Web 3 enthusiast & content creator.

Joined November 2023

- Tweets 10,127

- Following 1,725

- Followers 936

- Likes 5,974

297 Photos and videos

Rafa AI reminds me that not every opportunity deserves attention.

In crypto and tech, there's always something trending, something pumping, and something everyone is talking about.

The challenge isn't finding more opportunities—it's knowing which ones are worth your time.

Having a tool that helps filter the noise can be just as valuable as finding the next big thing.

Sometimes, clarity is the real advantage.

@Metamorfozzz_

@srsh_os

@RAFA_AI

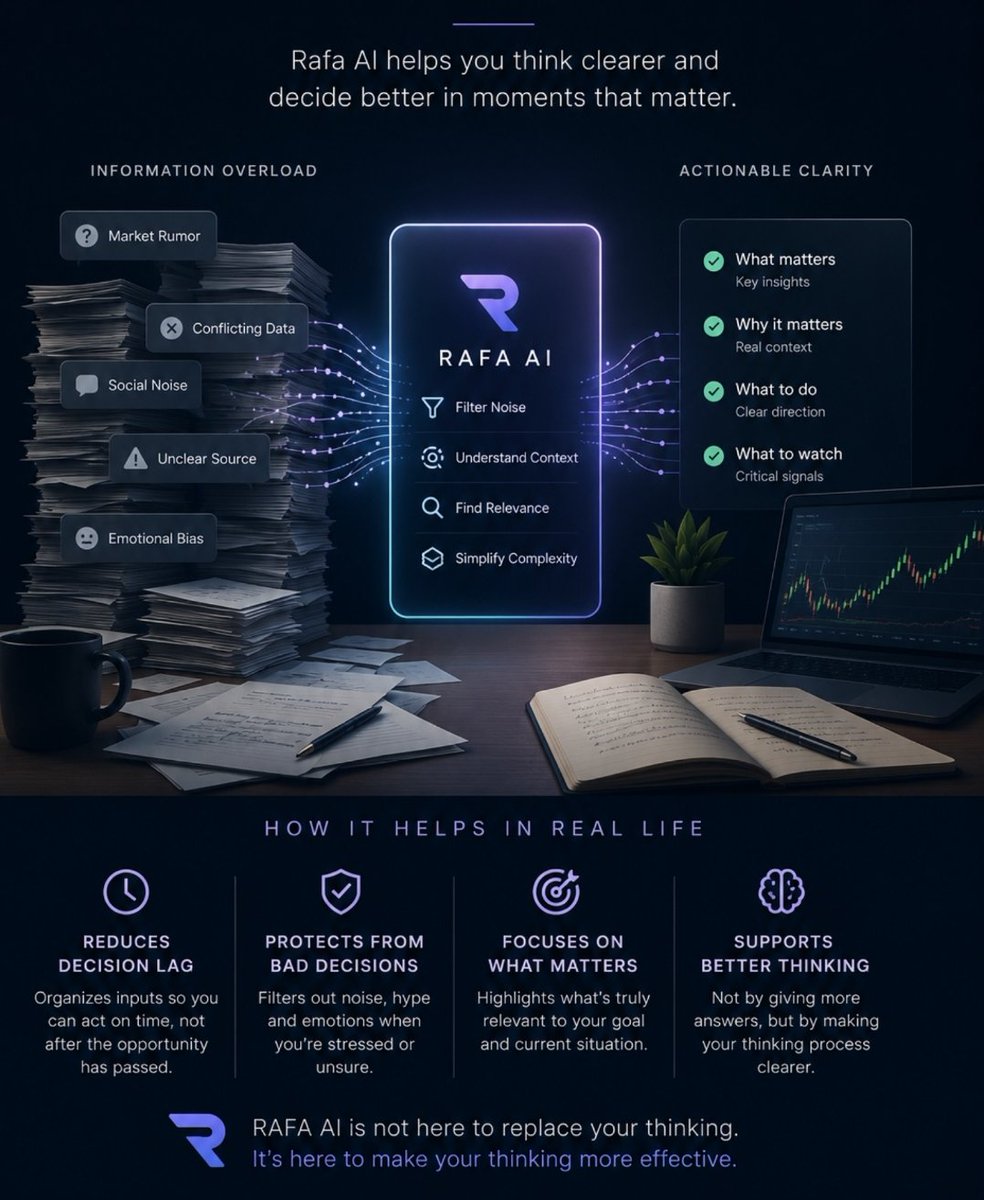

A more practical way to look at Rafa AI is: how do you avoid bad decisions when you’re stressed or unsure?

Most bad decisions don’t come from lack of intelligence-they come from reacting too fast, or thinking too scattered. When you’re under pressure, you either overthink everything or jump too quickly.

can be framed around this moment: it helps structure your thinking so you don’t rely on emotion or noise when making choices.

In real life, that could mean checking a trade setup, filtering a rumor, or even deciding whether to act or wait-without letting confusion take the lead.

@RAFA_AI

@Metamorfozzz_

@srsh_os

35

Famiiisky retweeted

Platinum Prompt for Options Traders 👇

Here's one to copy & paste into RAFA to squeeze out the very best alpha, market insights and trade setups...

"First assess overall market context, including VIX level and trend, broader indices, sector behavior, macro factors, and any upcoming events or catalysts. matrices

Second analyze the underlying price action, key technical levels, momentum, and any relevant fundamentals or news.

Third perform full volatility analysis covering current implied volatility, IV Rank calculated as current IV minus 52-week low divided by 52-week high minus low then multiplied by 100, IV Percentile as the percentage of the past 252 trading days where IV was lower than current, comparison of IV to historical or realized volatility through the volatility risk premium, put-call skew, term structure showing contango or backwardation, and expected move derived from ATM straddle pricing.

Fourth review liquidity metrics, including bid-ask spreads, volume, open interest, and any signs of unusual options activity in the provided data.

Fifth detect and identify trade setups by matching conditions to strategies: when IV Rank or IV Percentile is high above 50 percent especially above 70 to 80 percent combined with neutral or range-bound outlook or expected volatility contraction recommend credit spreads or iron condors for selling premium with defined risk; when IV Rank or IV Percentile is low below 50 percent especially below 30 percent combined with directional bias or expected larger move recommend long calls puts debit spreads or long straddles strangles; for event-driven situations such as earnings use short premium defined-risk structures pre-event to benefit from potential IV crush or long volatility structures if the anticipated move exceeds what is priced in; exploit skew or term structure dislocations with risk reversals calendars or vertical spreads; rank any detected setups by edge using probability of profit risk-reward ratio and alignment of vega exposure with the volatility outlook.

Sixth conduct quantitative evaluation of any proposed or detected trade by calculating or estimating maximum profit maximum loss upper and lower breakeven points approximate probability of profit and expected value, net position Greeks including delta gamma theta vega and relevant higher-order Greeks such as vanna for delta sensitivity to volatility changes vomma for vega sensitivity to volatility changes and charm for delta change over time, then generate P/L scenarios at multiple underlying price levels of plus or minus 5 10 and 20 percent and at IV levels of plus 10 points minus 10 points and unchanged both at expiration and at intermediate dates.

Seventh detail risk management including recommended position size based on maximum risk and any account parameters provided, assessment of defined versus undefined risk, specific exit rules such as profit targets of 30 to 50 percent of maximum profit for credit trades or stop-loss criteria based on price delta or time, hedging approaches, and overall portfolio Greeks impact.

Eighth run full scenario and stress testing for bull base and bear cases, plus stress tests for volatility spikes, gap moves, IV crush or expansion, and assignment risk, including worst-case outcomes.

Ninth, compare alternatives by outlining other viable strategies with their specific advantages and disadvantages.

Tenth flag any red flags such as poor liquidity, wide spreads, undefined risk in high volatility without hedges, ignoring events, poor sizing, or excessive gamma or vega exposure, and recommend a monitoring plan or conclude no trade meets criteria.

Structure every response with clear sequential headings that match the ten steps above. Use matrices for Greeks summaries, P/L scenarios, and strategy comparisons. Quantify all outputs wherever possible, such as specific breakeven prices or approximate probability of profit derived from delta or model approximations."

148

116

176

1,387

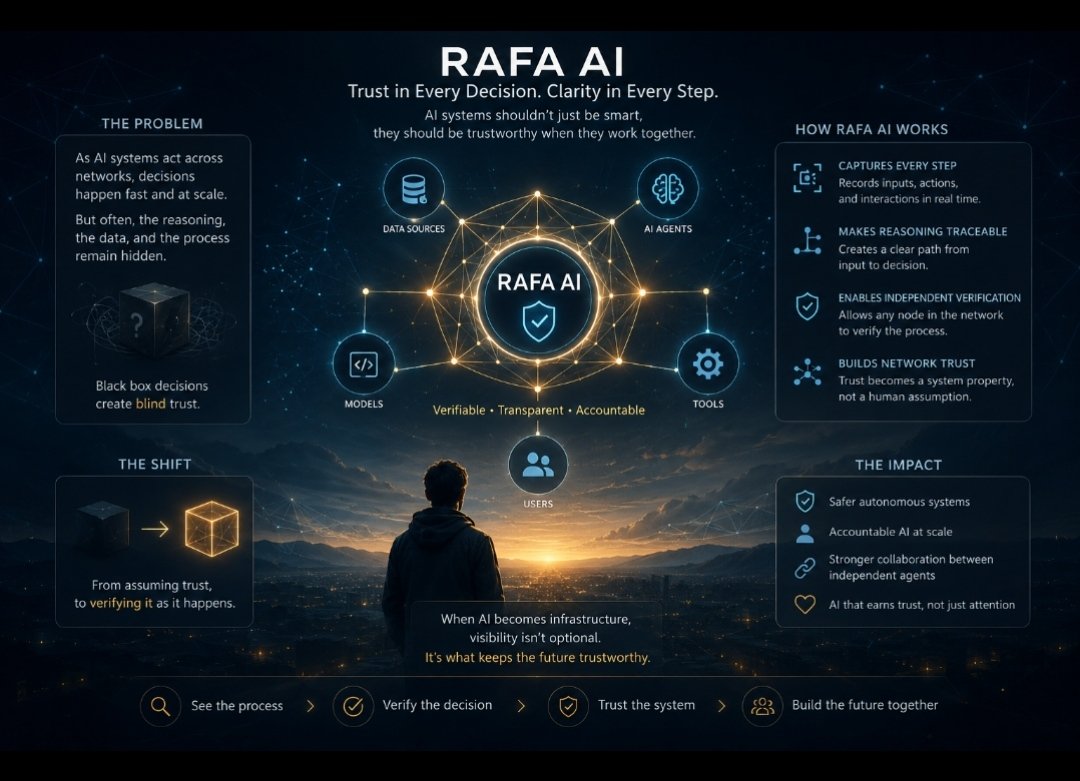

The first wave of AI was about capability.

“What can these models do?”

The next wave is about trust.

“Can these systems operate on sensitive data, inside real workflows, without creating unnecessary exposure?”

That is the problem Nesa is built to solve.

185

50

223

3,275

Famiiisky retweeted

16h

GM CT ☕️

Got your Golden Prompts ready for our AI Agents?

179

126

211

2,119

Famiiisky retweeted

12h

20x GTD for @TheChillBugs

▪️ Follow Like RT

▪️ Comment EVM wallet

Winners in 24hrs ⏱️

149

136

185

2,807

Famiiisky retweeted

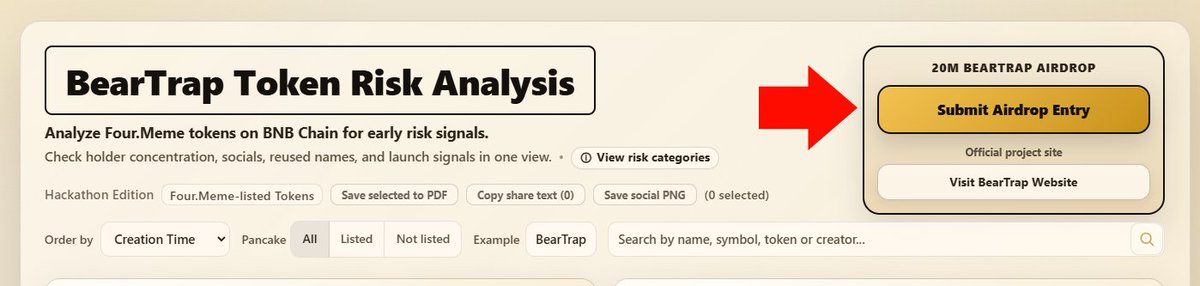

Jun 14

1/6

How to join:

Follow @BearTrap_Coin

Repost the first post in this thread

Comment under the first post

Join BearTrap Telegram:

t.me/BearTrapCommunity

Submit your entry through the BearTrap app:

hackathon.beartrapcoin.xyz/

117

182

218

2,512

💌 2 GTD , 7 FCFS spots

Tasks:

▫️Follow @Pagi_pe, @HexlingsNFT

▫️ Like & Rt

▫️Comment EVM Addy

⏰ 24 h

10000 || TBA || Eth

19

16

18

156

Famiiisky retweeted

Jun 15

10x GTD for @PixonaOrg

▪️ Follow @KingsEcheeh @PixonaOrg

▪️ Like RT

▪️ Drop EVM wallet

~ Winners in 24hrs ⏱️

266

233

310

5,463

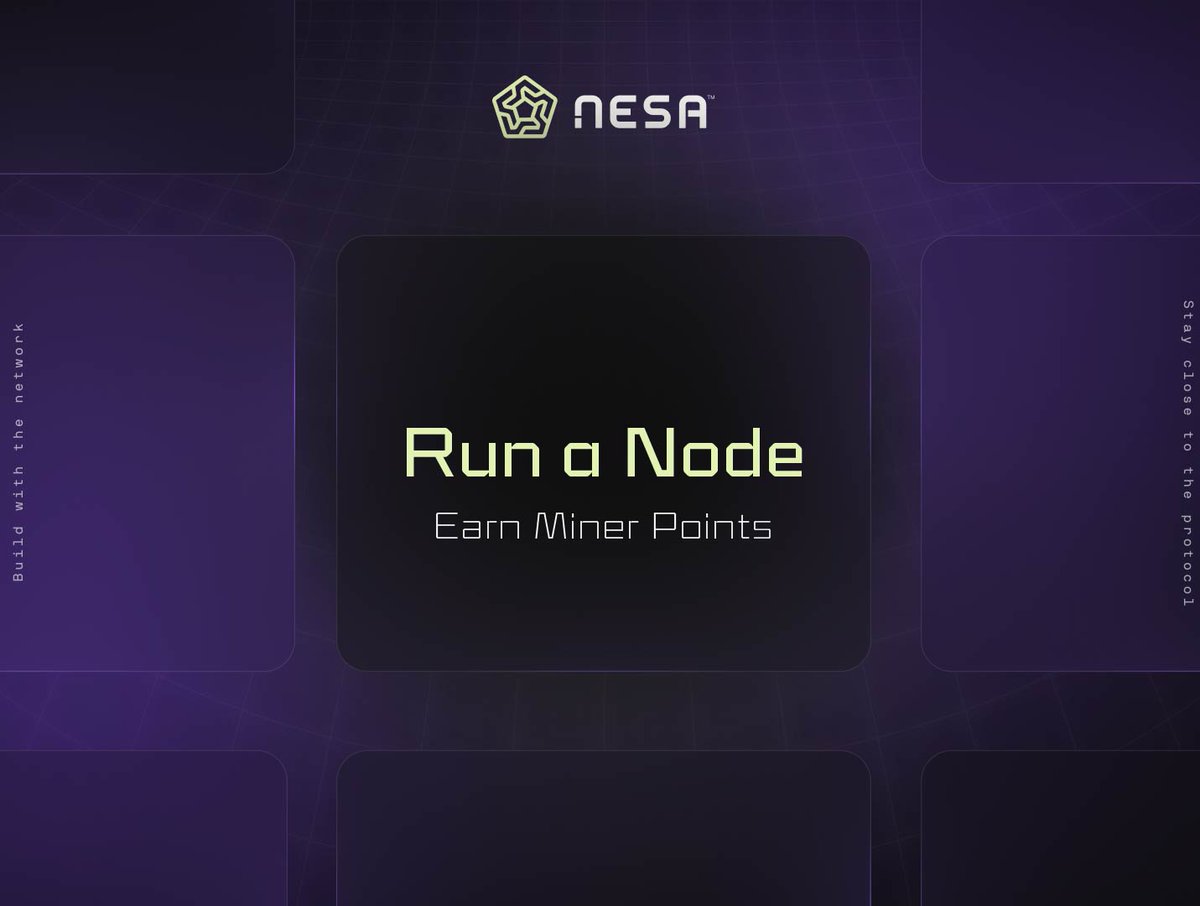

Nesa XP rewards activity.

Miner Points reward infrastructure contribution.

Join a network of over 170,000 operators by running a Node to support the network and earn Miner Points.

Get started today ↓

📚 Docs: github.com/nesaorg/bootstrap…

❓ FAQ: github.com/nesaorg/bootstrap…

🧰 Custom scripting: npmjs.com/package/@nesaorg/a…

💬 Need help? Join Discord: discord.gg/nesa

248

77

358

18,319

Famiiisky retweeted

Jun 14

AI can keep you entertained, or make you smarter, but RAFA can assist you in navigating a volatile market with Trade Ideas and Setups in:

- #optionstrading

- crypto

- stocks (and xStocks)

Try prompting our dedicated AI agents for unique market insights. Free to download today. Link in bio✊

180

128

246

3,803

Famiiisky retweeted

We are thrilled to announce our collaboration with @888s_Society for some Spots 🎉

Mint details:

SUPPLY ~ 10,000

PRICE ~ FREE Mint

DATE ~ TBA

📍Requirements

✅ Follow @888s_Society & @888_Societyclub

✅ Like Repost

✅ Drop EVM Address

Winners in 48hours🫡

122

85

101

763

Famiiisky retweeted

Jun 14

888_Society FREE Mint Spot Giveaway

1️⃣ Follow: @888s_Society ; @888_Societyclub; @the_peters & @bottleboy0xx

2️⃣ Like RT

3️⃣ Submit ETH address

⌚24hrs

163

93

135

2,672

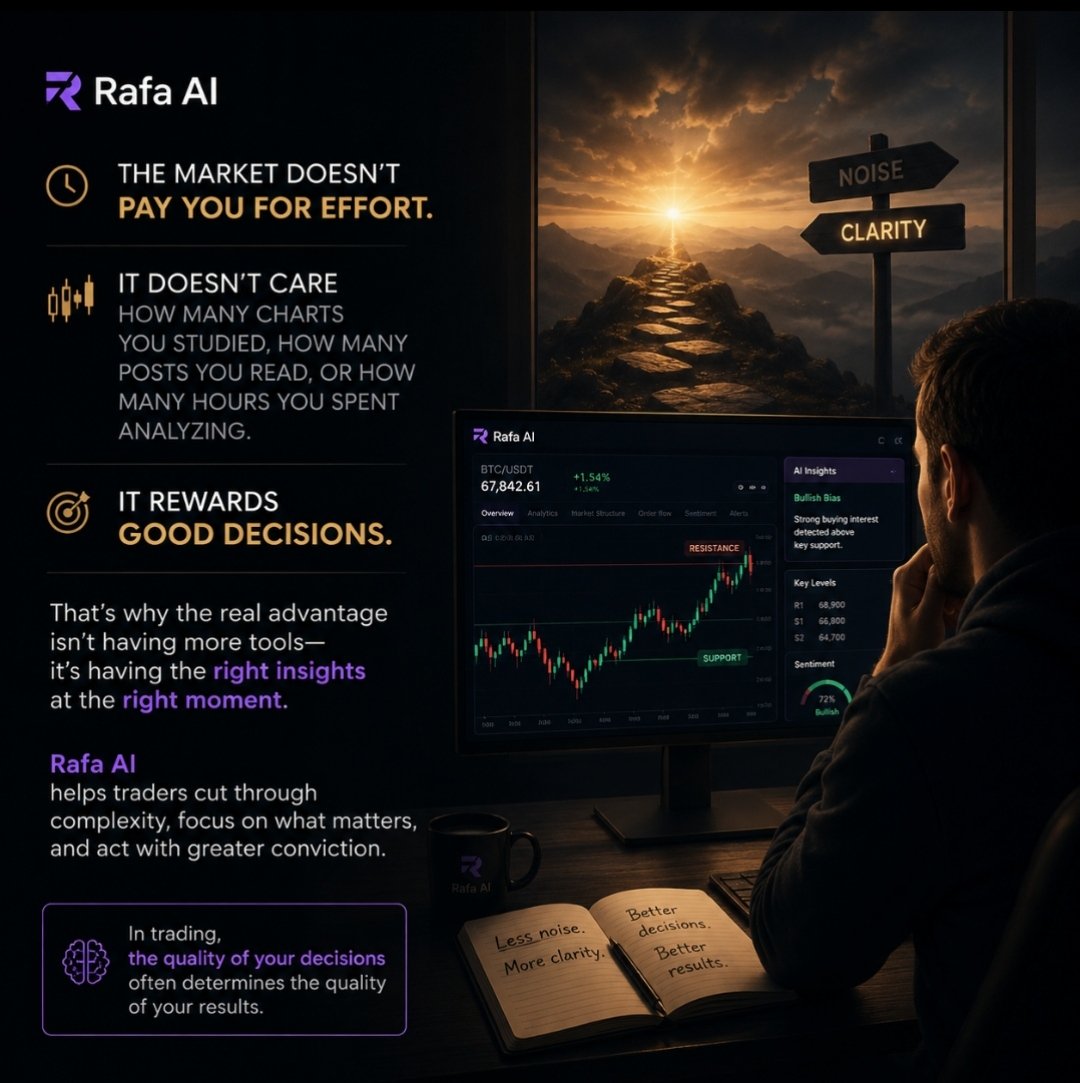

Rafa AI reveals a truth many traders learn too late:

The market doesn't pay you for effort. It doesn't care how many charts you studied, how many posts you read, or how many hours you spent analyzing.

It rewards good decisions. That's why the real advantage isn't having more tools-it's having the right insights at the right moment. Rafa AI helps traders cut through complexity, focus on what matters, and act with greater conviction.

In trading, the quality of your decisions often determines the quality of your results.

@RAFA_AI

@Metamorfozzz_

@srsh_os

A more practical way to look at Rafa AI is: how do you avoid bad decisions when you’re stressed or unsure?

Most bad decisions don’t come from lack of intelligence-they come from reacting too fast, or thinking too scattered. When you’re under pressure, you either overthink everything or jump too quickly.

can be framed around this moment: it helps structure your thinking so you don’t rely on emotion or noise when making choices.

In real life, that could mean checking a trade setup, filtering a rumor, or even deciding whether to act or wait-without letting confusion take the lead.

@RAFA_AI

@Metamorfozzz_

@srsh_os

6

Famiiisky retweeted

Jun 13

❓Which is your favourite RAFA Guru❓

News - breaks down complicated events ELI5

Strategy - analyzes TA, FA, and qualitative data

Quant Pro - weaponised autism on-demand

Depending on how you prompt RAFA, you'll tap into different agents.

Do you know how to get insights from all in one prompt?

135

104

175

2,586

Famiiisky retweeted

Jun 13

Traders rely on #optionsflow to identify unusual market behavior, so the Options Guru App streamlines it for you, to break down:

- Large/Sudden block trades

- Sweep orders

- Unusual options activity

- Open interest changes

- Dark pool activity

These signals show institutional positioning and potential shifts in market sentiment before they become obvious in price action.

You get it all in the simplest format, updated in real-time. #unusualoptions detects what the insiders know.

Incoming. Stay tuned for official updates when you can get your hands on the app.

131

103

171

2,616

Over 8.5 Million daily AI inference requests being processed on-chain, supported by a network of over 170,000 miners contributing compute resources.

Listen to our COO @stefanluke_ talk about the milestones we’ve quietly been ticking off and our plans for the future.

250

63

326

8,432

Famiiisky retweeted

Jun 11

112

14

126

450