Understanding Indian Stocks the Smart Way | Techno Funda Insights for Everyday Investors | Learn & Become Financially Free with Us | Disclaimer: No Buy/Sell Adv

Joined September 2024

- Tweets 918

- Following 16

- Followers 5,322

- Likes 196

572 Photos and videos

Pinned Tweet

20 Oct 2025

This clip gives a quick glimpse of how our services create value for investors

youtube.com/watch?v=HXLrESrH…

1

3

25

34,010

Shivalik Bimetal Controls Ltd

Management explained that their revenue planning is based on customer forecasts, which include both best-case and more realistic scenarios. Under best-case assumptions, revenue can return to earlier peak levels. However, even if some external factors prevent full recovery and they operate closer to a conservative or even pessimistic scenario, the business still remains strong.

The key change in the business model is the shift toward higher value-added components. Even if volumes do not fully recover to past levels, the value addition per unit is almost double compared to earlier strip-based products. This means that revenue growth may be moderate, but profitability and bottom-line contribution will be significantly better.

Management also highlighted that these transitions take time and may shift by a few quarters, but the direction is clear. Even if revenue eventually returns to earlier peak levels in the next 4–6 quarters, the company’s exposure to this customer will remain controlled. It will account for only about 17–18% of total revenue, compared to nearly 35–40% in the past.

Earlier, the company was heavily dependent on this customer, which created vulnerability when orders declined. Now the business is more balanced and diversified, so even small fluctuations in volumes will not significantly impact overall performance.

In short, the worst impact from the decline is largely behind, and the company is now in a stronger position due to better product mix, higher value addition, and reduced customer concentration risk.

#SBCL

4

25

8,197

Yasho Industries Ltd

Strong Growth Visibility: Management is targeting Rs. 1500 Cr. revenue by FY28 vs 830 Cr by FY26 and 35–45% volume growth, higher capacity utilization, and margin expansion as guidance.

Operating Leverage Play: With 75% utilization and Rs. 125 Cr. capex funded through internal accruals, EBITDA margins are expected to improve to around 20%.

#YASHO

1

6

26

1,474

Goldiam International Ltd

Growth Margin expansion

Plans to open 8-10 more stores by September 2026, targeting a total of 45-50 stores by the end of FY27.

Grew from 12 to 24 operational stores across 12 cities since January 2026 ( Rapid Stores)

Margin expansions reason has explained in below👇

One of the interesting concall for FY26 Q4.

5

34

1,693

Beta Drugs Ltd

The company has set a vision to achieve revenue of Rs. 850–900 Cr. by FY30, compared to Rs. 385 Cr. in FY26.

Near term triggers from concall:

Export supplies from recently awarded tenders will begin in Q1 FY27, with management targeting 50% export growth in FY27 and maintaining its Rs. 200 Cr. export revenue goal by FY28 through expansion into 14 new countries.

Export operations are normalizing after temporary delays, and management expects around 30% export revenue growth in H1 FY27.

The company plans to launch around four products in FY27, including two NDDS products, as part of a 20–25 product pipeline over the next 3–4 years.

The Nivian fertility business will contribute for the full year in FY27 and is expected to grow around 30% annually over the next 3–4 years, supported by distribution expansion and operational synergies.

4

37

2,196

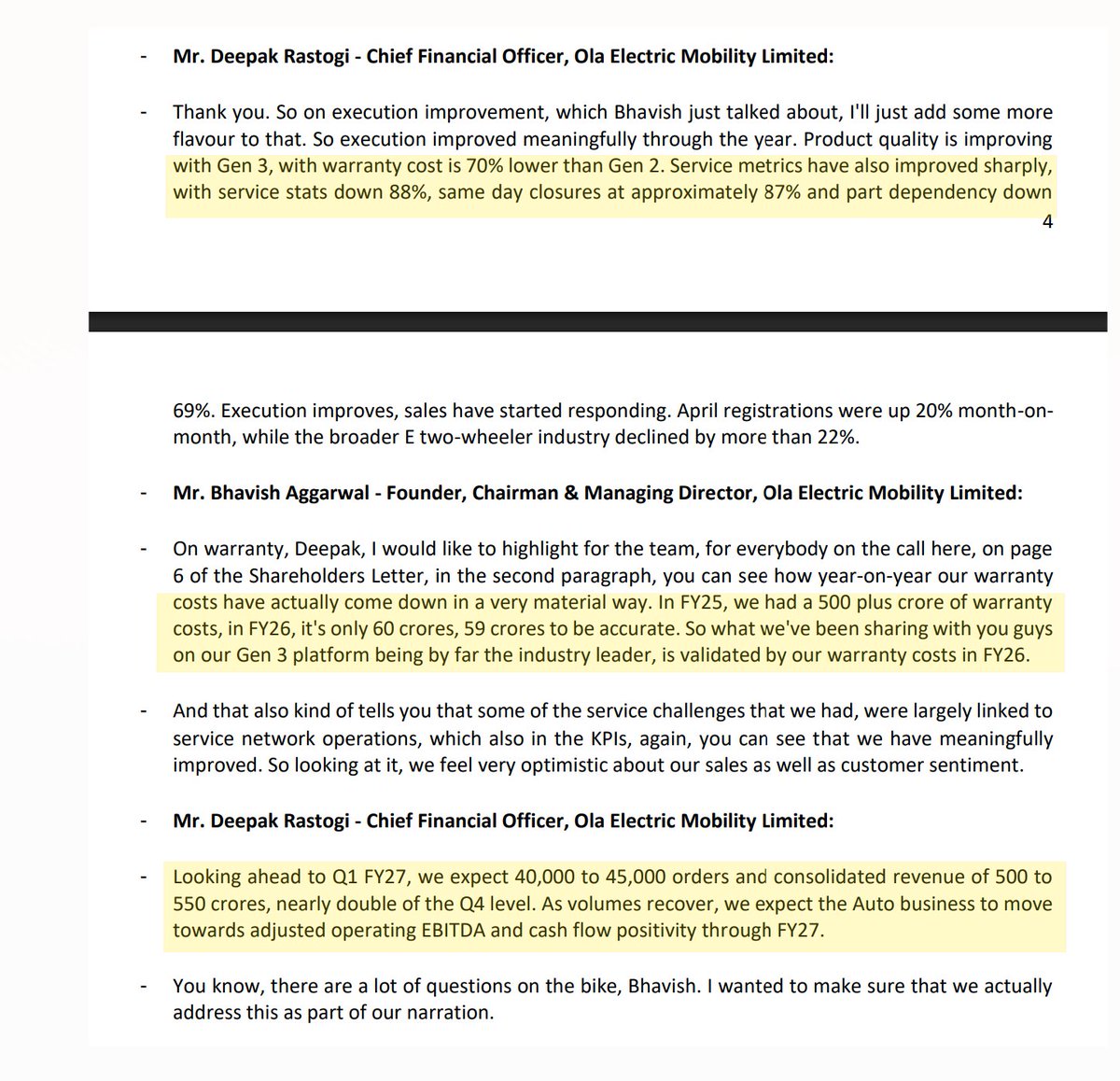

Ola Electric Mobility Ltd

The commentary from the company has indicating that the worst is behind them. The points highlighted below provide further clarity and support for this view.

#OLAELEC

8

4

51

3,826

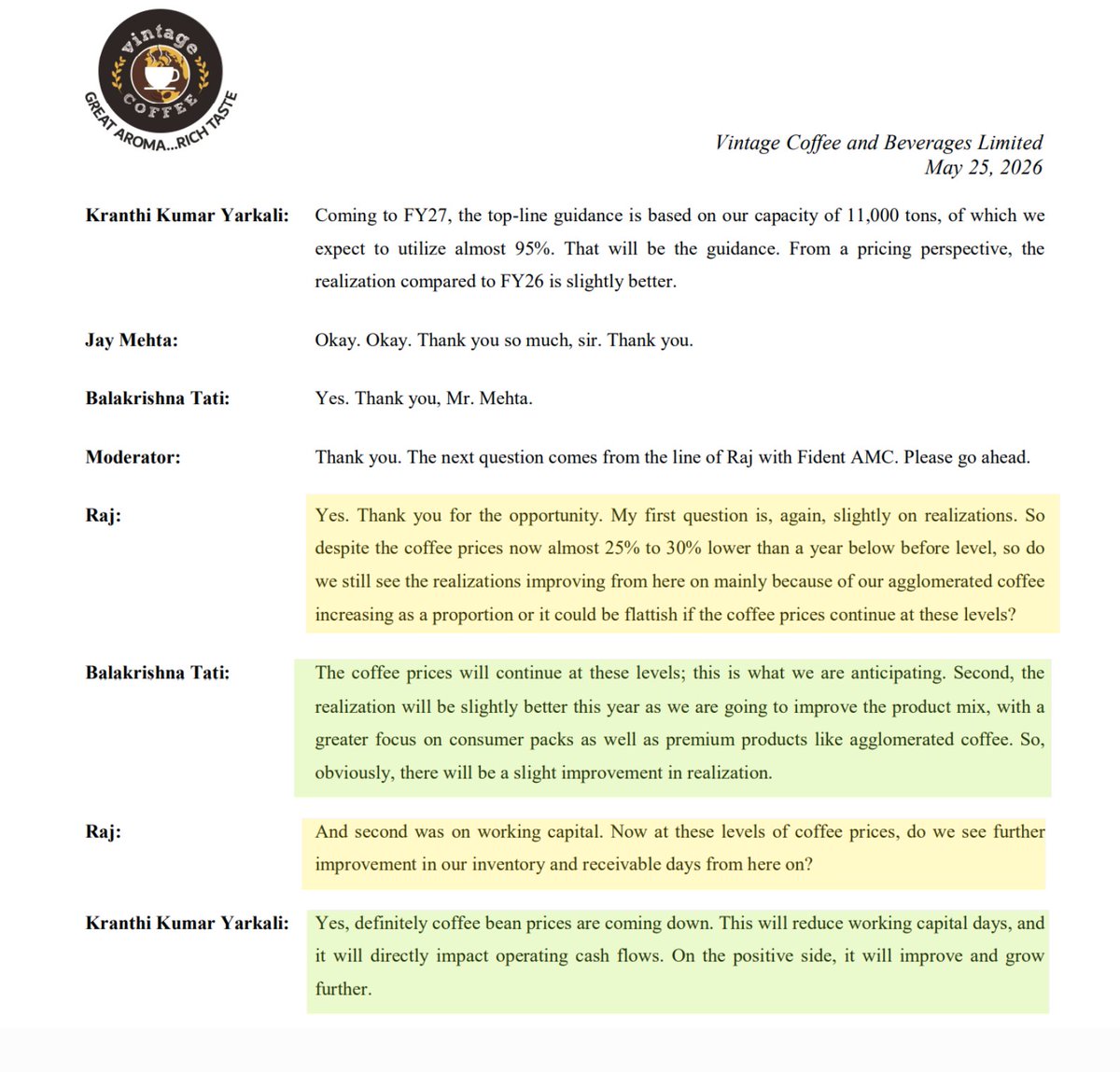

Vintage Coffee & Beverages Ltd

Since the concall, coffee prices have fallen by 10%. As management had anticipated stable coffee prices, this decline is a significant positive. Realizations are likely to improve, and working capital requirements are also expected to come down.

#VINCOFE

1

4

40

13,196

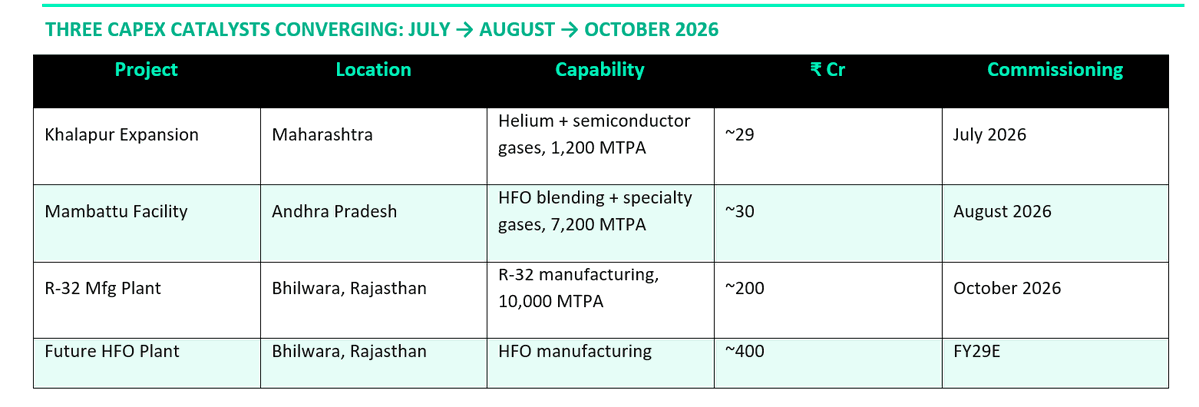

Quality Power Electrical Equipments Ltd

Quality Power said the ₹315 crore acquisition of Winwin Speciality Insulators is a strategic step to become a more fully integrated high-voltage electrical equipment player by adding ceramic insulators up to 1200 kV and polymer insulators up to 400 kV, along with an 18,000 MTPA automated plant built on German technology. The management clarified that the deal was done on an asset-value basis rather than an EBITDA multiple, and the facility had earlier been damaged in 2014 and has since been refurbished.

The company expects this acquisition to strengthen its position in the HVDC space and reduce supply-chain bottlenecks across its product portfolio. Management indicated that the plant should begin contributing within about six months, with the business potentially generating over ₹200 crore next year once approvals are in place. They also highlighted early execution progress by confirming the shipment of four containers to the US.

Strategically, the company aims to position itself as the “Hitachi Energy of India,” with a strong focus on exports to the US and Europe. Going forward, management plans to fully integrate this acquisition before pursuing further deals, while continuing to expand in BESS, GIS, HVDC, and data-center-related power infrastructure.

Key message : The management message is that the company is not just talking about growth; it is backing it with acquisitions, plant capacity, exports, and product expansion

#QPOWER

youtube.com/watch?v=ura3Hy45…

1

31

3,177

Syrma SGS Technology Ltd

"We are on the track for $1B revenue for FY28"

Syrma SGS is targeting about $1 billion revenue by FY28 and says it is on track, supported by a strong order book, new customer additions, and execution across multiple segments. The company is gradually shifting its business mix beyond consumer electronics into higher-growth areas such as data centers, defence, railways, healthcare, EV infrastructure, and industrial electronics, while keeping consumer electronics below 30% of total revenue.

Management expects revenue growth of 30% to 35%, EBITDA growth of around 30%, and operating cash flow at 30% to 40% of EBITDA. They also note that rupee depreciation supports the dollar revenue target when converted into rupees, while geopolitical factors increase costs related to logistics, freight, insurance, metals, and oil.

The PCB project is highlighted as a key future growth driver and could contribute around ₹1,000 to ₹1,200 crore by 2029–30. In the data center segment, Syrma SGS is currently active in power management and cooling and is working to enter the compute-board segment, which management believes could become a major growth opportunity if successful.

Overall, the company’s strategy focuses on scaling rapidly through higher-growth, higher-margin segments while maintaining strong cash flow generation.

youtube.com/watch?v=68NBirtq…

1

5

34

2,644

HFCL – Key Investor Takeaways

#HFCL

"EBITDA margins expected to improve by 3–4% in FY27"

HFCL is aggressively expanding its fiber optic cable ecosystem to support rising demand:

Fiber optic cable capacity increasing from 28 million fiber-km to 34 million fiber-km annually

Additional cable capacity of around 4–5 million km per year is also being added

Expansion is aimed at meeting rising demand from data centers and telecom infrastructure

Hyperscale data center projects require significantly higher fiber counts per cable

Company is unable to accept all business opportunities due to capacity constraints.

Planned capex is Cr. 125 for fiber expansion, Cr. 100 for connectivity solutions, and Cr. 580 for preforms/backward integration.

-------------------------------

Defense: Second Major Growth Engine and Order Book 2500cr.

Expected defense revenue is Cr. 500–700 in the current year, Cr. 1500 in the next year, and around 5000Cr within three years.

Growth Drivers:

---> Indigenous radar systems

--->Anti-drone solutions

--->Thermal weapon sights

--->Export opportunities

-------------------------------

Do watch management interview in below.

HFCL Ltd

Watch the management walk and talk 👌

youtube.com/watch?v=Coe-6Vek…

7

36

10,721

HFCL Ltd

Watch the management walk and talk 👌

youtube.com/watch?v=Coe-6Vek…

10

6,440

Financially Free ™ retweeted

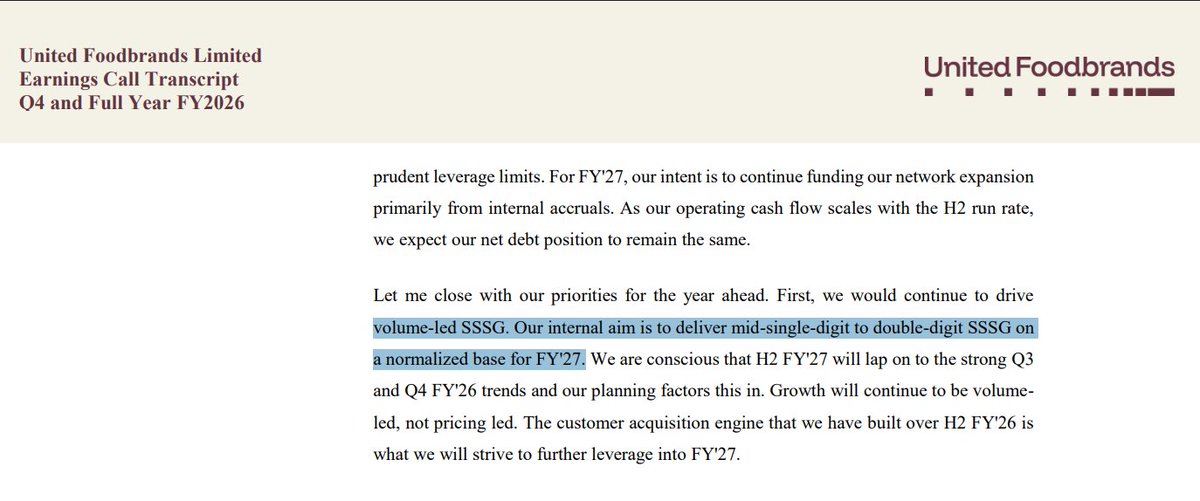

United Foodbrands Ltd

#UFBL

The new multi-brand strategy (SALT, Toscano) adds a fresh growth narrative beyond Barbeque Nation, making it an interesting turnaround candidate.

FY27 SSSG Outlook : Volume lead growth in Double Digits in SSSG.

The company has strong visibility to add 40 new restaurants in FY27, supported by 11 restaurants under construction and a robust pipeline of advanced commercial discussions.

Margins: 9-10% OPM for FY27 with Gross Margins improvement of 100 bps.

No buy or sell recommendation.

1

2

25

2,693

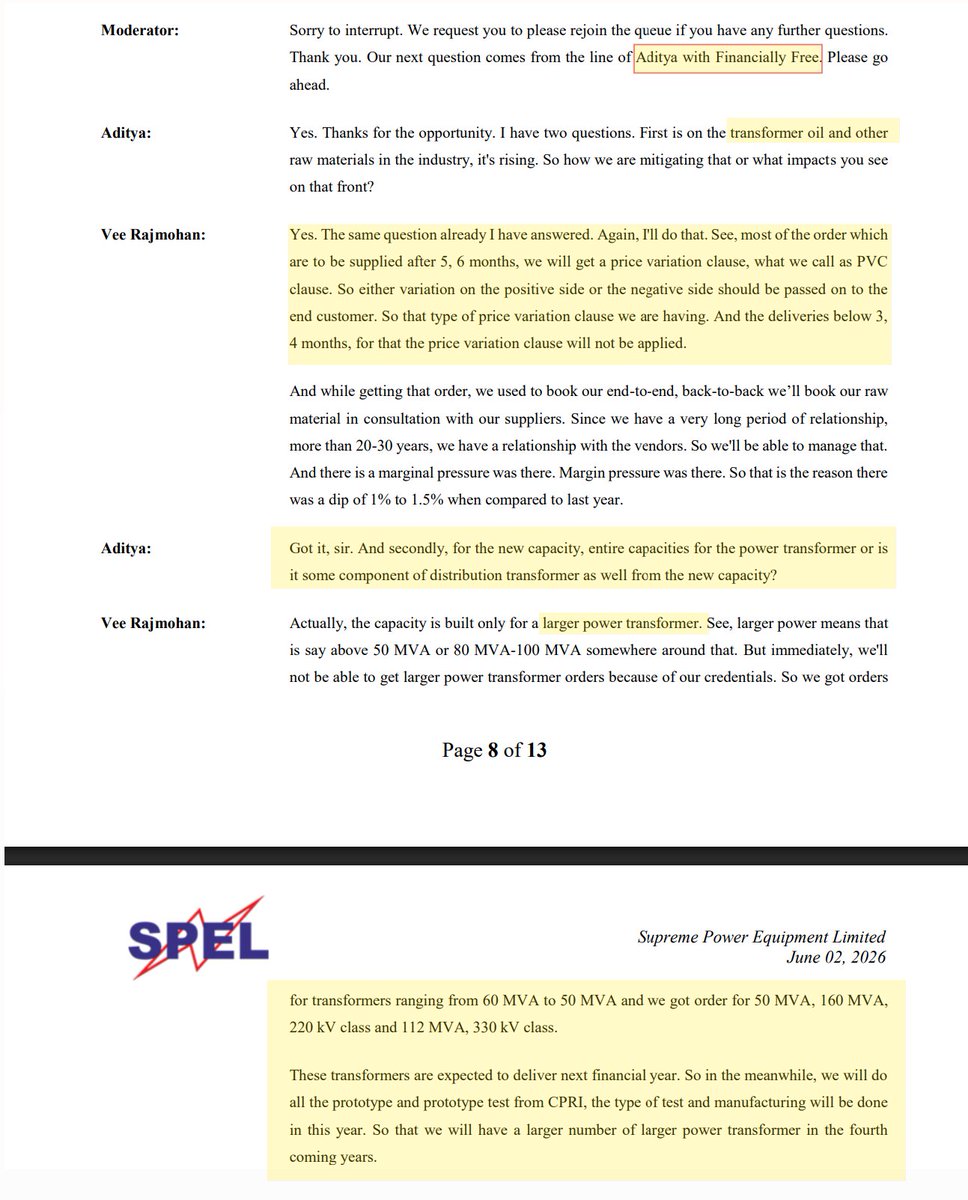

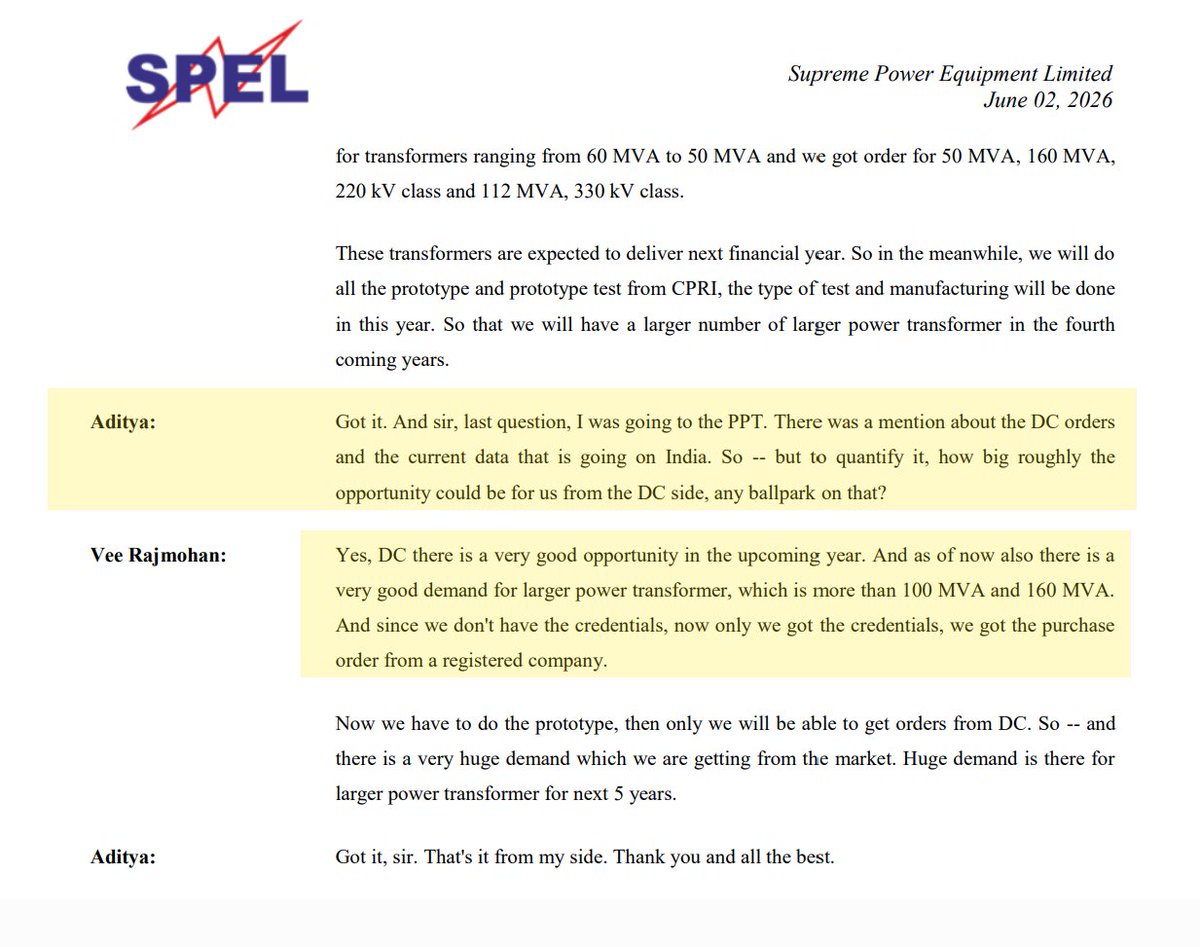

Supreme Power Equipment Ltd

#SUPREMEPWR

There were a few interesting questions raised by Our Analysts during the concall. One of the key discussions was on how the company is able to pass on raw material cost increases to customers through price variation clauses. Analysts also asked about value-added products such as Power Transformers and the last Data Centers enquiries .

Overall, the discussion provided some useful insights into the company's business and growth opportunities.

3

31

2,198

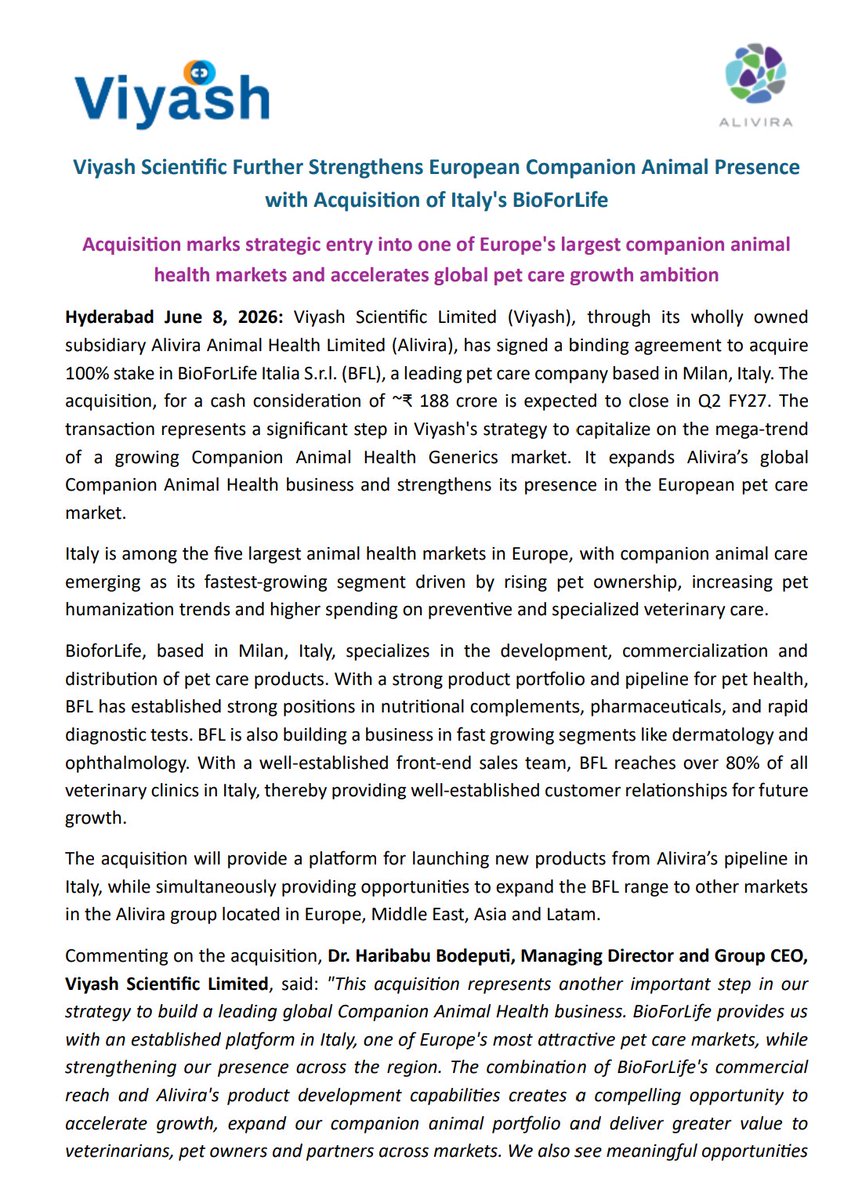

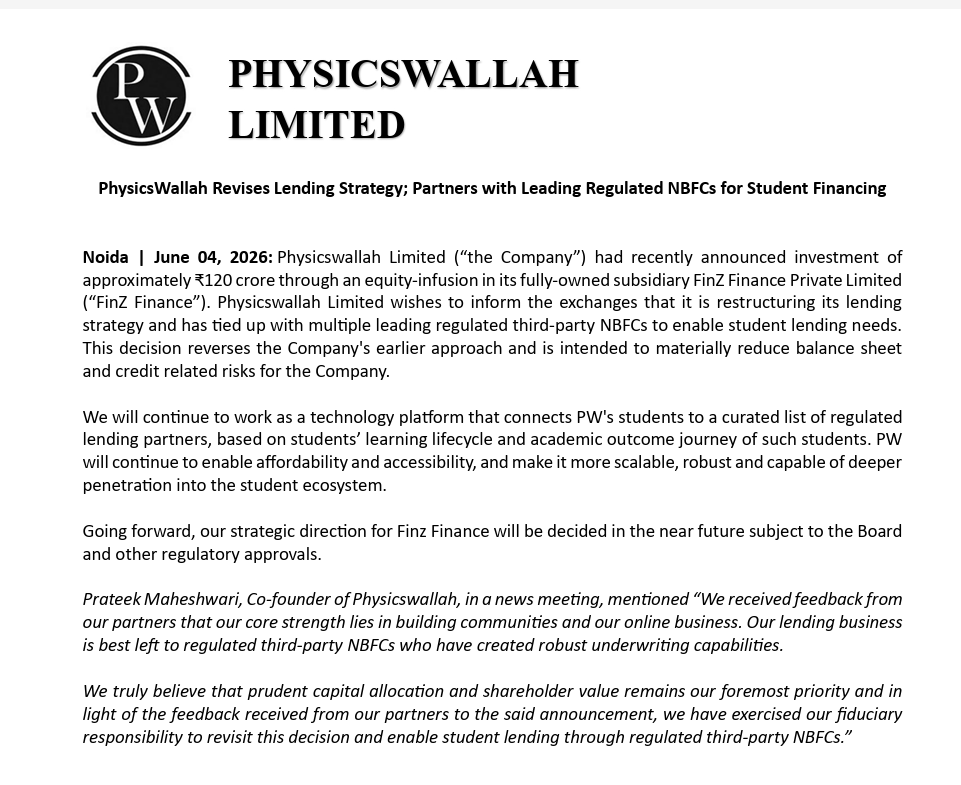

Viyash Scientific Ltd

#VIYASH

Viyash Scientific (via subsidiary Alivira) has signed a binding deal to acquire 100% of BioForLife Italia S.r.l.

a leading Milan-based pet care company for ₹188 crore cash. Deal expected to close in Q2 FY27.

Market Entry: Italy ranks among Europe's top 5 animal health markets, with companion animal care being its fastest-growing segment , a high-conviction growth bet.

Strategic Fit: The deal flows through Alivira (wholly owned subsidiary), reinforcing Viyash's focused push into the Companion Animal Health Generics space.

Immediate Commercial Leverage: BFL already covers 80% of veterinary clinics in Italy meaning no cold-start; revenue ramp potential is near-term.

Portfolio Synergy: BFL's strengths in nutritionals, pharmaceuticals, diagnostics, dermatology, and ophthalmology complement Alivira's existing pipeline.

Cross-Market Upside: BFL products can expand into Alivira's existing network across Europe, Middle East, Asia, and LatAm and vice versa.

6

44

3,970

Corning shares jump 9% after striking deal to power Amazon AI data centers in U.S.

cnbc.com/2026/06/08/amazon-t…

3

33

2,640

Corning shares jump 9% after striking deal to power Amazon AI data centers in U.S.

cnbc.com/2026/06/08/amazon-t…

13

3,613

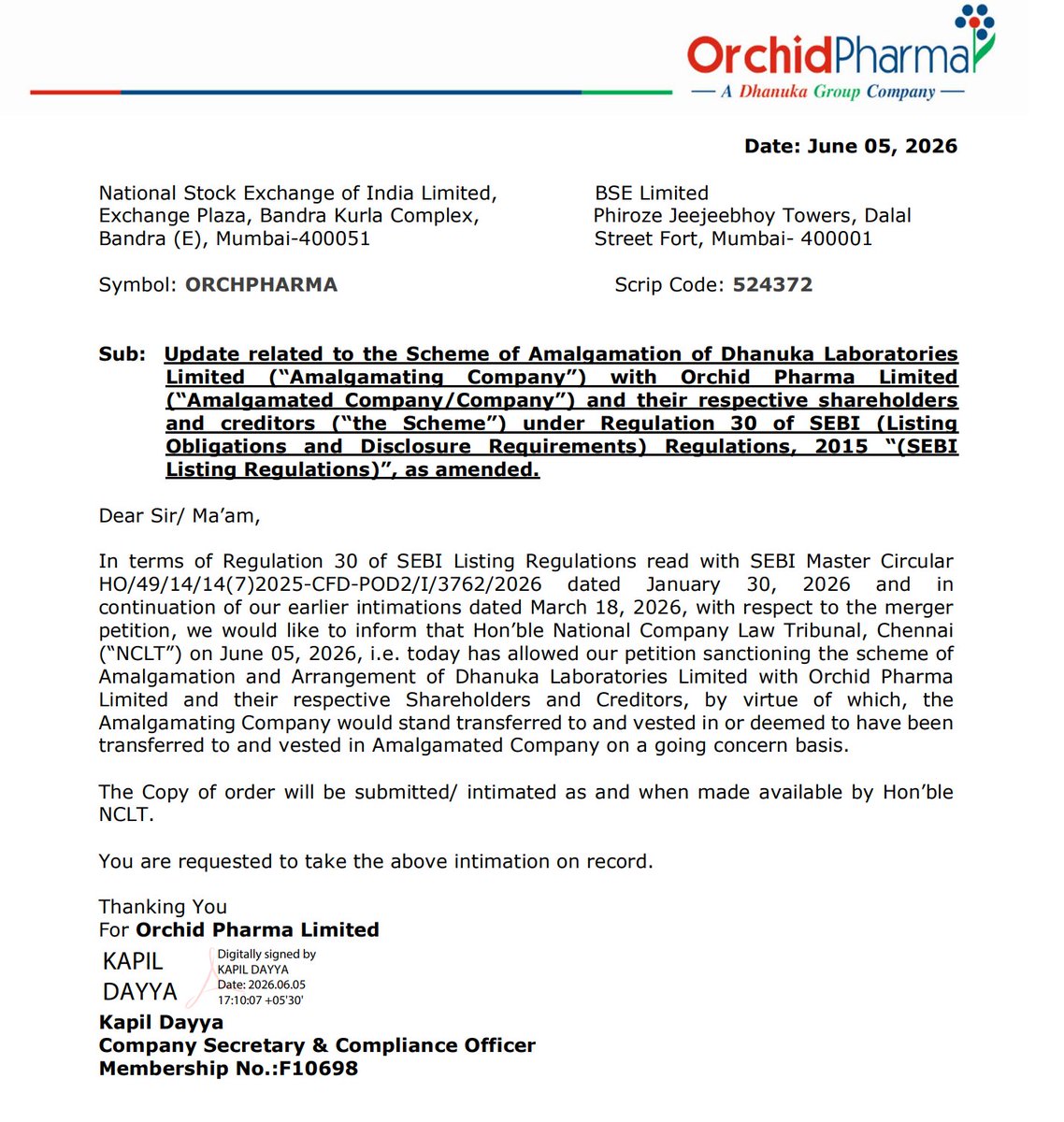

Orchid Pharma Ltd.

NCLT Chennai has approved the Scheme of Amalgamation of Dhanuka Laboratories with Orchid Pharma

Positive.

4

21

1,805

The AI and data center story is just beginning.

AirTrunk’s : Investing $30B expansion in India !

The Union Budget FY27 has announced a 20-year tax holiday up to 2047 for foreign companies that provide global cloud services using data centers located in India. This means such companies will not be taxed in India on global income generated through Indian data center infrastructure, provided services to Indian customers are routed through an Indian entity.

The objective is to remove tax uncertainty, attract large-scale global hyperscale and AI investments, and position India as a global data center hub. The benefit applies mainly to foreign cloud operators like global hyperscalers, not directly to domestic data center operators.

Reports and early industry reaction suggest that this policy is expected to unlock large investments, including major commitments such as AirTrunk’s ~$30B expansion in India, as global operators accelerate capacity buildout in response to strong policy visibility and AI-driven demand growth.

Today, AirTrunk operates across Australia, Japan, Singapore, Hong Kong, and Malaysia. It is now expanding aggressively into India and Saudi Arabia to capture the booming demand from cloud computing and AI.

In 2024, AirTrunk was acquired by Blackstone and Canada Pension Plan Investment Board in a transaction valuing the company at over A$24 billion, making it one of the largest infrastructure deals in Asia-Pacific history

Jun 5

India’s digital infrastructure journey is gathering remarkable momentum.

AirTrunk has announced plans to invest around Rs. 3 lakh crore ($30 billion) in India, and develop 5 GW of data centre capacity. This is among the largest proposed investments in the country’s digital infrastructure ecosystem.

Such investments will strengthen India’s position as a global hub for cloud computing and AI, while generating employment opportunities, supporting local supply chains and accelerating innovation-led growth.

It is clear that the future of the world’s digital economy is increasingly being shaped in India!

3

4

20

2,616