Joined August 2021

- Tweets 1,858

- Following 3,572

- Followers 478

- Likes 3,721

90 Photos and videos

3 Nov 2023

Scam Bankman-Fraud

2 Nov 2023

JUST IN: Sam Bankman-Fried officially found guilty on all seven charges.

30

FlowLambo ❤️ Memecoin retweeted

1 Nov 2023

POWELL SPEECH SUMMARY⚠️

1. The Fed decided to keep rates unchanged and to continue quantitative tightening (QT) at the same pace.

2. The Fed are not confident that policy is restrictive enough and are prepared to raise interest rates further if they aren’t happy with progress. However, they are proceeding carefully by pausing as they believe they have time to do so. The committee is NOT thinking about rate cuts at present. Powell emphasised that their current question is HOW high they are going and then the next question will be how long to stay there.

3. Powell iterated that the current stance of policy is restrictive, which he clarified means policy is putting downward pressure on economic activity and inflation.

4. He acknowledged that the risks of doing too much vs too little have become more two sided.

5. Inflation is well above target, but progress has been made. However, he noted that a few months of good data is not enough to convince them they are confidently getting toward target.

6. The Fed believes below trend growth is likely needed to get to target. He commented on the current strong pace of GDP growth, driven by robust consumer spending. He admitted The Fed may have underestimated the strength of household balance sheets following the pandemic.

7. GDP growth is forecasted to slow

8. Below trend growth (which he estimated to be around 2%) and softening of labor market is needed to get to target. Labor market remains tight but coming into better balance. Wage growth has shown some signs of easing to a pace closer to being consistent with their 2% target. They feel gratified that they have managed to see some good progress on inflation without significant job losses so far.

9. When asked about bond yields and their effect on monetary policy he stated that higher bond yields need to be persistent to have an effect on monetary policy stance. They can’t be as a result of market expectations of Fed interest rate decisions. The current rise in yields, if sustained, is going to have a negative impulse on economic activity. However, Powell was not comfortable estimating the equivalent rate hike effect that recent rises in bond yields will have.

10. Powell stated that Fed staff didn’t put a recession back as their baseline projection.

11. He acknowledged that inflation is painful for people, particularly for those with less disposable income.

12. Commented again about the uncertainty of lags of monetary policy changes. Stated It has been 1 year since last 75bps hike. He feels they are seeing the effects of the hikes seen last year. However, it’s hard to say how much. He noted part of implementing monetary policy is knowing there is significant uncertainty and that it takes time to see the effect.

13. He was asked about whether the projections from the dot plot still stood. He responded saying that when things change so do the Fed’s forecast and opinions and generally the further time goes on from the last dot plot the more things change. He also noted that the dot plot is not a policy promise.

• Essentially saying their previous projections have changed from September and thus their actions do not need to be in keeping with previous projections.

14. Fed are watching banking stress. They have been working with institutions so they have a plan for their unrealized losses. They don’t feel that rate hikes are worsening the picture for banks at present.

15. The Fed haven’t been thinking about extending the Bank Term Funding Program as of yet; they’ll make a decision in Q1 2024.

23

128

593

129,654

FlowLambo ❤️ Memecoin retweeted

1 Nov 2023

Get ready for the ultimate football collectible 🔷

99 carbon fibered beauties engineered for speed and lightness - the @adidas 'X Crazyfast' @Bugatti.

⌛ Auction starts November 8, 4PM CET

⚽ Benefits for ALTS Strikes

💳 Fiat on-ramp enabled by @Moonpay

🔌 Powered by adidas Collect

Learn more about the incoming auction via collect.adidas.com/bugatti. 💙🖤

35

97

268

36,996

FlowLambo ❤️ Memecoin retweeted

1 Nov 2023

Workers with in-person jobs spend about $51 a day that they wouldn't remotely, per USA Today.

364

990

7,287

1,574,600

31 Oct 2023

Hi, my name is @FlowLambo, and I’m a $MEME (@Memecoin) farmer at @Memeland.

On my honor, I promise that I will do my best to do my duty to my own bag, and to farm #MEMEPOINTS at all times.

It ain’t much, but it’s honest work. 🧑🌾

13

FlowLambo ❤️ Memecoin retweeted

29 Oct 2023

matthew perry has sadly passed away at the age of 54.. rest in peace.

1,909

65,785

278,552

24,022,386

FlowLambo ❤️ Memecoin retweeted

27 Oct 2023

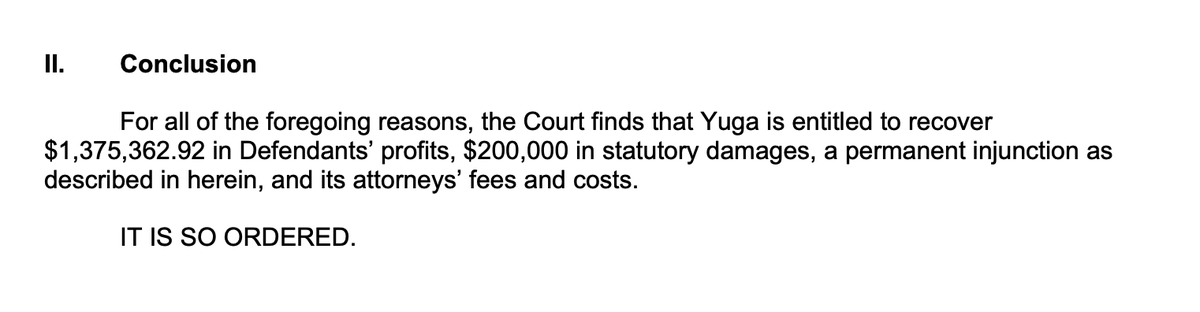

$1.5m legal fees and another $100k for our anti-SLAPP of all their bullshit. Bad day to be a scammer. Good day to be an ape.

Appreciate the note from the judge on how absurd this has all been:

“In addition, Defendants unnecessarily and inappropriately made disgraceful and slanderous statements about Yuga, its founders, and its counsel during litigation, including calling Yuga’s counsel “criminals” who support “racism, antisemitism, beastiality, pedophilia” and accusing them of “using cartoons to market drugs to young children.” These statements were egregious and far exceed the bounds of acceptable conduct.”

26 Oct 2023

BREAKING: Ryder Ripps and Pauly ordered to pay Yuga Labs over 1.5 Million Dollars in damages. They also must transfer control of the RR/BAYC smart contract to Yuga.

510

1,253

2,592

717,291

FlowLambo ❤️ Memecoin retweeted

26 Oct 2023

JUST IN: The S&P 500 has officially erased $4 trillion in market value since its July 27th high.

In 3 months, the S&P 500 has dropped 430 points and stands less than 1% away from correction territory.

The exact top in the S&P 500 came on the same day that Fed removed a recession from their forecast.

As markets fall to their lowest levels since May 2023, we are in a much different environment.

Last time the S&P 500 was at current levels, 3 rate CUTS were priced-in for 2023.

Now, rates are higher and futures are no longer showing rate cuts until July 2024.

Are stocks pricing-in a recession?

115

704

3,059

669,445

My brothers in bitcoin:

I spent six years managing new ETF launches for NYSE (2010-2016), and about 15 years in ETF product development and management.

The DTCC thing means absolutely nothing. Nothing. Get offline and spend time with your loved ones.

171

247

1,997

598,338

FlowLambo ❤️ Memecoin retweeted

24 Oct 2023

Drake hired Aaron Paul and Bryan Cranston from "Breaking Bad” to work as bartenders at his birthday party

Community note

While it is true that Aaron Paul and Bryan Cranston were present at Drake's birthday making some drinks to promote their Mezcal alcohol "Dos Hombres" collaboration, there is no evidence ANYWHERE that the stars were paid/hired to serve drinks as the event's bartenders.

insider.com/drake-breaking…

wsvn.com/entertainment/…

people.com/drake-37th-bir…

1,776

14,107

204,475

26,683,294

FlowLambo ❤️ Memecoin retweeted

24 Oct 2023

NEW: DTCC (DEPOSITORY TRUST & CLEARING CORPORATION) WEBSITE IS BACK ONLINE - @BlackRock'S ISHARES $BTC TRUST ($IBTC) IS STILL MISSING FROM THE ETF LIST

11

16

69

12,387

FlowLambo ❤️ Memecoin retweeted

24 Oct 2023

> Leak the ticker

> liquidate the shorts

> get them hyped

> remove the ticker

> liq the longs

> get all of em to re-short

> load up cheap again

> pump it again

Nothing personal kid.

248

892

5,920

880,935

FlowLambo ❤️ Memecoin retweeted

23 Oct 2023

Boomers selling their homes for $2 million after buying them in 1969 for 7 raspberries x.com/twesq/status/163140667…

765

16,793

132,788

9,540,203

EVERYTHING IMPORTANT THAT IS HAPPENING THIS WEEK ( ALL TIMES IN ET )

MONDAY

NOTHING REALLY

TUESDAY

4:00 PM GOOGLE EARNINGS 💰

4:05 PM MICROSOFT EARNINGS 💰

4:05 PM VISA EARNINGS 💰

4:10 PM SNAPCHAT EARNINGS 💰

WEDNESDAY

7:30 AM BOEING EARNINGS 💰

10:00 AM BANK OF CANADA RATE DECISION 🇨🇦

10:00 AM NEW HOME SALES 🇺🇸

4:05 PM FACEBOOK EARNINGS 💰

4:35 PM JEROME POWELL SPEECH 🇺🇸

THURSDAY

8:00 AM MASTERCARD EARNINGS 💰

8:15 AM ECB RATE DECISION 🇪🇺

8:30 AM Q3 GDP NUMBERS 🇺🇸

4:00 PM AMAZON EARNINGS 💰

4:00 PM INTEL EARNINGS 💰

FRIDAY

6:15 AM CHEVRON EARNINGS 💰

6:30 AM EXXON MOBIL EARNINGS 💰

8:30 AM PERSONAL SPENDING DATA 🇺🇸

10:00 AM CONSUMER SENTIMENT 🇺🇸

100

373

2,421

490,081

FlowLambo ❤️ Memecoin retweeted

21 Oct 2023

Another incredible week in AI!

DALL·E 3

Open AI

Google

Amazon

Microsoft

ChatGPT

Baidu

Anthropic

Now, here's what you need to know:

43

44

340

125,361

FlowLambo ❤️ Memecoin retweeted

19 Oct 2023

Elon Musk said on the $TSLA earnings call, per Reuters:

How detached from reality does the work-from-home crowd have to be while they take advantage of those who cannot work from home.

454

259

3,754

1,164,724