10,790 litres

And capacity is shifting toward grain-based — the thirstier kind. In Maharashtra, sugarcane is under 10% of cropped area but drinks over half the irrigation water.

The real signal:

This isn't "ethanol is bad." It created revenue for mills and managed sugar surpluses. But the programme has entered a new phase — where capacity utilisation, not energy security, is quietly driving policy.

Watch: whether future blending targets get justified by energy-security language or by the need to keep ₹40,000 Cr of plants running. That tells you what the policy is really solving for.

When a country builds double the capacity it needs and then raises targets to use it up — is that energy security, or rescuing investment that already went in?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

1

5

137

The cleanest tell: capacity (~20 bn L) is already nearly double what E20 needs (10–11 bn L), and it's still growing.

When supply runs that far ahead of demand, raising the blending target stops being an energy decision and becomes a capacity-utilisation one.

That's the quiet shift in what the policy is actually solving for.

9

Jun 12

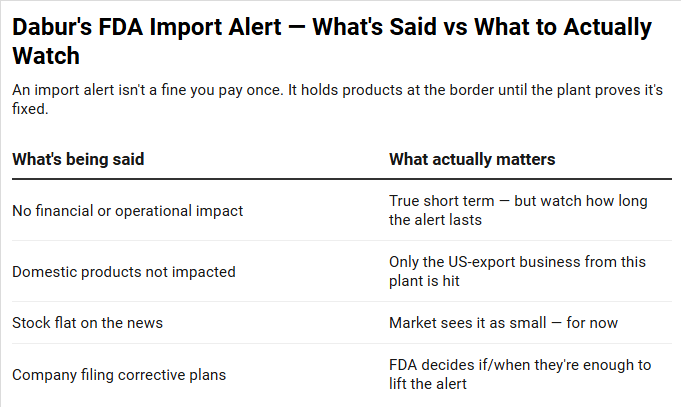

Dabur got a US FDA import alert — and says "no financial impact."

#Dabur #FMCG #FDA

The stock barely moved. But the why behind the alert deserves a closer read.

What happened:

The FDA inspected Dabur's Dadra & Nagar Haveli plant and flagged data integrity and maintenance lapses. Per the inspection report (via Reuters):

→ manufacturing records were falsified — to hide that equipment meant for one product was used for several others

→ a live bird and bird droppings were found in the raw material warehouse, about 30 feet from packaging materials

That's the part worth pausing on.

Why an import alert is different from a fine:

A fine is a cost you pay and move on. An import alert means US customs can detain Dabur's products from that plant without even examining them — until Dabur proves to the FDA it has fixed the violations.

So the products are effectively stopped at the US border until the regulator is satisfied. That's a trust problem, not a one-time payment.

The honest read:

Dabur's "no financial impact" is likely true short-term — its US health products (honey, hair oil, cough rubs, creams) are a small slice, and domestic business is untouched.

But falsified records sanitation lapses point more to a quality-culture issue than a one-off slip. That's what regulators scrutinise hardest, and it can take time to clear.

Watch:

→ how long the alert stays in place (months vs a quarter or two)

→ whether the FDA accepts Dabur's corrective plans on the first pass

→ any sign the scrutiny widens to other products or plants

The catch:

Today this is a small, contained event. It only becomes a real story if it lingers or signals broader quality gaps. The stock being flat tells you the market is, for now, taking the "no impact" line at face value.

When a company says "no financial impact" after a quality-related regulatory action, what do you weigh more — the size of the business affected, or what the findings say about how the plant is run?

$DABUR

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

88

Jun 12

The fair question this raises — the plant making these flagged products also serves the domestic market.

The FDA caught it on inspection.

Whether our own checks are as tight on domestic-only output is a debate worth having, openly.

24

Jun 12

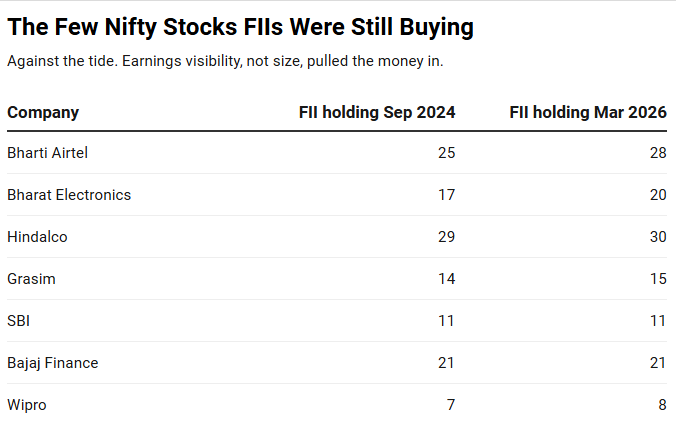

FIIs sold 43 of the 50 Nifty stocks since Sep 2024.

#Nifty #FII #StockMarket

The index? Basically flat. Not crashed.

That gap is the whole story — and most coverage is missing it.

The scary headline:

Foreign investors have pulled out of nearly every Nifty bluechip. The hardest hits (Sep 2024 → Mar 2026):

→ Trent: 26.62% → 15.59% FII, stock −51% from peak

→ TCS: 12.66% → 9.66%, −53% from peak

→ Eternal (Zomato): 52.53% → 32.61%, −33%

→ ICICI Bank: 46.21% → 34.48%

→ HDFC Bank: 48.02% → 44.05%

Even the "sacred" global favourites got trimmed. The selling wasn't one sector — it was broad and sustained.

So why isn't the Nifty down 30%?

Because someone was on the other side of every sale.

In 2026 alone, domestic investors (DIIs) have poured in over ₹4 lakh Cr. SIPs, mutual funds, retirement money. That wall of domestic cash absorbed the entire FII exit.

The real signal:

This isn't "FIIs control the market." It's the opposite — ownership of India's bluechips is quietly shifting from foreign hands to domestic ones. Five years ago, this much FII selling would've caused a deep correction. Today, DIIs just soak it up.

Why FIIs left (not panic — recalibration):

→ weak rupee cut dollar returns

→ single-digit earnings growth for 7–8 quarters

→ the global AI trade pulled EM money elsewhere

→ stretched valuations on the high-growth names

The part worth bookmarking:

A handful of stocks saw FIIs BUYING against the tide —

→ Bharti Airtel: 25.08% → 27.79%

→ Bharat Electronics: 17.27% → 19.51%

→ SBI, Hindalco, Bajaj Finance, Grasim, Wipro

Where foreign money stayed or added, the common thread was earnings actually showing up — not size or brand.

Watch: whether earnings growth breaks out of the single-digit rut. FIIs left because growth stalled, not because they hate India. Better earnings → the flow can reverse. Until then, DIIs are holding the floor.

When FIIs sell this hard but the index holds flat, what's the bigger takeaway — that foreign money is leaving, or that domestic money is now strong enough to not care?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

212

Jun 12

The cleanest tell isn't the selling — it's the buying.

FIIs added to Airtel, BEL, SBI, Hindalco, Bajaj Finance while exiting almost everything else.

The common factor?

Earnings delivery.

In a flat-earnings market, foreign money concentrated on the few places growth was actually visible.

That's the map, not the noise.

61

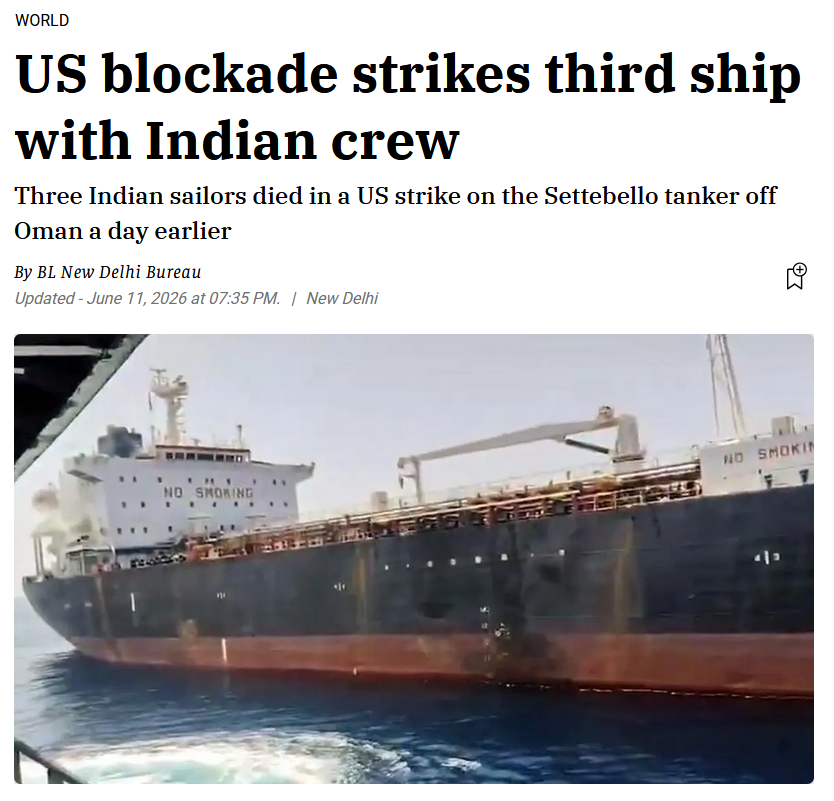

Jun 11

Friendship goals:

🇮🇳 We send warm wishes and gratitude.

🇺🇸 They send missiles at our sailors.

3 Indians dead. And we're still saying "thank you."

This isn't diplomacy. It's surrender with a smile.

Jun 10

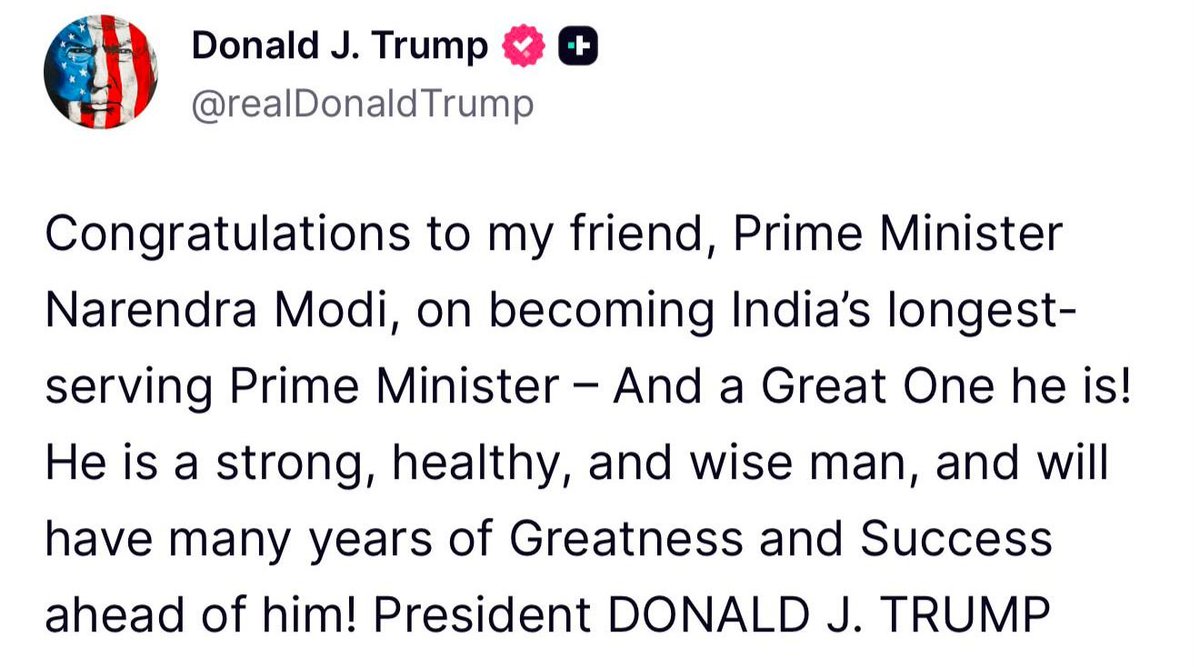

Thank you, President Trump, for your warm wishes.

I look forward to working with you to further advance the India-US Comprehensive Global Strategic Partnership, for the benefit of both our nations and the world.

@POTUS

@realDonaldTrump

35

Jun 11

3 Indian sailors murdered. 3 ships struck in 4 days.

If these were American bodies in the water, US carriers would already be lining up for retaliation.

Our response? A "strong protest" and a démarche handed to a Chargé d'Affaires.

When did Indian lives become this cheap? 🇮🇳

50

Jun 9

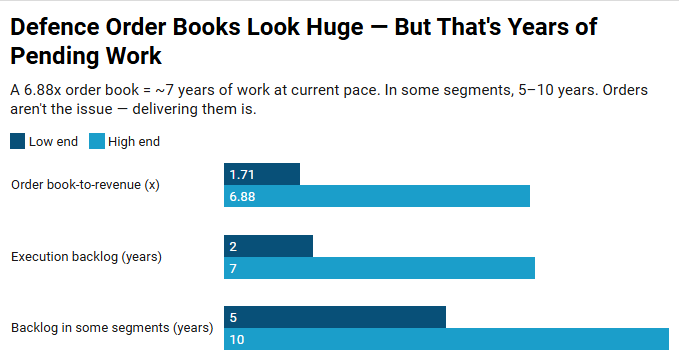

The cleanest way to read Defence Sector now:

Order book-to-revenue tells you the demand;

Revenue growth tells you the execution.

When the two diverge — big order book, flat revenue — that gap IS the bottleneck.

Q4FY26 made it visible at BDL, DCX and Zen.

x.com/EdgeOverHype/status/20…

Jun 9

Defence stocks get cheered for one thing: huge order books.

#DefenceStocks #MakeInIndia #HAL

That's now exactly where the risk sits.

The story has flipped. The question is no longer "is there demand?" — it's "can these companies actually deliver what they've already won?"

The numbers (PwC India CRISIL):

→ Domestic defence production hit a record ₹1.54 lakh Cr in FY25

→ India now exports to nearly 100 countries

→ Order book-to-revenue for major makers: 1.71x to 6.88x

Here's the part that gets glossed over:

A 6.88x order book isn't just a big number — it's roughly 7 years of work at the current pace. In some segments, the backlog stretches 5 to 10 years.

A fat order book is a backlog, not a guarantee.

And the cracks are already showing.

In Q4FY26, defence revenue for a brokerage's coverage came in broadly flat YoY and below estimates — held back by delivery delays at Bharat Dynamics, DCX Systems and Zen Technologies. Profitability held up; revenue didn't, because programmes slipped.

The real signal:

The bottleneck has moved from winning orders to executing them. PwC's point is blunt — adding capacity isn't enough. Planning, supplier coordination, workforce productivity and digital integration are what decide who delivers on time.

The split that matters:

Strong execution at HAL and BHE helped offset weakness at BDL last quarter. Same sector, same order tailwind — very different delivery.

Watch: revenue conversion, not order inflows. When the next results come, the question to ask isn't "how big is the order book?" — it's "how much of it actually turned into revenue?" That's what now separates the winners.

For a defence company, what tells you more about the next two years — a record order book, or whether last quarter's deliveries came in on time?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

27

Jun 9

Defence stocks get cheered for one thing: huge order books.

#DefenceStocks #MakeInIndia #HAL

That's now exactly where the risk sits.

The story has flipped. The question is no longer "is there demand?" — it's "can these companies actually deliver what they've already won?"

The numbers (PwC India CRISIL):

→ Domestic defence production hit a record ₹1.54 lakh Cr in FY25

→ India now exports to nearly 100 countries

→ Order book-to-revenue for major makers: 1.71x to 6.88x

Here's the part that gets glossed over:

A 6.88x order book isn't just a big number — it's roughly 7 years of work at the current pace. In some segments, the backlog stretches 5 to 10 years.

A fat order book is a backlog, not a guarantee.

And the cracks are already showing.

In Q4FY26, defence revenue for a brokerage's coverage came in broadly flat YoY and below estimates — held back by delivery delays at Bharat Dynamics, DCX Systems and Zen Technologies. Profitability held up; revenue didn't, because programmes slipped.

The real signal:

The bottleneck has moved from winning orders to executing them. PwC's point is blunt — adding capacity isn't enough. Planning, supplier coordination, workforce productivity and digital integration are what decide who delivers on time.

The split that matters:

Strong execution at HAL and BHE helped offset weakness at BDL last quarter. Same sector, same order tailwind — very different delivery.

Watch: revenue conversion, not order inflows. When the next results come, the question to ask isn't "how big is the order book?" — it's "how much of it actually turned into revenue?" That's what now separates the winners.

For a defence company, what tells you more about the next two years — a record order book, or whether last quarter's deliveries came in on time?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

193

Jun 8

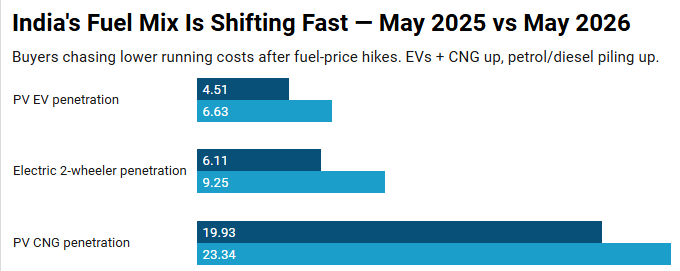

India's car market is quietly splitting into two.

#EVs #AutoStocks #MakeInIndia

EVs are running out of stock.

Petrol and diesel cars are piling up.

EV dealer inventory has dropped to single-digit days — and popular models may soon have waiting periods.

Meanwhile, larger petrol/diesel vehicles are stacking up unsold across showrooms.

Why now:

Recent fuel-price hikes pushed buyers toward lower running-cost options. The shift is showing in hard numbers (Vahan, May YoY):

→ PV EV penetration: 6.63% (was 4.51%)

→ Electric 2-wheeler: 9.25% (was 6.11%)

→ PV CNG: 23.34% (was 19.93%)

But here's the part most coverage misses:

The EV bottleneck is no longer demand. It's supply.

And the supply problem has changed shape. It's not the old chip shortage anymore. The new constraint is deeper:

→ battery cells

→ rare-earth magnets

→ EV electronics

→ Tier-2/Tier-3 vendors who can't scale fast without quality slipping

India can assemble cars fine. Tata's EV head said in-house capacity isn't the issue — it's the supplier side. The missing pieces are high-value parts India still imports.

That's why waiting periods are forming. OEMs would rather hold tight, lean inventory than risk battery-safety or quality failures by rushing supply.

The real signal:

This isn't a "buy EV makers" story. It's a "who makes the parts India doesn't yet localise" story. The government has already approved ₹7,280 Cr for domestic rare-earth magnet manufacturing — a tell on where the gap is.

One more shift: this demand is increasingly Bharat-led. Rural PV sales grew 30.35% YoY in May vs 18.8% urban. Small cars are reviving after years of premium-only growth.

Watch: whether EV waiting periods actually form in the next few weeks. If they do, the value moves upstream — to whoever can localise cells, magnets and EV components, not just to the brands selling cars.

When demand outruns supply like this, who usually captures more value — the company assembling the vehicle, or the one making the scarce parts inside it?

$TATAMOTORS

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

157

Jun 8

The cleanest tell here is the ₹7,280 Cr rare-earth magnet scheme.

Government doesn't put that kind of money behind a part unless it's a real choke point.

Electric two-wheelers may feel it first — their localisation cycles for traction motors and magnets are still the least mature.

33

Jun 5

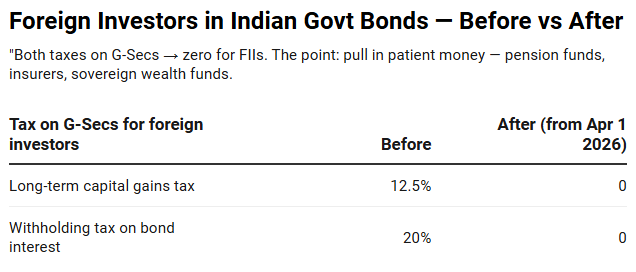

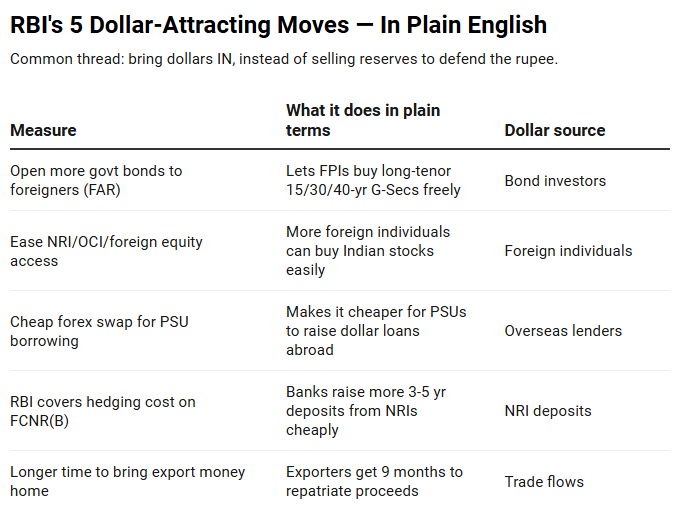

Government just made Indian govt bonds tax-free for foreign investors.

#FPI #GSec #Rupee

This is the bigger half of yesterday's rupee-defence push — and it's getting underplayed.

What changed (via ordinance, backdated to Apr 1, 2026):

For FIIs holding government securities →

→ 12.5% long-term capital gains tax → now 0%

→ 20% withholding tax on bond interest → now 0%

Both gone. Same benefit extended to the Bank for International Settlements.

Why this matters more than it looks:

A 20% tax on interest is a huge drag on a bond investor's return. Remove it, and an Indian G-Sec suddenly pays a foreigner a lot more in hand — without the yield itself changing.

Why now:

The rupee is under pressure (West Asia war crude spike FPIs pulling out of stocks). RBI announced incentives yesterday. This tax ordinance is the fiscal half of the same plan.

Read together:

→ RBI opened the door (eased FPI limits, long-tenor bonds)

→ Govt sweetened the deal (zero tax on G-Sec returns)

The target isn't hot money. It's patient money — pension funds, insurers, sovereign wealth funds. The kind that stays.

Plus: foreign individuals can now own up to 10% in a single listed company (was 5%), with the overall PROI limit raised to 24% from 10%.

The catch:

Tax-free returns make the bonds attractive — but global investors still weigh war, oil, and rupee risk. The incentive is strong; the timing of inflows still depends on global risk appetite.

Watch: whether FPI G-Sec inflows actually pick up over the next few weeks. The math now favours India — the question is whether nervous global money acts on it.

For a foreign bond investor, which removal moves the needle more — the 20% tax on yearly interest, or the 12.5% on capital gains?

For educational purposes only. Not SEBI registered investment advice.

Bookmark 🔖 Follow 🔔 for more high-signal India equity setups

1

108

Jun 5

The under-discussed number is the 20% withholding tax going to zero.

Capital gains tax only bites when you sell — but withholding tax hits the interest every single year.

For a buy-and-hold pension fund or sovereign fund, removing the annual drag is what actually changes the long-term return math.

23