Drive your investment success with intelligent analytics.

Joined May 2017

- Tweets 2,093

- Following 262

- Followers 3,353

- Likes 874

1,587 Photos and videos

Jun 12

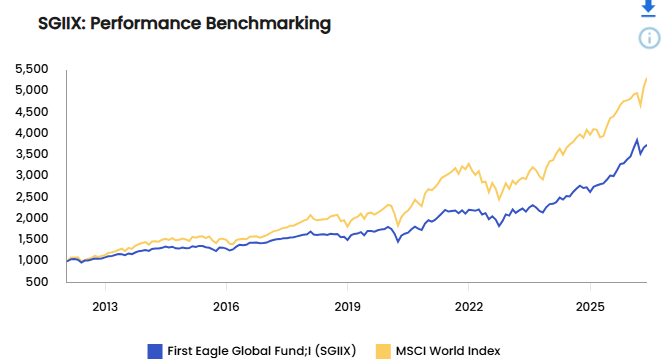

Product Review: First Eagle's $75bn Global Fund (SGIIX). What is the fund's strategy and performance?

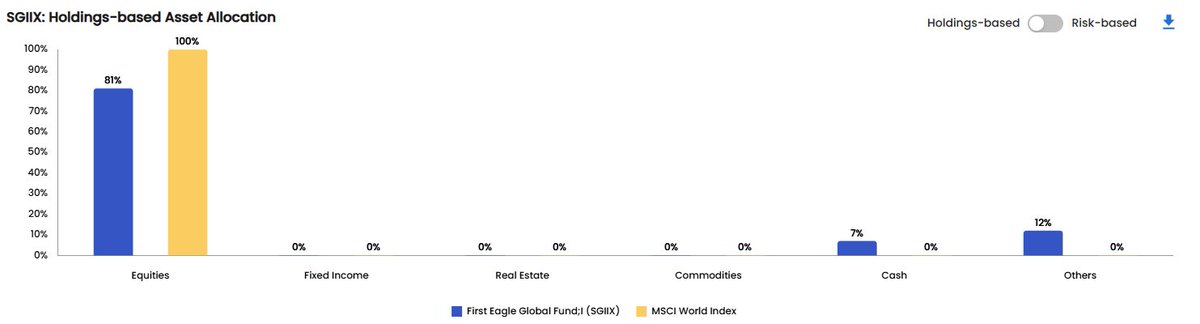

The fund has a track record going back to 1970 and provides exposure to global equities via a concentrated stock portfolio, plus a structural 10-20% position in gold and a similar allocation to cash for opportunistic investing.

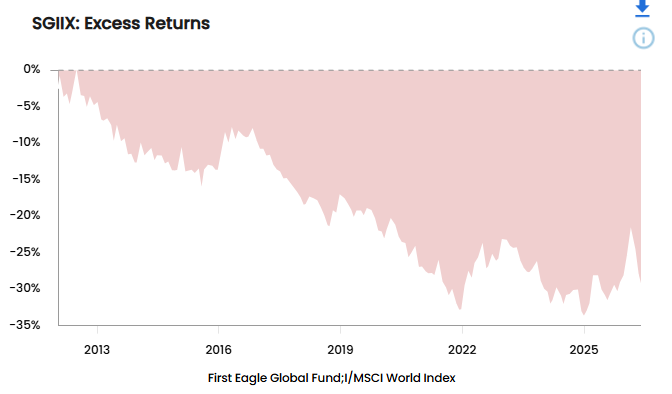

SGIIX's factsheet features the MSCI World Index as the benchmark and has outperformed it since the share class's launch in 1998.

finominal.com/fund-analyzer-…

1

2

289

Jun 12

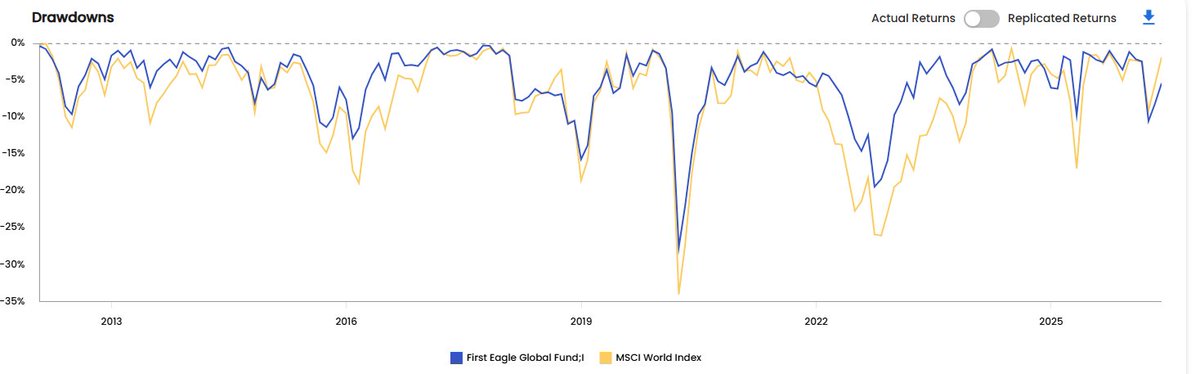

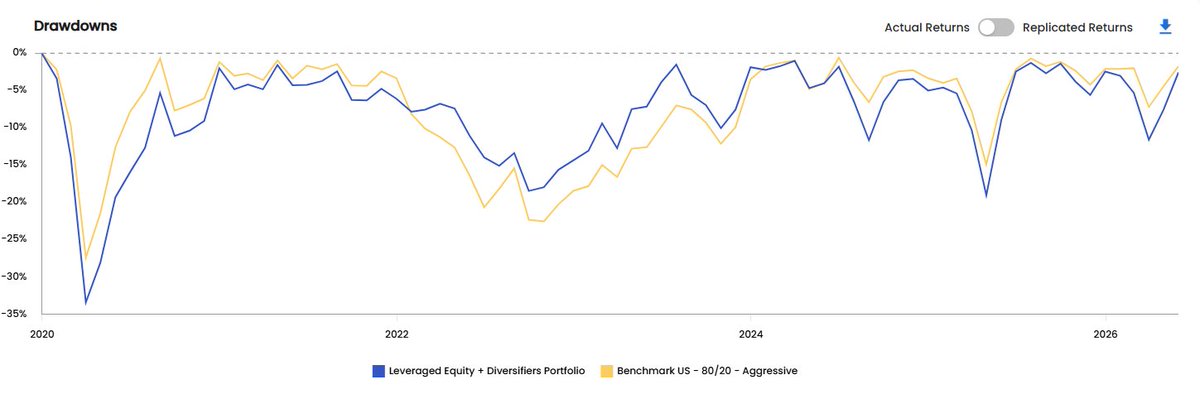

How has the fund performed in periods of market stress? We observe that SGIIX had consistently lower drawdowns during periods of market stress compared to the MSCI World Index. Given meaningful cash and gold allocations, this is to be expected.

finominal.com/fund-analyzer-…

1

88

Jun 12

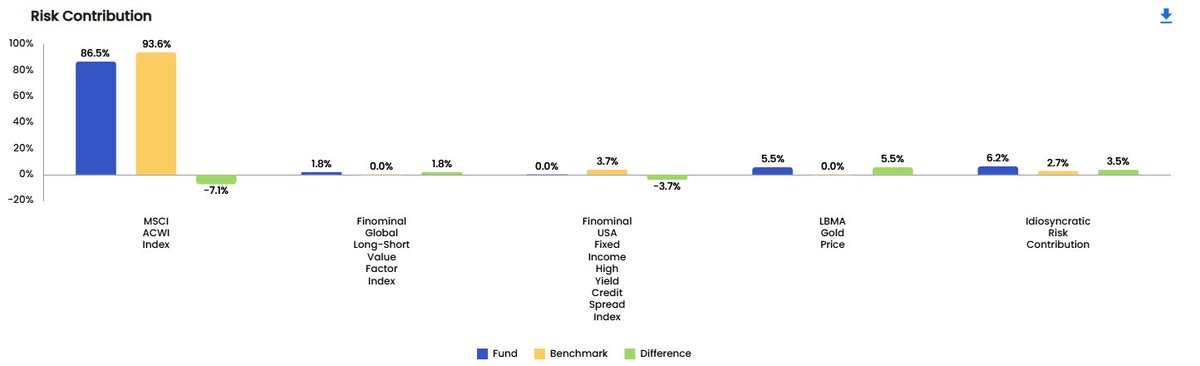

Can we replicate the fund? Yes, we can create a proxy portfolio using the MSCI World (70%), gold (15%), and cash (15%), mirroring SGIIX's investment strategy. The replication portfolio would have generated a higher CAGR and a slightly higher Sharpe ratio. However, it only costs 0.25% vs 0.86% for SGIIX.

finominal.com/asset-comparer…

76

Jun 10

We are excited to introduce our AI Document Reader, which instantly converts client brokerage statements into portfolios, ready for further analysis on Finominal. It also works for returns from fund fact sheets and unstructured text from emails. Spend less time on processing data and more time on generating insights.

finominal.com/statement-read…

122

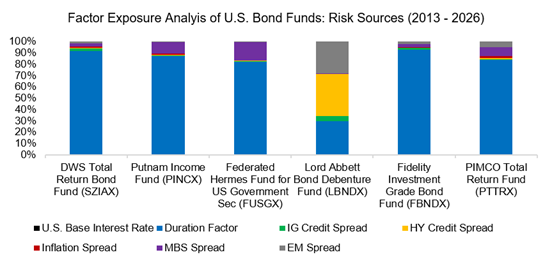

Factor Exposure Analysis 119: Fixed Income Factors III.

What is driving bond funds?

insights.finominal.com/resea…

205

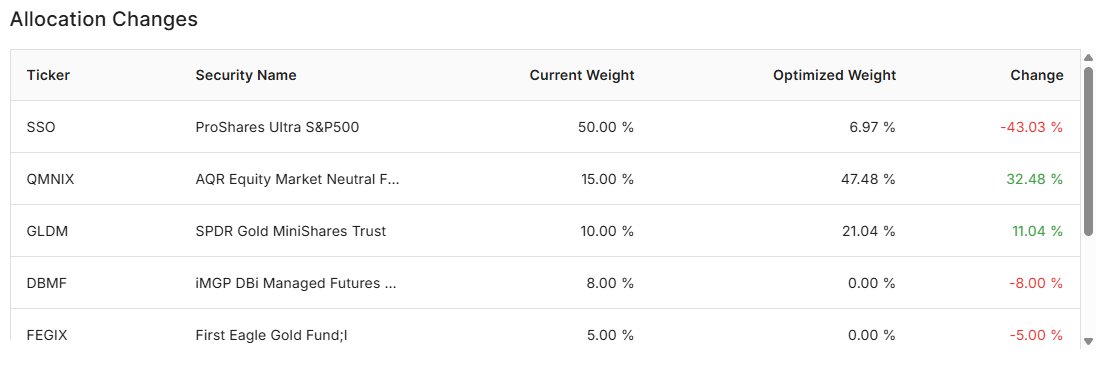

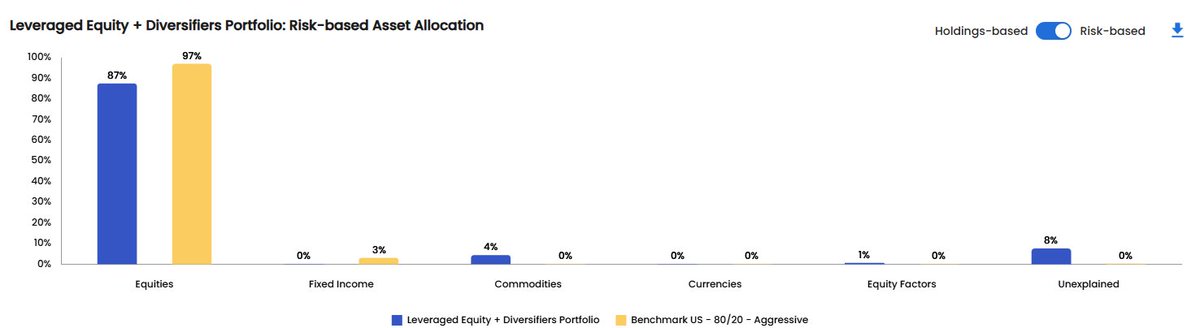

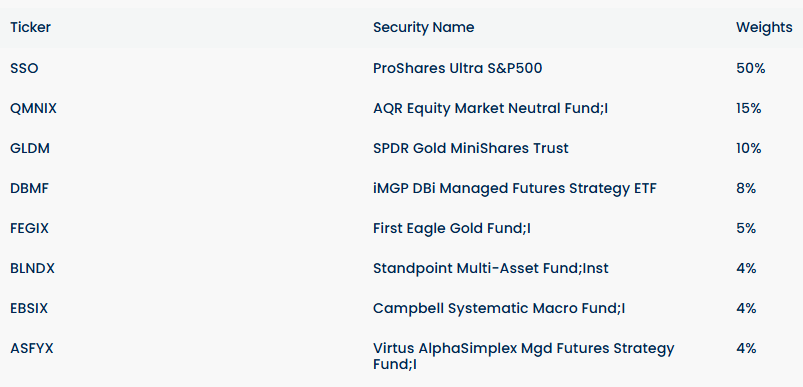

Portfolio Review: Leveraged Equity Diversifiers Portfolio. What are the current holdings?

This portfolio was sent by a client, who kindly agreed to our showcasing it. The portfolio aims to be an all-weather portfolio that uses leveraged equities to make more room for a higher allocation to diversifying strategies. It does not include bonds.

The largest allocation is to a 2x leveraged S&P 500 ETF (SSO, 50%), followed by the AQR Equity Market Neutral Fund (QMNIX, 15%) and gold (GLDM, 10%). The remaining funds mostly represent CTAs / managed futures funds. The portfolio is expensive at 0.93% pa.

finominal.com/portfolio-anal…

4

1

26

20,335

Can the portfolio be simplified? The portfolio comprises various uncorrelated strategies, such as equity market-neutral, gold, and managed futures, which makes portfolio simplification challenging. Naturally, the various managed futures funds could be replaced by a single fund, e.g., DBMF, which provides passive CTA exposure. However, investors could also consider allocating to funds such as Return Stacked US Stocks & Managed Futures ETF (RSST) and Standpoint Multi-Asset Fund (BLNDX), which provide equity and managed futures exposure in a single fund. However, RSST has no meaningful track record, and both are less diversified yet more expensive.

finominal.com/asset-comparer…

1

542

How does a Sharpe ratio-optimized version look?

Optimizing portfolios should be approached with caution, as out-of-sample results are typically far worse than in-sample results. However, optimization can be helpful in giving ideas for asset allocation. A simple, unconstrained Sharpe optimization would reallocate almost entirely away from the leveraged equities position (SSO) toward the equity market-neutral fund (QMNIX). Gold is preferable to gold miners; all managed futures funds would be allocated to the Campbell Systematic Macro Fund Class (EBSIX). Food for thought.

5

454

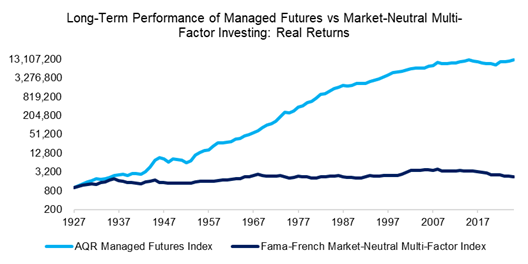

Managed Futures vs Factor Investing: A 100-Year Perspective. Rethinking traditional asset allocation.

insights.finominal.com/resea…

195

May 29

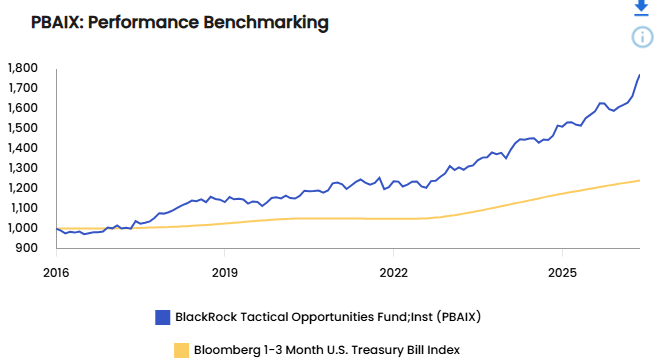

Product Review: BlackRock's $4bn Tactical Opportunities Fund (PBAIX).

What is the fund's strategy and performance?

PBAIX is a liquid alternative fund that aims to provide returns that are only weakly correlated with stocks and bonds. The fund can allocate long and short across asset classes and geographies. The fund has a track record dating back to 1993, but it changed to its current strategy in January 2016, so we will only analyze it from then onward.

The fund's factsheet takes U.S. T-Bills as the benchmark index, which is reasonable for an alternative fund, assuming it offers completely uncorrelated returns. PBAIX has outperformed its benchmark significantly since 2016.

finominal.com/fund-analyzer-…

1

239

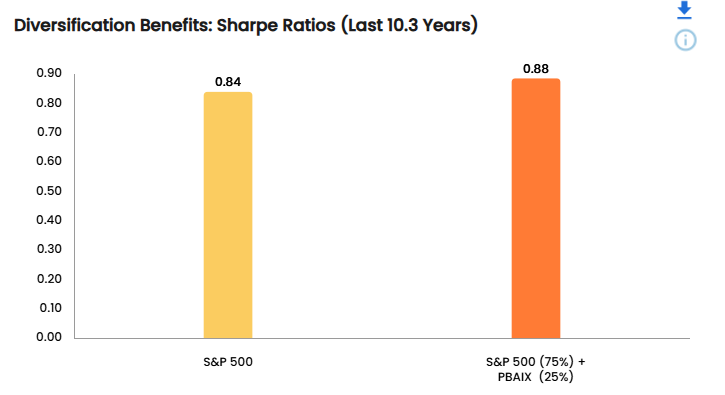

May 29

The fund has generated minor diversification benefits, as adding a 25% allocation to a portfolio comprised exclusively of the S&P 500 would have increased the Sharpe ratio from 0.84 to 0.88. Adding T-Bills would have generated a similar increase in risk-adjusted returns.

finominal.com/fund-analyzer-…

1

138

May 29

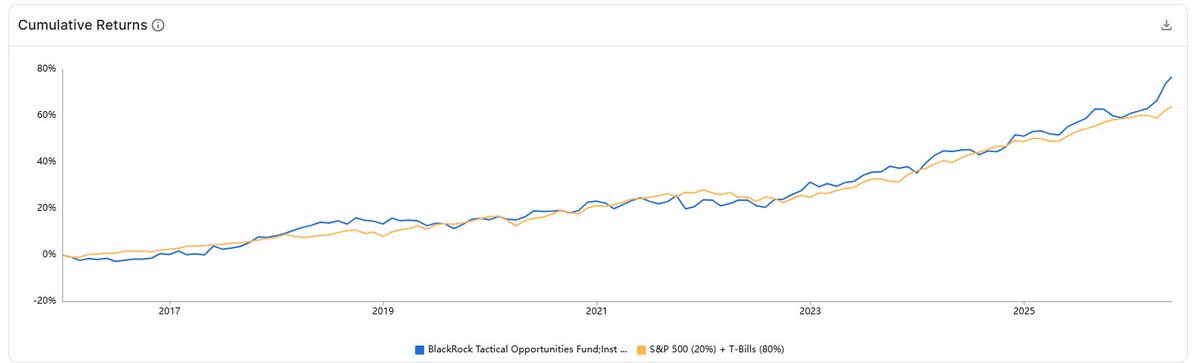

Can we replicate the fund? Given the tactical allocation strategy, a simple fund replication is challenging. However, we can create a better benchmark as the fund had a minor but consistent positive beta to the stock market. A combination of the S&P 500 (20%) and T-Bills (80%) would be more appropriate than only T-Bills. The return since 2016 would have been similar, but the benchmark had only half the volatility of PBAIX, thus generating a much higher Sharpe ratio.

finominal.com/asset-comparer…

123