Joined June 2017

- Tweets 2,024

- Following 274

- Followers 161

- Likes 1,064

1,069 Photos and videos

FRAGMENTS Value retweeted

We just published our Deep Value Report on Kohl’s ($KSS).

What pulled us in was not a pretty retail story.

It was the gap between the stock price and what still sits inside the company.

Kohl’s still owns hundreds of stores. It still has inventory, logistics assets, credit-card economics, and a customer file.

And in 2022, buyers were looking at the same company at prices far above today’s stock — including a reported $64/share offer from Acacia / Starboard.

We rebuilt the file in today’s dollars.

Here:cundilldeepvalue.substack.co…

1

1

1

352

FRAGMENTS Value retweeted

Deep Value Report — Petco Health and Wellness Co. ($WOOF)

Petco came public again at $18 in 2021. It was bought for roughly $4.6B in 2015. It was taken private at $29/share in 2006.

Today, the stock is around $3.

Those are not targets. They show the de-rating.

Here:cundilldeepvalue.substack.co…

1

58

Deep Value Report — Fubo ($FUBO)

Old Fubo was easy to pass on.

Good product. Brutal economics.

After Disney, the stock changed: Hulu Live TV, ESPN adjacency, Disney advertising, NBCU, and a public minority structure the market still discounts heavily.

The report is about whether that discount is too high.

Here:cundilldeepvalue.substack.co…

1

1

138

FRAGMENTS Value retweeted

Goodyear ($GT) trades around 0.6x book value.

That’s the easy part.

The harder part is figuring out what actually reaches the common shareholder.

Goodyear has real assets: roughly $7.6B of current assets, $3.9B of inventory, $2.6B of receivables, and a global tire footprint.

It has also already sold real assets. OTR, Dunlop and Chemical generated about $2.2B of gross proceeds. Buyers paid real money.

But the remaining company still has to prove the cash flow.

That is the work inside our full Deep Value Report.

Live now.

Here:cundilldeepvalue.substack.co…

1

1

125

FRAGMENTS Value retweeted

Jun 13

Cracker Barrel is a weird business. $CBRL

The old stuff is not just decoration. The porch, the store, the walls, the clutter — that is part of what people are buying.

Julie Felss Masino tried to move the company forward.

The customer reminded her what could not be moved.

CEO Series, Saturday.

Here:cundilldeepvalue.substack.co…

1

1

80

Jun 13

Cracker Barrel is a weird business. $CBRL

The old stuff is not just decoration. The porch, the store, the walls, the clutter — that is part of what people are buying.

Julie Felss Masino tried to move the company forward.

The customer reminded her what could not be moved.

CEO Series, Saturday.

Here:cundilldeepvalue.substack.co…

1

1

80

FRAGMENTS Value retweeted

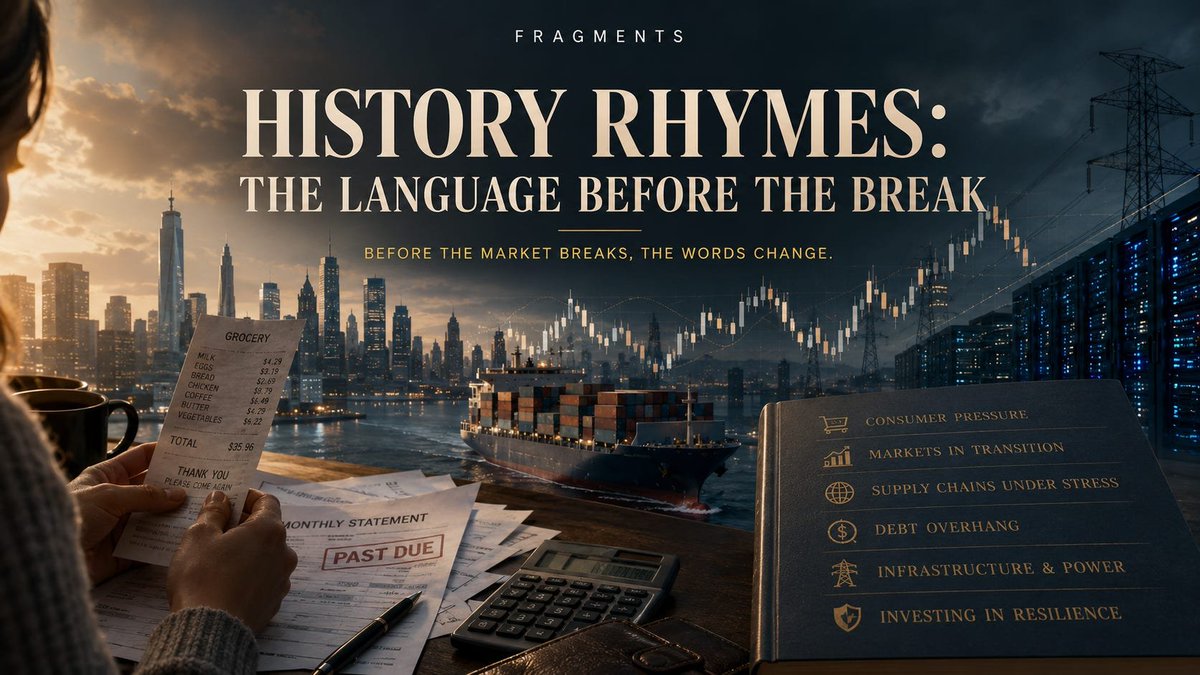

Jun 14

History Rhymes: The Language Before the Break

Burry, Marks, Klarman, Buffett, Templeton — different investors, different periods, same basic discipline:

they did not need the perfect macro forecast.

They needed price, patience, liquidity, and a balance sheet that gave them time.

Read it on FRAGMENTS. $NVDA

Here:cundilldeepvalue.substack.co…

1

1

77

Deep Value Report — Fubo ($FUBO)

Before Disney, Fubo was an easy pass.

Real product. Real audience. Brutal live-TV economics.

After Hulu Live TV, the stock is no longer just a small sports streamer.

It is now a public minority interest inside a Disney-controlled live-TV platform.

Different problem. Different math.

Here:cundilldeepvalue.substack.co…

2

9

939

FRAGMENTS Value retweeted

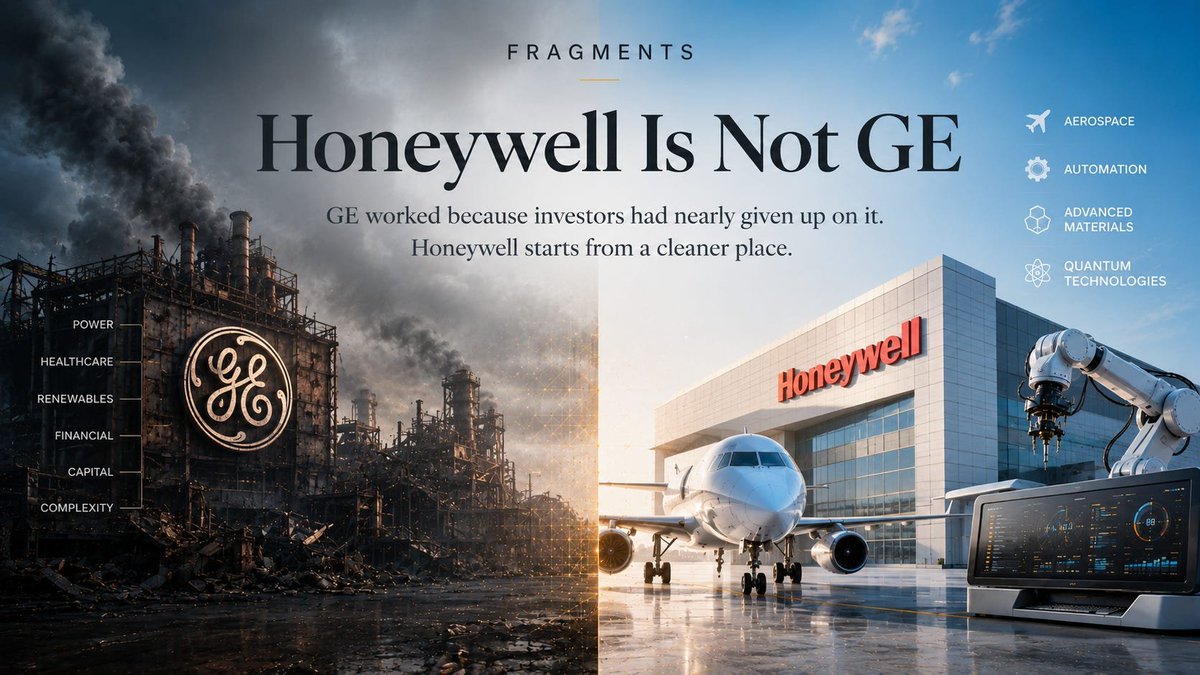

Honeywell Is Not GE

GE did not work because “breakups create value.”

GE worked because the old GE had years of mistrust inside the price. Larry Culp cleaned up the wrapper, then Vernova changed category when the market started caring about electricity again.

Honeywell is different.

Everyone already knows the assets are good.

$GE $HON

Here:cundilldeepvalue.substack.co…

1

1

186

FRAGMENTS Value retweeted

Jun 11

Top Aces: The Company Selling a Believable Enemy

We published this Shadow Builder a few weeks ago.

Now Top Aces just announced an agreement to acquire Select Global International, a Canadian company focused on simulator-based fighter pilot instruction for the RCAF.

That matters.

The article was not really about private F-16s. That was the visible part.

The bigger story was that Top Aces was becoming a private layer inside military readiness: live adversary flying, former fighter pilots, realism, repetition, and training capacity that air forces increasingly need but do not always want to build entirely on their own.

This new SGI deal fits that idea almost too well.

SGI brings simulator-based fighter pilot instruction and former CF-18 instructor pilots. Top Aces brings more than two decades of live-fly operational training.

Put them together and you are no longer just looking at a company flying against air forces in the sky.

You are looking at a company moving closer to the full training environment around the pilot.

Live aircraft. Simulators. Synthetic training. Former military instructors. Canada preparing for fifth-generation airpower.

That is why I wrote about Top Aces.

Not because the jets look cool.

Because the company shows how military readiness is being rebuilt below the headline level — through private infrastructure, specialized training, and people who understand what real air combat preparation requires.

Top Aces sells a believable enemy.

With SGI, it is moving deeper into the system that makes that enemy useful.

Here: open.substack.com/pub/cundil…

1

1

1

91

Jun 15

New FRAGMENTS today: The Freight Recession Has a Price Tag.

I wrote this one because the simple trucking story felt too simple.

Diesel is high. Rates have been weak. Small carriers have been squeezed for years. Some capacity is leaving the market.

That part is known.

The more interesting part is what happened while the industry still looked ugly: buyers kept showing up.

Werner bought FirstFleet. Knight-Swift bought U.S. Xpress. Heartland bought CFI. TFI bought Daseke.

Those deals do not prove the cycle has turned. They do not prove every trucking stock is cheap. But they do give something useful: prices.

Real buyers, writing real checks, for freight assets after several years of pain.

So the question became more interesting than “is trucking good or bad right now?”

The better question is: after the freight recession, what are these assets actually worth?

Maybe this is close to the bottom of the cycle. Maybe it is not. But when strategic buyers are still paying for the assets after the pain, it is worth slowing down and looking at the numbers.

That is what this article does.

Not a diesel article. Not a freight-rate article. Not a recommendation.

A look at what recent trucking deals say about asset values, book value, and one messy public company where the math might still be worth doing: Universal Logistics. $ULH

Here: cundilldeepvalue.substack.co…

1

66

FRAGMENTS Value retweeted

Deep Value Report — Petco Health and Wellness Co. ($WOOF)

Petco is not a buyout rumor.

The stock is around $3, the business still does nearly $6B of annual sales, and the real question is simple: can stabilization become cash after rent, interest, and store investment?

Here:cundilldeepvalue.substack.co…

1

1

1

124

FRAGMENTS Value retweeted

Jun 11

Deep Value Report — Mosaic ($MOS)

At around $20, MOS is not a clean, easy stock.

It is a hard-asset deep value case.

Book value is much higher than the stock price. The company owns real fertilizer infrastructure: Potash, Phosphate, Brazil, Ma’aden, inventory, receivables, plants, terminals, permits, and land.

The problem is not that Mosaic has no assets.

The problem is that Phosphate margins got crushed and the market does not trust how much value will reach shareholders.

That is why we rebuilt the company from the balance sheet up.

Here:cundilldeepvalue.substack.co…

1

1

265

FRAGMENTS Value retweeted

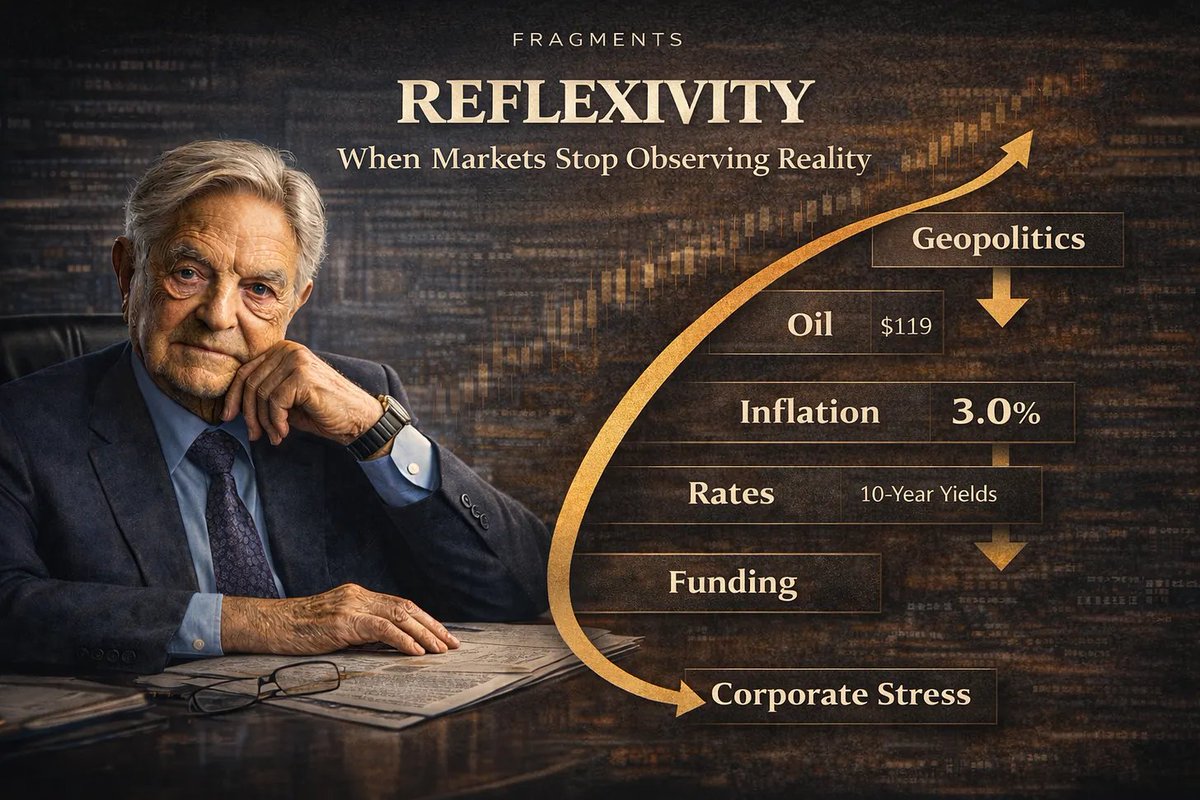

Reflexivity — When Markets Stop Observing Reality and Start Creating It $TSLA

I don’t like using the word reflexivity just to sound smart.

Most of the time, people use it as a fancy way to talk about bubbles. Stock goes up, company raises money, story gets better, stock goes up again. Fine. That version exists.

But I think the more useful version is the one we are seeing now.

A real shock hits the system. In this case: Iran, oil, inflation fear, bonds. Then the market reacts. And the reaction itself starts changing the conditions for everyone else.

Oil does not stay oil.

It becomes inflation expectations. It becomes bond yields. It becomes funding costs. It becomes refinancing pressure. It becomes a different conversation inside companies.

That is the part I wanted to write about.

Not reflexivity as a theory.

Reflexivity as plumbing.

How a geopolitical event travels through markets until it becomes a business problem. How price stops being just information and starts becoming pressure. How deep value stocks can get trapped in negative loops when low prices reduce flexibility, capital access, and time.

The article is really about one question:

when the market reacts to a shock, what does that reaction force everyone else to do next?

Here:cundilldeepvalue.substack.co…

1

1

134

Jun 14

History Rhymes: The Language Before the Break

The article is about the moment before markets admit the regime has changed.

Not the crash.

Not the headline.

The language before it.

“Selective consumer.”

“Waiting for clarity.”

“Refinancing risk.”

“AI power demand.”

“Resilience.”

That is usually where the shift starts.

Read it on FRAGMENTS. $CEG

Here:cundilldeepvalue.substack.co…

29

Jun 14

History Rhymes: The Language Before the Break

Burry, Marks, Klarman, Buffett, Templeton — different investors, different periods, same basic discipline:

they did not need the perfect macro forecast.

They needed price, patience, liquidity, and a balance sheet that gave them time.

Read it on FRAGMENTS. $NVDA

Here:cundilldeepvalue.substack.co…

1

1

77