Always Running Mid-Cycle Pricing. Former Sell-Side Analyst. Roaming around the private markets now. Not Investment Advice

Joined January 2018

- Tweets 185

- Following 1,267

- Followers 685

- Likes 823

23 Photos and videos

Is it just me or do the #'s not tie here? The "DCF Scenario" output has PV of TV of $2.1T and The target price calc has a PV of TV of $2.4T.... Same PV of uFCF, same terminal growth and same WACC. Seems to be lower discount factor implying 2 less years of discounting. What am I missing? At the lower TV would imply a TP of ~$160/sh vs. $190/sh.

1

346

Preview of NY if the Knicks win the ship

May 30

Fires and clashes near Parc des Princes after PSG beat Arsenal in the Champions League. Scooters and bikes torched, riot police deployed. Familiar scene after major PSG wins.

1

6

1,357

New VC-subsidized service just dropped. Get it while it lasts and before AI makes the physical economy a dystopia just like the current state of white collar work

May 28

Today, we're launching shift. We're starting by cleaning your apartment in New York City, for free.

Here's how it works. Book a shift cleaning. A vetted shift operator comes to your home wearing one of our devices. They clean. They leave. You pay nothing.

In exchange, we record the cleaning. Robotics is being built on data about how people do daily tasks, and the value of that recording is what funds the service. Anything personal in it is anonymized before the recording is processed.

By now, you have heard about the shift to AI more times than you can count. About the shift toward you, the part where you actually feel it, you have heard almost nothing. Shift is what starts to make it concrete, in specific cities, with specific services.

Today, cleaning in New York. Soon, handymen, repairs, and errands across the globe. And this is just one side of shift, with more on the way.

Comment “shift” and we’ll send you an early access link.

1

289

The $GFL / $SES.TO merger getting this contentious wasn't on my bingo card.

My position is unchanged: this isn't the optimal outcome for either party. That said, $SES.TO shareholders are getting a good price today. At 11x forward (announced price) or ~10.5x using current $GFL price, investors should take their ball and go home. For continued energy beta via OFS, I'd point you to $CEU.TO, a best-in-class specialty chemicals biz trading at 9.5x that's tied to production (vs. drilling activity), much like $SES.TO's base biz.

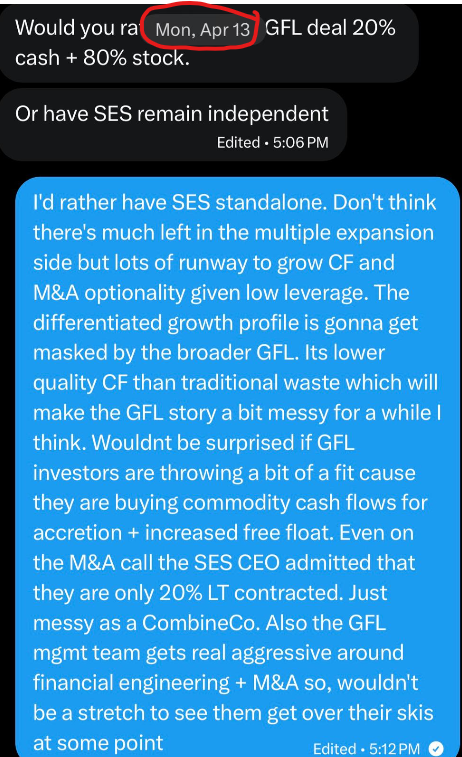

My comment below on preferring $SES.TO standalone is b/c a combo with $GFL is sub-optimal for both sides.

$GFL shareholders want truly non-cyclical CFs. Adding OFS pressures the multiple by muddying the story and weakens $GFL's ability to do accretive SW M&A, especially opportunistic M&A in economic downcycles.

For $SES.TO shareholders, the standalone growth profile gets watered down by the broader $GFL. That's not to say $SES.TO is a "waste" biz whose chart will grind up and to the right, as many suggest. When the next energy downcycle hits (and it will), the multiple will compress dramatically. But $SES.TO holders should be given the chance to trade around that growth profile and energy cycle volatility.

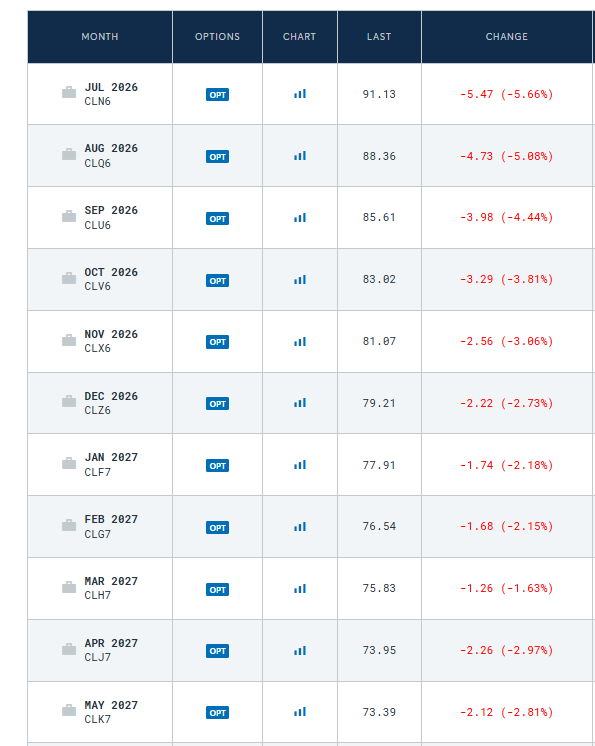

My near-term view on $SES.TO is positive: the Iran situation should inject a geopolitical risk premium into oil that we haven't seen in a decade . Layer on renewed focus on security of supply, which will point major crude and products buyers to NAM. $SES.TO's core business will benefit because it supports Canada's long-life resource base and an oil price anywhere close to US$80 is great for basin-wide profitability and will support healthy activity levels.

If $SES.TO's multiple keeps grinding higher as generalists conflate commodity CFs in a constructive oil price environment with business quality, this opens the door to accretive M&A of actual waste assets and a longer-term pivot. That's the additional optionality in the $SES.TO thesis, but it requires that the oil price remains high enough for long enough. Once again, this highlights $SES.TO's exposure to energy beta.

1

4

28

11,049

Some have asked whether listening to the $GFL & $SES.TO M&A call changed my view on the txn.

In short, not really. Here are two additional takeaways for everyone's benefit 1 positive and 1 negative.

( ) Mgmt seemed to confirm that they will use the additional funding capacity (FCF & debt capacity) to fund more traditional waste M&A which I think is a positive

(-) The $SES.TO CEO flagged that ~20% (of rev?) was tied to 10-year contracts with CPI escalators, suggesting the rest of the revenue base is more merchant/cyclical in nature. The txn is being done leverage neutral, let's call it 3.5x. Given the cyclicality, I don't think its prudent to lever the $SES.TO CFs at the same level as legacy $GFL. $SES.TO makes up just ~1/5th of the PF EBITDA so maybe it doesn't matter but, this just speaks to how much financial engineering is contributing to the optics of the txn.

Another thing worth highlighting is that $SES.TO's midstream business seems to not fit with the "waste" narrative and ppl have asked what can be done with it. I would caution against using large cap midstream multiples to value the $SES.TO assets. There is a material difference in asset quality between gathering pipelines and long-haul egress pipelines/integrated systems. A good comp would be $GEI.TO's recent Chauvin acquisition at 7.5x EBITDA. Even if we were to be generous and say that the $SES.TO assets are worth 1x more (~15%) a sale of the assets would be dilutive versus the purchase multiple of 11x driving up the price paid for the waste assets. Said another way, I don't view monetization of the midstream assets as a value creation lever in this txn.

2

20

3,609

$SES.TO is my top PA position. Happy to see the takeout news from $GFL. But, just to play devil's advocate, I think the acquisition is being done for near-term financial accretion and is materially dilutive to the GFL base business' cash flow quality with little synergy outside corporate G&A.

GFL's base business locks in revenue through 3-10 year municipal contracts and 3-7 year commercial deals, with CPI escalators, fuel surcharges etc. A truly acyclical business. Secure's legacy waste processing book (incl. Tervita and NewAlta assets), which makes up the bulk of its volumes, is transactional and spot-priced: no contract duration, no CPI escalation, no volume commitments. Pricing flexes with oil market conditions. Secure has layered on some higher-quality take-or-pay deals on newer projects (12-year Montney, 10-year Clearwater), but these sit on top of the uncontracted core. Bolting Secure onto GFL dilutes the weighted-average contract quality of the combined business, effectively swapping toll-booth economics for commodity-linked spot revenue.

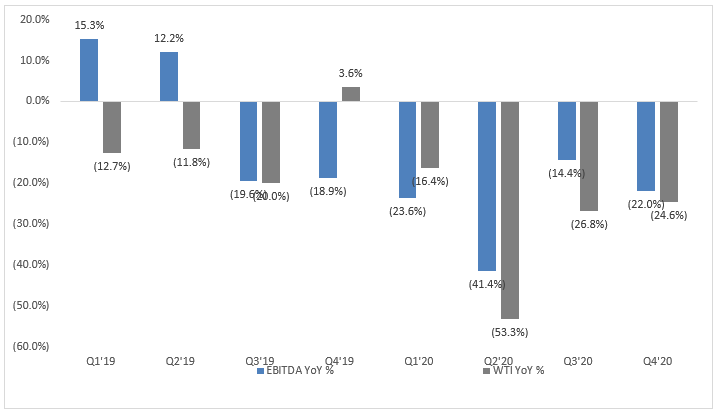

The 2019-2020 drawdown in oil prices shows the cyclicality of the legacy Secure business. 1H19 EBITDA growth was masked by IFRS 16 adoption and the placement into service of the Kerrobert pipeline. Outside of those inorganic contributions, EBITDA captured material beta to the oil price, with management calling out "challenging industry fundamentals stemming from volatile crude oil pricing" in Q4'19.

On pricing power, Secure's largest (highest-quality) customers (ie: $CNQ) have a significant ability to insource disposal wells, landfills, etc., handicapping Secure's ability to aggressively take price and likely keeping a lid on the ROIC/ROIIC of the business. This is net dilutive to the existing GFL franchise, which for the most part has significantly higher pricing power (reflected by contract structure).

GFL is buying at 11x EBITDA. Let's be generous and call it 11x FCF (G&A synergies offset maintenance capex). That's a sub-10% cash yield. If they were buying sub-8x and using the FCF to fund traditional waste growth, I would be much more excited about the prospects. But at 11x, with the quality dilution, I come out much more cautious.

That's not to say this can't be well received by the market. A good analogue would be the two recent major acquisitions by $GEI.TO in the USGC and Alberta. Both were materially dilutive to overall contract quality, but the market came out more focused on the increased scale of the business and the growth pipeline brought on by the acquisitions.

6

4

50

8,436

I realize that this post is bearish in the context of $SES.to being my largest position. My first and only buy of the stock was in early March, 2023 when the competition tribunal ruled against the Tervita merger. My thinking at the time was that $SES.to would challenge the ruling and even if forced to sell at a punitive multiple, they would harvest FCF from the assets in the intervening period such that the stock should be down $0.50/sh max. IIRC the stock was down something to the tune of $1.50/sh. I'd known the mgmt team for years at that point and knew it as one of the higher quality oil/oil-related businesses I had encountered and was bullish on the Tervita merger overall. So, I bought it pretty aggressively. I've never sold a share because I see additional runway for the stock and use it as oil beta for the overall PA. That being said, I've always been resistant to the narrative that it should trade with a multiple anywhere near the true waste peers given cyclicality. It's an OFS business and should be treated as such until M&A materially changes the business mix.

11

1,201

Commodity Adjusted EBITDA retweeted

Mar 1

Seeing wider confirmation of this now.

Big deal, especially right now with Iran.

Ukraine either just accidentally really overplayed its hand, or is very intentionally playing serious hardball at a perilous moment for the global oil market.

Mar 1

Ukrainian projectiles successfully struck port infrastructure in Novorossiysk, Russia. Likely the terminal for oil loading has been struck.

129

256

1,539

214,359

Have really enjoyed the the engagement on X recently, h/t @compoundpapi. I’m a former Canadian sell-side analyst energy analyst that has spent the last few years in private energy/infrastructure investing. I want to stay sharp in public markets and contribute to the community. Thinking of doing some more long form content. What should I write about first?

Poll is glitchy please comment or DM suggestions. Was thinking:

1. Current sector outlook

2. Single Name Deep Dive

3. Investment Philosophy

4. Active Management vs. Private Assets

1

1

5

1,228

Option?

100%

1

0%

2

0%

3

0%

4

2 votes • Final results

1

517

Commodity Adjusted EBITDA retweeted

12 Nov 2025

Haven’t followed closely for years. Pitched $CMG.TO as a short many years ago to land my first job. The concept that this was gonna be O&G CSU was beyond laughable to me. That said, it is a cyclical business, growth will be lumpy and swinging the target multiple around when you hit trough earnings doesn’t really make sense. I Always run mid-cycle pricing on normalized earnings for cyclicals. Whether 18x is the correct figure I have no idea because I have no context on underlying EBITDA forecast.

1

1

6

1,032

1 Oct 2025

Looks like $OXY shareholders are about to get fleeced once again by Buffett. The unrivalled capital allocation ability of Hollub strikes again. Let this be a lesson to all those who blindly follow 13F’s. You and the big dogs are not playing the same game.

3 Sep 2024

2

2

946

1 Oct 2025

1

373

17 Jun 2025

Sec. 70524 from the Finance Committee Reconciliation Text appears to expand MLPs eligible income to include hydrogen storage, CCS, nuclear, hydro power, and geothermal IYKYK 🤮🤮🤮

2

379