Scenturion| Cryptocurrency updates| @MGBX_EN| Ambassador| Registration link mgbx.com/register/pwAde1zO

Joined January 2024

- Tweets 5,000

- Following 882

- Followers 139

- Likes 2,943

312 Photos and videos

Pinned Tweet

Jun 11

$IREN investment thesis is based on a simple observation: the infrastructure required for Bitcoin mining shares many characteristics with the infrastructure needed for AI computing.

Jun 11

Pre market looking promising.

1

222

Jun 13

Artificial intelligence has further strengthened $CRWD position. AI can improve threat detection, automate responses, and enhance security operations, making the company's platform more valuable as cyber threats evolve.

Some Quick Facts From the $SPCX Prospectus

Definitions:

1) Falcon 9 is its rocket system that launches satellites, people & cargo into orbit.

2) Falcon Heavy is Falcon 9 with 2 extra rocket boosters for much larger launch capacity.

3) Dragon is its spacecraft that carries people & goods.

4) Starship is its next-gen rocket currently moving from testing to commercial use.

A lot of Launch Segment Firsts:

1) 2008 -- First private company to successfully launch a liquid-fuel rocket into low earth orbit.

2) 2012 -- First private company to guide & dock a spacecraft at the International Space Station

3) 2015 -- First company to use a rocket's own downward thrust to land (propulsive landing)

4) 2017 -- First rocket re-flight

5) 2020 -- First private company to dock astronauts at the International Space Station

Dominant Launch Segment Positioning & Roadmap:

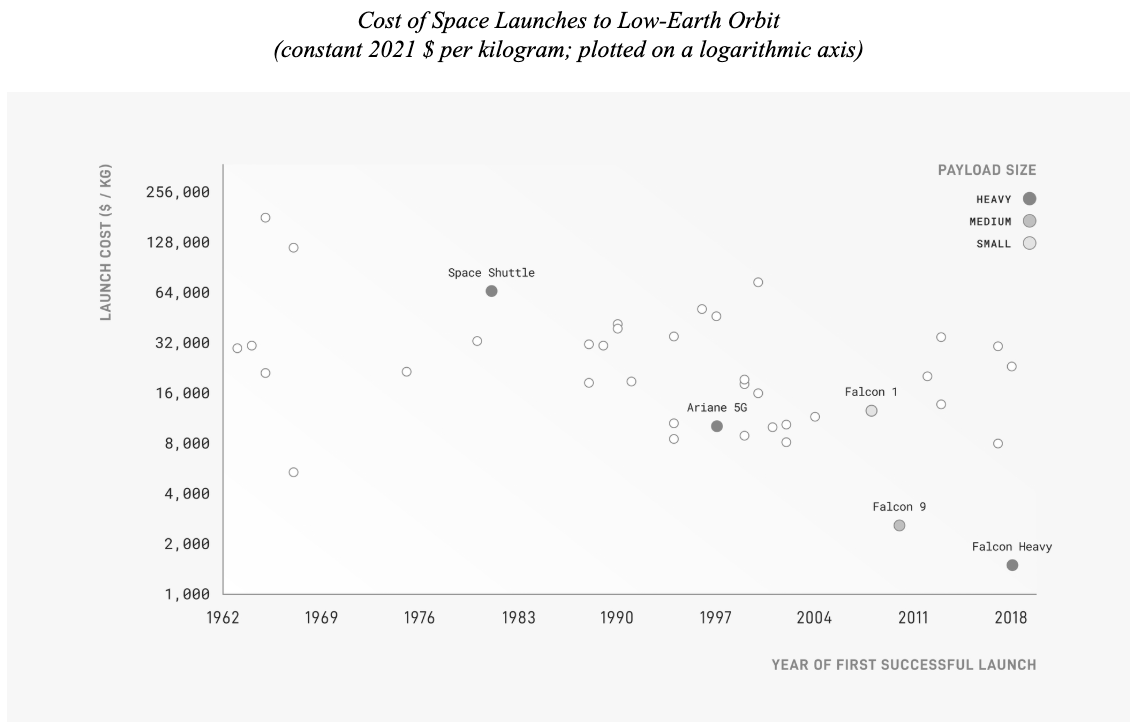

1) Falcon 9 has a 99% mission success rate. This is 85% cheaper per kilogram to launch than average (per NASA). The lead has only grown from there. Falcon Heavy is 92% cheaper per kilogram than the average substitute.

2) Cost edges come from things like the top piece of their rocket (the upper stage) costing SpaceX $5M to build vs. $50M for legacy competition. The power of vertical integration.

3) Falcon 9 Falcon Heavy have an 80% share of global mass to orbit since 2023.

4) Starship is next. This will come with a fully reusable design that can immediately refuel and launch again. Starship can also carry 3x-4x the weight vs. Falcon Heavy in low earth orbit... making it perfect to deploy giant satellites & data centers. They hope this will boost their cost per kilogram lead from 92% with Falcon Heavy to 99% for Starship use cases.

5) They aim to charge $90M/launch on Starship, which is far cheaper than other options.

6) A lot of launch capacity right now is dedicated to Starlink rather than 3P customers. This gives them a lot more flexibility to cater to demand while servicing their own needs. It also means they're not stuck with excess capacity if a partner cancels or delays a launch. They can use it for Starlink.

7) While margins for the segment are pressured due to investments right now, they make more than $67M per launch & it costs them $15M to run it. The unit economics are good & should support healthy long-term margins.

Starlink & Connectivity:

1) 2022 -- First company to build "consumer-grade phased-array terminals." These are flat, stationary satellite dishes that use software to steer radio signals so they can track moving satellites without actually moving themselves. That simplifies design, lowers cost & improves durability.

2) 2025 -- First commercially scaled direct-to-mobile satellite cluster... bypassing the need to connect to cell tower service that is often unavailable.

3) Starlink has grown from just over 2M users in 2023 to 10M in Q1 2026.

4) Extending connectivity to deeply remote areas & using it for mission-critical things like emergency response around the world are resonating (not to mention commercial opportunities with airlines).

5) One thing to keep an eye on is pricing power. They cut pricing from $99 in 2023 to $81 for 2025. It fell from $86 in Q1 2025 to $66 in Q1 2026. While that's not amazing, it was to take advantage of excess capacity already in place & to steal share faster. It's also a byproduct of mix-shift to lower ARPU countries.

6) Starlink has a 63% EBITDA margin.

7) The larger, more distributed low orbit satellite base creates a 95% latency edge vs. the competition due to parking these machines closer to point of consumer connection. Setup is way easier, there are no cancellation fees & customers can easily pause service whenever they want to. Pay when you need to use it.

8) While overall cost for Starlink is a bit higher than some more antiquated solutions, the vastly better performance means cost per megabit is a lot lower.

xAI:

1) Part of SpaceX as of January 31st.

2) Grok has 550M monthly active accounts.

3) These investments are why GAAP EBIT swung from a 2024 gain to a 2025 loss. Connectivity is deeply profitable. Launch Systems aren't losing nearly as much.

4) Floated a $28.5 trillion TAM for this segment.

5) Anthropic will pay SpaceX $1.25B per month for access to compute within its AI segment. That equates to $15B per year for a segment that did just $3.2B in 2025 revenue.

Financials & Valuation:

1) Revenue compounded at a 34% clip from 2023-2025 to reach $18.7B. Q1 2026 revenue 15% Y/Y.

2) -$4.6B in GAAP net income for 2023, $791M for 2024 & then -$4.94B for 2025. Q1 2026 net income was -$4.3B vs. -$528M Y/Y. xAI M&A costs, Starship investments & ongoing compute investments are greatly weighing on margins right now.

3) Space segment revenue rose 8% Y/Y in 2025 to reach $4.09B. GAAP EBIT margin for the segment fell from breakeven to -16% Y/Y. They're front-loading a lot of Starship costs right now.

4) Connectivity segment revenue rose 50% Y/Y in 2025 to reach $11.40B. GAAP EBIT margin impressively moved from 26% to 39% Y/Y.

5) AI segment revenue rose 22% Y/Y in 2025 to reach $3.2B. GAAP EBIT loss worsened from -$1.56B to -$6.36B Y/Y as they aggressively fund future growth.

6) Nearly $16B in cash & equivalents; $29B in long-term debt.

7) $10.1B in Q1 2026 CapEx vs. $4.1B Y/Y. $20.7B in 2025 CapEx vs. $4.4B in 2023.

8) $135/share = a $1.7T valuation. Seeing projections for $23B in 2027 EBITDA. So that's 74x 2027 EBITDA with EBITDA growing around 70% Y/Y at that time if estimates are correct. It looks like it will open well over $135.

Misc. Notes:

1) Only 4% of the share count is being offered at the open. 40% of locked shares unlock after 180 days. The full lockup expiration happens at 365 days.

2) Musk has next-level job security. Activists can't threaten his grip. Ousting him would require a majority vote within class B shares... and he owns most of those class B shares.

2

46

Jun 13

The investment case for $CRWD is compelling because cybersecurity spending is increasingly viewed as essential rather than discretionary

Kind of sort of extremely wild that a single person could end up owning 5 of the most influential companies in history.

Equally wild that this same person posts things like this 😂🙂

1

35

Jun 13

$CRWD CrowdStrike has established itself as one of the most important cybersecurity companies in the world, and its relevance continues growing as digital threats become more sophisticated.

1

32

Jun 13

$VELVET's appeal lies in its exposure to a long-term trend rather than a temporary narrative.

100% of velvet:native protocol-owned liquidity on Base has now been migrated to @AerodromeFi

As the leading DEX on Base, Aerodrome has become the primary trading venue for liquidity, volume, and users across the ecosystem

By consolidating liquidity into a single venue, we aim to provide:

- Deeper liquidity for velvet:native

- Better trading experience

- Lower slippage

- More efficient capital utilization

- Stronger alignment with the Base ecosystem

This migration represents another step in optimizing the velvet:native market structure as trading activity across Velvet continues to grow

1

107

Jun 13

The investment thesis for $VELVET is tied to the professionalization of crypto markets.

Jun 12

The New Home Base of VELVET ✈️

@Velvet_Capital protocol-owned liquidity has migrated from the competition to Aerodrome.

Why? On Aerodrome, protocols can stake liquidity to earn maximally while contributing to the top pools by volume on Base.

Swap & LP $VELVET today.

1

81

Jun 13

$VELVET operates in a segment of the crypto market that often receives less attention than meme coins or AI narratives but may ultimately prove more durable

The World's Highest IQ Holder uses Velvet

(IQ credit: World Memory Championships) @yhbryankimiq

And now we're announcing a trading competition with his project, solana:7XLu71Wvq7zuNU7TP5qjYY8kqg9zxtrsb7sJEEF6pump

900,900 solana:7XLu71Wvq7zuNU7TP5qjYY8kqg9zxtrsb7sJEEF6pump in rewards a 50% Gems boost on all Volume Gems for the pair over the next 3 days

How tokens will be distributed:

- First 100 People to trade $100 of XRPS will receive their share of a pool of 180,180 solana:7XLu71Wvq7zuNU7TP5qjYY8kqg9zxtrsb7sJEEF6pump

- 720,720 solana:7XLu71Wvq7zuNU7TP5qjYY8kqg9zxtrsb7sJEEF6pump will be distributed proportional to trading volume on XRPS

Trade as much XRPS on Solana with Velvet over the next 3 days to maximize your rewards

1

78

Jun 12

The investment case for $CRV is closely linked to the future growth of decentralized finance itself.

1

67

Jun 12

$CRV remains one of the most important assets in decentralized finance because of its connection to Curve Finance, a protocol that has played a foundational role in stablecoin liquidity and on-chain capital efficiency.

1

52

Jun 12

$SKYAI's long-term success will depend on whether it can convert interest into meaningful usage rather than relying solely on the AI narrative.

$SKYAI Perps now live @Bybit_Official

Keep grinding.

1

44

Jun 12

The opportunity for $SKYAI is substantial because the market is still in the early stages of understanding how AI and blockchain may interact.

May 29

AI will stay and grow exponentially.

But most AI companies will go bust. There are just too many.

Even survivors will see huge price fluctuations.

There will be new survivor entrants too.

Same as any other new industry, really.

1

93

Jun 12

$SKYAI sits at the intersection of two of the most powerful themes in modern technology: artificial intelligence and blockchain.

Introducing BNB Hack: AI Trading Agent Edition

For the first time, build smart agents that can strategize and trade while you sleep, using a full stack from BNB Chain, @coinmarketcap & @TrustWallet

• 2 tracks, 3 weeks to build (June 3 to 21)

• $36,000 cash prize pool

• Win API credits, mentorship and ecosystem support

Here's everything you need to know 🧵👇

1

44

Jun 11

If management successfully capitalizes on AI demand while maintaining exposure to Bitcoin, $IREN could emerge as one of the more unique growth stories in the technology sector.

Jun 11

New All In stock tomorrow.

As always subscribers get first access to my trade before i post it to the public.

If you want first access here you go.

x.com/CKCapitalxx/creator-su…

1

196

Jun 11

$IREN is one of the more fascinating transformation stories in the public market.

Jun 11

SpaceX IPOs tomorrow at a $1.75 trillion valuation. $SATS owns more than 2% of SpaceX.

It seems like almost nobody is doing the math on what that is actually worth.

EchoStar swapped a chunk of its wireless spectrum for a stake of more than 2% in SpaceX last September as part of the FCC approved $40 billion deal with SpaceX and AT&T.

At the time SpaceX was valued far below where it is about to list. Tomorrow that stake gets repriced against a $1.75 trillion company.

At that $1.75 trillion price, TD Cowen pegs EchoStar’s SpaceX stake at roughly $31 billion and puts a $155 target on the stock.

But SpaceX is widely expected to trade well above its IPO price.

Run the same math at a $2 trillion valuation and that stake jumps to around $40 billion on its own, which is more than EchoStar’s entire $36 billion market cap today.

You would be getting the SpaceX position alone for more than the whole company is currently worth, with everything else thrown in for free.

And there is a lot else. A $40 billion spectrum sale to AT&T and SpaceX that wipes out the 2026 debt wall everyone was scared of.

Around 5 million satellite TV customers. 2 million Sling subscribers. 7 million Boost Mobile customers. 700,000 broadband customers.

One of the most valuable spectrum portfolios in the country sitting on top of roughly $10 billion in net cash.

The market spent years treating EchoStar as a dying satellite TV company buried in debt. That story is finished.

The spectrum deal cleared the overhang and the SpaceX stake quietly turned this into one of the only ways for public investors to own a real piece of SpaceX.

The honest risk is the roughly $22 billion in debt and the fact that the FCC transfers do not fully close until 2027. This is not a clean bet.

But at $116, with SpaceX about to list and likely run toward $2 trillion, the math points higher. TD Cowen sees $155 even using the conservative number.

SpaceX prices tonight. EchoStar owns 2% of it.

3

202

Jun 11

The primary risk is valuation. $NOW is already recognized as a high-quality growth company, meaning expectations remain elevated.

1

45

Jun 11

Unlike hardware companies that depend on product cycles, $NOW generates predictable subscription revenue while continuously expanding its product offerings.

1

30

Jun 11

While much of the AI conversation focuses on chatbots and generative AI applications, $NOW is focused on something arguably more valuable: integrating AI directly into business workflows.

1

26

Frowler Scent Games retweeted

Jun 10

$1000 for whoever predicts the country that will win the world cup.

This post will be pinned and winners will be picked at the end of the final.

Jun 10

24 hours to go.

12,724

1,040

17,520

1,583,264