Investor. Small cap asia, tech, monopolies, semi’s

Joined July 2022

- Tweets 1,335

- Following 396

- Followers 1,738

- Likes 2,134

271 Photos and videos

Pinned Tweet

15 Mar 2025

Thread of my ideas shared on this platform

12

9

6,340

Another Japanese cybersecurity stock:

Cyber Security Cloud $4493.

A ¥18B small-cap running Japan's leading web-application-firewall SaaS: Shadan-kun guards SME websites, while WafCharm uses AI and threat intelligence to automate the cloud WAFs running on AWS, Azure and GCP. It's ~90% recurring revenue with roughly 1% monthly churn — sticky subscription plumbing that sits in front of a customer's website and rarely gets ripped out. 66% gross margins, a 22% return on equity, and revenue still compounding at 42%, the fastest grower on my list.

This is the opposite end of the Trend Micro trade. Where Trend Micro is mature, cash-rich and pays you to wait, Cyber Security Cloud is small and all-growth: ¥18B buys the whole business, there's almost no net cash to hide behind (~¥455M), and you're paying ~21x forward earnings / ~13x EBITDA / ~3.4x sales. Flip the multiple and it's a ~5% earnings yield. A token ~0.3% dividend at a 6% payout tells you the character: cash gets plowed straight back into 40% growth.

Operating margins have compressed hard and trailing earnings fell sharply even as revenue surged — growth is being bought, not banked yet. Add small-cap liquidity and a thin balance-sheet cushion, and this is the higher-risk, higher-variance end of the theme.

5

619

Jun 13

Trend Micro $4704

¥766B global cybersecurity company, founded in Japan in 1988 and now one of the oldest pure-play security vendors in the world. It protects enterprise endpoints, servers, and hybrid-cloud workloads through subscription software (XDR, threat detection, cloud security) — the kind of mission-critical, contract-locked tooling that's deeply embedded in IT stacks and painful to rip out. The economics show it: 77% gross margins, a 34% return on equity, and earnings that grew 34.7% last year.

The reason it's interesting is the price. ¥766B buys the whole business, but ~¥229B of that — nearly a third of the market cap — is just net cash sitting in the till, with zero debt. Strip it out and you're paying an enterprise value of only ~¥537B for a global security platform: roughly 6.3x EBITDA and under 2x sales. Flip the ~20x forward earnings multiple and that's a ~5% earnings yield on a 34% ROE compounder — at a time when US cyber peers like CrowdStrike, Palo Alto and Zscaler trade north of 50x earnings. Shareholders are paid to wait, too: a ~3.1% dividend at a ~71% payout plus steady buybacks, a ~4.5% shareholder yield, all resting on a fortress balance sheet.

The catch is growth. Revenue at only ~9%, and the stock sits near its 52-week low (¥5,900 against a ¥10,935 high) as the market frets about share loss to faster-moving rivals and Microsoft's security bundling.

Not investment advice.

2

14

2,568

Jun 13

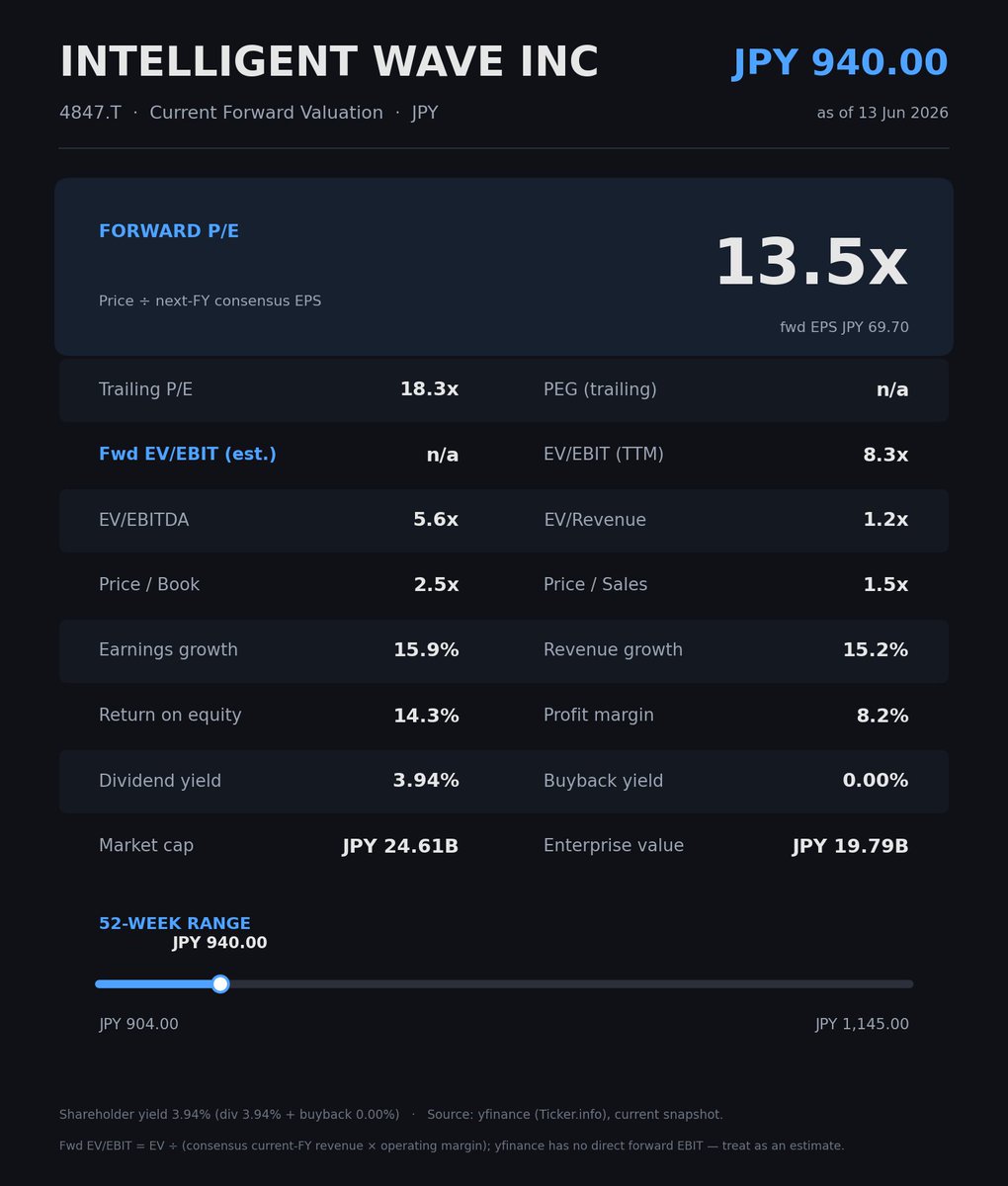

Intelligent Wave $4847

This ¥25B small-cap quietly runs ~70–80% of Japan's credit-card authorization processing — the invisible rails nearly every card transaction in the country clears through. Deeply embedded, high switching costs, recurring revenue. FY24 operating profit grew 30.5%, and management targets ¥30B sales by 2030 (~16% CAGR).

¥24.6B is the price for the whole business — and ~¥4.8B of that (≈20% of the market cap) is just net cash in the till, zero debt. Net it out and you're paying ~5.6x EBITDA / ~1.2x sales for the dominant payment rails of an entire country. Flip the 13.5x forward multiple and that's a ~7% earnings yield on a 14% ROE compounder — while comparable Japanese software names routinely sit north of 20x.

~3.9% dividend yield at a ~72% payout, no buybacks.

The watch-item is concentration: Japan-centric revenue and exposure to payment-tech shifts — the price of a small-cap that owns one country's plumbing rather than many.

Not investment advice.

1

6

626

Jun 12

keep in mind anytime a VC throws around a gen z slang its OFF LIMITS FROM THEN ON

167

Jun 11

Growth rate per capita / P/E of the listed Exchange

Poland and Greece are the standouts

1

4

472

Jun 11

$7735 SCREEN Holdings

While the crowd piles into the obvious semicap names, SCREEN controls ~80% of the global single-wafer cleaning market — an unglamorous but mission-critical step that scales with every new node and every HBM stack feeding AI demand. That dominance shows up in the numbers: ~26% operating margins, sticky customers, and recent quarterly sales of ¥183B ( 32% YoY). Yet it still trades around 14–15x forward earnings vs peers at 19–21x — a 20% ROE compounder riding the AI/memory capex wave at a discount.

On capital return: a conservative ~1.8% dividend at a steady ~30% payout — but the real lever is the ¥221B net-cash pile, reinvestment-led with room for opportunistic buybacks. You're paid to wait while it compounds, not for income.

The watch-item is China (~49% of semi revenue): equal parts opportunity and export-control risk. A best-in-class GARP setup in semis.

1

11

659

Jun 11

It's pretty incredible that we can create custom visuals of pretty much anything we could ever want

PLUG YOUR AGENT INTO FINANCIAL DATA

1

256

Jun 10

Hardest problem for small mid cap is a free news feed that actually sources good, relevant news

Jun 8

A Bloomberg Terminal costs $30,000 a year.

Someone just built one for free.

In minutes.

With no local setup.

1

479

Jun 10

The best opportunities I'm looking at in Japan & Korea:

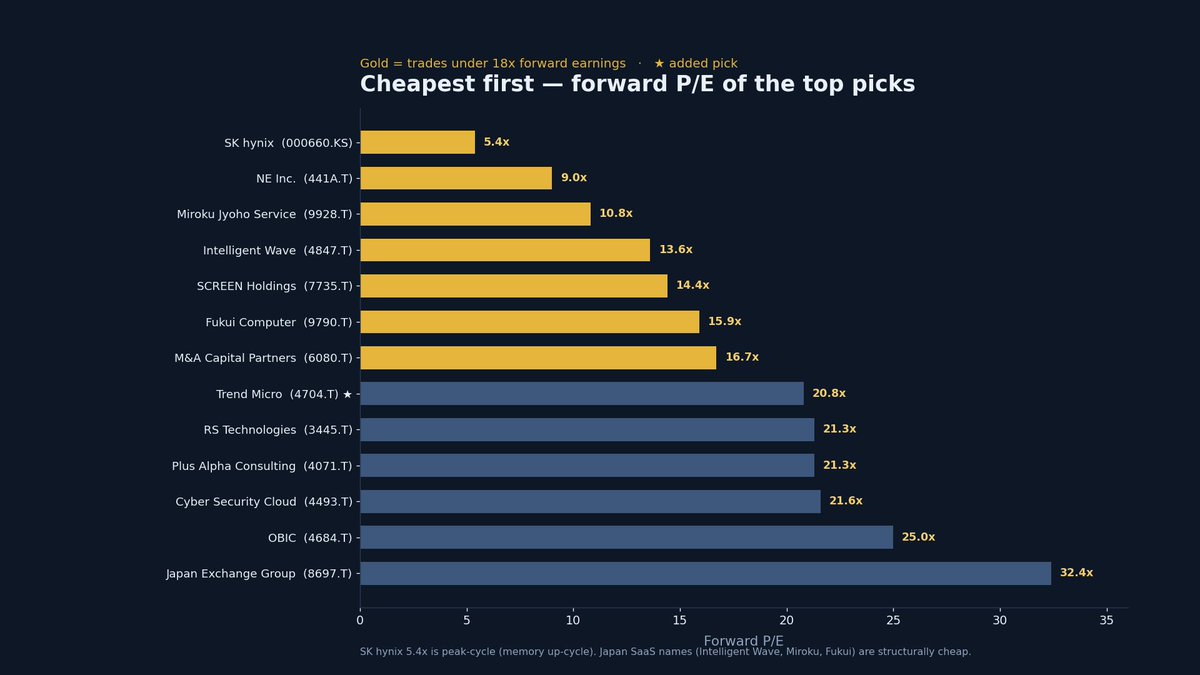

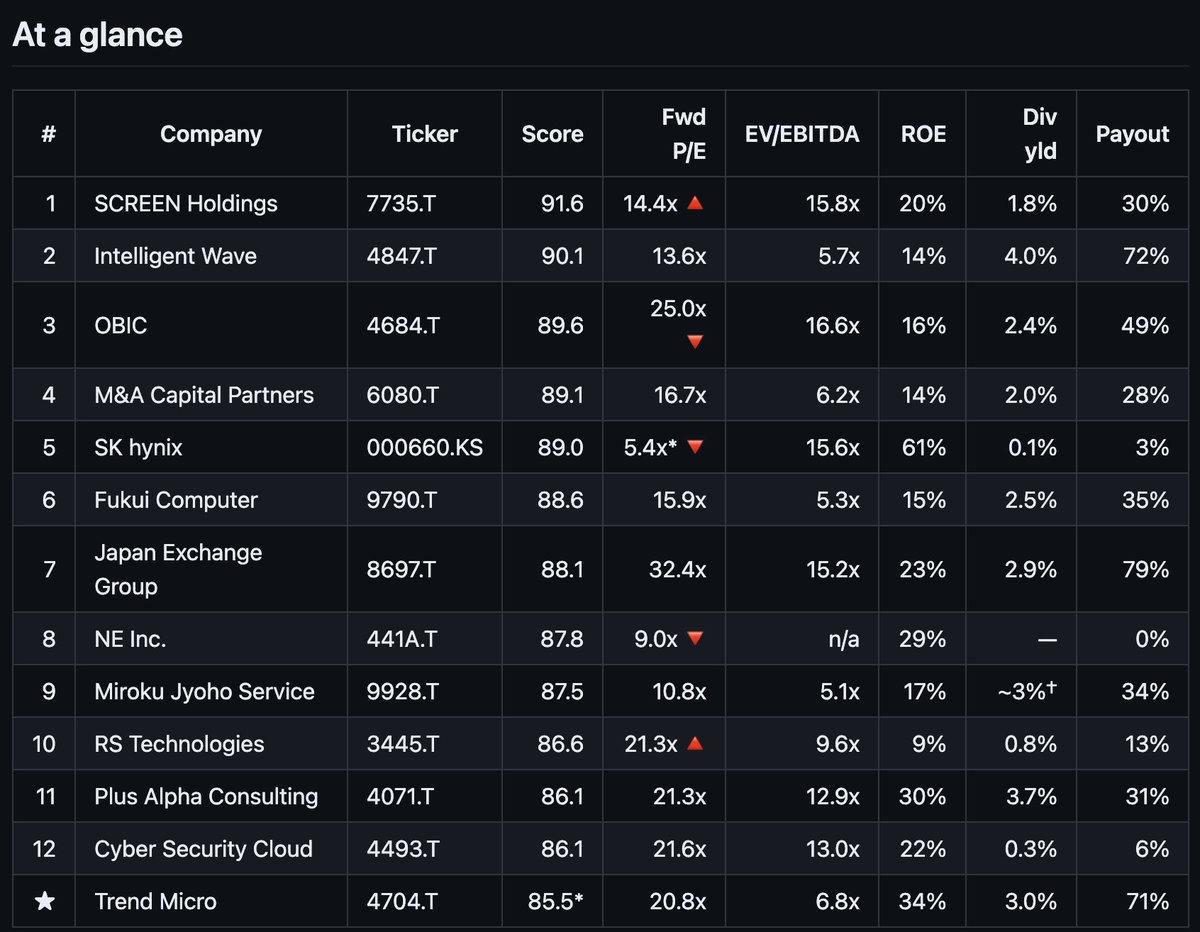

1. SCREEN Holdings (7735.T) — 91.6 · Semis Dominates single-wafer cleaning (~80% share), 26% op margins, riding the semicap up-cycle. Valuation: fwd P/E 14.4x · EV/EBITDA 15.8x · rev 9% · ROE 20% · net cash ¥221B. Re-rated 🔺 91% since pitch but still ~14x vs peers at 19-21x. Capital return: ~1.8% yield, conservative ~30% payout held steady through the cycle. The ¥221B net-cash pile is the real lever — funds room for opportunistic buybacks; reinvestment-led, not income.

2. Intelligent Wave (4847.T) — 90.1 · Software 70-80% share of Japan's credit-card authorization processing — sticky, non-bank payments infrastructure. Valuation: fwd P/E 13.6x · EV/EBITDA 5.7x · rev 15% · ROE 14% · net cash ¥4.8B. Cheap on both metrics; no re-rating. Capital return: income-style — ~4.0% yield on a high ~72% payout. Returns most of earnings as dividends; you get paid well to hold while it compounds.

3. OBIC (4684.T) — 89.6 · IT Services #1 ERP for Japanese SMEs (~30% share), 63% operating margin, 99% retention, fortress balance sheet, cloud optionality. Valuation: fwd P/E 25.0x · EV/EBITDA 16.6x · rev 11% · ROE 16% · net cash ¥207B. Re-rated 🔻 -26% — cheaper entry on a premium compounder. Capital return: ~2.4% yield, steadily rising dividend at ~50% payout. The ¥207B net cash is famously under-deployed — the bull case includes management finally returning more (buybacks / higher payout) under TSE governance pressure.

4. M&A Capital Partners (6080.T) — 89.1 · Capital Markets #1 domestic M&A intermediary for Japan's SME-succession wave. Asset-light, 81.5% equity ratio, zero long-term debt. Valuation: fwd P/E 16.7x · EV/EBITDA 6.2x · rev 82% · ROE 14% · net cash ¥44.8B. Capital return: ~2.0% yield, low ~28% payout — earnings mostly retained to fund the growing deal pipeline. Asset-light model throws off cash; return is via growth a modest, growing dividend.

5. SK hynix (000660.KS) — 89.0 · Semis HBM memory leader (MR-MUF packaging edge) with real pricing power on AI-driven, contractual demand; 60-70% HBM gross margins. Valuation: fwd P/E 5.4x · EV/EBITDA 15.6x · rev 198% · ROE 61% · net cash ₩32.5T. The 5.4x is on peak-cycle earnings — cyclical cheapness, not structural. Capital return: token ~0.1% yield, ~3% payout — cash is consumed by HBM capex. Policy is a fixed annual dividend floor (₩1,200/sh) plus cyclical top-ups. Buy this for the cycle, not the cheque.

6. Fukui Computer (9790.T) — 88.6 · Software Regional near-monopoly in construction CAD/software, 25% op margins, 70% recurring revenue, 18-22% 3yr CAGR. Valuation: fwd P/E 15.9x · EV/EBITDA 5.3x · rev 26% · ROE 15% · net cash ¥24.1B. One of the cleanest cheap-quality names here. Capital return: ~2.5% yield, ~35% payout — steady, well-covered dividend backed by recurring revenue and net cash. Balanced reinvest-and-pay profile.

7. Japan Exchange Group (8697.T) — 88.1 · Capital Markets Monopoly operator of the Tokyo & Osaka exchanges — the quintessential toll-road / market-infrastructure moat. Valuation: fwd P/E 32.4x · EV/EBITDA 15.2x · rev 45% · ROE 23% · net cash ¥58.0B. Best-in-class moat, but priced for it. Capital return: dividend-led — ~2.9% yield on a high ~80% payout. Capital-light monopoly returns the bulk of profit; progressive dividend policy. The reliability is the point.

8. NE Inc. (441A.T) — 87.8 · Software Japan's dominant e-commerce order-management hub (~33% share, 6,570 merchants), 40% EBIT margin, 110% ROIC, <1% monthly churn. Valuation: P/E 9.0x (ttm) · ROE 29% · net cash ¥3.0B. Re-rated 🔻 -26%; screens very cheap for the quality (small-cap, ¥8.7B mcap). Capital return: no dividend yet — recent IPO retaining 100% to reinvest at 110% ROIC. Return is pure compounding for now; a payout could initiate as growth matures. Watch for first dividend as a re-rating catalyst.

9. Miroku Jyoho Service (9928.T) — 87.5 · Software ~30% share of accounting-firm ERP, 99% renewal rates, capital-light, cloud transition lifting ARR ( 35%). Valuation: fwd P/E 10.8x · EV/EBITDA 5.1x · rev 9% · ROE 17% · net cash ¥8.9B. Cheap on a 99%-renewal recurring base. Capital return: shareholder-friendly — ~34% base payout topped up with special dividends (which inflate the trailing yield to ~7%). Recurring cash funds a generous, growing distribution. Normalize the yield to ~3% for planning.

10. RS Technologies (3445.T) — 86.6 · Semis Global leader in wafer reclaiming (~33% share), ~10x sales growth in a decade, less cyclical than prime wafers. Valuation: fwd P/E 21.3x · EV/EBITDA 9.6x · rev 9% · ROE 9% · net cash ¥80.6B. Re-rated 🔺 44% — less of a bargain, still reasonable. Capital return: low ~0.8% yield, ~13-30% target payout — cash is reinvested into wafer-reclaim capacity expansion. Growth-first; the dividend is a token, not the thesis.

11. Plus Alpha Consulting (4071.T) — 86.1 · Software Enterprise HR-SaaS leader (Talent Palette), ~50% margins, high switching costs from 6,000 features, ~20% CAGR. Valuation: fwd P/E 21.3x · EV/EBITDA 12.9x · rev 14% · ROE 30% · net cash ¥15.5B. Premium multiple justified by the ROE and stickiness. Capital return: ~3.7% yield, ~31% payout, plus an initiated ~6% buyback. Founder owns ~40% — interests aligned, and the buyback signals confidence. Dividend repurchase combo.

12. Cyber Security Cloud (4493.T) — 86.1 · Software WAF SaaS (Shadan-kun / WafCharm), 90% recurring, ~1% monthly churn, 6 straight years of 25% revenue & op-profit growth. Valuation: fwd P/E 21.6x · EV/EBITDA 13.0x · rev 42% · ROE 22% · net cash ¥455M. Fastest grower in the group (small-cap, ¥18.2B). Capital return: minimal ~0.3% yield, ~6% payout, plus a ¥450M buyback. Cash reinvested into 40% growth — return is overwhelmingly via compounding, with the buyback a small capital-discipline signal.

★ Trend Micro (4704.T) — 85.5* · Software (Cybersecurity) Global cybersecurity leader (endpoint, cloud, network security) with deep enterprise installed base and recurring subscription revenue. Valuation: fwd P/E 20.8x · EV/EBITDA 6.8x · rev 9% · ROE 34% · op margin 21% · net cash ¥229B (zero debt). The 6.8x EV/EBITDA 34% ROE net cash is the standout — much cheaper on cash-flow than the P/E suggests. Added pick; score estimated, not from the original screen. Capital return: dividend-led — ~3.0% yield on a generous ~71% payout, supplemented by periodic buybacks. Mature, cash-generative model that returns the bulk of earnings while still growing. Strongest income profile of the cybersecurity names here.

1

3

7

1,164

Jun 10

I have to say, Fable can write pretty good investment research BUT you have to plug it in to live financials for it to produce accurate financials

x.com/FirstHillcap/status/20…

2

1

629

i fear the substack notes feed is turning into Linkedin

if it hasn't already

3

303

119850.K

META

005935

Kioxia

8299.TW

All interesting

Whenver firsthill says interesting I look

2

8

1,830

Someone find those WSB edits of the ape army

114

AI still can't make investment decisions but it is very good at finding specific ideas and lookalike companies - the kind of stuff that takes forever like going A-Z. If you can just make good decisions I think a lot of the hard work is over, esp as models get better.

Going A-Z through an exchange for ideas could not be a better LLM task - Synthesize a large data set where the cost of a few errors is meaningless.

Can even load Claude code with up to date financial data for every stock.

Any one else working on this and getting good results?

1

1

1

343

$GPW was top of my list for anyone hunting under a $1b market cap. cheap PE, plenty of growth, untapped upside in data sales in a growing economy.

has a public stock exchange ever gone bankrupt?

(not as cheap as it was now)

1

286

wrote this one up a while back. a japanese company with a $531m market cap sitting on $520m of cash and $800m of marketable securities.

yes those numbers were right. and they returned cash to shareholders.

rerated a lot since

331

Li Lu on how to invest under $100k:

interesting one, in Korea there's a form of securities called preferred securities. basically non voting common stock that pay a slightly higher dividend. not much more, but no voting rights.

cheap way to own the same business

1

1

480

You can borrow at 1.8% per year to buy a Japanese company that pays you 8% per year.

Costs you nothing

4

13

2,294