Joined January 2021

- Tweets 12,793

- Following 743

- Followers 61,046

- Likes 20,537

6,819 Photos and videos

Pinned Tweet

6 Aug 2025

Excited to share—we’re now SEBI Registered!

After 2 years of consistently sharing insights on X, we received several inquiries about launching our own research services.

So, we decided to go ahead, get SEBI Registered, and launch our dedicated Research Desk, focused on uncovering high-growth opportunities in the Smallcap & Midcap space.

We're now also live on Smallcase!

There’s been a lot going on in the background over the last few months.

Thanks for the continued support—we’ll keep striving to add value!❤️

134

15

604

213,489

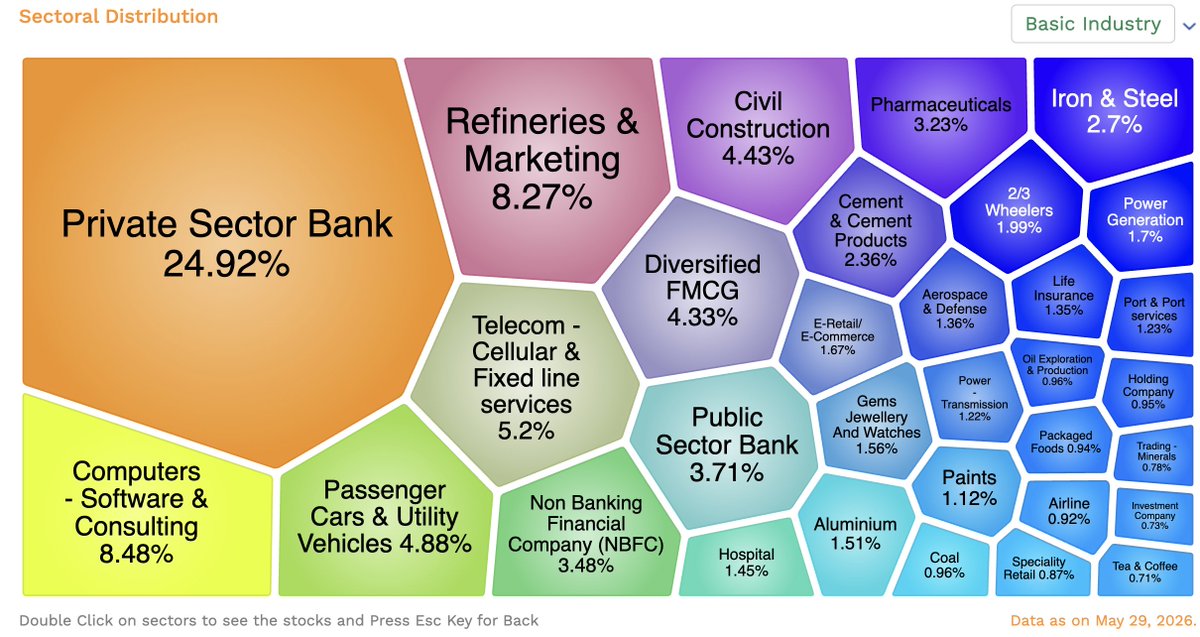

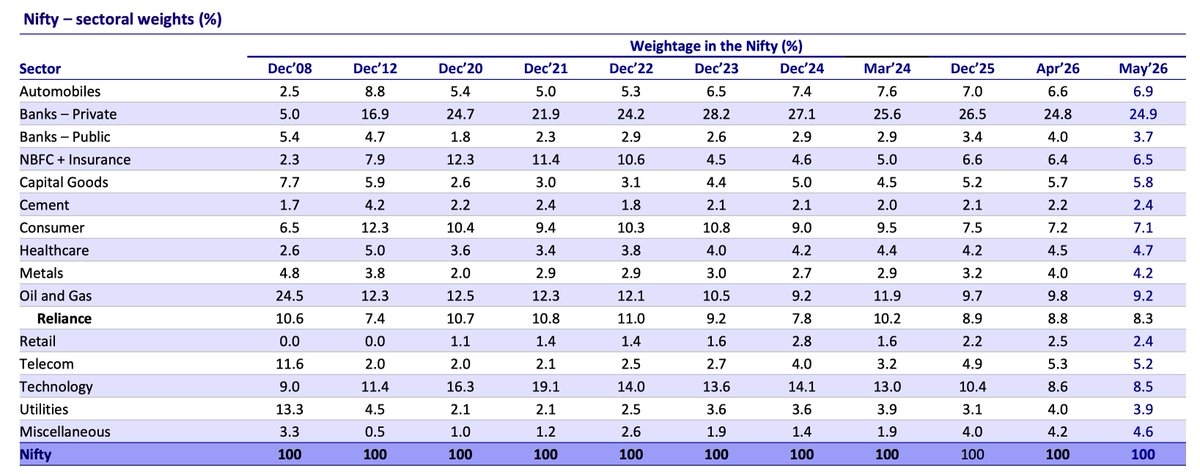

Nifty’s Technology weight has seen a sharp reset over the last few years

From 19.1% in Dec’21,Technology weight has now declined to 8.48%

Current IT weight in Nifty is mainly driven by:

Infosys - 3.77%

TCS - 2.14%

HCLTech - 1.16%

Tech Mahindra - 0.87%

Wipro - 0.54%

Together, these stocks now account for 8.48% of Nifty

The bigger point is that index composition is slowly changing

Wipro is also likely to be removed from Nifty50 as per reports. If that happens, IT weight will reduce further.

5

25

2,091

How Index weight have changed over time

x.com/EquityInsightss/status…

Nifty Sectoral Weight

Sectors where weight has increased recently : Telecom, Capital Goods, Metals, Healthcare

Sectors where weight has decreased : Technology, Consumer, Oil & Gas, Private Banks

Nifty is still heavily driven by financials, with Private Banks, Public Banks and NBFC Insurance together contributing 35%

Nifty continues to remain heavily dependent on Financials, Oil & Gas and Technology

Although Technology & Consumer weight has reduced meaningfully from the peak

src : MOFSL

3

1,120

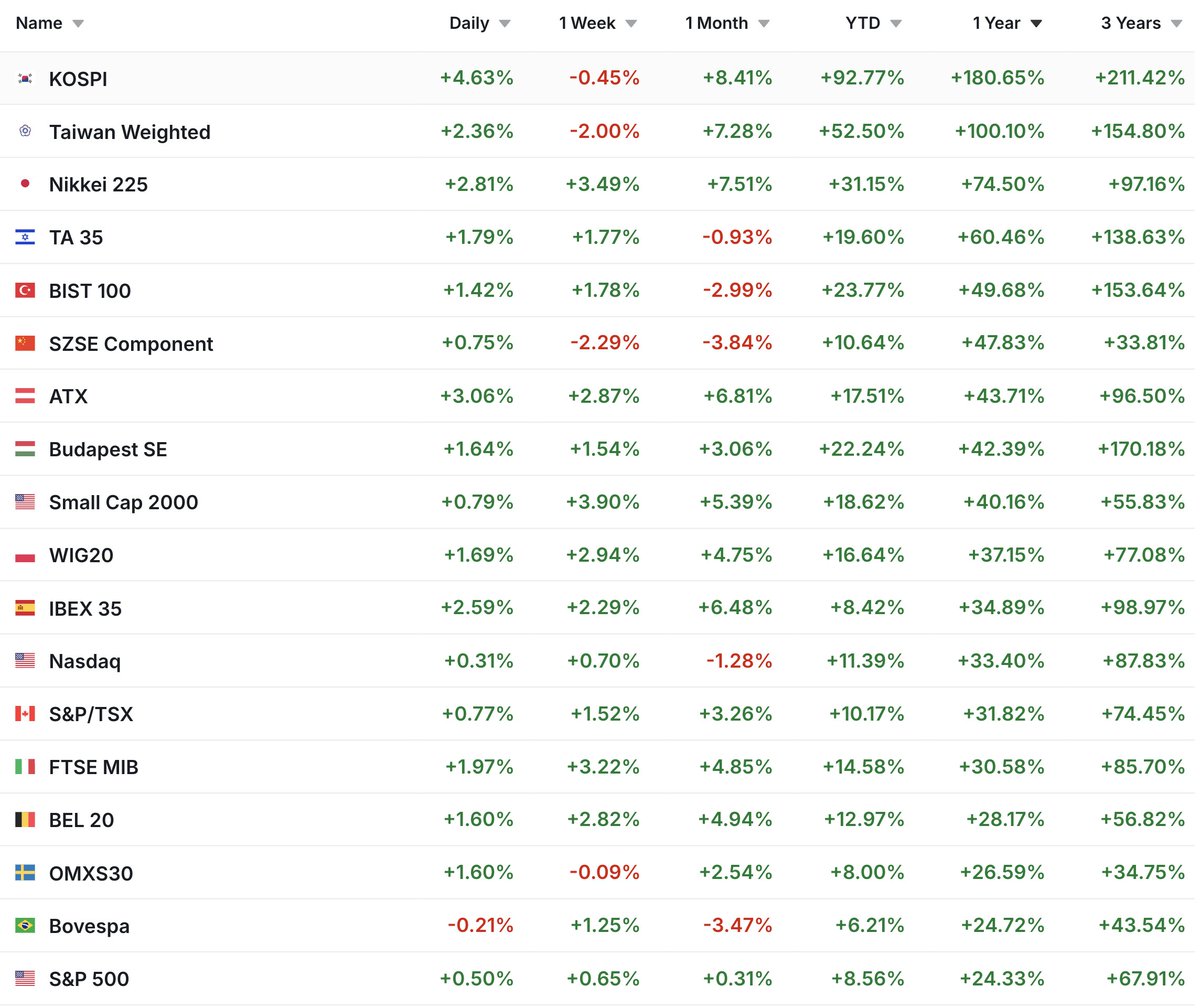

Top performing global indices over 1 year as well as YTD:

🥇 Korea

🥈 Taiwan

🥉 Japan

1

2

13

1,469

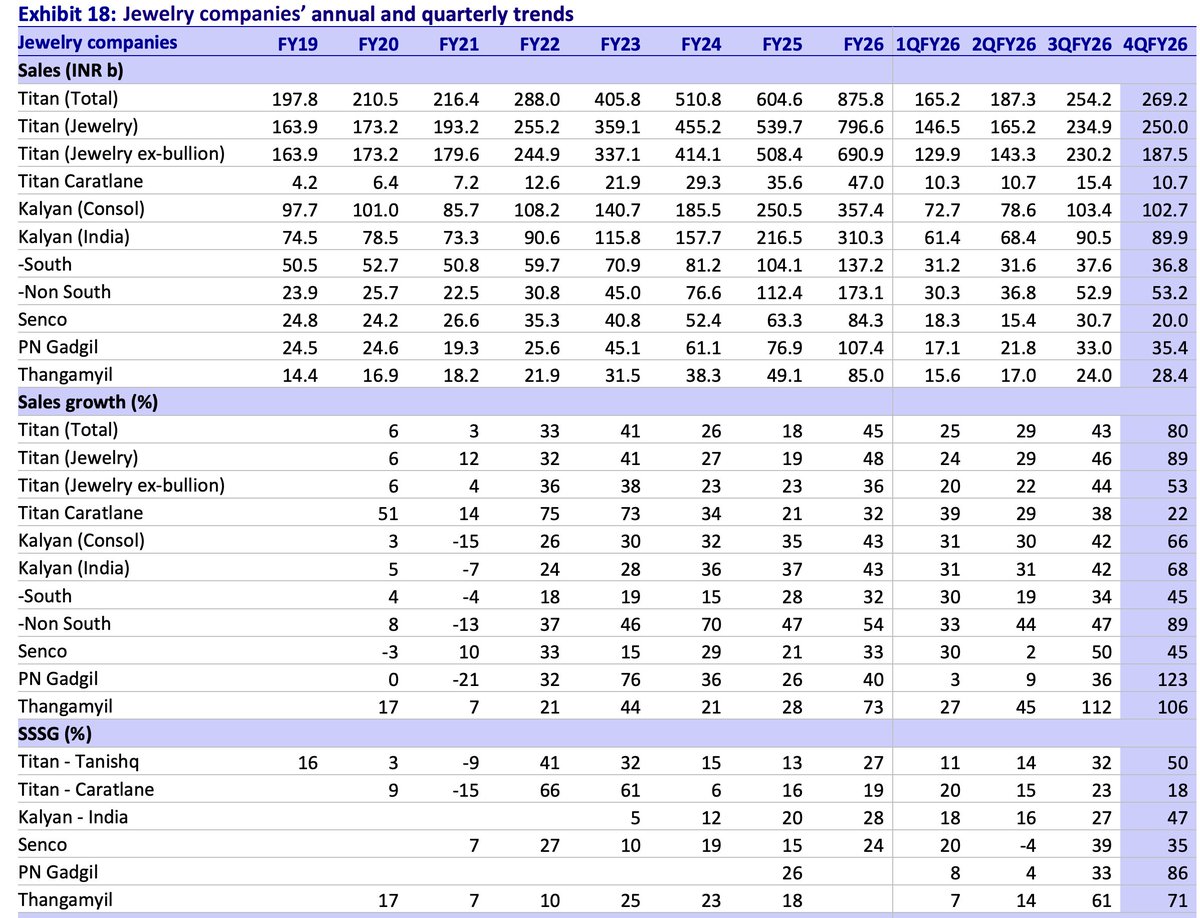

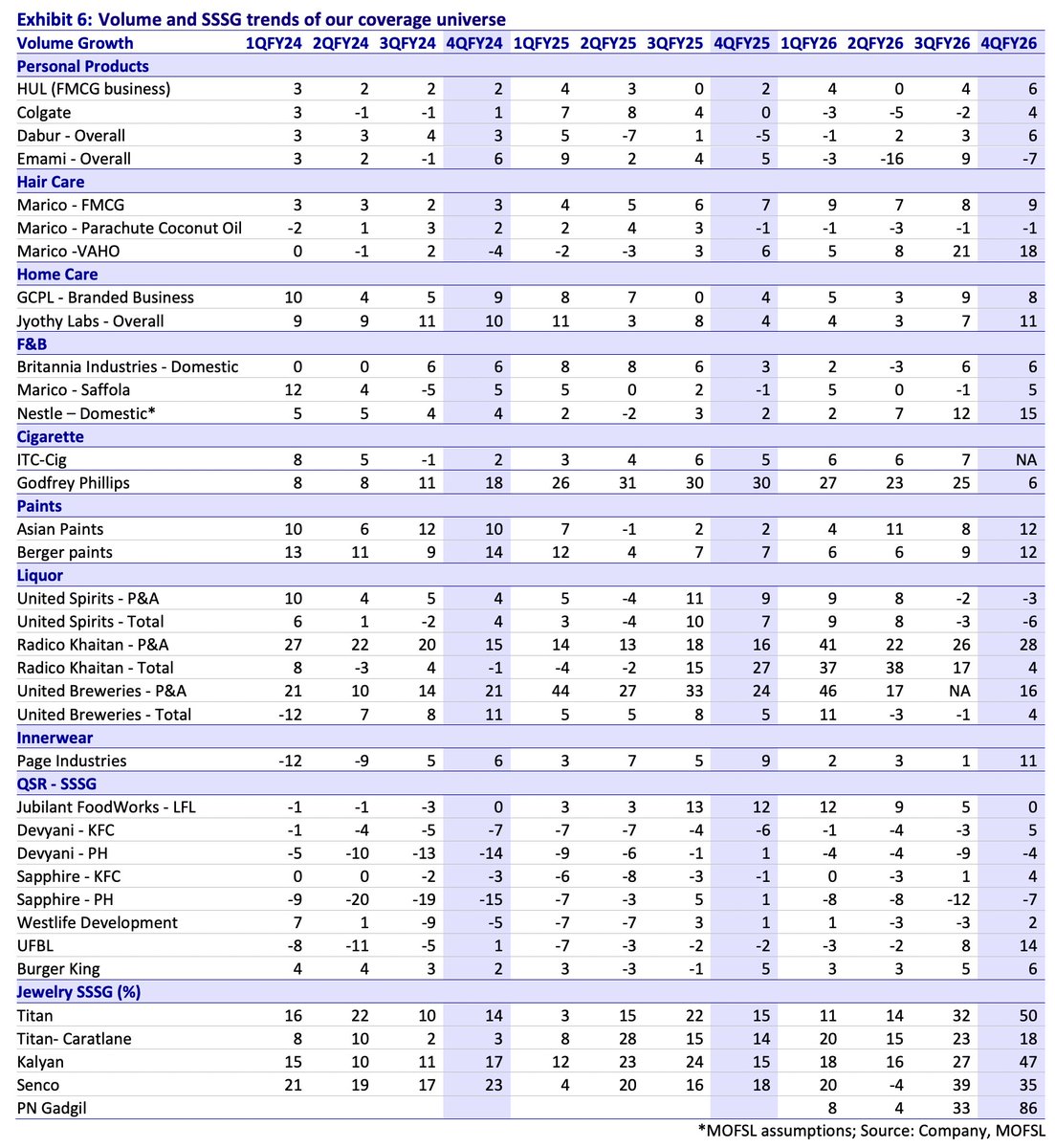

Commentary across Jewellery Companies💎

Titan, Kalyan, P N Gadgil, Senco Gold, Thangamayil, D.P. Abhushan⏬

Organised jewellers delivered strong FY26, supported by higher gold prices, wedding demand, formalization & continued store expansion

Demand has remained resilient even at elevated gold prices

Jewellery buying in India is largely budget driven

Customers generally come with an INR budget rather than a volume budget

So when gold prices rise, grammage reduces, but ticket size & REV can still remain strong

This is why many organised jewellers have been able to report strong REV growth despite high gold prices

Another major trend is old gold exchange.

Old gold exchange is becoming a structural driver for the sector

It helps customers manage affordability, supports conversion & reduces dependence on fresh gold buying

For many jewellers, old gold exchange can move towards 50% share in FY27

At the same time, bars & coins saw strong demand in FY26 because of investment led buying during rising gold prices

But bars and coins are low margin products, so whenever the mix of bars & coins increases, margins get diluted

Going ahead, if coin & bar demand slows after the duty hike, customers shift more towards jewellery, it is positive for margins

To manage high gold prices, jewellers are focusing on affordability led products

This includes: Studded jewellery, Lightweight jewellery & Lower caratage jewellery

These products help customers stay within budget & also support margin improvement

Titan is also experimenting with newer formats like Hues & beYon, showing that large players are trying to create new category engines beyond traditional jewellery

Store expansion remains a key growth driver, especially for organised players entering newer geographies & capturing market share from smaller jewellers

Kalyan is expanding outside South India, PNG is scaling outside Maharashtra, Senco is also expanding beyond East India

Kalyan & PNG are scaling through FOCO led formats

This reduces capital intensity, improves ROCE & allows faster store expansion

Growth trajectory remains intact for FY27, with most organised jewellers guiding to maintain 20% growth, led by store expansion, SSSG & continued market share gains from unorganised players.

2

35

2,869

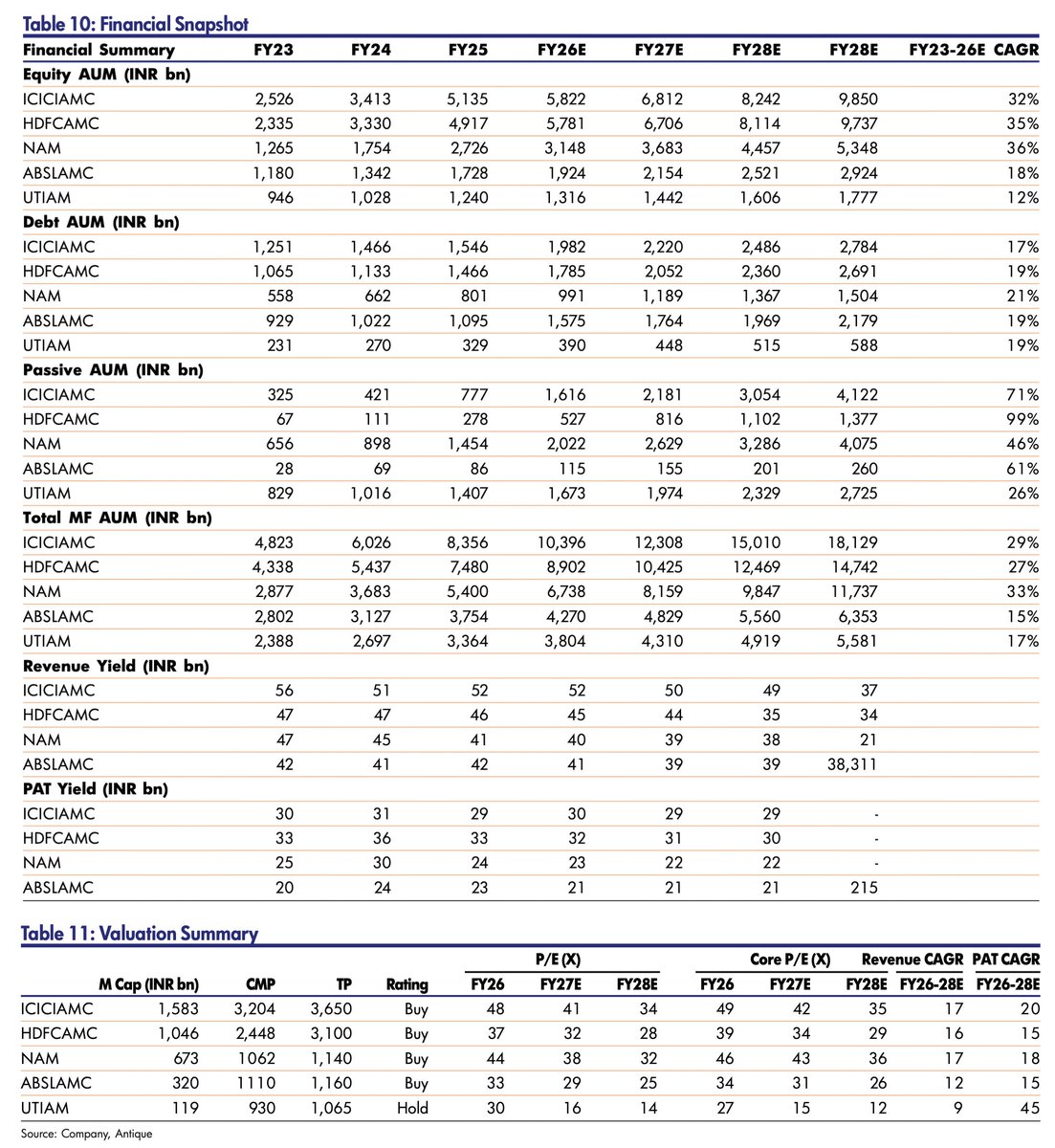

Comparison of leading AMC's - ICICI, HDFC, NAM India, ABSL & UTI AMC across AUM growth, financials & valuations

Equity AUM growth remains the strongest for NAM, HDFC & ICICI AMC, with FY23-FY26E CAGR of 36%, 35% & 32%

src : Antique

5

5

47

3,885

Top 15 Concalls Worth listening (2):

Titan

Goldiam

CarTrade Tech

TD Power

Prestige Estates

Blackbuck

Syrma SGS

Interarch Building

Rategain Travel

Privi Speciality

Edelweiss

Waaree Energies

Gaudium IVF

Coforge

Tata Capital

Many insights shared by the management, worth tracking

Not a buy/sell reco

Only for study purposes

6

7

110

7,458

Top 15 Concalls Worth listening :

Bajaj Finance

V2Retail

Garware Hi Tech

Nuvama

Pearl Global

Indo Count

SBFC Finance

360One

Smartworks

Wework

Northern ARC

Credit Access

Arman Financial

Tips Music

Vishal Mega Mart

Many insights shared by the management, worth tracking

Not a buy/sell reco

Only for study purposes

6

2,502

Titan’s new growth engines - Hues & beYon

Titan is not only focusing on traditional gold & studded jewellery, but is also creating new growth engines to expand the overall jewellery category

Titan has launched 'Hues' as its new natural gemstone based jewellery collection

The strategic rationale is to add a new dimension to jewellery beyond coins, gold jewellery & studded jewellery

Management said consumers are increasingly becoming design seekers, not just value seekers

Hues has around 200 styles, 50% of the collection is priced between Rs 40,000 & Rs 2.5 lakh, range goes up to Rs 10 lakh

The collection is focused on wearable & daily use jewellery, not just locker based jewellery

beYon is Titan’s lab grown diamond platform

Titan currently has 2 beYon stores, Management plans to scale beYon to around 10-12 stores across 2-3 cities

Company wants to first test the model at this 10-12 store scale before going for a national launch

Titan sees beYon as part of a twin-engine approach to grow diamond adoption in India

During the Valentine’s period, management said beYon saw good traction

However, they also clarified that the current sample size is too small, so they do not want to extrapolate too much from one store.

1

2

59

4,891

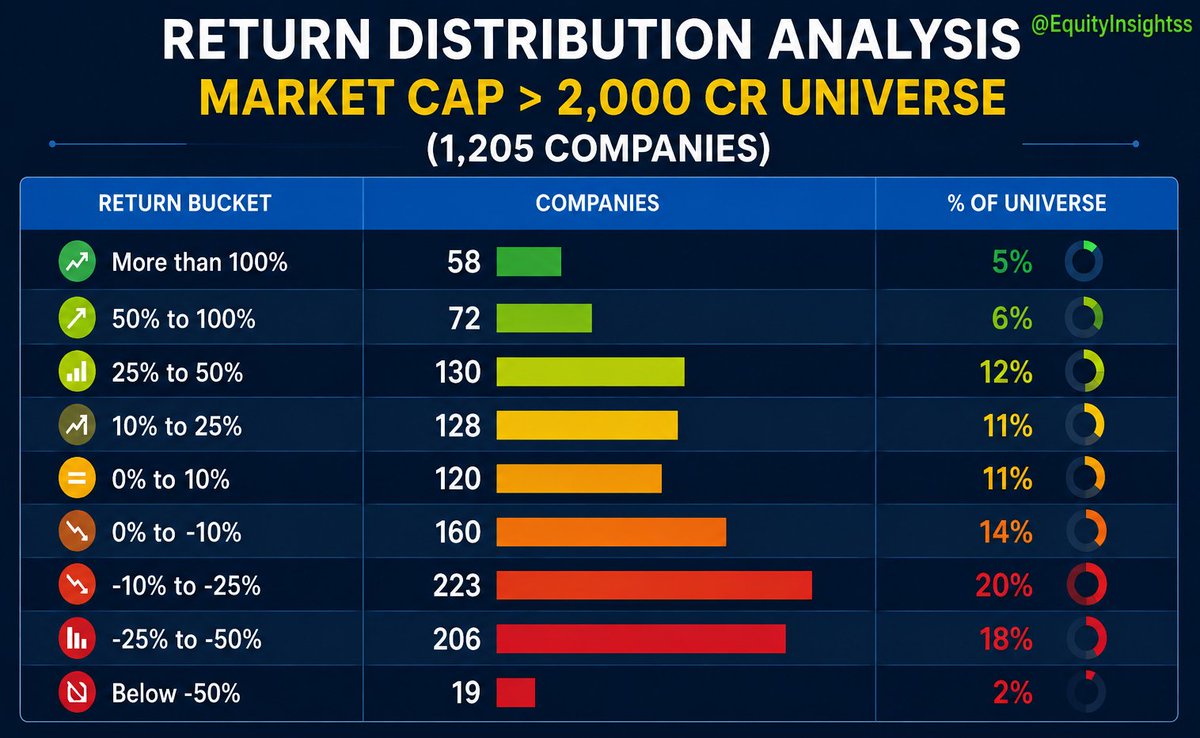

Market breadth tells a very different story from headline indices

1,205 companies in the dataset with Mcap > 2,000 Cr

Median 1 year return stood at -2.6%, while the average 1 year return stood at 10.5%.

This clearly shows that the market rally has been highly skewed.

A small set of outperformers has pulled the average return higher, while the median stock is still negative.

Only 508 companies delivered positive 1 year returns, which is 42% of the total universe & 46% of companies where 1 year return data is available

On the other hand, 608 companies delivered negative 1 year returns, which is 50% of the total universe & 54% of companies where 1 year return data is available

This means more companies have delivered negative returns than positive returns over the last 1 year.

130 companies delivered more than 50% returns, while 58 companies delivered more than 100% returns.

Wealth creation has been concentrated in a limited set of names.

At the same time, correction has also been sharp in many pockets.

Median fall from 52W high stands at 21%, while the median fall from all time high stands at 32%.

622 companies are down more than 20% from their 52W highs.

357 companies are down more than 30% from their 52W highs.

Only 140 companies are trading within 5% of their 52W highs.

Another important point is the difference between winners & losers.

Median return of companies with positive 1 year returns is 27%.

Median return of companies with negative 1 year returns is -19%.

There are pockets of massive wealth creation, but broad based participation is missing.

This is a classic selective market.

2

3

45

5,584

We have pushed our latest Smallcase rebalance

x.com/EquityInsightss/status…

We have pushed our latest Smallcase rebalance

Overall, our portfolio companies have delivered well & have largely achieved their guidance

Portfolio EPS growth stands at >25%

We added 2 new companies in this update where earnings visibility looks strong

Detailed rationale has been mentioned in the update

Outlook for FY27 also remains encouraging, with most companies continuing to guide for sustained growth momentum

Our focus remains simple - stay with companies that are delivering, exit where execution is weak.

5

3,112

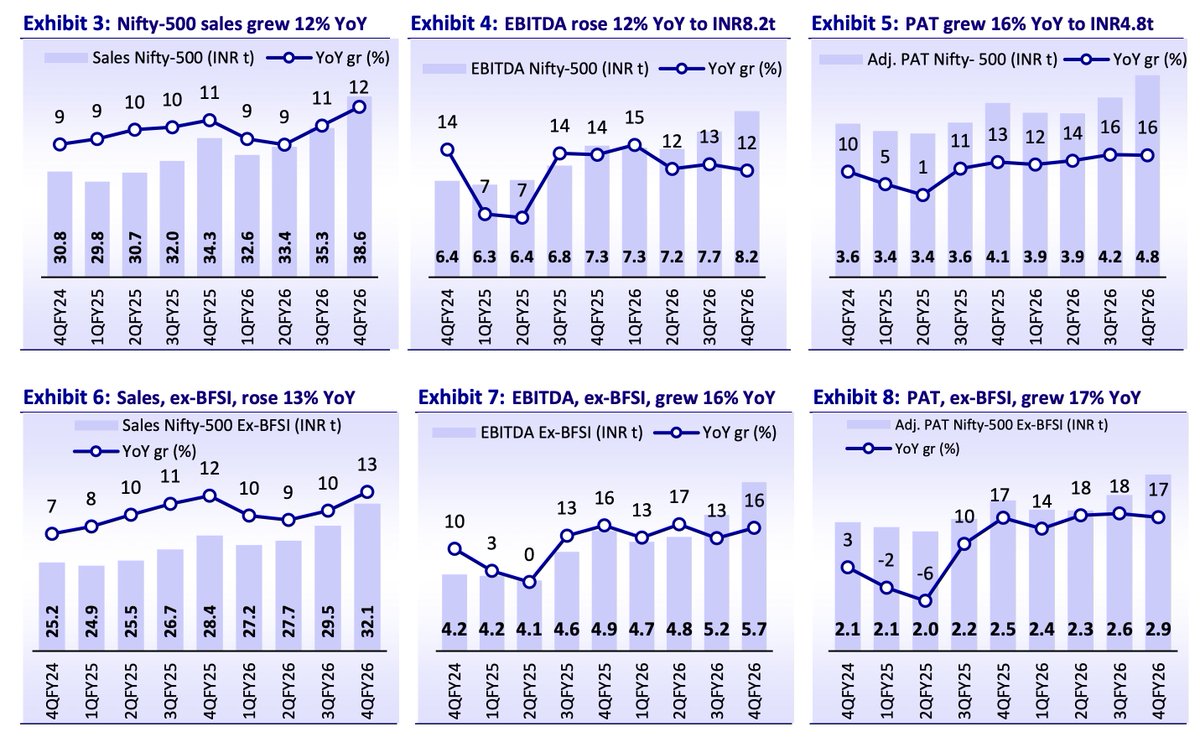

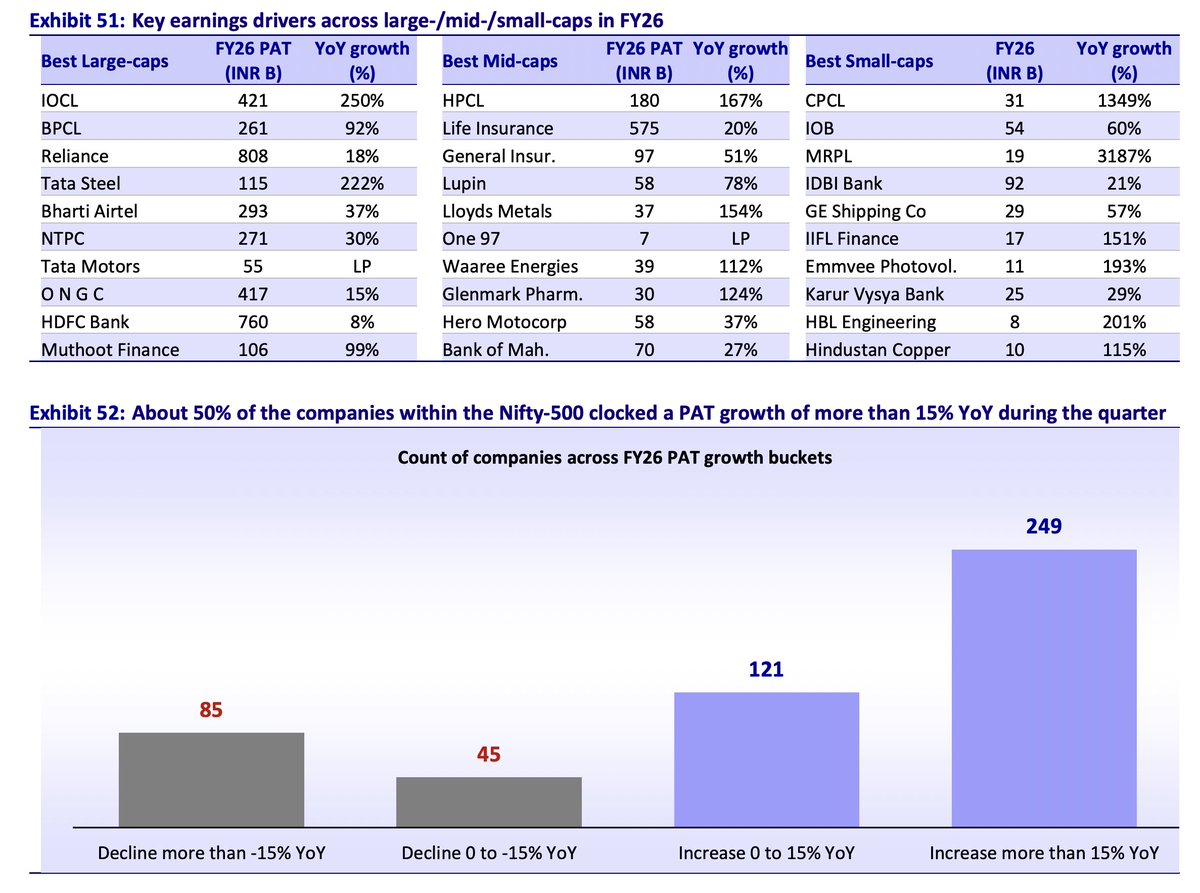

Nifty 500 delivered 16% YoY PAT growth in Q4FY26

Ex-financials, earnings growth was even stronger at 17% YoY

Nifty500 PAT grew 16% YoY vs Nifty50 PAT growth of only 4% YoY

Nifty500 EBITDA grew 12% YoY vs Nifty50 EBITDA growth of 5% YoY

Sales growth for Nifty500 stood at 12% YoY, which was the highest in the last 13 quarters

Nifty Midcap150 PAT grew 34% YoY, much higher than Nifty500 at 16%, Nifty100 at 12% & Smallcap250 at 13%

Around 50% of Nifty 500 co's reported earnings growth above 15% YoY

src : MOFSL

2

1

44

4,308

AI stock of India?

Up 700% in 1 year, trading at 199x earnings

31

12

356

45,940

Crazy ! Cupid have given REV & PAT guidance till FY29 !

They ended FY26 with

REV : 358 Cr & PAT : 108 Cr

They are projecting 390 Cr PAT in FY29...

1

16

5,556

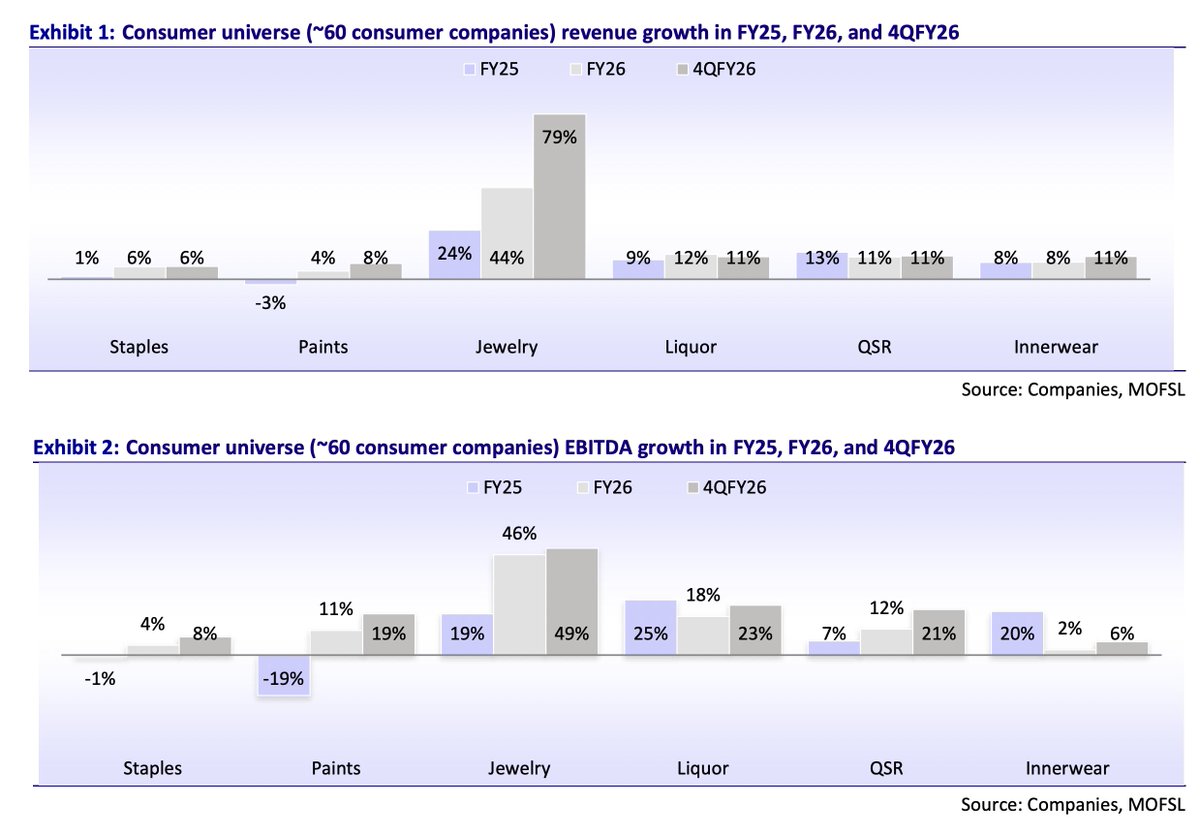

Growth trend across the Consumer Universe

It compares REV & EBITDA growth across key segments like staples, paints, jewellery, liquor, QSR & innerwear

Jewellery is the clear outperformer in the consumer space

Paints have started recovering after a weak FY25, other segments are also seeing early signs of recovery

src : MOFSL

4

1

31

4,129

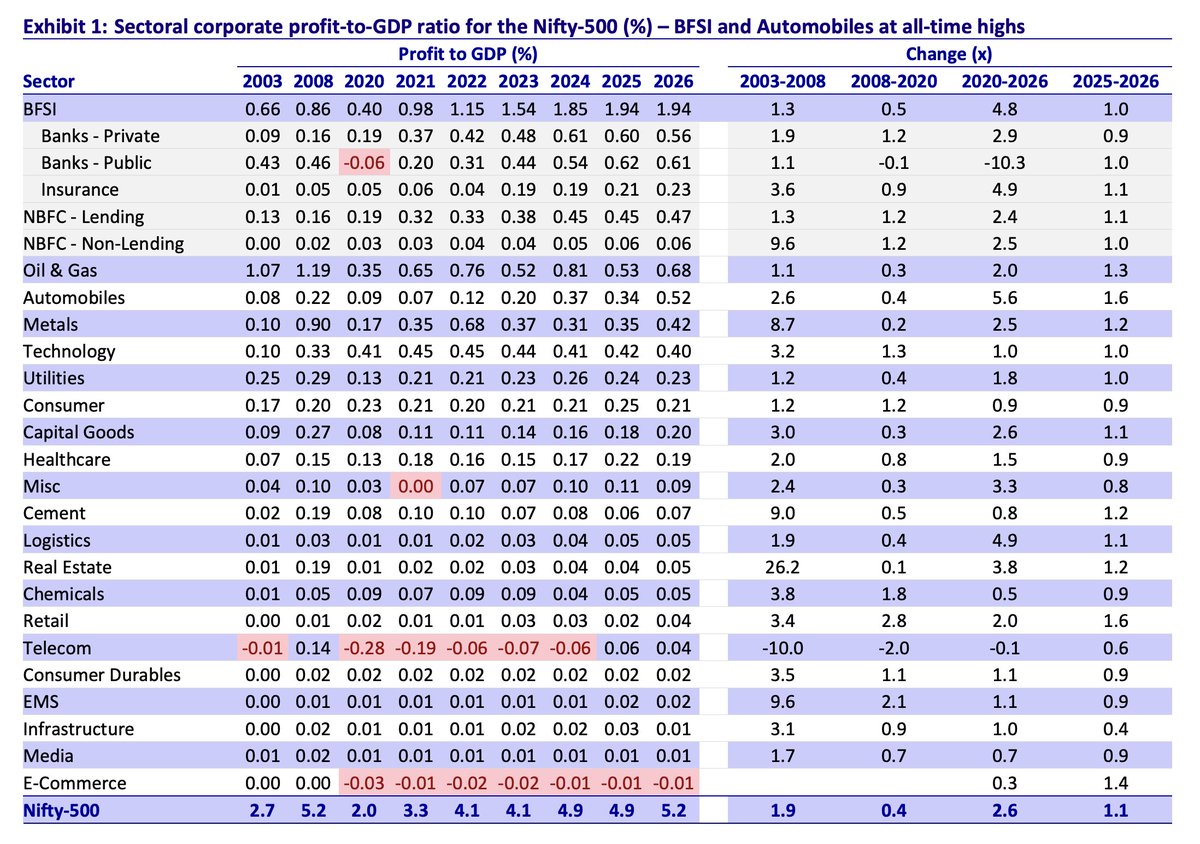

Nifty 500 corporate profit/GDP ratio surged to an all time high of 5.2% in FY26

This is a major milestone, as corporate profitability has now surpassed the previous peak of 5.2% seen in FY08

Corporate profits grew 15.6% YoY in FY26 while Nominal GDP grew 8.9% YoY in FY26

The key point is that corporate profit growth continues to outpace nominal GDP growth

The journey has been quite interesting

From 5.2% in FY08, the ratio declined consistently & bottomed at 2% in FY20

src : MOFSL

5

5

57

8,403

Nifty 500 REV & Margins trend

Strongest growth phase was b/w FY03-FY08

2

12

2,207

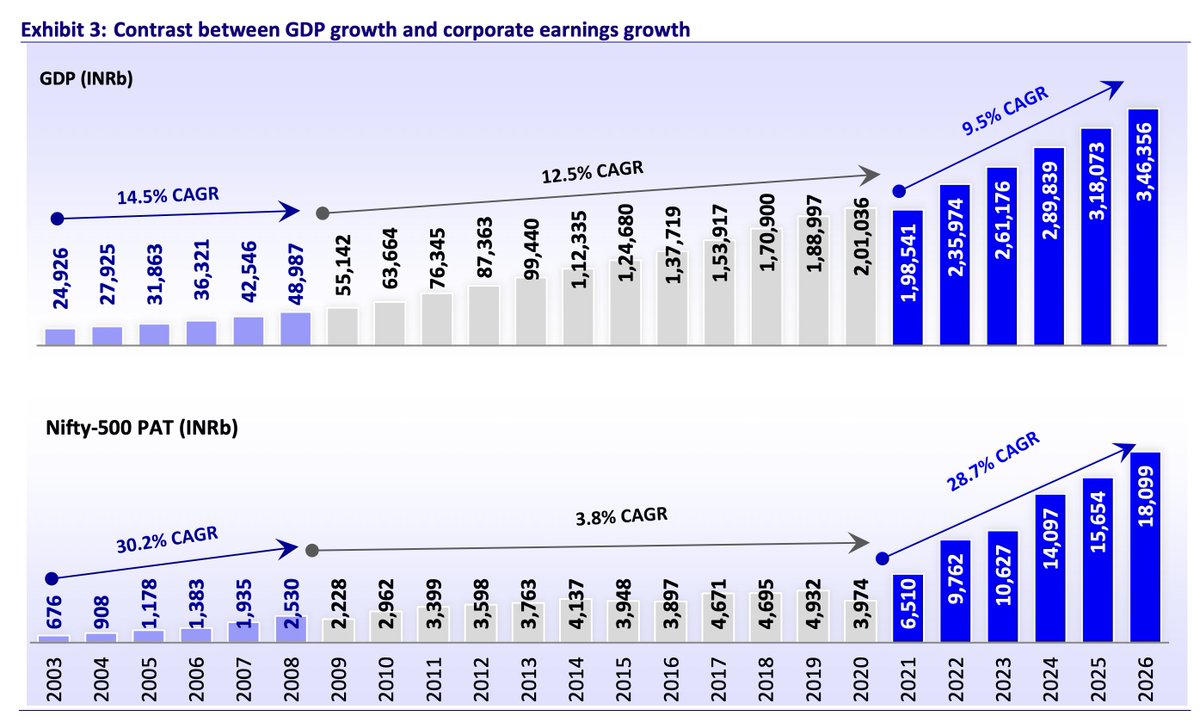

During 2003-08, India’s GDP compounded at 14.5% CAGR, while Nifty 500 PAT compounded at a much stronger 30% CAGR

During 2008-20, GDP still compounded at 12.5% CAGR, but Nifty 500 PAT grew at only 3.8% CAGR

This led to the corporate profit/GDP ratio falling from 5.2% in FY08 to just 2% in FY20

During 2020-26, GDP growth was relatively lower at 9.5% CAGR, but Nifty 500 PAT compounded at 29% CAGR

src : MOFSL

6

16

77

7,826

Sectoral corporate profit/GDP ratio for Nifty 500

13

2,386

All research reports & insights shared here

t.me/equityinsightselite

5

2,389