FILPS is a UAE-based fintech enabler helping banks scale with AI-powered digital solutions backed by 20 years of global fintech expertise.

Joined September 2024

- Tweets 100

- Following 2

- Followers 10

- Likes 0

97 Photos and videos

Pinned Tweet

18 Sep 2025

Filps is a UAE-based global fintech enabler that works together with banks, financial institutions and service providers to design, implement and scale bespoke digital solutions that help achieve business goals and drive real impact. With a technology stack that draws strength from platforms that have powered some of South Asia’s most significant digital financial transformations, Filps is your behind-the-scenes fintech strategist - acting as both the solution architect and the transformation consultant - identifying gaps, shaping strategy, and staying with the institution throughout execution.

72

Jun 12

Shield the core. Scale the edge. Your legacy core wasn't built for 10M pings/minute. You don't need a "Rip-and-Replace"—you need an orchestration layer to handle high-concurrency demands safely.

Jun 5

Preserve the digital loop. When funds exit as cash, banks lose data and the float. Close the loop with an orchestration layer that connects utilities, groceries, and lenders.

3

Jun 2

Local payment networks are sitting on infrastructure that global merchants need — but can't easily reach.

FlxPop creates the channel. Here's how it works for acquirers and banks.

Read more: filps.com/insights/introduci…

1

May 29

For digital finance providers, the challenge isn't just the app—it's the acceptance. Filps' Merchant Management System (MMS) turns any smartphone into a payment terminal, ensuring digital funds stay digital within the bank's ecosystem. Close the loop.

6

May 18

Onboarding is a milestone. Retention is the goal. For banks/PSPs, volume is a vanity metric. Success is keeping liquidity digital. Don't just count users—orchestrate the ecosystem that keeps them.

2

May 11

MSMEs are the structural backbone of the Asian economy, yet the "credit gap" remains a persistent barrier. Traditional business lending models often struggle with the real-time velocity and diverse risk profiles of these enterprises.

When working capital isn't available at the point of decision, growth cycles are interrupted. For financial institutions, heavy manual underwriting and legacy data silos can make it difficult to capture this high-velocity segment at scale.

The transition to automated, data-driven business lending represents a significant technical unlock. By integrating alternative data and real-time decisioning, institutions can move MSME lending from a manual process to a high-volume, precision-driven engine for regional expansion.

Learn more in our blog on Indonesia’s UMKM Credit Gap: filps.com/insights/closing-i…

2

May 8

The global economy now moves at 24/7 real-time velocity, yet many institutional cores remain tethered to "end-of-day" batch cycles. This legacy constraint creates more than just technical debt, it creates liquidity gaps and prevents the launch of the contextually relevant, instant services that customers now expect.

While internal teams seek greater visibility to manage risk and performance, the operational complexity of legacy cycles can often influence the speed of modernization. Moving toward real-time decisioning is more than a technical shift; it provides an architectural path to surface value and security exactly when and where it's needed most.

19

May 4

In 2026, the success of digital transformation isn't measured by how much you change your core, but by how seamlessly you connect to the world around it.

The traditional "rip-and-replace" approach to core banking is too slow and too risky for the today’s market velocity. True agility comes from a decoupled architecture that leverages partner ecosystems for rapid scale-up.

Digital transformations work when you build on partner ecosystems. You don't need to overhaul your core to stay ahead.

8

May 1

Value leaks when your customers and partner merchants move outside your ecosystem. A Closed-Loop Digital Ecosystem ensures that value compounds between your customers, merchants and you. By closing the loop, you turn disconnected transactions into a self-sustaining cycle of data, intelligence, and loyalty, where every dollar spent reinforces your ecosystem's growth.

11

Apr 27

The bank of the future isn't an office building. It's a companion to your daily life. At Filps, we are building for that reality. By unlocking the potential of digital innovation at scale, we enable the architectural shift from destination to companion, ensuring that financial utility is always present.

2

Apr 22

Most core banking systems today operate like a black-and-white camera trying to capture a rainbow.

They see the "amount" of a transaction with sub-second precision. But they are blind to the "impact." In 2026, market leadership belongs to the institutions that move past high-level claims and toward Unit Economics.

Read how we’re closing the disclosure gap:

filps.com/insights/earth-day…

4

Apr 20

What if you could tap into borrowing needs that would otherwise be “unprofitable”? Complex risk assessments and paper-heavy workflows mean that some lending products are simply not feasible. We provide the architecture to enable infinite combinations of credit strategies—Fly now, Pay later; Fuel now, Pay later—delivered exactly at the point of decision.

2

Apr 15

Filps is excited to welcome Yoshitha Silva as our Country Manager for Sri Lanka.

With a strong background in business development and IT solutions, Yoshitha brings strategic expertise in managing complex account relationships and driving digital value. His prior experience at tech leaders like WSO2 has equipped him with a sharp understanding of regional market dynamics and client needs.

At Filps, he will lead our operations in Sri Lanka, partnering with local financial institutions to deliver bespoke, future-ready digital solutions.

Welcome aboard, Yoshitha.

7

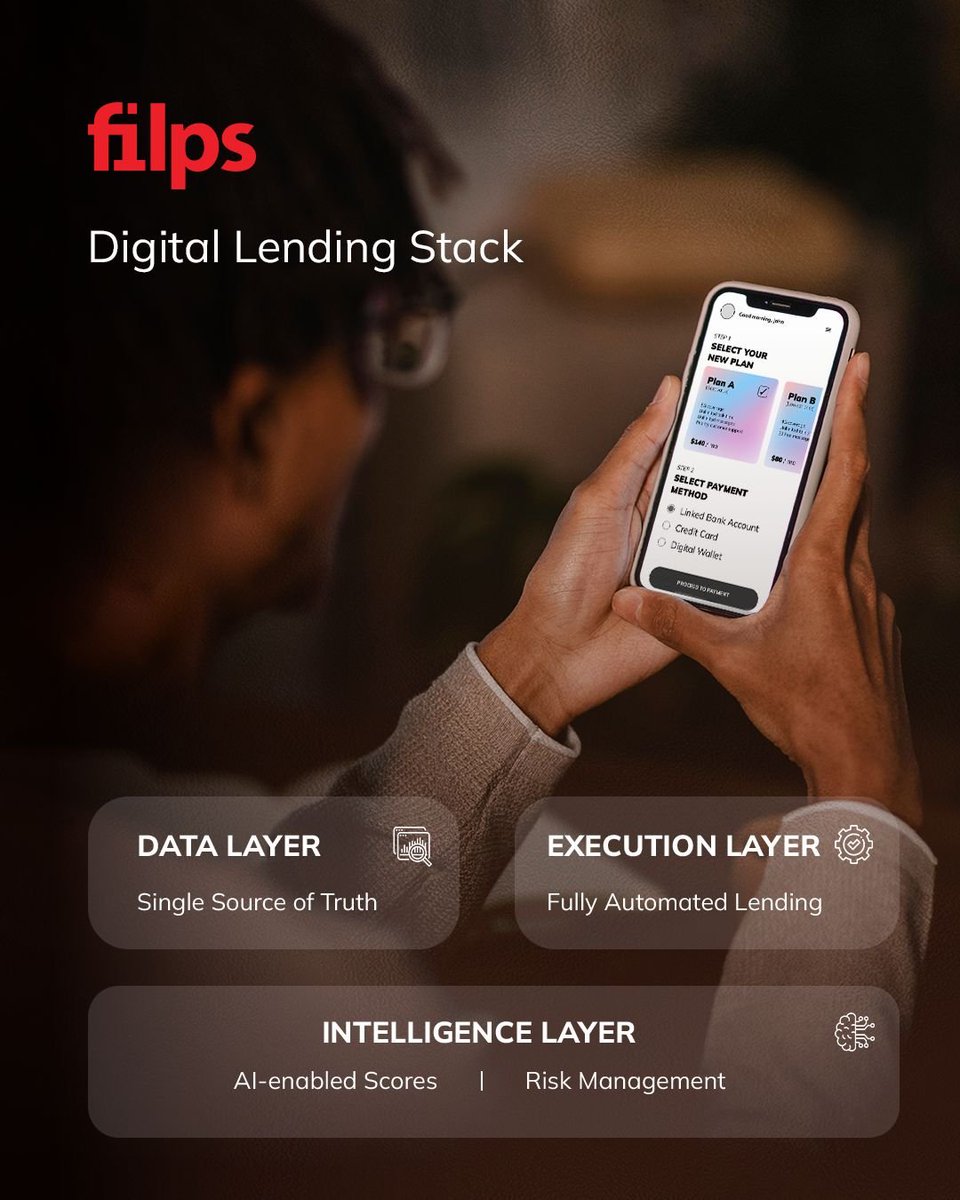

Apr 13

The best credit experience isn't found on your website or brochure; it's found at the point of decision.

Traditional lending relies on the customer doing the heavy lifting: searching, comparing, and applying. True digital leadership is about being present in the moments that matter.

By leveraging the Digital Lending Stack and Smart Middleware, we enable institutions to co-create value with their entire partner ecosystem. We move credit from a destination to a natively embedded companion, delivered precisely when and where your customer needs it most.

Deliver credit where life happens.

1

Apr 10

Banking is evolving from a physical destination to an Intelligence Layer that surfaces in moments that matter. Our AI-driven risk management doesn’t just record history it analyzes behavioral signals and transaction patterns. Our Digital Lending Suite provides the architecture to serve gig workers and MSMEs and other underserved segments with responsible, real-time credit.

2

Apr 6

Onboarding in minutes, access in seconds. The Filps digital onboarding suite eliminates friction associated with customer acquisition - from AI-enabled verifications to fully digital onboarding.

8

Apr 3

Personalization has moved away from “Dear [first name]” styled messages and emails. Your music app knows your favorite music genre. Your on-demand video service knows what new releases you might want to watch this weekend.

Don’t just create an app that shows your users where they spent last week, create a personalized experience that works with them.

1

Mar 30

The best banking experience is the one you don't notice. It happens in the background. Secure. Instant. Frictionless.

When payments are embedded into the apps we use every day, banking stops being a chore and starts being an enabler.

Don’t build banking that people go to, build one that comes to them.

2

Mar 27

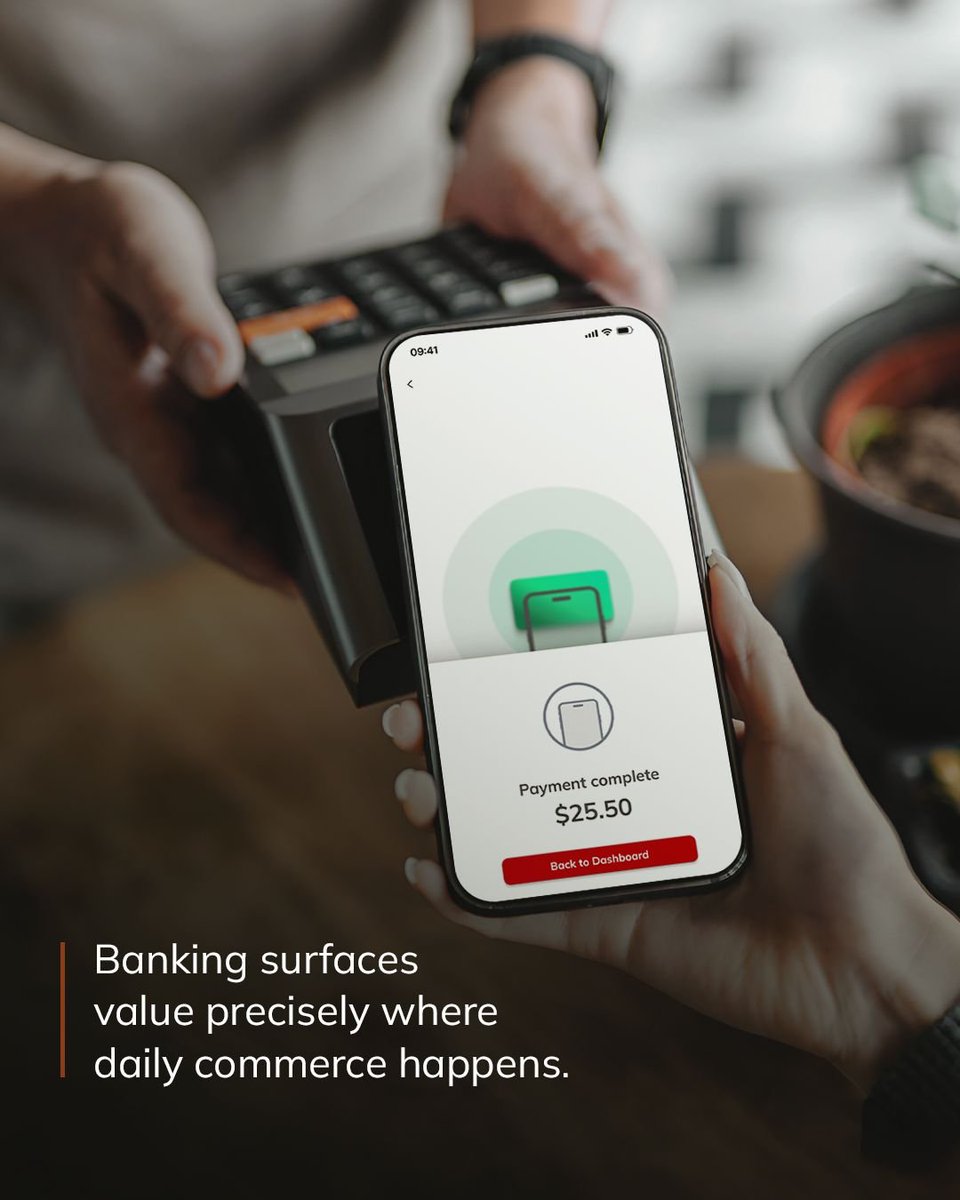

Traditional banking waits for you to visit a branch. Modern banking meets you at the moment of transaction. With Filps, make financial products including instant merchant payments, micro-lending and loyalty points available where your users already live.

3

Mar 25

The world's most powerful payment terminal is already in your merchant's pocket.

With SoftPOS, you can turn any smartphone into a secure point of sale.

Accept payments anywhere, anytime by making onboarding easier for merchants.

4