Joined April 2017

- Tweets 3,671

- Following 172

- Followers 7,152

- Likes 7,761

498 Photos and videos

Pinned Tweet

24 Jan 2022

Thread on all the companies investigated upon on the French Hidden Champions substack. Will add to it as new companies are analyzed.

1/ Precia

frenchhiddenchampions.substa…

4

11

75

Never ever forget.

Jun 5

90% of the soldiers on the first boats to hit the beach didn't live to see the end of the day. Look at those faces. Some of them never made it to 18.

Never forget that they paid the ultimate price for our freedom. We live our lives the way we do because of them.

1

3

31

1,827

Help Andy get his account back.

@X

Apr 20

@evfcfaddict got hacked and is having trouble getting help from @X.

Be extra careful about which links you click on. #helpandy

1

3

1,407

FFH.TO a very interesting recap of the AGM. Great read.

Apr 18

Some quick observations on the Fairfax AGM $FFH.TO. While it’s painful to travel from Australia to get there, the availability of management before and after the meeting combined with hanging out with the amazing shareholders makes the trip a must.

No great revelations regarding the numbers this year, but the trip was rewarding in handicapping the tails on the thesis.

Left Tail Compression

1/ Prem was beaming. He was doing the rounds before the AGM and dropped by the Meadow Foods stand while I was there. Big smile, handshakes all round. Healthy, happy, engaged, and no doubt enjoying “the plan coming together”. If Thursday was anything to go by he will be around for years to come.

2/ Succession is deep and real, not theoretical. Peter Clarke ran half the AGM presentation. Brian Young ramping at the insurance group. Wade Burton confirmed as investment succession.

3/ Cats. 1-in-250 PML of $3.5B now fits inside $4B of annual earnings. Peter Clarke confirmed this is the first time in Fairfax’s history. A big cat costs a year of earnings, not capital.

4/ Reserves holding. 19 consecutive years of favorable development. 2.9 points favorable in 2025 alone. The rumours from the dark corners of the internet of skeletons in the closet remain just that.

5/ No top-line incentive. Prem and Brian Young both explicit at the AGM. No Fairfax company is compensated for premium growth. Everything is bottom-line. Structurally immunizes against the classic soft-market blowup. Pencil sharpeners for all and an explicit job security message to boot.

6/ Liquidity stack is substantial. $2.7B holdco cash and investments. $2B undrawn credit facility. No near-term debt maturities for three years. The 2008 replay has a ready buyer, not a forced seller.

7/ Fixed income conservatively placed but ready to move at scale and speed when opportunity presents. Kleven Sava alongside Brian Bradstreet fielding questions post-AGM was great to see.

Right Tail Expansion

8/ $5B operating income run-rate with 3-4 year visibility. $2.5B interest and dividend, $1.5B underwriting, $1B associates. Around $150 EPS pre-gains. First time management has put a hard floor on the number.

9/ Float is $40B, around $2,000 per share, compounded at 18% since inception. Cost-of-float has been negative 4.5% over five years. Fairfax is paid to hold the float. That is the engine.

10/ Crystallization is active. Poseidon half-sold at $28.30 for $865M pretax gain. Excess fair value on associates now $4.2B pretax, around $200 per share. A decent chunk of dry powder just became available.

11/ International scaling is real. Bright (South Africa) 20%, Colonnade 18%, Asia 15%, Polish Re 15%. The $6B international premium base is now larger than all of Fairfax 15 years ago.

12/ Decentralization let Fairfax double premium from 2016 to 2022 almost entirely organically. 26 companies on the ground. Each independently doubled into the hard market. When the next hard market arrives, the structure is larger, geographically diversified, and the runway longer.

As I said at the outset no major revelations but the trip was worth it just to shrink my view of the left tail.

11

2,600

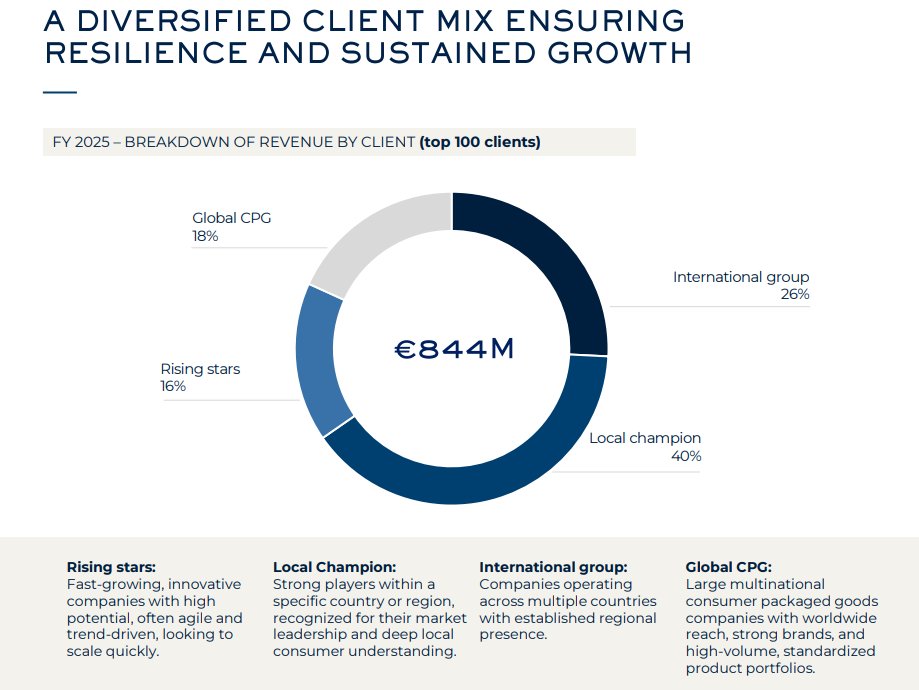

Robertet: the interesting slide!

Rising stars!

23

2,174

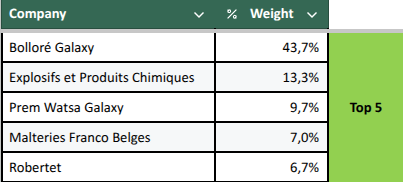

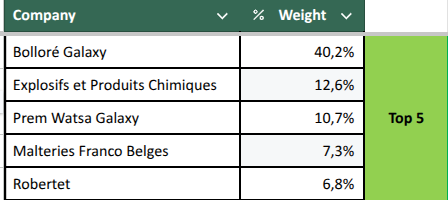

Still my top 5. Represents 80,5% of the portfolio. Usually markets go down after I post this.

What is yours?

11

2

61

14,922

Bill Ackman through Pershing wants to buy UMG at 30,4 € per share.

To be followed!

6

38

7,593

Good moves by Bolloré! Remember they got 99 M shares at 5,75€ 0,25€ with the 2023 tender offer. Now in 5 days they already got 26,5 M at 4,82€ and they are probably still buying! Massive move

Hier et aujourd’hui deux belles déclarations d’achat d’Odet sur BOL.

Aujourd’hui au prix max de 4,86€.

1

28

3,131

Odet for Vincent Bolloré.

Bolloré for Cyrille Bolloré.

Havas for Yannick Bolloré.

Each would have their investment vehicule.

I am probably wrong!

2

14

2,401

Well it seems Bolloré is hitting hard with buybacks great move! It looks looks like a tender but it is not a tender!!

If I were Bolloré (which I am not!) I would keep buying Bolloré and Odet shares especially as I benefit from the mother daughter tax regime so tax leakage will be very low with the exceptionnal dividend.

The joy of the self controlling loops!

What goes around come around!!

1

19

2,939

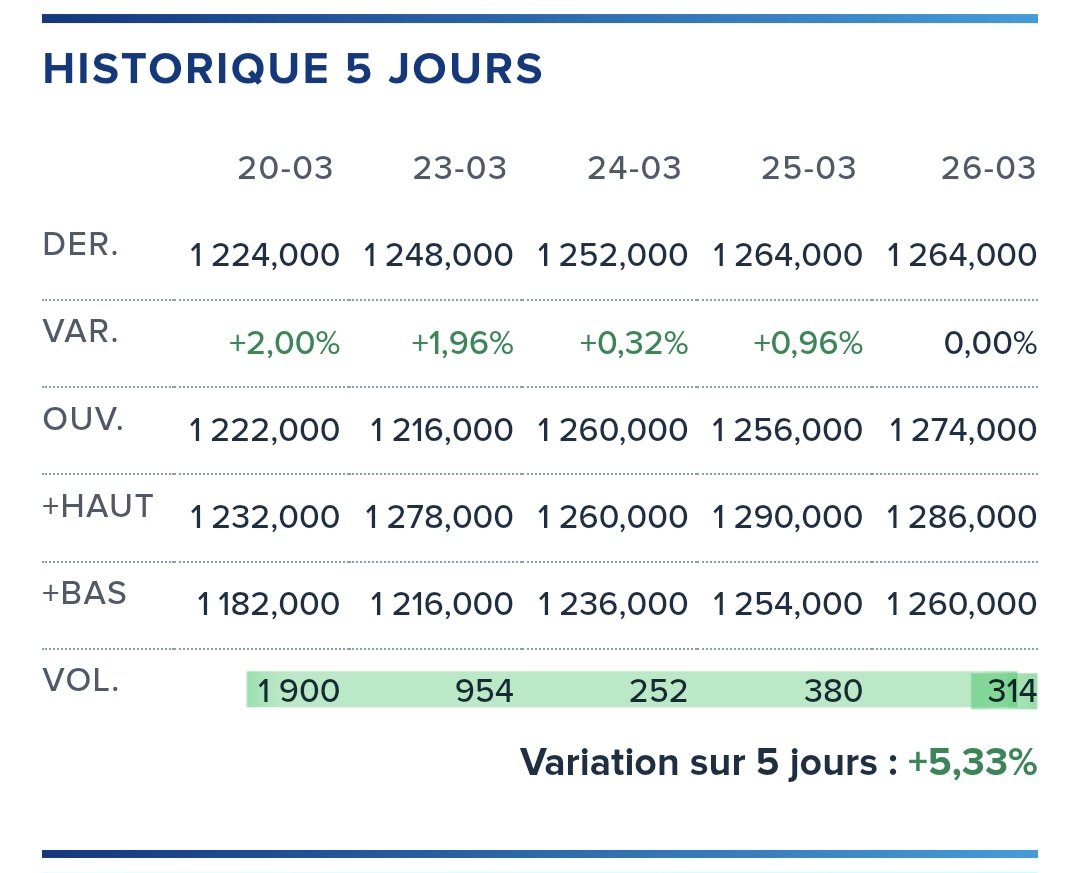

Bolloré volumes last 5 days.

The 20/03 is linked to options but still think we will see some multiple buys by Odet.

Sofibol will take care of the Odet buys.

1

1

17

1,355

Bolloré galaxy: Sofibol buying Odet (282 shares at 1195€ on average) and Odet buying Bolloré (591 323shares at 4,76€) on the 19th of march.

If I were Bolloré (which I am not!) I would just buy as many as I could especially as they benefit from the mother daughter tax regime.

1

2

20

3,254