differentiated insights for value investing . Thats it

Joined August 2024

- Tweets 9,106

- Following 62

- Followers 19,849

- Likes 8,446

2,825 Photos and videos

Pinned Tweet

3 Aug 2025

My take on position sizing , very less spoken about when it comes to process building

Understanding this opens up lot more non linearity of gains

8 Jun 2025

My take on position sizing , hope some of you may find it useful

10

11

156

133,713

ValueEquity retweeted

While you all know which of our ideas have delivered very well and grown multifold in returns and we made a lot , this is a post to showcase some mistakes and where I have gone wrong with my initial thesis ( highlighting 3 of all types of mistakes to avoid , that I did so you don't have to )

1) Rupa ( down 28% and had to exit , this was 2 years back, in Hindsight a pathetic investment , but lets see what went wrong

The managing family has run this household name famous brand , in my initial thesis I was looking to play the post covid rural recovery that would play out across their product portfolio and the regions that they focused on

The main mistake I made : did not judge the management well ! They made a series of bad decisions and I kept watching it , first it took them forever to find a new CEO, they invested heavily in the Lal sing chadda film and thought that would cause a turnaround ( remember bubba from forest gump? this was a bad movie showcasing the same with Aamir Khan and Rupa

I think one thing that I really learnt is how the most obvious theme should be played better , I could've easily chosen better companies to play the rural recovery , from lenders to other brands , but I not only lost some money on this , also for 2 years wasted my portfolio space on this , hence I always learnt the need to play the right theme through the right company matters more than actually picking the right theme

2) Ola Electric ( up 7% on this now , but at one point it was down 24%, still own the shares) but was still a bad relative decision from relative market

Over the years , I always focus on looking at industry structure first then looking at qualitative factors that matter with developing my channel as well to see on ground situation, but in this case I dont regret investing in Ola but I regret the fact that it was the second best decision

The best decision ( which I should have made, but did not ) was to invest in Ather , everything was in their favor , market share rate of change , quality , better customer relationships and also the numbers, but because of seeing some good gains in the portfolio I made a poor decision of playing the Ola turnaround ( got in too early and Ignored the opportunity cost and also let the bias of how cheap can it get ( rookie mistake ) , but no harm in accepting it

I still believe they might be able to turnaround , but I regret not being able to make the better decision which was not only obvious now but also then

3) PDS ( -30% and had exited ) , a lot of you think why I keep focusing on entry valuation so much even in very high quality businesses , this is my reason

PDS is a great business , they have the best in class brands , great PE kind of investments as well , even a world class apparel sourcing system ( HBS even has a case study on how good their business model is )

But my mistake was entering at really high valuation cycle where the earnings were almost near highs , post which due to some client issues and nature of cycle changing , the equation changed , and that's what happens when you pay up , the fragility increases , as high your entry valuation is , the less number of things have to go wrong to loose money , small mistakes cost big when your entry valuations are wrong

Also , another mistake I ignored and honestly that should've been the very easy exit decision is when they hired BCG for consulting on " margin improvements and sustainability " , this is obviously a sign that things are getting worse , managements hire consultants only in 2 cases , either they want global validation , or when they need someone to blame

In any case , as an investor it was a bad idea to let it happen , as I say in India the opportunity cost of making a mistake is very high in investing , there are many companies that are doing really good things and we need to make sure we avoid bad decisions to let the good ones do their job well

Lesson learnt , that good companies bought at bad valuations can hurt

The point of sharing these mistakes is so that you all don't do what I did , and that mistakes are a part of the game , and even after making these stupid mistakes , the portfolio has done better in multiples to the indices , but mistakes happen , goal is not to repeat them ,

I will keep repeating , goal is to build a process with a 60-70% hit rate right position sizing , this will take care of everything !

1

3

27

1,817

ValueEquity retweeted

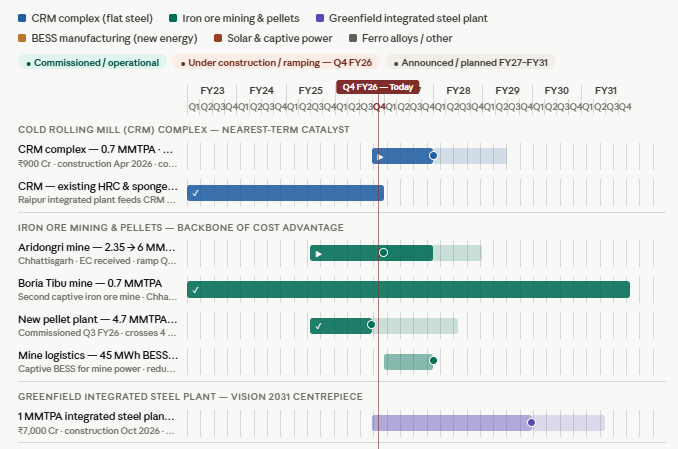

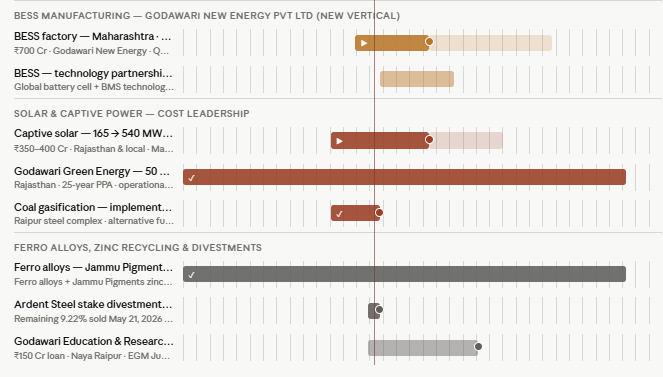

GPIL capex tracker

source: internal research

1

13

1,923

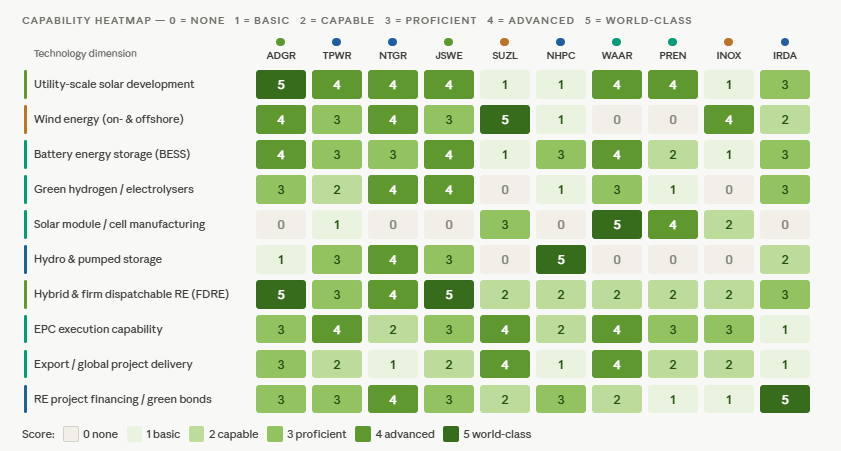

Renewable energy players in India , capability mapping of the companies

source: internal research

1

2

18

1,950

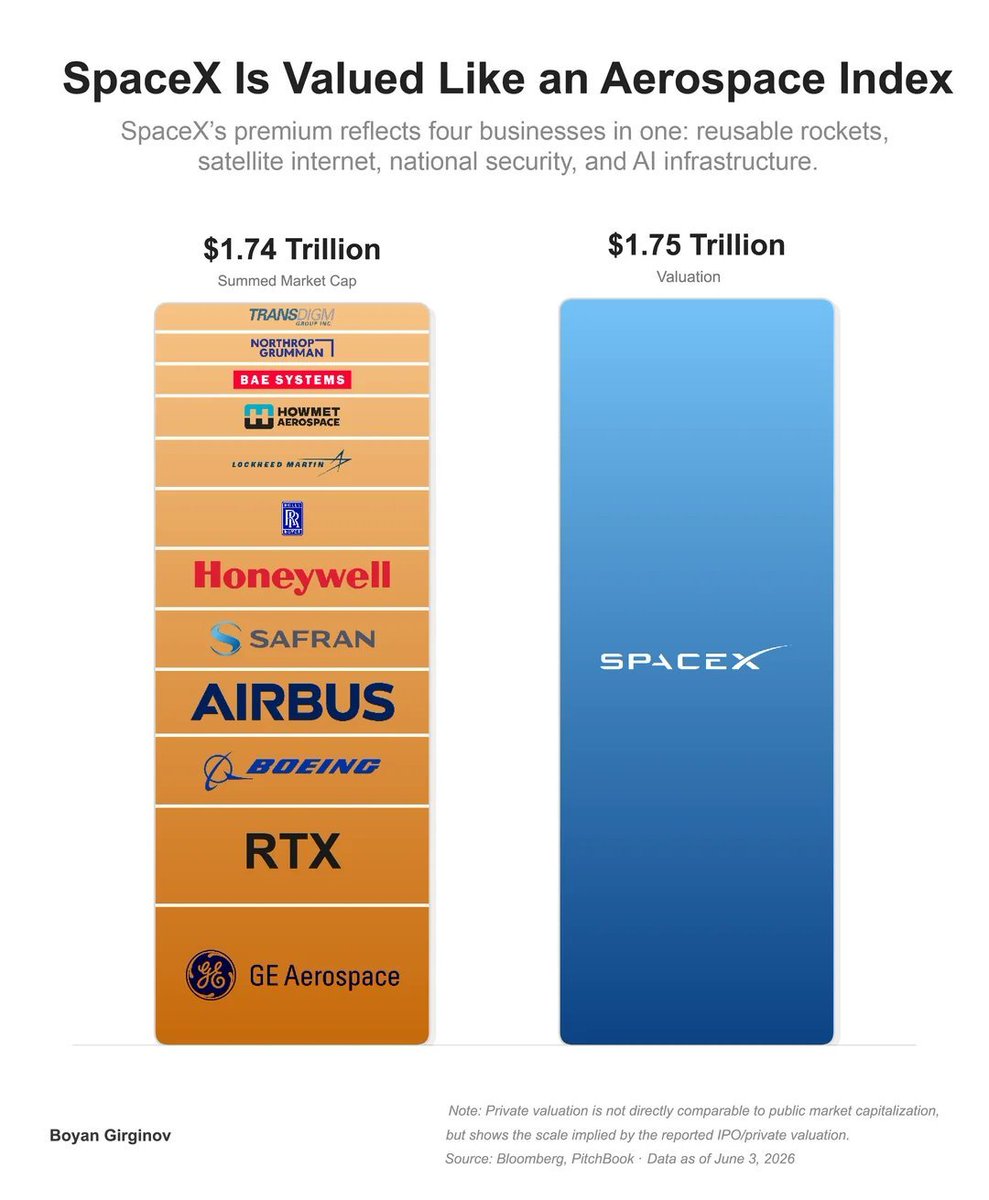

CDMO sector , my key takeaways from recent Wuxi and US government guidelines and what to take away from it

Jun 12

CDMO sector and Wuxi recent guidelines from US government very well explained by the management of BlueJet Healthcare , that yes theme is strong , but not to take this as Euphoria

My understanding

1) This is only for federally funded programme

2) China still ahead a lot in ADC and wallet share of US customers , main goal is to take some of that wallet

3) 5 years time to notify , running contracts are not impacted at all , it is mostly incremental

4) yes there is definitely a China 1 but it is not as Euphoric as is portrayed , structurally positive reset , but euphoria is misplaced

5) we will have a needle moving impact because we still have incremental scope that is really large , focusing on capacity and platform diversification

( R&D)

youtube.com/watch?v=Hefgn3Ia…

source: @NDTVProfit and great questions by @niraj_shah and @TamannaInamdar

1

20

2,533

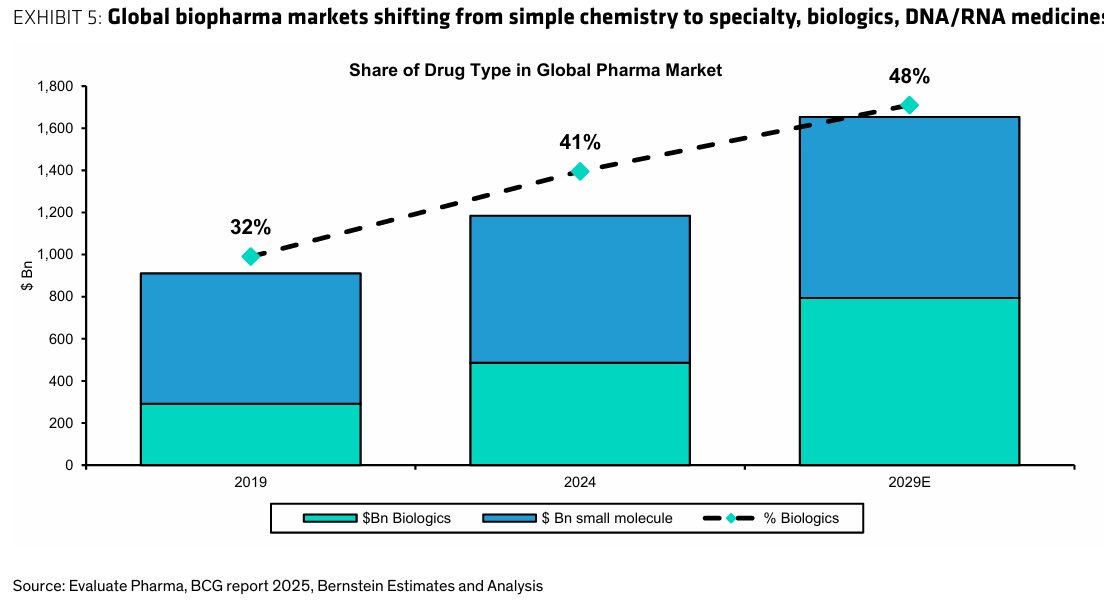

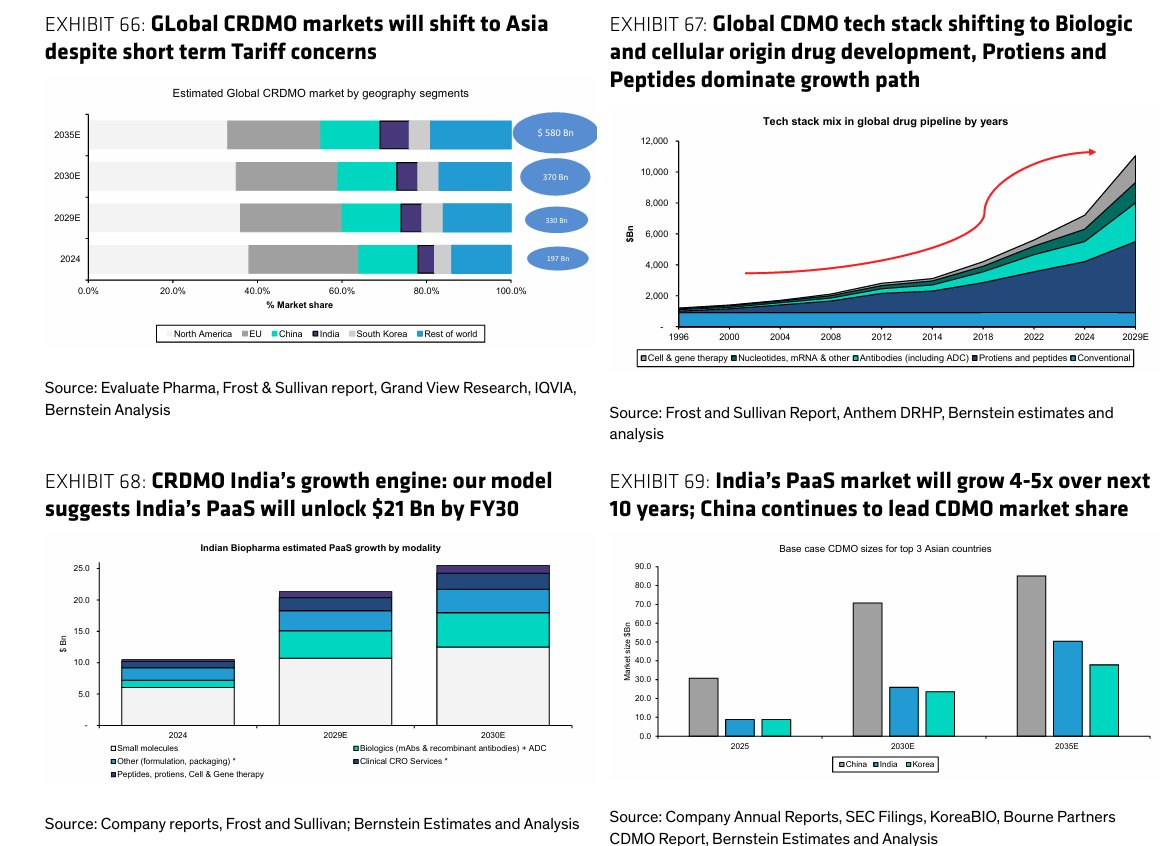

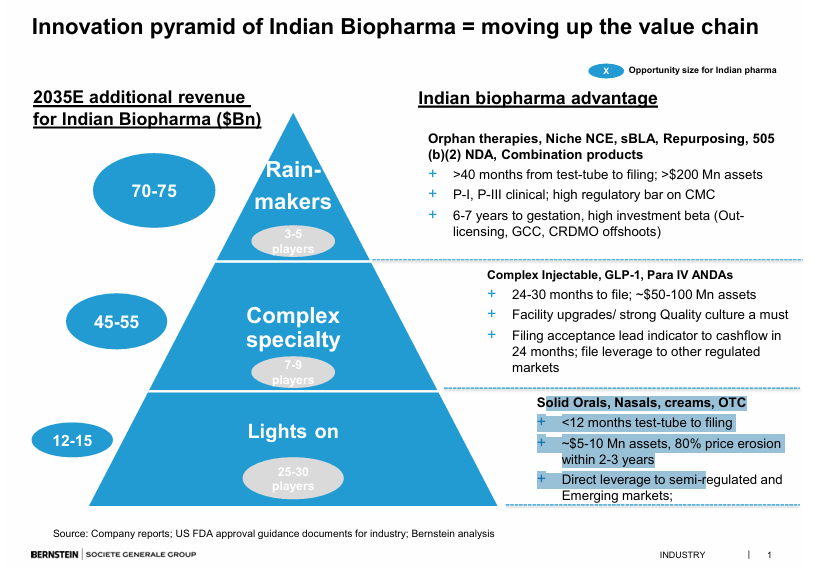

Global biopharma markets shifting from simple chemistry to specialty, biologics, DNA/RNA medicines and also most importantly it contributes incrementally large to the profit pool as well

Moving up the value chain adds ~126Bn to Industry by 2035, also mapping out the Indian Biopharma revenue by asset type

Focus on capability depth building and where the capex is going into , those will be the levers of the incremental growth !

2

25

1,937

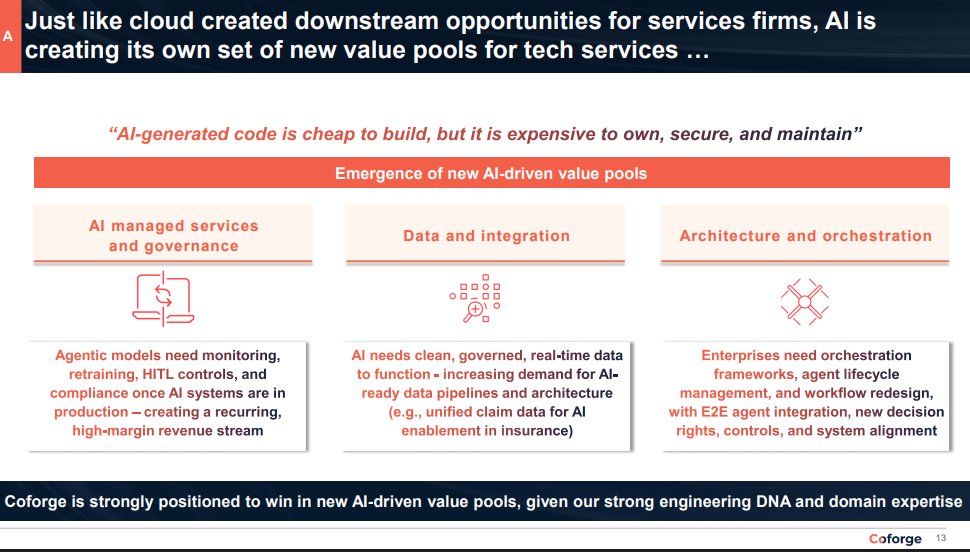

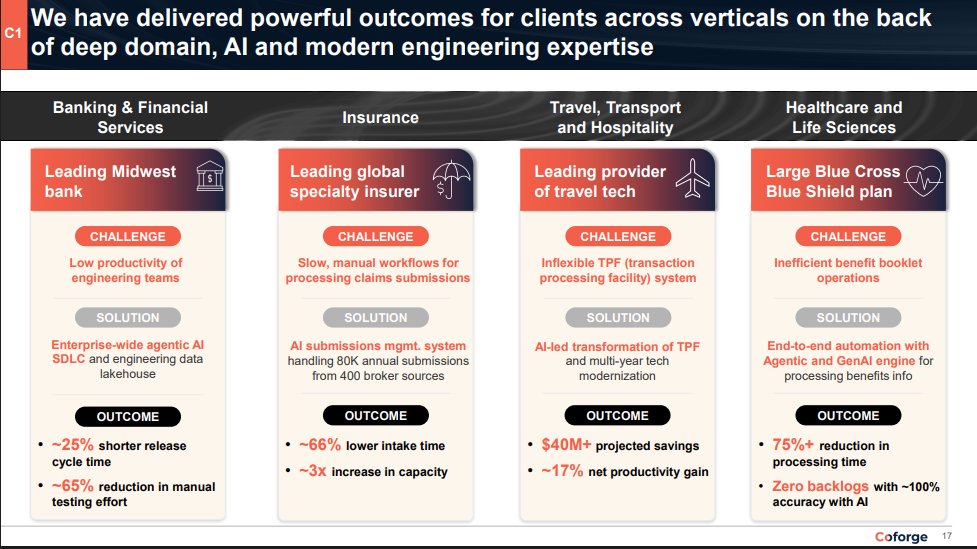

Coforge , they believe AI is rapidly creating new value pools for the industry and unlocking a $ 160-180B market opportunity growing at 35% to hit ~$800B in the next 5 years

On market sentiment , Services aren’t disappearing, but rather recomposing, as “labour-as-default” gets disrupted by agent delivery

Coforge is focusing aggressively deploying hybrid AI ‘Mod Squads’ – a bespoke delivery unit, grounded in deep domain intelligence, which generalist models simply cannot match

For evaluating IT co's that can pivot now these are things to look for

1) Hours /Person billing shifting to outcome based billing

2) Solutions stack has to pivot to domain specific guardrail relied and agentic solutions with strong sectoral niche rather than a one size fits all

3) Employee force has to pivot to AI usage internally and enterprise level AI has to be a norm to clients , pivoting the whole approach

disc: biased , no reco , no financial advice

3

42

2,750

Why sideways markets help broadening research universe and it’s honestly a best market to someone who’s playing the long game

Jan 12

Sideways markets give the best opportunity to research and build competence and understanding in sectors and track peak pessimism and also good growth opportunities

1) Concalls are more rational in tough sectors that were once darlings of the market pessimism sector calls like Chemicals, Pipes , Microfinance , no aggressive guidance , more business specific conversations in calls and rationality prevailing in analysts questions also increasing quality of conversation

2) Frustrated shareholders in good companies, sideways markets can be brutal , some small headwinds or short term issues end up correcting stocks with structural tailwinds and earnings trajectories , this is where the opportunity for the incremental shareholder comes into the picture to read and create a differentiated insight

3) Going aggressive in research in sideways market , as there is a base case sentiment everywhere , it is easier to read companies as the stocks don't run away , you get time to build a good pipeline of opportunities

15

2,694

ValueEquity retweeted

Jun 13

PPFAS Flexi cap , one additional reasons its better then many flexicap funds is that they have seen many cycles of managing public money , From fragile 5 in 2014, to demonetization to Covid , Russia and Ukraine and still remained to their thesis of value and never budged , will always hold that respect !

This is my opinion , and you all know that I like schemes from Helios and Old bridge too , and not a lot of people agree with that , but I think some of them are doing a phenomenal job , with Sameer and Kenneth at the forefront ! ( see their previous track record )

My MF pf is fairly concentrated but I think alot about it , yes PPFAS flexicap is now similar to a large cap scheme , but I trust their ability to keep deploying capital at better rates as our market grows as well !

3

3

69

8,913

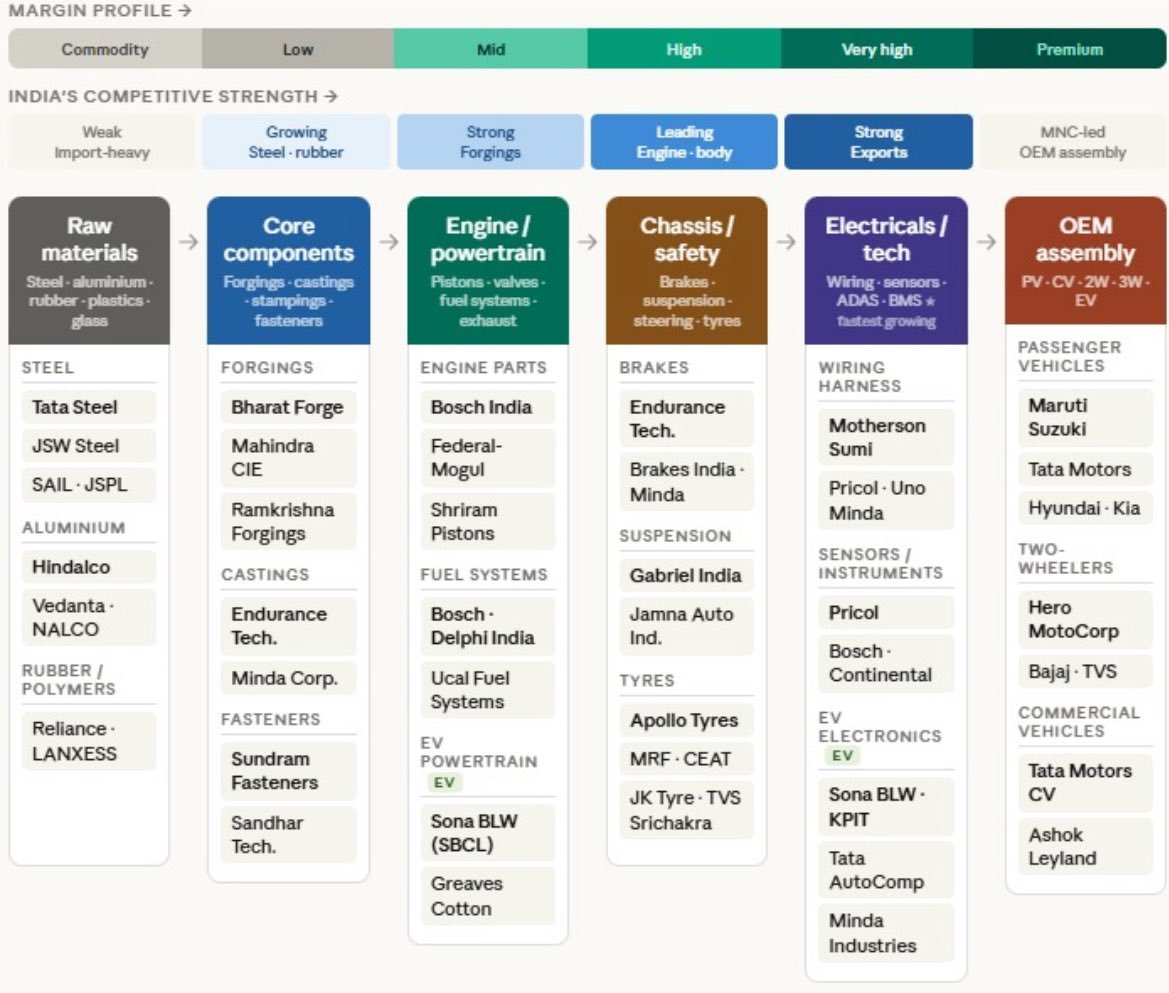

Auto ancillaries Industry in India , mapping the companies with stage , detailed chart with presence in value chain

source: internal research

May 19

Auto ancillaries Industry in India , mapping the companies with stage , detailed chart with presence in value chain

source: internal research

1

26

2,949

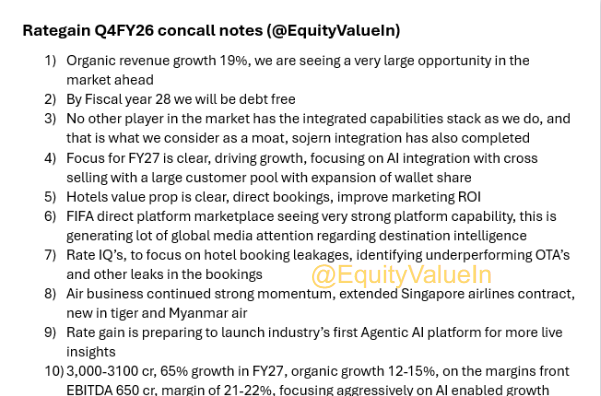

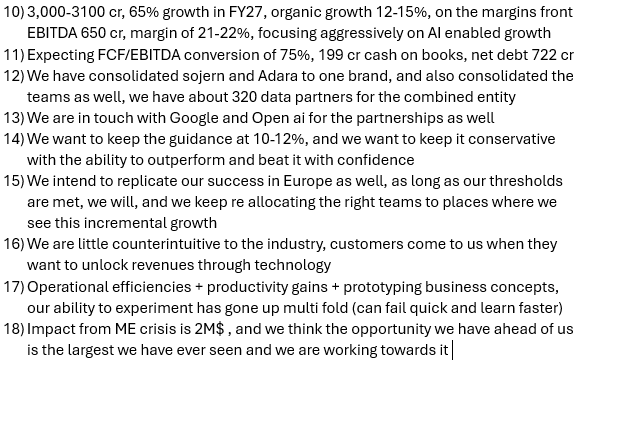

Jun 13

Rategain Technologies Q4FY26 concall notes , my notes

Done well

May 22

Rategain Technologies Q4FY26 concall notes ,my notes from the call concluded , some very interesting commentary on using AI and also creating a culture to keep experimenting through AI based focused outcomes

One of the co's in IT space I like a lot , apart from the my usual favorites like coforge , indegene !

2

29

3,036

Jun 13

IT companies I like and their commentaries on AI , Rategain has already done very well in last 2 months!

May 23

Rategain : We are enabling AI into all our offerings , but also using it internally to run experiments aggressively for less cost , prototype products and focusing on experimenting so we can expand our product reach , fail fast to grow right

Coforge: Focusing on Outcome based billing, integrating newer solutions and training an AI Enabled workforce that can build enterprise level Agentic AI solutions that can actually solve industry problems

AI is creating value pools, 6 MOAT’s we believe - deep domain expertise (generic AI is commodity), strong client intimacy (focusing on relationship), re invented delivery models (monetization AI employees), Agility at scale, Scalable purpose-built agents (One AI Platform) and AI enabled workforce

Indegene : AI domain expertise led growth is what we intended to capture , domain knowledge ( pharma ) with the ability to offer more agentic platform level solutions can help us grow wallet share substantially

In the 3 IT companies I like , things in common , focus on agentic enterprise AI , wallet share expansion and ability to capture profit pool , these are key notes I liked from their recent management commentaries

21

3,099

Jun 13

Mumbai through Atal Setu always remains a good reminder for the amazing infra that is being built in India , amazing stuff , I enjoy this every time

2

38

3,340

Jun 13

Lots of interest for the spaces , thanks folks ! , I realized last one was a a while ago .. , anything specific you all want me to add as well?

Jun 11

Should we do a spaces soon ? Been a while ..

Let me know if you folks are interested !

5

15

3,388

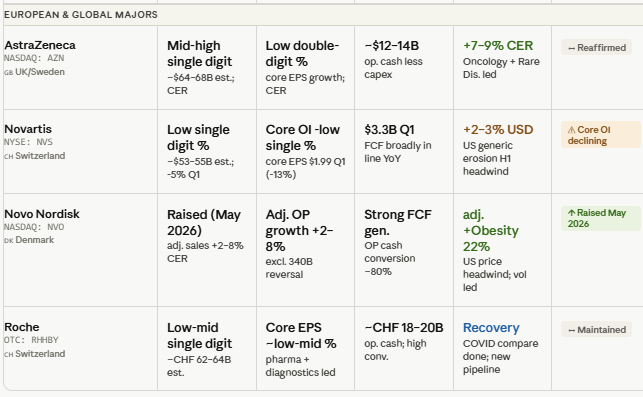

Jun 13

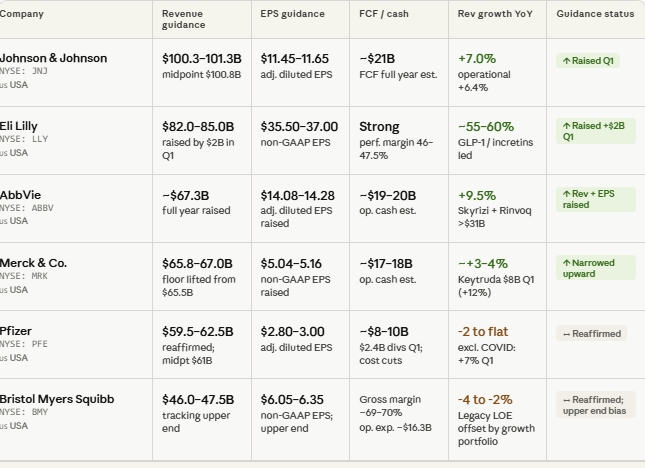

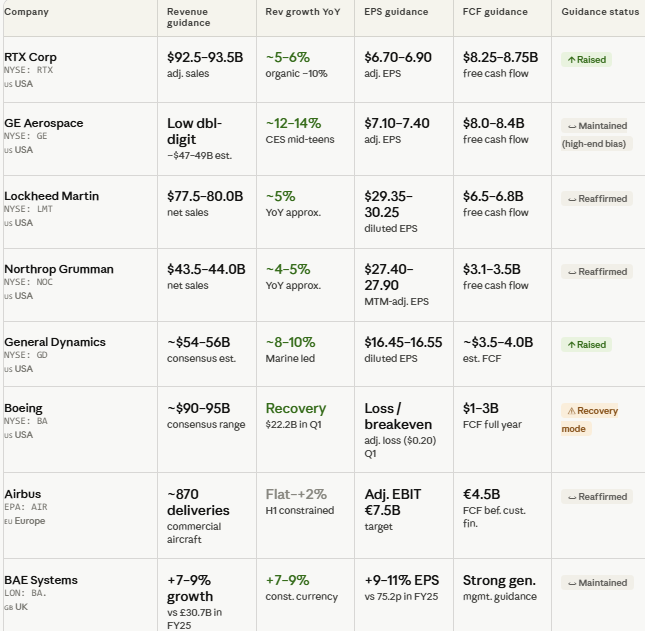

Global Big Pharma numbers and guidance for the next year ,key patent related info and mapping the players

Will also do a post on the pipeline and mapping the

Indian partners so we can start mapping out profit chains

source: internal research

6

49

3,608

Jun 13

Doing a post on my investing mistakes over the weekend

From Rupa , Ola to PDS and how things can go wrong sometimes with due process and what I learnt from it

2

41

3,138

Jun 13

Don't confuse conviction and ego , if market does not reward your thesis after the duration of your thesis plays out and you continue to hold on to an underperforming business , not because of short term problems but structural problems , do not let the ego be justified by calling it conviction , admit the error and move forward

And time adjusted return is very important , conviction is good when you know the game you play , do not confuse it

I have also made these mistakes , and learnt from them to be a little wiser than yesterday

4

2

28

2,119

Jun 13

One thing to note is how much weightage you give to the perception multiple of a company , is a multiple higher on the basis of a story or ability to execute , any way it is a thin line to see this

I have tried to put some work on trying to work on how to look at multiples in the context of story , early days but so far have a loose theory around it , will write about it

1

22

1,959