10,840 Photos and videos

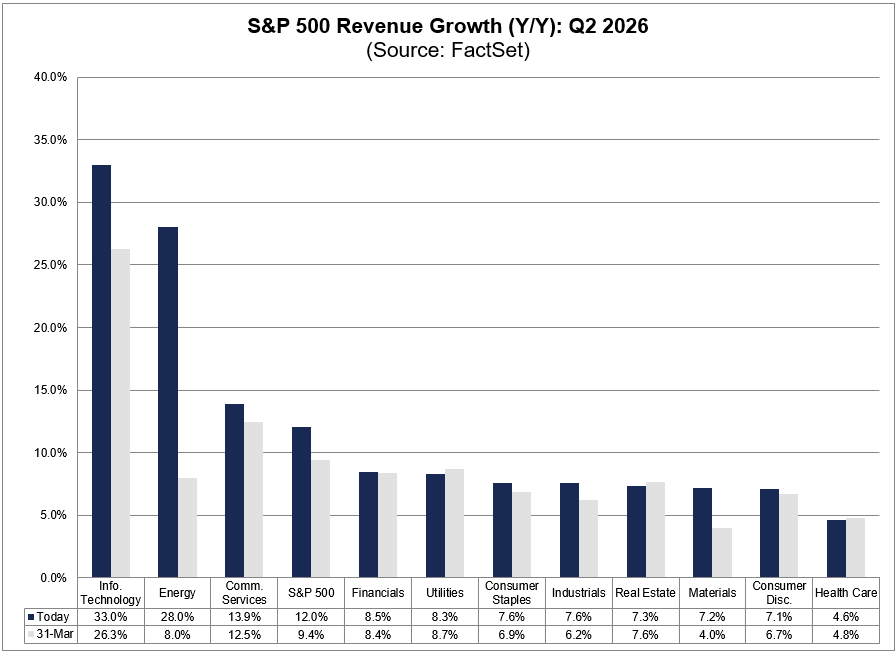

$SPX is expected to report Y/Y revenue growth of 12.0% for Q2 2026, which is above the estimate of 9.4% on March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

2

14

2,572

We offer thematic template stress tests within Portfolio Analysis Risk reports in the @FactSet Workstation. Read our blog article on stress testing investable indices and strategies as a response to a hypothetical AI bubble burst: bit.ly/4e0WdyI

1

2,217

$SPX is expected to report Y/Y earnings growth of 21.9% for Q2 2026, which is above the estimate of 18.7% on March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

1

8

12

2,748

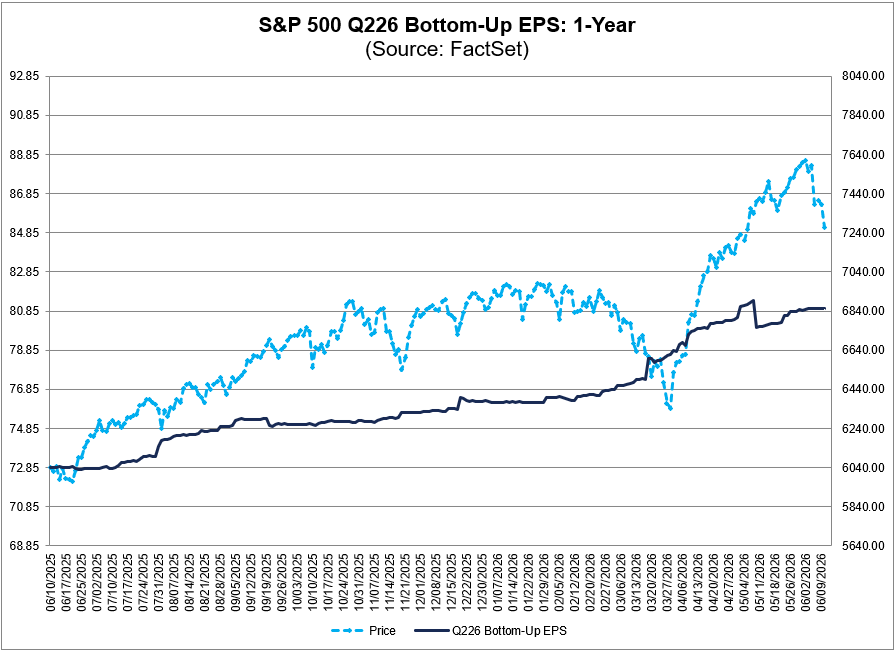

Analysts have increased Q2 EPS estimates for $SPX companies by 2.7% since March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

1

5

19

3,025

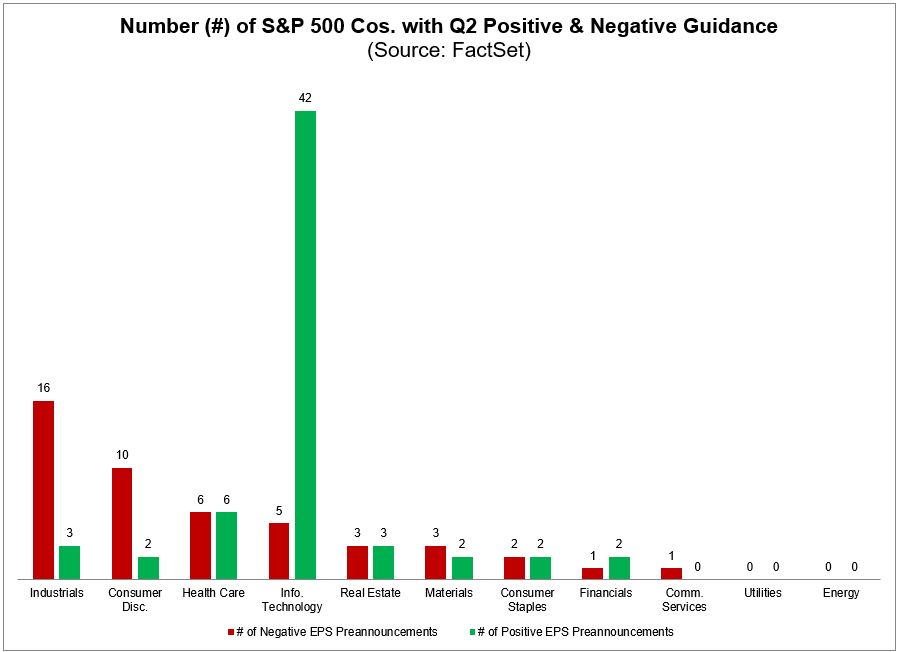

62 $SPX companies have issued positive EPS guidance for Q2 2026, led by the Information Technology sector at 42. #earnings, #earningsinsight, bit.ly/4w62Civ

2

10

2,502

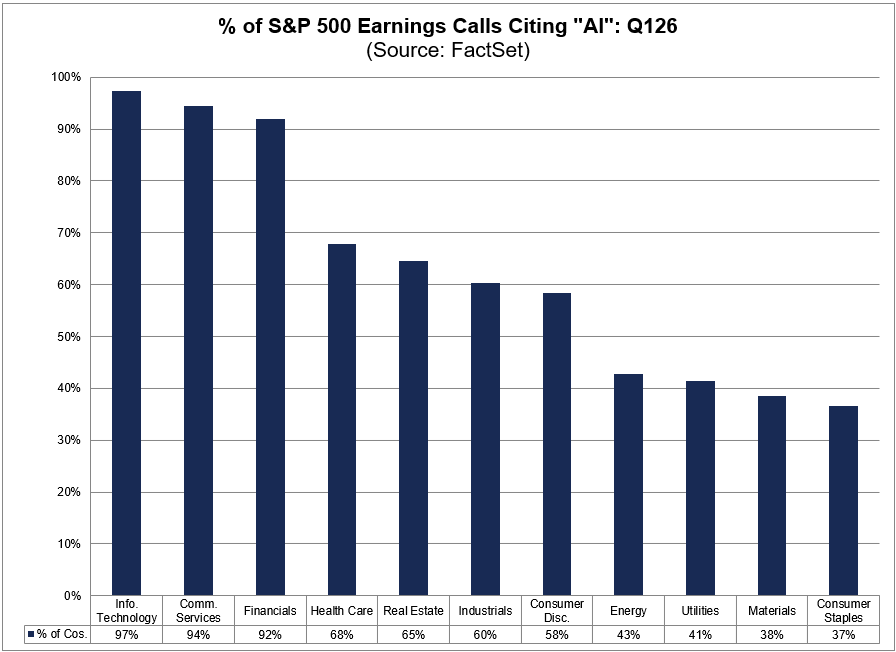

The $SPX Information Technology (97%), Communication Services (94%), and Financials (92%) sectors have the highest percentages of Q1 earnings calls where the term "AI" was cited. #earnings, #earningsinsight, bit.ly/4w62Civ

1

4

13

2,387

Don't let the peak rush hour stop you from staying connected to the U.S. economy and corporations - StreetAccount Evening Market Recap has got you covered. #marketupdate

Listen here: feeds.captivate.fm/factset-s…

3

1,897

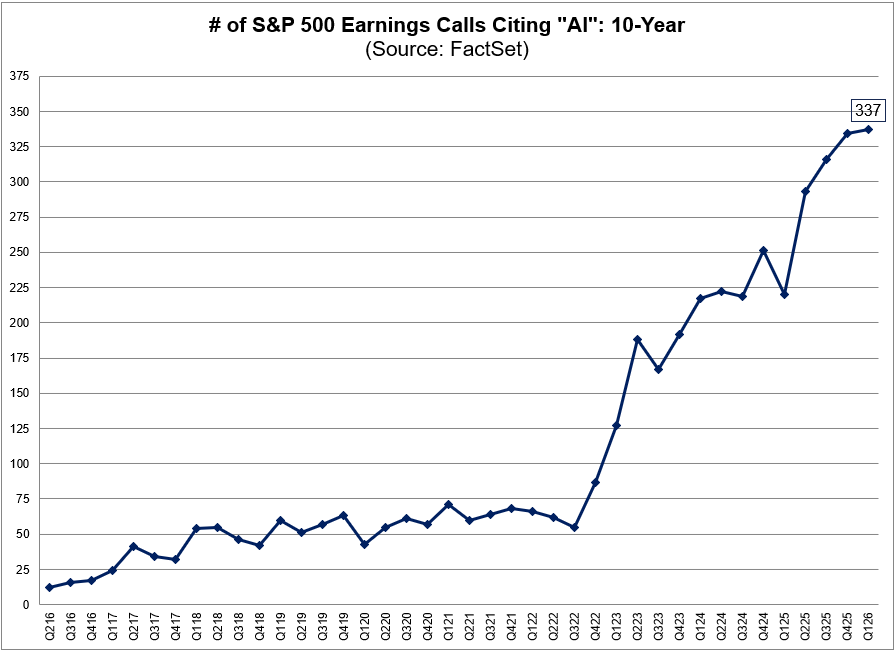

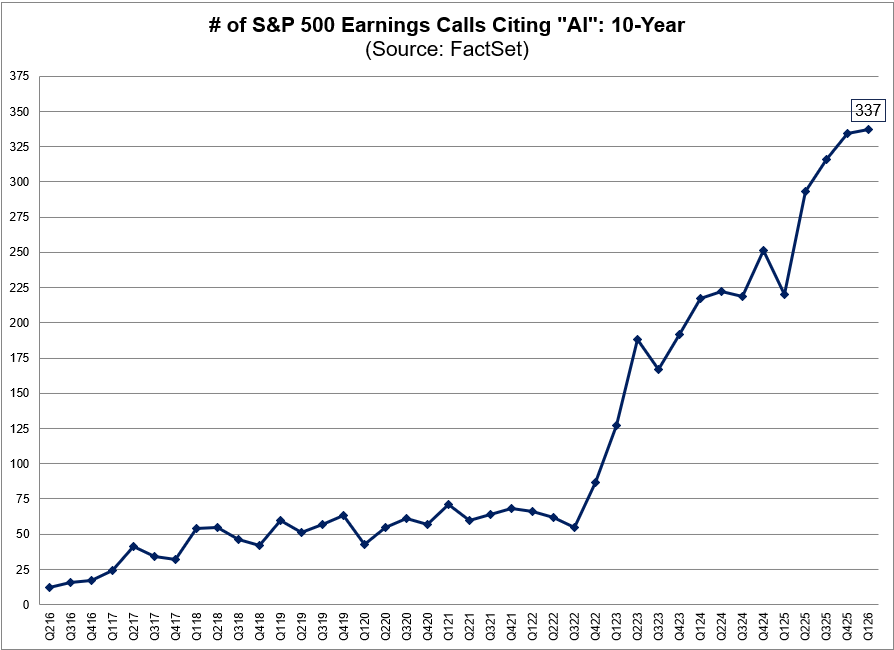

The term "AI" was cited on 337 earnings calls conducted by $SPX companies for Q1 2026, which is the highest number over the past 10 years. #earnings, #earningsinsight, bit.ly/4w62Civ

1

3

11

3,053

Cobalt's Q4 2025 benchmark data is live. For 2010-2015 Global PE vintages, top quartile funds delivered ~30% IRR through years 2-5, while even bottom quartile funds produced ~10% at realization. A strong cohort. Read more: bit.ly/4eBBLVh

3

2,131

The term "AI" was cited on 337 earnings calls conducted by S&P 500 companies for Q1, which is the highest number over the past 10 years.

Read the full article by John Butters: bit.ly/4ghB199

1

2

8

2,373

Busy day ahead? No problem. Get your market updates on the go with #StreetAccount Daily Podcast - the perfect pre-market listen for your commute. #multitasking #financialnews

Listen to the latest episode: feeds.captivate.fm/factset-s…

4

2,018

Financial Market Preview - Friday 12-Jun bit.ly/369hi69

1

1

1,839

Busy day at the office? Don't worry, we've got you covered with the #StreetAccount Evening Market Recap - your daily dose of financial news in under 5 minutes

Listen to the lastest episode: feeds.captivate.fm/factset-s…

2

1,909

Evening Market Recap - Thursday, 11-Jun bit.ly/369hi69

1

3

2,001

StreetAccount Update: $SPCX SpaceX Pre-IPO Perp Activity Ahead of Friday's IPO

Current SPACEX Pre-IPO Tokenized Equity offerings Sentiment Recap:

• Prices reflect on-chain synthetic perpetuals (Hyperliquid & Binance Futures). These contracts are price-based perpetual contracts that track the market-implied expected price of one share of Class A or common stock. Contracts represent localized trading sentiment only and are currently available in specific jurisdictions outside the US, though we expect broader domestic access following the CFTC's recent ruling and US vendors beginning to roll out perps domestically, notably Kalshi, which surpassed $1B in volume within days of launching on 3-Jun

SPCX/USDC Trading Price (per Hyperliquid):

• At Current: $167 | High: $168.66 | Low: $162.99

• $4.26 / 2.60% in past 24 hours

• 24Hr Volume: $81.0M | Open Interest: $158.0M | Funding: 0.0004%

SPCX/USDT Trading Price (per Binance Futures):

• At Current: $166.50 | High: $168 | Low: $158.42

• 1.53 / 0.93% in past 24 hours

• 24Hr Volume: $210M | Funding: 0.00500%

• Per SpaceX's amended S-1 filing (555.6M shares at an expected price of $135.00/sh), current on-chain perpetual contracts are trading at a ~20% premium to the $135 offering price

• StreetAccount notes the final SPCX IPO pricing/allocation is expected to be set today post-close, with trading commencing on the Nasdaq 12-Jun, although SPCX has locked the price at $135 despite underwriters looking to be more flexible on final price based on demand. SpaceX is considering allotting up to 30% of the offering to individual retail investors, above the standard 5-10% of order book historically, while targeting a valuation of ~$1.75-$1.77T. (CNBC)

• Per Bloomberg, Retail order interest attracted over $70B of the $75B (Bberg), with the overall book more than four times oversubscribed (Bberg); separately, a media report indicates that BlackRock has placed at least a $5B order. Banks are expected to stop taking orders from institutional investors after market close today at 16:00ET.

$SPCX #SpaceX #IPO #PreIPO #TokenizedEquity #CryptoFutures #RetailInvesting #Nasdaq #onChain

Gain immediate access to unparalleled insights with #StreetAccount: bit.ly/3xqrpo7

1

7

3,076

Accompanying our blog article on stress testing on investable indices and strategies as a response to a hypothetical AI bubble burst, we offer thematic template stress tests within Portfolio Analysis Risk reports in the @FactSet Workstation: bit.ly/4v2HgSV

1

1,664

The term "Inflation" was cited on 218 S&P 500 earnings calls last quarter, the third straight quarter that number has climbed 📈

That's still well below the 2022 peak, but the direction is one-way for now...

@GuyAdami and @LizThomasStrat discuss the latest Earnings Insight on MRKT Call

3

14

6,362

Street Takeaways - $ORCL Oracle Q4 Earnings ($201.26)

Overview:

• Shares (10.4%) premarket following the stronger EPS and revenue print driven primarily by services outperformance. Op margin 150bps above, RPO sharply ahead, CFO/FCF beat, Capex higher and deferred revenue missed.

• Mgmt. guided Q1 EPS and revenue ahead at the midpoint, while initial FY27 EPS was above and revenue affirmed. Additionally, the Co expects to raise $40B in FY27 through a combination of debt and equity financing including its previously announced $20B at-the-market equity issuance.

• Analysts leaned constructive following the solid overall print, highlighted by surging RPO, driven by accelerating AI and cloud demand. Several encouraged by near term capacity execution, with ~1GW projected to come live in Q1'27, almost matching the whole of FY26. However, FY27 gross margin impact was flagged, as the aggressive expansion plays out, resulting in a underwhelming EPS guide, pressuring the stock. While a further $40B debt/equity raise triggered some pushback, most see this as manageable given the record backlog and strong bookings momentum, with confidence in IaaS growth acceleration and infrastructure GM expansion.

$ORCL #Oracle #Earnings #Cloud #AI #Capex #RPO #Guidance #Tech #Q4Results #EarningsRecap

Gain immediate access to unparalleled insights with #StreetAccount: bit.ly/3xqrpo7

8

2,435

In his analysis, Colin Devereaux at @FactSet discusses the strong results from the 2010-2015 private equity vintages. Key findings from Global PE (Buyout, Growth, VC) funds in this cohort:

• Top quartile funds delivered ~30% IRR through years 2-5

• Bottom quartile funds were still producing as high as 10% returns at realization, a notable floor

• The J-Curve effect is clearly visible in early quarters, with performance normalizing as vintages mature

Read the full benchmark breakdown in the article: bit.ly/4fEm0Oz

3

1,849