Joined July 2020

- Tweets 2,550

- Following 189

- Followers 985

- Likes 2,097

569 Photos and videos

Jun 11

Still uploading PDFs for loans?

Account Aggregator fixes that.

• 22 crore users

• 2.88B accounts enabled

• ₹1.6L crore loans processed

UPI changed payments.

AA is changing financial data.

7

Do SIPs work?

The ET Wealth–Crisil SIP Study 2026 says yes — but only with time.

The mistake: judging a SIP after 1–2 years.

SIPs aren't built to avoid volatility.

They're built to help you invest through it.

Time in the market > timing the market.

19

₹5 lakh surgery today.

~₹18.5 lakh in 10 years.

(At 14% medical inflation)

Future Hospital Bill =

Today's Bill × (1 Medical Inflation)^Years

Your health cover may stay the same.

Hospital bills won't.

Before renewing, ask:

Will my cover still protect me 10 years from now?

13

Before India wakes up, GIFT Nifty is already trading.

It reflects overnight global sentiment:

• US markets

• Oil

• Fed commentary

• Global events

But remember:

GIFT Nifty ≠ Nifty Spot.

It's a futures contract.

Use it to gauge sentiment, not predict the open.

151

₹8L hospital bill today.

~₹14–15L in 5 years.

(Assuming medical inflation 12-14%)

Formula:

Future Bill = Current Bill × (1 Medical Inflation)^Years

Health insurance doesn't become inadequate overnight.

Medical inflation does it slowly.

27

May 29

India built an international stock exchange.

NSE IX:

• Based in GIFT City

• USD trading

• ~21 hrs/day access

• GIFT Nifty moved from SGX to India

• Global products, dollar-settled

India isn’t just joining global finance.

It’s building the platform.

238

May 28

NFTs. Metaverse. SPACs. Play-to-Earn.

Same cycle every time:

Idea → cheap money → FOMO → crash.

The tech may survive.

The investor often doesn’t.

18

May 25

Your 20s aren’t about looking rich.

They’re about:

• building savings habits

• avoiding lifestyle inflation

• creating financial breathing room

Discipline compounds before money does.

16

May 22

Same PAN.

Same Aadhaar.

Different KYC forms every time.

CKYC 2.0 wants to change that.

One reusable KYC across banks, brokers, MFs & insurance.

Biggest challenge?

Security, not convenience.

26

May 20

Financial freedom isn’t one big jump.

It’s 7 levels.

Most people dream about: Level 7 → abundant wealth & complete freedom

…while still struggling with: Level 3 → escaping paycheck-to-paycheck stress.

You can’t skip the middle.

That’s where real financial progress happens.

11

May 18

NPS Swasthya ≠ health insurance.

It’s backup liquidity.

Remember:

• Only 25% withdrawal

• Market risk still exists

• Emergencies & crashes can overlap

Insurance first.

Emergency fund second.

1

25

May 14

AI can analyse spending.

Doesn’t mean it understands your finances.

• Good at patterns

• Weak with tax nuance

• Confidently wrong sometimes

• Privacy risks are real

Use AI for questions.

Not blind decisions.

16

May 13

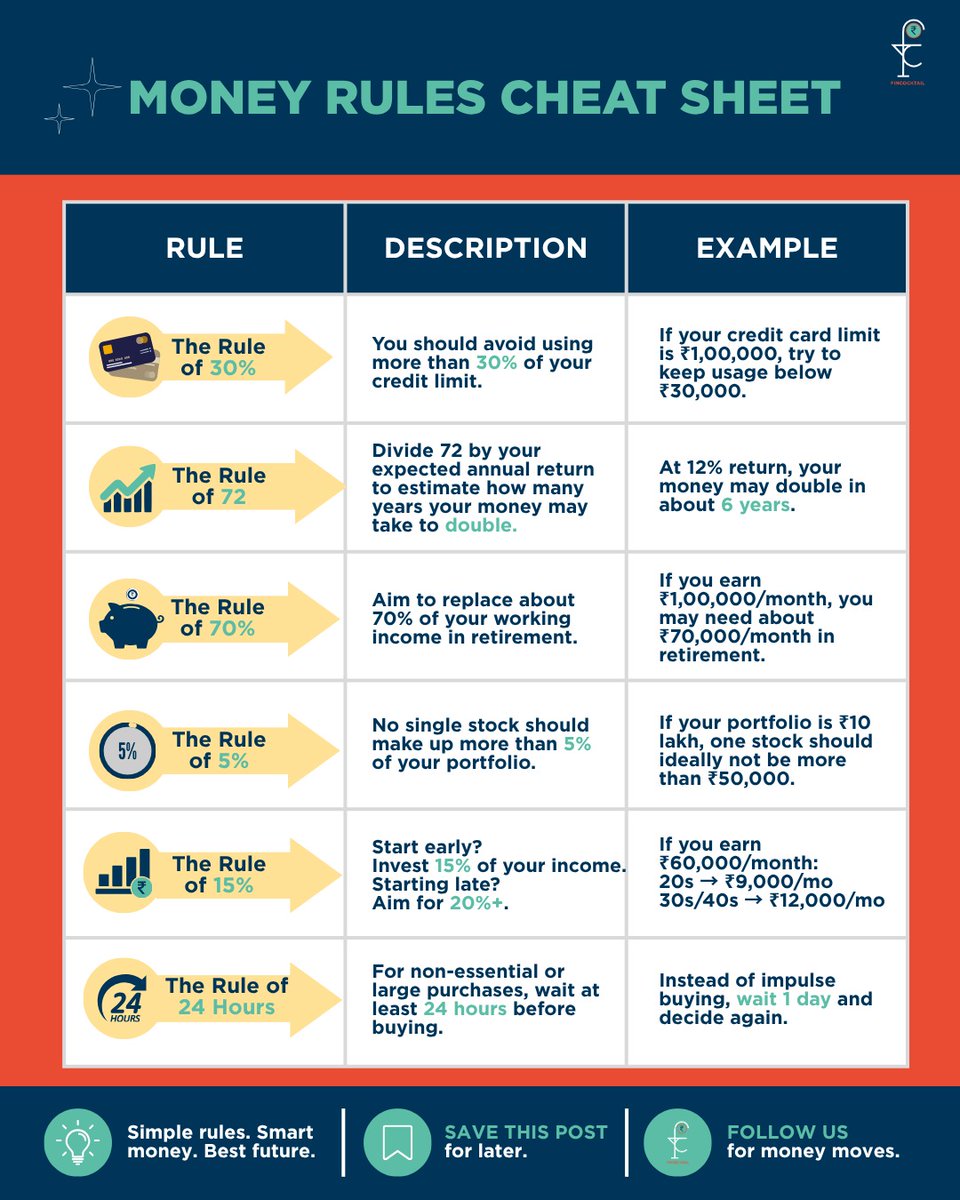

6 simple money rules:

• Credit usage <30%

• Rule of 72

• Diversify

• Invest 15% income

• Pause before impulse buys

Simple rules > emotional decisions.

1

21

NSE just changed gold investing in India.

EGRs:

• SEBI-regulated

• Backed by physical gold

• Held in demat form

• Tradable on exchange

• Convertible to physical gold

Gold is moving from lockers → exchanges.

29

3 simple investing rules:

• 100 minus age → equity allocation

• Core–satellite → stability growth

• Emergency fund first → liquidity matters

Simple portfolios outperform complicated ones.

13

3 simple investing rules:

• 100 minus age → equity allocation

• Core–satellite → stability growth

• Emergency fund first → liquidity matters

Simple portfolios outperform complicated ones.

17

Apr 29

Your child’s retirement can start today.

NPS Vatsalya:

• Open from birth

• ₹10K/year

• Long-term compounding

Tax benefit (old regime)

Start early. Time does the heavy lifting.

16

Apr 24

RBI cuts rates.

Your EMI stays same.

Why?

• Not all loans linked to repo

• Slow reset cycles

• Banks don’t auto-adjust

Small % gap = big cost.

Check your loan type.

30

Apr 22

Your PAN = your financial identity.

Misuse isn’t obvious.

You find out late.

• Links loans, banks, taxes

• Issues show up on triggers

• Fix takes time

Check AIS & credit report.

31

Apr 15

From Apr 1, 2026:

15G/15H → Form 121

Use it to stop TDS if income < tax limit.

Remember:

• Submit early

• PAN mandatory

• Per bank submission

Don’t lose money unnecessarily.

86