Specialized service, providing high quality economic and political reports on emerging markets in CEE, Eurozone, MENA, SSA and Asia since 2004.

Joined June 2012

- Tweets 26,483

- Following 1,247

- Followers 1,837

- Likes 34

15,315 Photos and videos

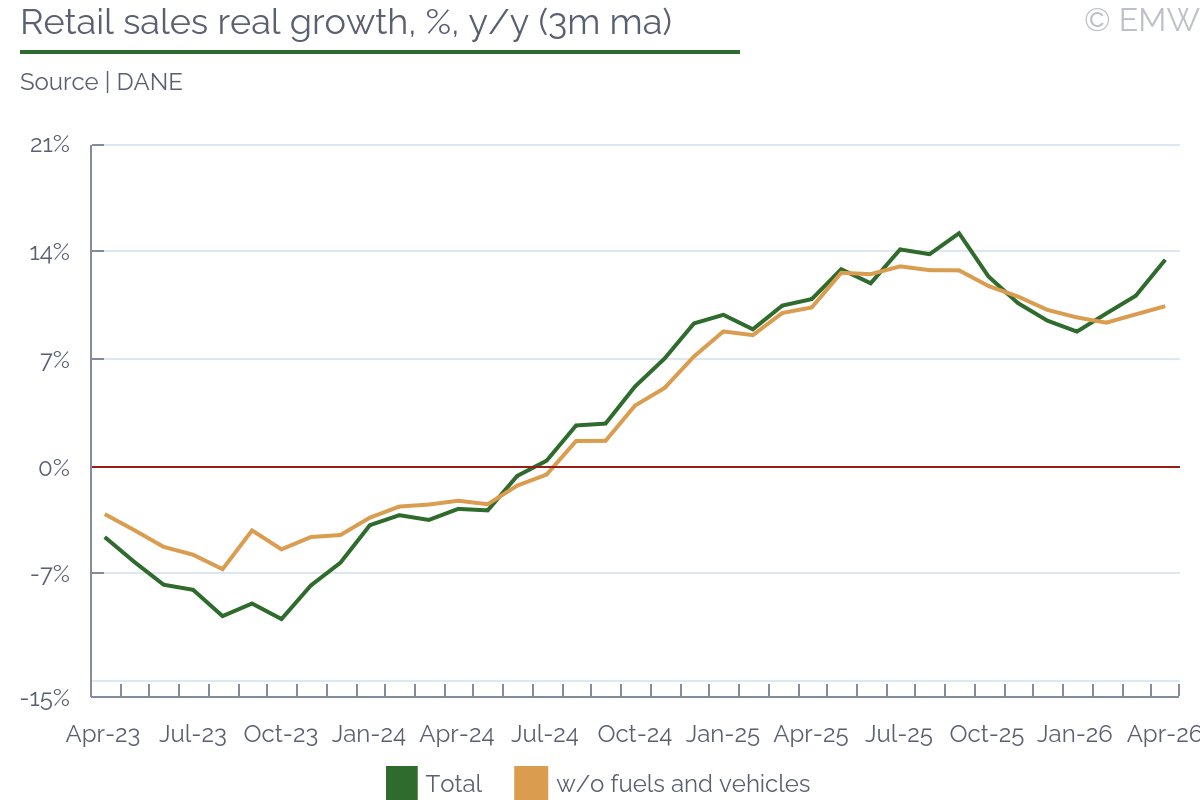

#Colombia - Retail sales jump 14.9% y/y in April, led by autos and electronics

- Vehicles and motorbikes drive 8.5pps of headline growth; sa sales ex-vehicles rise 0.3% m/m

- YTD hikes of 200bps yet to dent consumption; another BanRep hike on Jun 30 may cool H2 demand

emergingmarketwatch.com/brow…

#EmergingMarkets

16

#Colombia - Industrial output up 3.0% y/y in April, manufacturing leads

- Mining recovers in Apr but remains down 2.8% YTD; oil price tailwind on Middle East tensions expected to lift prints through Q2

- Electricity and coal output drive 1.5pps of headline growth; 8 of 26 activities record slight y/y declines

emergingmarketwatch.com/brow…

#EmergingMarkets

44

#Brazil - Retail sales rise by below-consensus 1.0% y/y in April

- Sales growth eases from 4.0% y/y in March, missing consensus for 2.0% increase

- Retail sales fall 1.5% m/m in April in sharpest decline since December 2023

emergingmarketwatch.com/brow…

#EmergingMarkets

1

48

#Philippines - Govt to issue 5.5-year, 10-year and 25-year Eurobonds

- Bonds are rated Baa2 by Moody's, BBB by S&P and BBB by Fitch

- Price guidance set at 85bps over US treasuries for 5-year notes, 125bps for 10-year bonds

emergingmarketwatch.com/brow…

#EmergingMarkets

33

India just posted its best export month on record. The trade deficit got wider anyway.

Merchandise exports hit USD 45.2bn in May, an all-time high, up 18% y/y. The growth was broad: engineering goods up 24.5%, petroleum products up 54.9%, electronics up 11.6%. Even shipments to West Asia held roughly steady through the conflict, rerouted via ports in Oman.

So why did the deficit widen 25% y/y to USD 28.2bn? Imports grew faster, up 20.6% to USD 73.4bn. The standout line was gold. Imports jumped 60% in April-May to USD 9.0bn, even at elevated prices.

That gold number is the tell. When households pile into gold at record prices, it usually says more about confidence in the currency than about jewellery demand. The rupee fell to almost 97 per dollar this year, a record low, before the RBI and government stepped in with measures to attract foreign capital. Some investors are now shorting the rupee as a "bad carry" trade.

The cushion is services. India ran a services surplus near USD 17.7bn in May, exports of USD 36.8bn against imports of USD 19.1bn, which absorbed a large part of the goods gap. That surplus is doing real structural work for the external account now.

Two things could ease the pressure from here. The Strait of Hormuz is set to reopen on Jun 19 under the US-Iran deal, which should lower the oil and fertiliser bill for the world's third-largest crude buyer. And New Delhi and Washington look close to an interim trade pact, with the US Trade Representative due in India on Jun 23-24.

Goldman Sachs has already trimmed its 2026 current account deficit forecast to 1.3% of GDP. We think that's reasonable if oil keeps falling and gold demand cools. But both are big ifs. If crude stays high and households keep buying gold, the current account stays under pressure into the second half, and the rupee remains the variable to watch.

Our base case: the worst of the import shock is probably behind India. The gold habit and the oil price will decide how fast the external account heals.

#india #gold #emergingmarkets

1

1

70

#Russia - Current account surplus narrows to USD 6.7bn in April – CBR estimate

- Exports fall due to lower physical volumes and discounts

- RUB appreciation and seasonality influence the shifts

- Current account expected to narrow further

emergingmarketwatch.com/brow…

#EmergingMarkets

40

#Lebanon - President welcomes US-Iran peace deal, sees opening for stability in country

- Aoun says deal could help end cycles of violence and pave way for stability, recovery and reconstruction

- He also stresses need for strong state institutions in Lebanon

- Parliament speaker Berri, who is key political ally of Hezbollah, welcomes provisions to halt hostilities across Lebanon

emergingmarketwatch.com/brow…

#EmergingMarkets

60

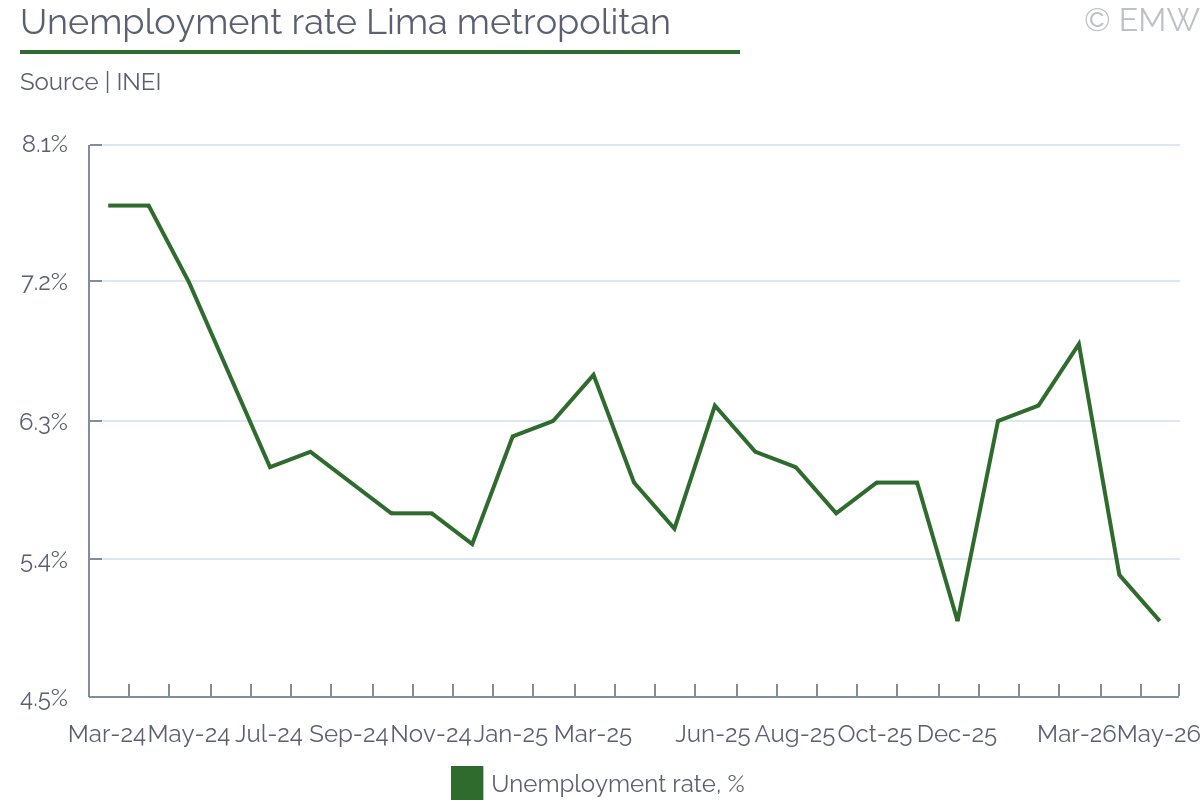

#Peru - Unemployment rate in Lima falls to 5.0% in March-May

- Unemployment rate comes in better than consensus expectations

- Employed population increases 6.7% y/y, adding around 367,800 jobs in the quarter

- Adequate employment rises 9.6% y/y to 3.8mn, while underemployment remains below the level recorded in the same period of 2024

emergingmarketwatch.com/brow…

#EmergingMarkets

1

42

#IvoryCoast - Budget deficit shrinks by 69.3% y/y in Jan-Apr

- Deficit accounts for about 0.4% of full-year GDP projection

- Revenue is largely in line with expectations thanks to tax proceeds while grants fall

- Investment spending remains below target which might be due to delays in project implementation

- Budget deficit appears on course to meet full-year target of 3% of GDP but risks related to Middle East conflict remain

emergingmarketwatch.com/brow…

#EmergingMarkets

3

48

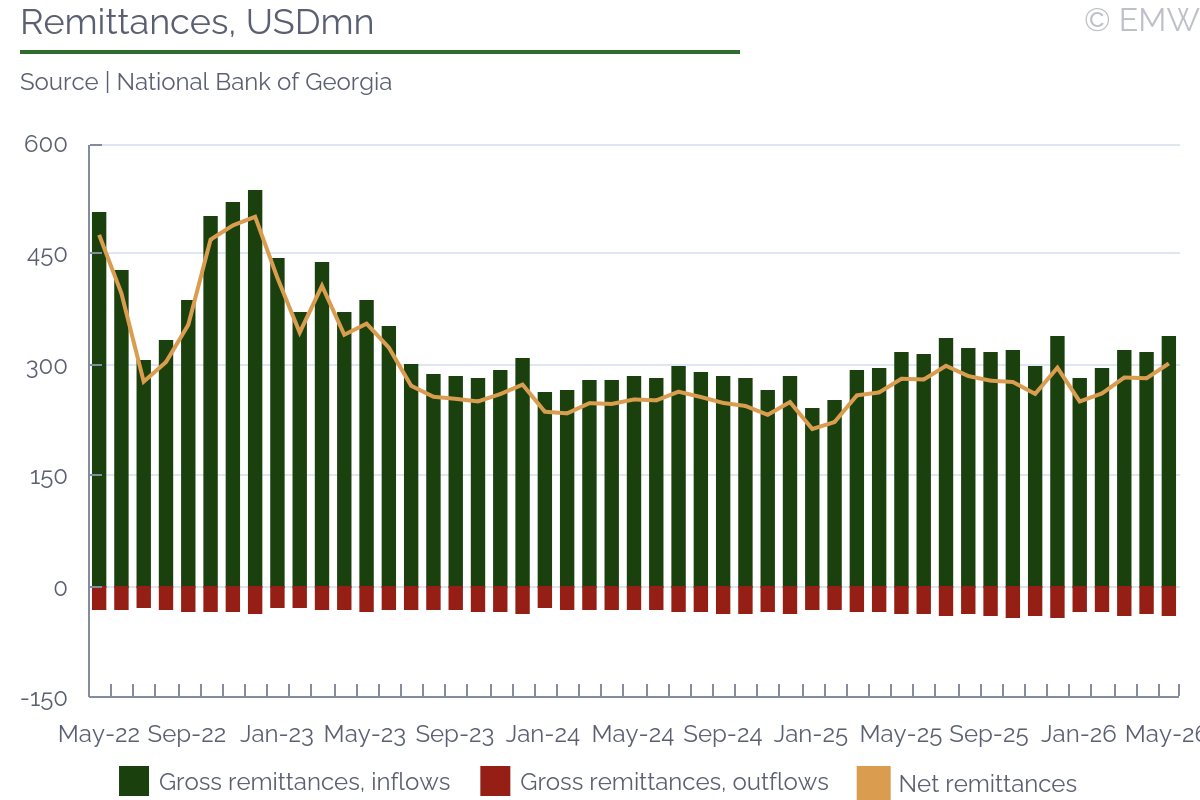

#Georgia - Remittances rise in May

- Net remittances increase from USD 282.9mn in Apr to USD 302.9mn in May

- USA, Italy and Russia traditionally lead inflows

emergingmarketwatch.com/brow…

#EmergingMarkets

47

#Mongolia - General government budget posts MNT 73.4bn surplus in May

- Revenues and spending volume broadly stable m/m

- Tax receipts continue to grow, impact of VAT strong in May

- Cumulative budget deficit posts MNT 1.35tn

emergingmarketwatch.com/brow…

#EmergingMarkets

41

#Kazakhstan - Composite indicator growth climbs to 4.3% y/y in Jan-May

- Industry and retail sales maintain upward trajectory

- Result in agriculture stable, construction growth eases

- Outcome generally expected, extraction should support growth trend beyond Tengiz incident

emergingmarketwatch.com/brow…

#EmergingMarkets

62

#Turkey - Erdogan camp points to late-2027 route for final candidacy bid

- Parliamentary elections in late 2027 or early 2028 to let Erdogan run again, according to presidential adviser Mehmet Ucum

- This strategy avoids drafting new constitutional amendments entirely

- Ucum calls early-election talk premature, citing wars and security

emergingmarketwatch.com/brow…

#EmergingMarkets

73

Pakistan's FY27 budget rests on one number it has missed for years. The Federal Board of Revenue must lift tax collection by 17.6% to PKR 15.3tn. Last year it fell short by a record PKR 1.15tn. Now it has to do better with almost no new taxes.

FinMin Muhammad Aurangzeb tabled the budget on June 12, after a rare delay. It keeps Pakistan inside its $7bn IMF programme. The primary surplus target is 2% of GDP, down from 2.5% this year, and the general government deficit widens to 3.6% of GDP.

The revenue side is the gamble. The FBR is meant to hit that 17.6% jump mostly through enforcement, not new measures. Around PKR 500bn is pencilled in from better compliance, PKR 150-200bn from a new 1% tax on small retailers, and the rest, roughly PKR 1.6tn, from inflation and growth. Provinces have agreed to hand back over PKR 1tn to the centre, what Aurangzeb calls "cooperative federalism", partly to fund a 15.9% rise in defence spending.

For bondholders, the fiscal anchor is what counts. Pakistan has rebuilt credibility on the back of IMF discipline. The $1.3bn disbursement last month and a rupee that's been Asia's most stable currency this year show it's working. Hitting the 2% primary surplus keeps that intact and supports the return to global markets.

External financing tells the story. Net external borrowing is set to fall 47% to about $2.8bn, and the government plans roughly $2bn of Eurobond, Sukuk and Panda issuance in FY27, after $1.25bn this year. The IMF sees reserves climbing to a record $20.9bn. That's a sovereign trying to normalise its access to global capital.

The catch is at home. Net domestic financing jumps 67.6% to PKR 6tn, which crowds out private credit, and debt servicing still eats 46% of current spending.

We think the revenue target is the weak link. If the FBR slips, and history says it probably will, the government faces a familiar choice: new taxes or deeper cuts to an already thin development budget. Our base case is that growth gets sacrificed before the fiscal targets do.

Watch the central bank, which will likely stay tight with inflation seen quickening to 8.2%, above its 5-7% range. And watch the timing of the first Eurobond. Both will tell us whether the market buys the consolidation story.

#pakistan #emergingmarkets #fiscalpolicy

86

#SaudiArabia - CPI inflation edges up to 1.8% y/y in May

- Heavy-weight Housing and utilities remains main driver of inflation, specifically actual rents for housing

- Food prices become vulnerable to supply line disruptions, security risks

- Energy subsidies, currency peg shield Saudi consumers from global inflationary pressures

- Saudi Aramco hiked diesel prices by 8% at start of 2026, but diesel has very small weight in consumer basket

emergingmarketwatch.com/brow…

#EmergingMarkets

2

2

58

#UnitedArabEmirates - Moody's affirms Abu Dhabi's Aa2 ratings and maintains stable outlook

- Abu Dhabi has exceptionally large financial assets

- GDP to contract 9.5% in 2026 and jump 17% in 2027

emergingmarketwatch.com/brow…

#EmergingMarkets

72

Bangladesh's new government just staked its credibility on a tax target almost nobody in Dhaka thinks it can hit.

The Bangladesh Nationalist Party presented its first budget on June 11, four months after winning the February 2026 election that followed the youth uprising. The headline is ambition. The fine print is doubt.

The FY27 budget is sized at BDT 9.38tn, up 19% from the revised FY26 figure. The Annual Development Programme jumps 50% to BDT 3tn, as the government tries to spend its way to 6.5% growth, up from an estimated 5.0% this year. Inflation is seen at 7.5%, with the policy rate held at 10% for now. The fiscal deficit is set to widen to 3.5% of GDP, from 3.2%.

To pay for it, the National Board of Revenue has been handed a BDT 6.04tn tax target, 20.1% above FY26 collections. We think that number is unrealistic. The NBR pulled in BDT 3.27tn over July to April, leaving BDT 1.76tn to find in the final two months of the year, a pace it has never come close to. The country's main business chamber warns the push risks turning into taxpayer harassment, and the opposition expects the shortfall to top BDT 2tn.

Why does this matter beyond Bangladesh? Because the gap between target and reality is where the risk sits. If revenue disappoints, and we think it will by a wide margin, either the deficit drifts past 3.5% of GDP, or the development programme gets cut mid-year. Both land just as Dhaka prepares to enter a fresh IMF arrangement. External financing is already pencilled in to surge 89.4% to plug the hole.

Reserves are projected to recover to USD 41bn, and reliance on domestic bank borrowing is set to ease, both supportive on paper. But the whole budget rests on a revenue line we don't trust.

Our base case at EmergingMarketWatch: the tax target gets missed, the development programme gets trimmed during the year, and the IMF talks set the real fiscal anchor. Watch the first-quarter collection numbers and the terms of the new programme. They'll tell you whether 6.5% growth was ever more than an aspiration.

#emergingmarkets #bangladesh #fiscalpolicy

96

Colombia just promised to cut its primary deficit by 3 percentage points of GDP in two years. We think that's a stretch.

The Finance Ministry unveiled its Medium-Term Fiscal Framework on Friday, 9 days before a presidential runoff. The numbers are built on ambition. The primary deficit closed 2025 at 3.5% of GDP. The MTFF sees it falling to 2.1% in 2026 and just 0.5% in 2027.

That whole path rests on two things: a new tax reform and spending cuts. Neither is in hand.

The ministry also trimmed 2026 financing needs to COP 150.5tn, down from COP 155.0tn in February. The final cash buffer for the year drops to COP 7.1tn, less than half the COP 17.6tn projected just four months ago. The cushion is thinning.

Here's why the targets ring hollow. This government failed to contain spending between 2022 and 2026. It tried three tax reforms and missed each time. The last attempt, in December 2025, aimed for COP 16.9tn and went nowhere. Now the same fix is being promised by an administration on its way out.

The politics make it harder. The Jun 21 runoff pits Ivan Cepeda, who would broadly continue Petro's line, against opposition candidate Abelardo de la Espriella. De la Espriella and his running mate Juan Restrepo have already pledged to scrap several ministries and cut at least 700,000 public jobs. If he wins, this framework gets rewritten. If Cepeda wins, it's a baseline at best.

There's a quieter problem in the debt mix. Officials have touted falling external debt ratios. But that mostly reflects Colombia shifting issuance onto the domestic market. The internal interest bill climbs to COP 74.2tn by 2027, dwarfing the external bill of under COP 10tn. For bondholders, the headline number looks better while the underlying burden moves home. Local yields have pushed to historic highs through H1 2026 on exactly these worries: sticky current spending, flat revenues, and a government reluctant to tighten.

Our read: the MTFF is a signaling exercise aimed at markets before the vote, and it lands late. The framework convinces no one of consolidation it hasn't delivered in four years. Watch the Jun 21 result first. The fiscal path Colombia actually follows won't be set by this document. It'll be set by whoever wins, and by whether the next Congress lets them.

#colombia #fiscalpolicy #emergingmarkets

79

#Colombia - FinMin unveils Medium-Term Fiscal Framework for 2026, ambitious targets ahead

- MTFF sets 2026 financing sources revised down to COP 150.5tn from COP 155.0tn in February's financial plan; final cash buffer drops to COP 7.1tn

- Primary deficit seen at 2.1% of GDP in 2026, falling to 0.5% in 2027

- Fiscal consolidation hinges on new tax reform and spending cuts; fragmented incoming Congress and electoral uncertainty cloud execution

- Javier Cuéllar's declining external debt metrics mask heavier domestic load; internal interest bill rises to COP 74.2tn in 2027

emergingmarketwatch.com/brow…

#EmergingMarkets

49

#Ecuador - CPI inflation cools to 0.92% y/y in May, as energy relief offsets fuel surge

- Transport adds 0.92pps to headline inflation as diesel prices jump 69% y/y, reflecting rising import bill and subsidy phase-out

- Esmeraldas refinery recovery may ease price pressures ahead, but Ecuador's dependence on imported refined products limits further relief

- Services CPI eases to 2.1% y/y from 2.2%; CPI ex-food slows to 1.2% y/y from 3.3%, signaling broad disinflation

emergingmarketwatch.com/brow…

#EmergingMarkets

4

63