I tweet what I want and speak the Truth.

Joined July 2018

- Tweets 19,942

- Following 1,049

- Followers 1,655

- Likes 28,328

2,226 Photos and videos

Smart money understands Japan.

5 steps ahead.

Do you understand?

21

1

60

The Bank of Japan just hiked its policy rate to 1% (highest since 1995) at the June 15-16 meeting, with expectations it may pause bond tapering amid jittery JGB markets. The yen has been hovering near 160/USD despite prior interventions (authorities spent ~11.7 trillion yen / $73B recently), prompting fresh warnings of “decisive measures” from the finance ministry. Ten-year JGB yields have climbed toward the mid-2% area (with longer tenors higher), reflecting both BOJ normalization and fiscal expansion concerns under the current administration.

Real wages have been under pressure, import costs elevated (energy/Middle East factors), and debt-to-GDP sits around 230-237% — the highest among major economies. Fiscal policy has turned more expansionary (stimulus, subsidies on fuel/food), with a shift toward managing the debt-to-GDP trajectory over multiple years rather than rigid primary-balance targets. Growth forecasts remain modest (~0.5-0.8% range for 2026).

Markets are not treating this as an imminent crisis.

The Nikkei has hit record highs at times, and some analysts (e.g., Ed Yardeni) argue Japan’s issues won’t cascade into a major global problem the way a true emerging-market or leveraged Western blow-up might. Carry-trade unwind fears appear more muted than in prior episodes. Period.

1

58

So many worries about Japan. HA!

It’s an arm’s length relationship with a debasement strategy for a bifurcated global economic rotation.

1

21

Modine Manufacturing ($MOD): Landmark $4 billion long-term capacity agreement (LTA) through 2029 with a strategic data center customer for its Airedale by Modine cooling solutions. Includes upfront funding for capacity expansion. Record orders with ~5-year visibility; shifting focus to data center thermal management (spinning off legacy auto business). Direct contract serving the cooling/power-density bottleneck.

1

25

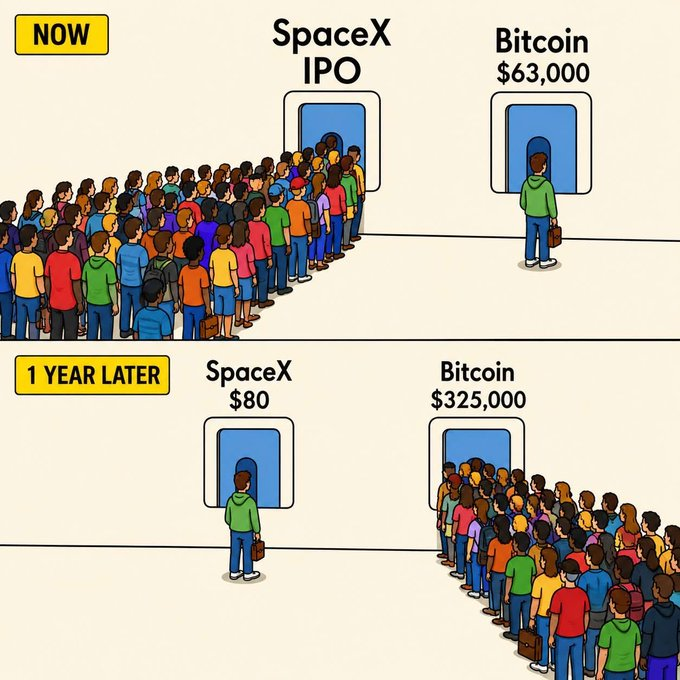

$SPCX $1T in revenue by 2030 and people said $135 was too expensive.

Hmmmm.

Careful who you listen to!

1

39

So many people worried about Japan.

So many people bearish.

So many people said don’t buy $SPCX.

The loud herd goes one way.

You?

1

40

Elite Intuition retweeted

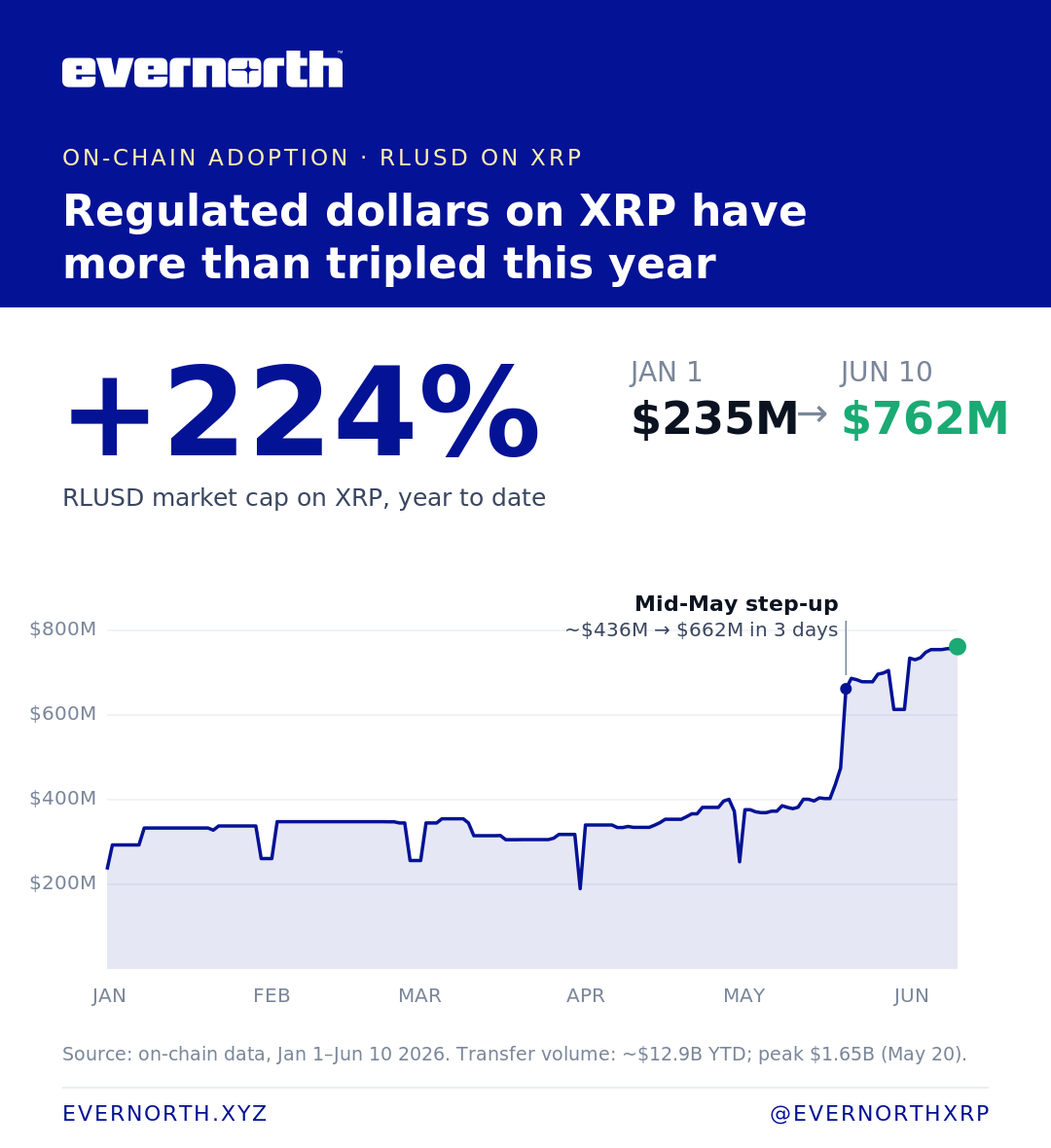

RLUSD on the XRP Ledger continues to grow!

RLUSD on XRP is up 224% this year from $235M to $762M, according to XRP Ledger data as of June 10, 2026. Don’t forget it still needs its Swap Kid though! (evernorth.xyz/blog-post-05-2…)

This content is for informational purposes only and does not constitute investment advice. Digital assets involve risk, including potential loss of principal. Learn more about Evernorth: evernorth.xyz/blog-post-03-1…

16

199

791

71,661

Elite Intuition retweeted

I got @PeterSchiff to admit bitcoin is not going to zero on national television.

Next he will reveal he owns a bunch of bitcoin too…

205

236

3,206

242,865

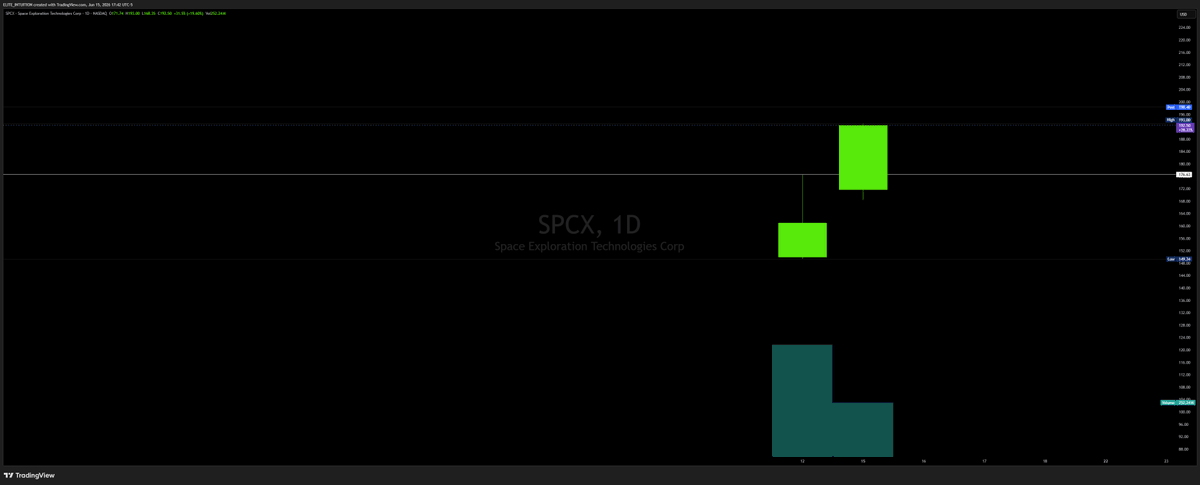

I don't care what anyone says. This is a very bullish candle on $SPCX.

Volume maybe lower, but still bullish.

4hr chart says so, too.

1

69

Prove me right or wrong... I'm fine either way.

I can go play both sides.

Get it...

1

34

The next wave of AI, Robotics, Quantum and Space.

Be 5 steps ahead.

1

30

With all the money printed from December until now; when they announce rate cuts here soon, what's gonna happen? 😁

1

29

Bears... you see that call volume right before close on $QQQ?

2

95