An independent trust dedicated to the achievement of a financial system that delivers value for a green and inclusive digital economy

Joined November 2011

- Tweets 11,986

- Following 600

- Followers 7,875

- Likes 4,583

6,034 Photos and videos

This case study analyses Unity Homes’ innovative mortgage structure, its impact on Unity Home’s target market and applicability to the wider Kenya’s housing market.

Traditionally reliant on cash buyers due to the high cost of construction finance, Unity Homes used to typically sell to investor buyers who had ready cash available to finance the construction of the units, and excluded a large segment of potential buyers who required mortgage financing.

To address this, Unity Homes piloted a performance guarantee-backed mortgage model, supported by FSD Kenya.

This model allowed banks to release the mortgage value during construction, de-risking the financing process and enabling developers to accept mortgages without waiting for legal registration.

📈The results have been transformative:

🔹 Mortgage sales went up from under 2% of total sales to 30% of revenue in 2025

🔹 $7.1 million in approved mortgages, with 170 applicants in the pipeline

🔹 Women now account for 65% of uptake

The pilot was tested with average unit prices of KShs 7 million, and average loan to value at 85%. Given the proof of concept, the same mechanism can now be replicated to lower cost units, as long as the developer balance sheet and track record are there.

📖 Read the full case study: fsdkenya.org/blogs-publicati…

1

106

Kenya’s persistent shortfalls in every day food items such as eggs, milk, fish and honey present immediate, commercially viable entry points for rural youth, but unlocking these opportunities requires a shift in how finance is designed for agri-food systems as well as investment in capacity development of youth led agri-enterprises.

This is according to the recently published Food Systems Analysis commissioned by FSD Kenya through the Green Finance for Youth Employment (GFYE) project, examining five priority value chains across 14 counties. The value chains analysed in the study were dairy, horticulture, poultry, fisheries and aquaculture, and apiculture.

The analysis reveals persistent supply gaps across all these five value chains, documenting Kenya’s annual deficit of 5 billion eggs; 6.5 to 7.5 billion litres of milk; 340,000 metric tonnes of fish; and 5,500 metric tonnes of honey. These shortfalls are largely met through imports, signalling immediate market opportunities for domestic production by youth-led enterprises.

Read the full report for more about the study, the findings, and the recommendations here: fsdkenya.org/wp-content/uplo…

1

50

FSD Kenya, the International Fund for Agricultural Development (IFAD), and the National Treasury and Economic Planning last week shared the findings of the Green Finance for Youth Employment Food Systems Analysis report.

The Food Systems Analysis was commissioned by FSD Kenya through the Green Finance for Youth Employment (GFYE) project, to study five priority value chains (dairy, horticulture, poultry, fisheries and aquaculture, and apiculture) across 14 counties.

The analysis revealed persistent supply gaps across all these five value chains, documenting Kenya’s annual deficit of 5 billion eggs; 6.5 to 7.5 billion litres of milk; 340,000 metric tonnes of fish; and 5,500 metric tonnes of honey. These shortfalls are largely met through imports, signalling immediate market opportunities for domestic production by youth-led and youth employing enterprises.

However, unlocking these opportunities for youth-led and youth employing enterprises, requires a shift in how finance is designed for agri-food systems as well as investment in capacity development of youth-led and youth employing agri-enterprises.

For the full report, its findings and recommendations click here: fsdkenya.org/wp-content/uplo…

The Green Finance for Youth Employment (GFYE) project is funded by the Ministry for Foreign Affairs of Finland through International Fund for Agricultural Development (IFAD) and implemented by FSD Kenya in partnership with AGRA and Cordaid Kenya. GFYE is embedded within the IFAD-funded Rural Kenya Financial Inclusion Facility (RK-FINFA), overseen by the National Treasury and Economic Planning and it aims to support at least 8,000 rural youth and 500 youth-led or youth-employing enterprises by expanding access to green finance and strengthening enterprise capacity.

65

How do Kenyans actually navigate the financial realities of seeking healthcare?

@felistusmbole and @natellous share early insights from the FSD Kenya, Ekko Insights and Georgetown University healthcare financial diaries study, revealing three important shifts shaping health-seeking and financing behaviour.

First, there has been a move towards digital payments, driven in part by the 2016 waiver on transaction fees for amounts below KShs 100. This has made it easier for households to manage small, frequent health related expenses.

Second, persistent medication stock-outs in public facilities mean communities rely heavily on private pharmacies. While this fills a critical gap, it also introduces new risks including inconsistent quality of care and increased use of alternative medicines.

Third, proximity does not always equal access, with many patients, especially those with chronic conditions, still needing to travel to higher level facilities for treatment. The cost and time involved remain a significant barrier.

Read more: fsdkenya.org/blogs-publicati…

This blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report (pdf) here: fsdkenya.org/wp-content/uplo…

1

94

The Nanyuki Bulk Water Project is a case study of how innovative finance can unlock climate resilience, economic growth, and improved livelihoods.

As a flagship initiative under the county green preparation facility, the project demonstrates how well-structured, bankable infrastructure can attract green capital while addressing critical service gaps.

By strengthening water access in a fast-growing urban area, it is not only improving public health and supporting businesses, but also laying the foundation for sustainable, inclusive growth.

Beyond infrastructure, the project signals a shift in how counties can mobilise investment through combining technical preparation, climate alignment, and market-ready design to crowd in private capital.

This approach helps turn local development priorities into viable opportunities for green financing. As a result, jobs are created, resilience strengthened, and a pathway opened for counties to actively participate in Kenya’s growing green capital markets.

Read more: fsdkenya.org/blogs-publicati…

This blog by Mugwe Manga and Sarah Makena is one of the articles in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report (pdf) here: fsdkenya.org/wp-content/uplo…

81

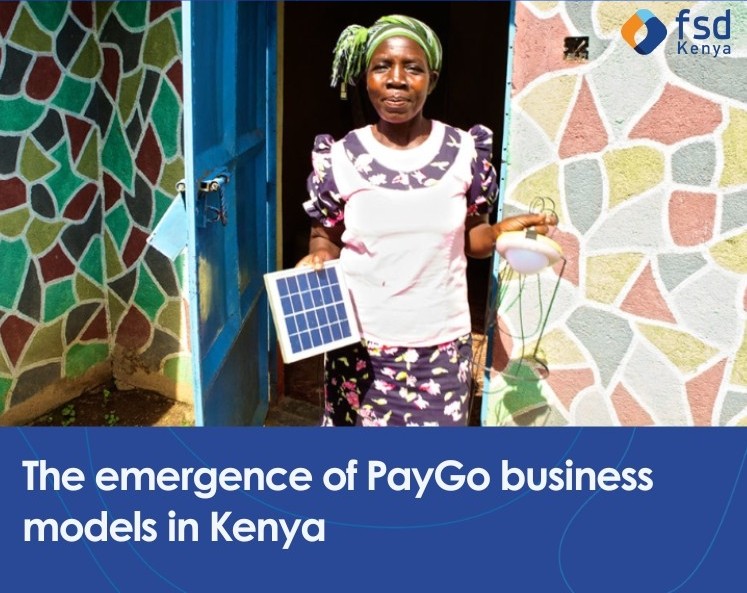

Kenya’s PayGo story is a demonstration of one pathway for inclusive market systems to scale.

From the early 2010s, PayGo models unlocked access to solar home systems for low-income households in Kenya by pairing small, flexible payments with mobile money.

What started as a solution for energy poverty quickly evolved, and today, the same model finances smartphones, household appliances, and productive assets, expanding both opportunity and resilience.

The journey of PayGo in Kenya was not linear.

Early growth was fuelled by impact capital and rapid customer acquisition, often at the expense of short-term profitability, but with time, the sector matured, diversified, and, like much of the economy, faced stress during Covid-19.

Today, Kenya remains an interesting PayGo market, serving over 1.5 million customers, with providers improving unit economics, refining risk management, and moving steadily towards sustainability.

This evolution offers important lessons on what it takes to build markets that truly work for low-income consumers.

📘 Explore the case study of the emergence of PayGo business models in Kenya in FSD Kenya’s 20-year review here:

fsdkenya.org/wp-content/uplo…

1

86

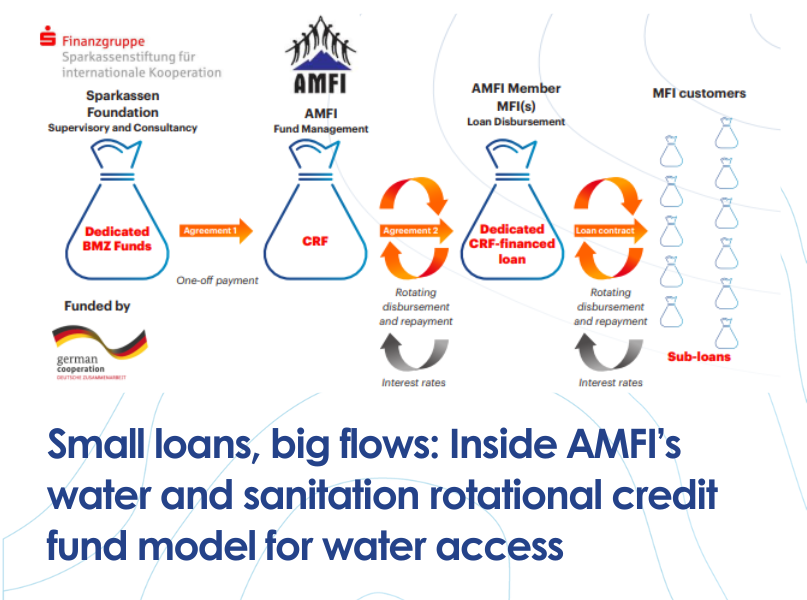

Small, well-structured finance can unlock large-scale change, particularly in essential services such as water and sanitation.

@seeta_v_shah writes about FSD Kenya's support to

@AMFIKENYA's rotational credit fund model, which demonstrates how small loans, when organised through community-based systems, can improve access to water infrastructure.

Through pooling of resources and rotating credit among members, the model enables households and local providers to invest in water connections, storage and sanitation solutions without requiring large upfront capital.

The approach is notable for combining financial inclusion with practical service delivery.

It builds on existing social structures, reduces risk through collective participation and improves repayment performance, while simultaneously creating a pathway for underserved communities to gradually upgrade their water access in a sustainable manner.

Evidence from the model suggests that demand for water financing remains strong where products are tailored to income patterns and local realities, and that scalable solutions will depend on strengthening partnerships between financial institutions, community groups and service providers.

The experience offers useful lessons for expanding access to basic services while deepening financial inclusion.

Read the full blog here: fsdkenya.org/blogs-publicati…

This blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report (pdf) here: lnkd.in/d5KWVWPd

1

115

By 2024, 1.76 million Kenyans were receiving a monthly stipend of KShs 2,000 through a government payment platform built over two decades.

Its origins trace back to the Hunger Safety Net Programme, where FSD Kenya took on an unusual role for a market facilitator, the role of managing payments to households in arid and semi arid lands of northern Kenya.

The intention of the payment platform went beyond delivering money to vulnerable households, and by managing payments in some of Kenya’s most infrastructure-poor regions, the programme was designed to help build the underlying financial rails needed to serve people sustainably.

Simply put, the programme was designed to digitise government payments in ways that work for low-income households while also supporting financial market development.

FSD Kenya worked with the National Treasury, Central Bank of Kenya, the National Drought Management Authority, the Kenya Bankers Association, VISA, Mastercard, and donors to design a shared platform for social protection payments.

The design introduced a choice-based model where beneficiaries had the selection of four contracted payment service providers at account opening, with periodic windows to switch. The intent of this approach was to place agency in the hands of recipients and competitive pressure on providers.

When Covid-19 hit, the platform helped the government reach vulnerable households at speed.

This case study is one of several in our twenty year review of market systems work in Kenya's financial sector.

Read the full report here: fsdkenya.org/wp-content/uplo…

1

114

Kenya’s intermediary cities are on the frontline of rapid urbanisation, climate risk and rising demand for inclusive economic opportunity.

Turning urban plans into tangible investments, jobs and viable local economies requires more than good intentions. It demands coordination, evidence and capital that is fit for purpose.

@dunoyaro and @felistusmbole share insights from the Sustainable Urban Economic Development Programme (SUED), which shows what it takes to move from urban economic diagnostics to bankable investments that deliver results on the ground.

The blog outlines how structured urban economic planning, rigorous feasibility analysis and targeted seed funding can help de‑risk investments and crowd in private and public finance.

To date, the Sustainable Urban Economic Development Programme (SUED) has mobilised significant investment across multiple municipalities, supporting thousands of jobs and demonstrating what is possible when planning, finance and implementation are deliberately linked.

The blog also reflects on what it takes to sustain momentum: sequencing reforms, navigating land and infrastructure constraints, building local capacity, and maintaining investor confidence.

Looking ahead, opportunities in climate-smart agro‑processing, green infrastructure and circular economy solutions point to where the next wave of urban jobs could come from.

👉 Read the full blog:

fsdkenya.org/blogs-publicati…

This blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report here: lnkd.in/d5KWVWPd

#GoFarGoTogether

67

Kenya’s inclusive finance journey has been shaped by strong demand‑side insights.

To unlock the next phase of impact, the supply‑side, i.e., how financial service providers collect, share, and use data to serve different customer segments better, must be strengthened.

FSD Kenya’s Market Information Lead, @Kwatindi explores how building a robust supply‑side data market infrastructure can catalyse data‑driven innovation through @WEFIKenya.

The Code offers a practical framework for standardising and using provider‑level data, with a clear focus on improving financial access for women‑led micro and small enterprises (WMSMEs).

Embedded within Kenya’s National Financial Inclusion Strategy (NFIS) 2025 –2028, the WE Finance Code aligns leadership, data, and accountability across the ecosystem.

With the @CBKKenya as the National Champion, and delivery anchored through a collaborative, multi‑stakeholder model, the Code is moving from intent to implementation.

Read the full blog here: fsdkenya.org/blogs-publicati…

@Kwatindi's blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report here: lnkd.in/d5KWVWPd

59

The April 2026 edition of the FSD Kenya newsletter is out!

The newsletter shares a round-up of event updates, blogs and publications from FSD Kenya, including insights from a 20‑year review of FSD Kenya’s impact since 2005, demonstrating how Kenya’s financial sector has evolved, and the role FSD Kenya has played in driving that transformation.

It also spotlights FSD Kenya's 2025 annual report, events and webinars as well as blogs and publications published since the beginning of the year.

👉 Read the newsletter here:

mailchi.mp/fsdkenya/financia…

📩 Not yet on our mailing list?

Subscribe to receive insights, research and updates from FSD Kenya straight to your inbox:

fsdkenya.us5.list-manage.com…

2

69

FSD Kenya retweeted

Members of the public are invited to submit comments on the draft Financial Consumer Protection Framework no later than 𝐓𝐮𝐞𝐬𝐝𝐚𝐲, 𝐀𝐩𝐫𝐢𝐥 𝟐𝟖, 𝟐𝟎𝟐𝟔

The draft Framework and the feedback template are available on the CAK’s Website - lnkd.in/djS_fxb7

1

12

14

1,787

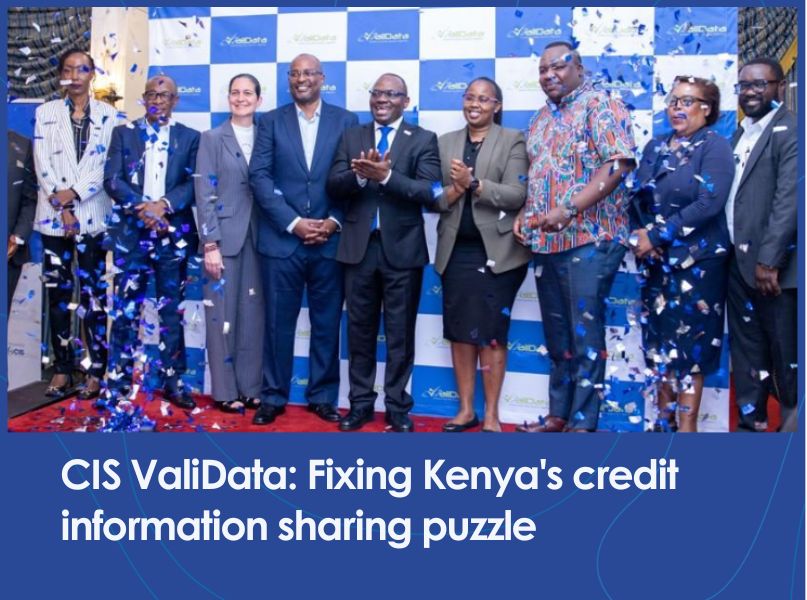

Access to affordable and appropriate credit remains elusive for many Kenyans, especially women and micro & small enterprises.

While many Kenyan enterprises, individuals and households have access to credit, many still rely on informal, high-cost lenders, mostly as a result of weak and fragmented credit information systems that fail to capture the borrower's full borrowing story.

FSD Kenya's head of policy and infrastructure Francis Gwer unpacks how CIS ValiData offers a practical, system-level solution, enabling lenders to validate and submit standardised credit data to all licensed credit reference bureaus simultaneously. He also explains how improving data quality at the source, through CIS ValiData, strengthens market transparency, supports fairer risk-based pricing, and creates pathways for more inclusive access to credit.

➡️ Read the full blog here: fsdkenya.org/blogs-publicati…

This blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report here: lnkd.in/d5KWVWPd

1

2

117

In 2005, only about three in ten Kenyan adults (27%) had access to formal financial services. Twenty years later, that figure stands at eight in ten (84.7%).

One of the most significant game changers in this increase of access to formal financial services in Kenya was the uptake of mobile money.

FSD Kenya’s role in the creation of M-Pesa was subtle and largely out of the public eye, but nonetheless significant.

FSD Kenya did not provide the funding for the original experimentation which led to the creation of M-Pesa by Safaricom, supported by Vodafone.

However, seeing the potential early on, FSD Kenya funded a consultancy which assisted the early development; and more importantly, played an important role in advocating for the ‘no objection’ letter from the Central Bank of Kenya (CBK), which allowed M-Pesa to launch in 2007, in advance of enabling regulations which followed six years later.

FSD Kenya: Twenty years of a market systems approach in the Kenyan financial system, documents FSD Kenya's contribution to the development of Kenya's financial sector.

📄 Read the full report here: lnkd.in/drC4AhK4

1

149

Shared services could reshape the future of SACCOs in Kenya.

SACCOs remain a cornerstone of Kenya’s financial system, mobilising savings, expanding access to credit, and supporting household and enterprise resilience.

In 2024 alone, the sector crossed the KShs. 1 trillion asset mark, underlining its growing importance to the economy. Yet this growth is unfolding against a backdrop of rising technology costs, fragmented systems, tightened regulatory requirements, and limited access to national payments infrastructure.

In this piece from FSD Kenya's 2025 annual report, FSD Kenya's infrastructure lead Juliet Mburu explores how shared services offer a practical pathway to address these constraints, enabling SACCOs to pool resources, strengthen operational efficiency, and compete more effectively in an increasingly digital and interconnected financial sector.

📖 Read the full blog here:

fsdkenya.org/blogs-publicati…

This blog is one of the entries in FSD Kenya’s 2025 annual report. Read the full FSD Kenya 2025 annual report here fsdkenya.org/wp-content/uplo…

132

When FSD Kenya was established in 2005 as a specialised market systems facilitator, only about three in ten Kenyan adults (27%) had access to formal financial services. Twenty years later, that figure stands at eight in ten (84.7%).

FSD Kenya has worked with the public sector, the financial services industry, and other partners in Kenya and beyond to develop a financial sector that better addresses the real-world challenges that low-income households, micro and small enterprises, and underserved groups such as women and youth deal with on a day to day basis.

📘 FSD Kenya: Twenty years of a market systems approach in the Kenyan financial system, is a new report reflecting on two decades of applying a market systems development approach to the Kenyan financial system.

The report reviews how the financial sector has evolved since 2005, the roles played by public and private sector actors, and the contribution of facilitation over direct delivery. It examines what has changed, what has endured and the trade-offs that have shaped outcomes for households, micro and small enterprises and the wider economy.

It looks at the underlying conditions that enable markets to function, including the quality of data and evidence, the policy and regulatory environment, core infrastructure and the innovation ecosystem. The report assesses how these elements interact, where progress has been uneven and where risks to financial health and resilience remain.

The report also reflects on FSD Kenya’s institutional evolution, lessons from unintended consequences and evidence of harm, and the relevance of market systems thinking in a more digital, more concentrated and more complex financial system. It is intended as a contribution to ongoing debate among policymakers, regulators, funders and practitioners working to build inclusive and sustainable financial markets.

📄 Read the full report here: fsdkenya.org/blogs-publicati…

114

What does contributing to the building of a financial system that delivers value for a green and inclusive digital economy, while strengthening financial health for women and micro & small enterprises (MSEs) in Kenya, look like?

📘 FSD Kenya's 2025 annual report provides a glimpse into that.

The report highlights key work and insights from the year, including:

🔹 Insights from the 2024 FinAccess sub-sector reports

🔹 Fixing Kenya’s credit information sharing puzzle through CIS ValiData

🔹 The rise of shared services for SACCOs across Kenya

🔹 Credit inclusion for small‑scale producers and MSEs using alternative data

🔹 A county green preparation facility flagship driving jobs, growth and green capital markets

🔹 Understanding Kenyans’ needs, health seeking and financing behaviour through the healthcare financial diaries

🔹 Catalysing data‑driven innovation through the WE Finance Code Kenya Chapter

🔹 AMFI’s water and sanitation rotational credit fund model for water access

The report also presents insights from a 20‑year review of FSD Kenya’s impact since 2005, showing how Kenya’s financial sector has evolved and the role FSD Kenya has played in driving that transformation.

📖 Read the full report here:

fsdkenya.org/blogs-publicati…

101